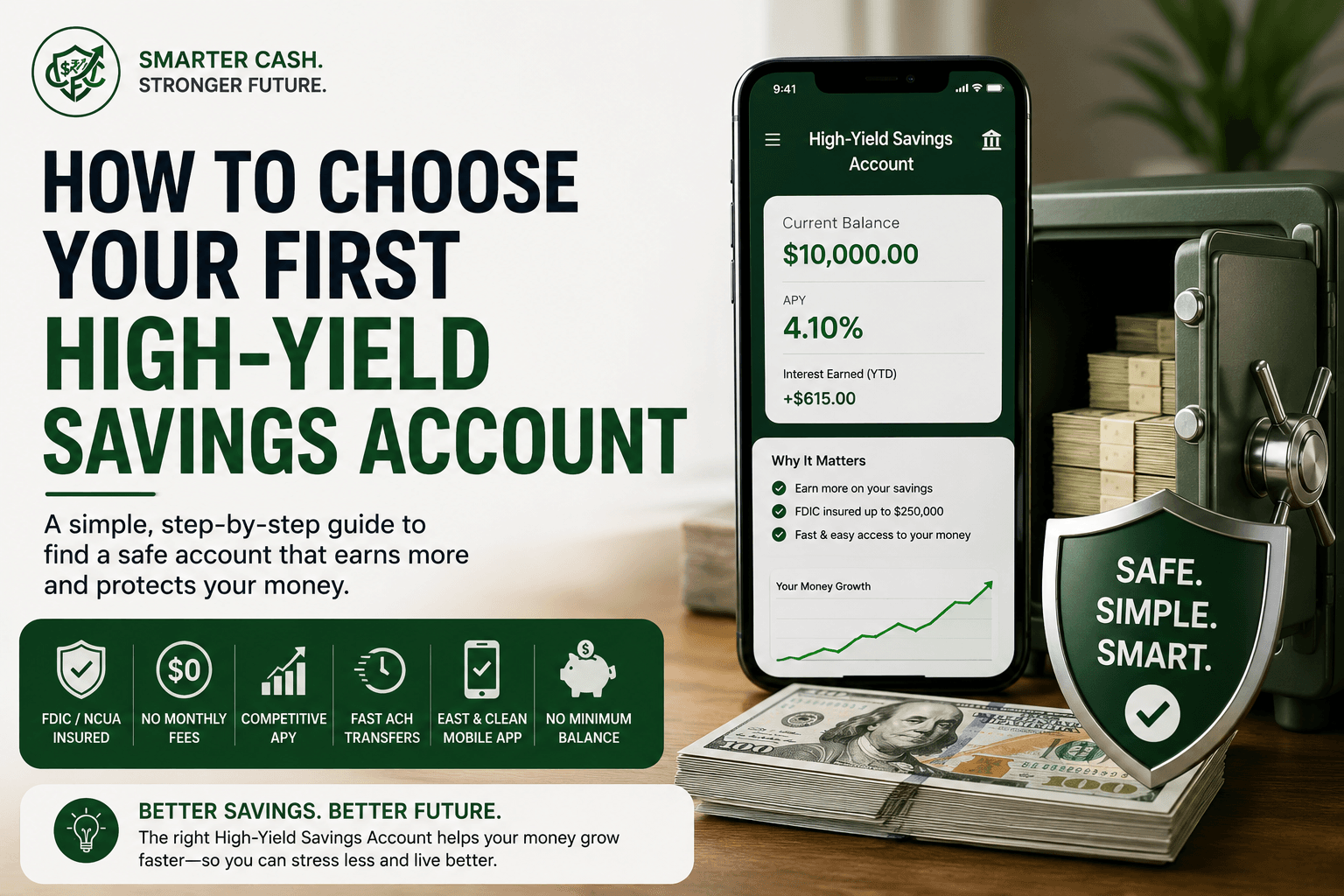

How to Choose Your First High-Yield Savings Account

Selecting a High-Yield Savings Account (HYSA) comes down to verifying four non-negotiable criteria. Learning how to choose your first high-yield savings account is one of the easiest, lowest-risk structural upgrades you can make to your personal cash flow. It requires zero investing knowledge and takes less than fifteen minutes of administrative setup. As of 2026, most competitive high-yield savings accounts offer APYs that far exceed traditional savings accounts, completely shielding your cash from melting away to inflation.

