How to Increase Your Credit Limit Without Hurting Your Credit Score

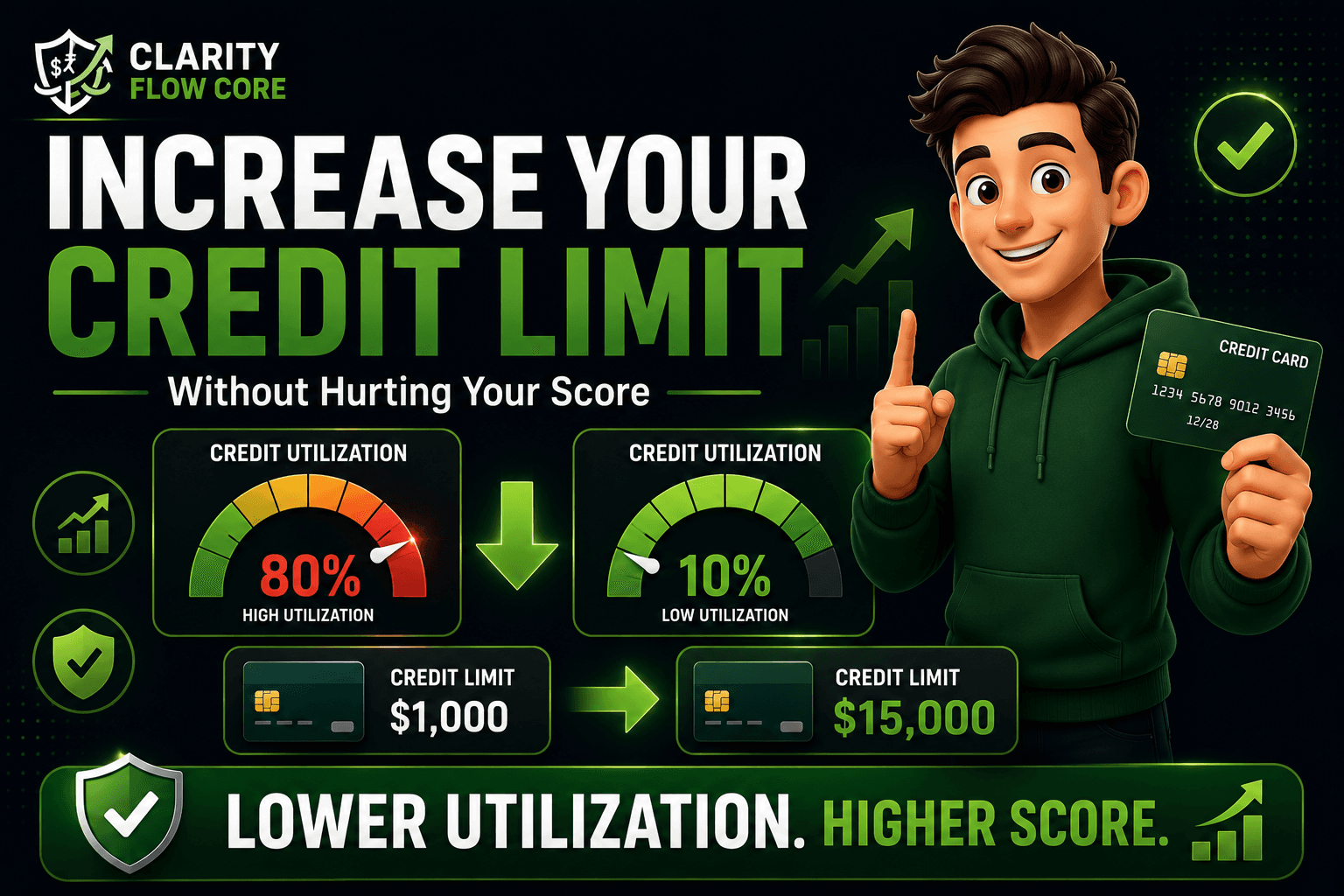

You just booked a flight, bought groceries, and paid your cell phone bill. You have the cash sitting in your checking account, ready to pay off your credit card completely. But when you log into your banking app, you notice a massive problem: your credit utilization has spiked to 80% because your card only has a restrictive $1,000 credit limit.

A low credit limit is a financial chokehold. It forces you to micromanage your purchases, make multiple payments a month just to free up space, and constantly worry about accidental score drops.

The obvious solution is to ask your bank for more credit. But this is where the fear sets in. Financial forums and well-meaning family members often warn that asking for a higher limit will trigger a “hard inquiry,” damaging your credit score just when you are trying to build it.