Here is the definitive operational framework to verify bank safety, compare advanced features, and select the perfect high-yield vault for your financial goals.

The Four-Point Checklist to Choose Your First High-Yield Savings Account

To filter out the noise and make a tactical decision, grade every prospective account against this strict four-point framework:

1. The Legal Shield: FDIC or NCUA Insurance

This is the single most critical, non-negotiable step. You must ensure the institution is fully backed by the federal government.

- For Online Banks: Look for the explicit phrase “Member FDIC”.

- For Digital Credit Unions: Look for the explicit phrase “Insured by NCUA”.

This insurance guarantees that if the bank fails or suffers a catastrophic internal collapse, the federal government will reimburse your personal deposits dollar-for-dollar up to $250,000 per depositor, per institution.

How to verify: Do not just take the marketing website’s word for it. Scroll to the very bottom footer of the bank’s homepage. You should see an FDIC or NCUA logo alongside a certificate number. You can verify this number manually using the BankFind Suite (FDIC).

2. True Zero Maintenance Cost

A high interest yield means nothing if the bank reclaims that money through hidden maintenance fees. Your target account must offer:

- $0 Monthly Service Fees.

- $0 Minimum Balance Requirements to maintain the top advertised APY.

- $0 Account Activation Fees.

- $0 Inactivity Fees.

Traditional legacy banks rely heavily on these micro-transactions to generate revenue. You should never have to pay a financial institution a recurring subscription fee to hold your cash.

3. Sustainable APY Performance

Aim for a yield that is significantly higher than the national traditional banking average. However, sustainability matters more than chasing the absolute highest possible interest rate. The top tier of reliable HYSAs typically cluster within a tight range of each other (usually separated by just 0.10% to 0.25%).

Be wary of unverified apps offering exceptionally high yields, as these are often temporary “teaser rates” that disappear after 90 days, or require you to jump through operational hoops like executing twenty debit card transactions a month.

4. Operational Velocity and Liquidity

An emergency fund is only useful if you can access the cash when an emergency actually strikes. Ensure you can clear electronic ACH transfers back to your primary checking account within 1 to 3 business days without punitive withdrawal limits. Top digital banks typically clear outward ACH transfers within 1 to 2 business days.

(If you frequently need check-writing privileges or a dedicated debit card for your savings, you may want to compare a Money Market Account vs High-Yield Savings Account).

At-a-Glance: High-Yield vs. Legacy Banking

| Feature | Premier HYSA Target | Legacy Bank (Avoid) |

| Federal Insurance | Yes (FDIC/NCUA) | Yes |

| Average APY | 4.00%+ | 0.01% – 0.40% |

| Monthly Maintenance Fee | $0 | $5 to $15 |

| Minimum Balance Requirement | $0 | $500 to $5,000+ |

| ACH Transfer Speed | 1–3 Business Days | 1–5 Business Days |

The Core Math: Why the Switch Matters

Traditional checking and savings accounts pay an average interest rate of roughly 0.40% to 0.60% Annual Percentage Yield (APY). Because online-only banks lack the staggering overhead expenses of traditional banks—such as physical commercial real estate leases, teller salaries, and physical security infrastructure—they pass those corporate savings directly to you in the form of elevated interest rates.

Let’s look at a raw comparison of how a $15,000 emergency fund buffer performs over a 12-month timeline (For a deeper breakdown, read our full guide on the High-Yield Savings Account vs Traditional Savings Account):

| Financial Metric After 1 Year | The Legacy Bank Approach | The High-Yield Approach |

| Principal Capital Deposited | $15,000 | $15,000 |

| Advertised Interest Rate (APY) | 0.40% | 4.10% |

| Total Annual Interest Earned | $60.00 | $615.00 |

| Monthly Cash Payout Average | $5.00 | $51.25 |

| Net Opportunity Loss | -$555.00 | $0.00 |

By simply shifting that exact pool of cash to an online HYSA, you pocket an extra $555 in passive return completely risk-free. That is enough to cover an entire utility bill cycle or significantly pad your cash cushion.

Secondary Features: Upgrading Your Banking Experience

Once you have verified the four core non-negotiables above and seen the math, you can use secondary features as a tie-breaker between top-tier institutions.

🪣 Savings Buckets and Sub-Accounts

The best digital banks allow you to digitally partition your single savings account into distinct “buckets” or “envelopes.” Instead of looking at one lump sum of $10,000, you can organize your cash visually:

- Auto Repair Fund: $2,000

- Annual Vacation: $3,000

- Core Emergency Buffer: $5,000This psychological separation prevents you from accidentally spending your emergency fund on a discretionary purchase.

📱 Mobile App Usability and Security

Since an online bank lacks physical branches, the mobile app is your only point of interaction. Check the app store reviews before opening an account. You want an app that offers:

- Biometric Login: FaceID or fingerprint scanning for fast, secure access.

- Multi-Factor Authentication (MFA): Support for authenticator apps (like Authy or Google Authenticator) rather than just SMS text codes.

- Seamless Mobile Check Deposit: The ability to snap a photo of a check and deposit it instantly.

🎧 Customer Support Accessibility

If your account is ever frozen or an ACH transfer goes missing, you need to know someone will pick up the phone. Check the bank’s customer service hours. Premier institutions offer 24/7 phone support with US-based representatives.

3 Common Mistakes When Opening an HYSA

Shifting your cash into a high-yield vehicle is smart, but failing to understand the operational rules of modern digital finance can cause unexpected friction.

1. Falling for the FinTech Wrapper Trap

Many slick apps advertising high-yield returns are Financial Technology (FinTech) platforms, not actual chartered banks. They use software to “sweep” your money into a network of third-party partner banks. While your money is technically safe, if the FinTech platform experiences a technical glitch, your cash can become temporarily locked behind an administrative wall. The Fix: Choose an established, direct online bank that holds its own banking charter to minimize third-party risk.

2. Chasing the Relationship Tier Mirage

Many traditional commercial banks now advertise competitive APYs to prevent customers from leaving. However, these are often “Relationship Rates.” To qualify, you may be required to keep a massive minimum balance of $25,000 and maintain a $5,000 monthly direct deposit. If you miss a requirement, your interest rate automatically collapses back down to a miserable baseline tier.

3. Not Knowing Your Target Balance

Before deciding where to keep your cash, it is highly recommended to review Emergency Fund Basics and figure out how much emergency fund do you really need. Depositing too little leaves you vulnerable to unexpected expenses and debt, while hoarding too much cash prevents you from investing for long-term compound growth.

Not sure what your exact savings target should be? Use our free Advanced Emergency Fund Analyzer to calculate the exact cash buffer you need based on your specific monthly expenses, job stability, and financial goals.

The Tax Implications of High-Yield Interest

A common misconception for beginners is that bank interest is “free money.” It is important to understand the tax architecture of an HYSA.

Interest is Taxable Ordinary Income: The IRS views the interest you earn in your high-yield savings account as standard taxable income. It is taxed at your highest marginal tax bracket. At the end of the tax year, if your account generated more than $10 in interest, your bank is legally required to send you a Form 1099-INT. You must report this amount on your federal tax return.

Even after taxes are deducted, the net gain from an HYSA vastly outperforms leaving the cash to stagnate in a legacy bank.

The Strategic Setup: Automating Your New Account

Once you select your target high-yield savings account, you need to seamlessly plug it into your existing personal finance system. Trying to manage your cash flow manually every month is a guaranteed recipe for failure. (Wondering how to split your funds? See How Much Should You Keep in Checking vs Savings?).

Step 1: The Small Micro-Deposit Verification

When you open your new online account, you will link it to your existing everyday checking account. The platform will execute one or two tiny micro-deposits (usually small amounts like $0.12 and $0.07) to verify the connection.

Step 2: Set Up an Automated Push

You have two automated options to build your wealth effortlessly:

- The Direct Deposit Split: Ask your employer’s payroll department to split your upcoming paycheck. Instruct them to route a percentage of your take-home pay to your traditional checking account for bills, and direct the remaining amount straight into your new HYSA. (Step-by-step tutorial: How to Automate Savings Using Split Direct Deposit).

- The Automated Pull Transfer: Schedule a fixed recurring transfer inside your new high-yield portal to execute automatically on a specific day of the month.

Before Opening the Account Checklist

Ready to pull the trigger? Before clicking “Open Account” on a bank’s website, verify these final details to ensure you are getting a premier product:

✔ FDIC or NCUA Insured (Check the website footer for the certificate)

✔ $0 Monthly Maintenance Fee

✔ Competitive APY (Above 4.00% as of 2026)

✔ No Minimum Balance (To earn the stated APY)

✔ ACH Transfer Speed (1 to 3 business days)

✔ Mobile App Reviews (Checked the iOS/Android App Store)

✔ Customer Support Availability (Clear phone number or live chat options)

Frequently Asked Questions (FAQs)

1. Is an online high-yield savings account as safe as a traditional bank branch?

Yes, absolutely. From a structural safety standpoint, an online bank with a verified FDIC certificate is legally identical to a multi-billion-dollar brick-and-mortar bank down the street. The federal government backs your deposits up to $250,000 in both locations.

2. Are high-yield savings account rates guaranteed?

No. All high-yield savings account rates are variable. The APY you receive is directly tied to macroeconomics and the benchmark federal funds rate. If the Federal Reserve cuts interest rates to stimulate the economy, your rate will drop. (If you want a guaranteed rate for a fixed period of time, check out our guide on High-Yield Savings Account vs CD: Which Is Better?).

3. How many times can I withdraw money from my HYSA every month?

Historically, federal regulations (Regulation D) strictly limited consumers to six convenient withdrawals per month. While the federal government has indefinitely paused the enforcement of this rule, many individual banks still maintain an internal cap of six withdrawals per statement cycle. Treat your HYSA as a long-term storage facility, not a daily spending account.

4. Can I open an HYSA if I have a low credit score?

Yes. When you apply to open a savings account, banks screen your banking history through ChexSystems rather than running a credit check. They strictly look for unpaid bank fees or fraudulent behavior. A low credit score will not stop you from opening an account.

5. How long does it actually take to transfer my money out in an emergency?

Standard ACH transfers take 1 to 3 business days to clear and arrive in your external checking account. However, many premier online banks now offer complimentary ATM cards, allowing you to withdraw physical cash instantly if needed.

Trusted Banking & Savings Resources

- Federal Deposit Insurance Corporation (FDIC) – Verify whether a bank is FDIC-insured, understand deposit insurance limits, and learn how your savings are protected.

- National Credit Union Administration (NCUA) – Learn how federally insured credit unions protect deposits through NCUA share insurance.

- Consumer Financial Protection Bureau (CFPB) – Explore guidance on choosing and managing checking and savings accounts, avoiding unnecessary fees, and understanding banking services.

- MyMoney.gov – U.S. government financial education covering saving strategies, emergency funds, budgeting, and financial planning.

- BankFind Suite (FDIC) – Search for FDIC-insured banks and verify a financial institution before opening an account.

Disclaimer: The information provided on Clarity Flow Core is for educational and informational purposes only and should not be construed as professional financial, tax, or legal advice. Interest rates (APYs) and account terms are subject to change by financial institutions at any time. Always conduct your own research or consult with a certified financial planner before making major financial decisions. For more details, please review our full Disclaimer.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.