You do not have to rely on rumors. Getting a higher credit line is a standard banking procedure driven entirely by math and risk algorithms. If you know how the system works, you can secure a massive bump to your purchasing power without sacrificing a single point on your credit report.

In this comprehensive guide, we will break down exactly how to increase your credit limit safely, explain the critical difference between hard and soft pulls, and give you the exact strategies to force the bank to say yes.

⚡ Quick Answer

The safest way to increase your credit limit without hurting your score is to request an increase through your bank’s online portal or mobile app, specifically looking for language that indicates a “soft pull” or “no impact to your credit score.” If you keep your credit utilization low, pay your bills on time for at least six straight months, and proactively update your income in your profile, many major banks (like Amex, Capital One, and Discover) will grant increases with zero negative impact on your FICO score.

To understand exactly what is at stake when you hit the “Request Increase” button, here is a breakdown of the two ways banks check your profile:

| Inquiry Type | Score Impact | Visibility to Others | Typical Bank Action | Best Strategy |

| Soft Pull (Soft Inquiry) | Zero impact. Your score stays exactly the same. | Only you can see it on your report. | App-based automated requests, routine account reviews. | Always prioritize. Update your income online to trigger these naturally. |

| Hard Pull (Hard Inquiry) | Drops score by 3 to 5 points temporarily. | Visible to all future lenders for 2 years. | Calling a representative, asking for massive limit jumps. | Avoid if possible. Only accept a hard pull if you urgently need the space. |

Why You Should Increase Your Credit Limit (The Hidden Math)

Many consumers believe that having a high credit limit is a bad thing because it invites the temptation of massive debt. If you lack financial discipline, that is absolutely true. But if you treat your credit card like a debit card and pay your balance in full every month, a high credit limit is one of the most powerful tools for manipulating your FICO score upward.

This all comes down to Credit Utilization.

Credit utilization accounts for 30% of your total FICO score. It is the ratio of how much debt you currently owe compared to how much credit you have available. The mathematical rule of the industry is that your utilization should never exceed 30%, and ideally, it should sit below 10%.

Let’s Run the Math

Imagine you put all your monthly living expenses on a credit card to earn points. You spend $1,500 a month.

- Scenario A (Low Limit): Your credit limit is $2,000. Because you spent $1,500, your credit utilization is an alarming 75%. The credit bureaus view you as financially distressed and a high risk of defaulting. Your score plummets, even if you pay the bill off completely at the end of the month.

- Scenario B (High Limit): You successfully requested an increase, and your new limit is $15,000. You still spend the exact same $1,500 a month. Your utilization instantly drops to 10%. The credit bureaus view you as highly responsible with abundant cash flow. Your score skyrockets.

In Scenario B, you did not change your spending habits. You did not pay off debt faster. You simply manipulated the math in your favor by expanding the denominator of the equation.

To see exactly how much a higher limit will drop your utilization and boost your specific profile, run your current numbers through our Credit Utilization Calculator & Recovery System.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationHow to Increase Your Credit Limit Safely (Exact Steps)

There are three primary strategies to get the bank to extend your purchasing power. We will rank them from the safest (zero risk) to the most aggressive.

Strategy 1: The Automatic Increase (The Patience Play)

The absolute safest way to get a higher limit is to let the bank do the work for you. Most major credit card issuers conduct automated account reviews every 6 to 12 months.

During these automated reviews, their algorithms check your payment history and your spending volume. If you are consistently maxing out a $1,000 card but paying it off in full multiple times a month, the algorithm realizes it is losing out on transaction fees (swipe fees) because your limit is artificially restricting your spending. They will often automatically bump your limit to $2,000 or $3,000 and notify you via email. This is always a soft pull and never hurts your score.

Strategy 2: Proactive Online Income Updates (The App Strategy)

Banks cannot increase your credit line if they think you are broke. When you first applied for your starter credit card, you told them your income. If three years have passed, you have likely received raises, changed jobs, or started a side hustle.

Log into your credit card’s mobile app or desktop portal and find the “Profile” or “Account Settings” tab. Look for an option to “Update Income.” By officially raising your stated income in their system, you frequently trigger an immediate, automated soft-pull credit limit increase.

Strategy 3: The Manual Online Request

If patience and income updates do not work, you must ask directly. Nearly all modern credit card portals have a dedicated button labeled “Request Credit Limit Increase.”

This is where you must read the fine print. Before you click submit, the bank must legally disclose how they will check your credit. Look closely at the text above the submit button.

- If it says: “Requesting an increase will not impact your credit score,” you are safe. This is a soft pull.

- If it says: “By clicking submit, you authorize us to pull a copy of your credit report,” stop immediately. That legal phrasing almost always indicates a hard pull.

If you are unsure how this move will shift your overall profile, model the scenario first using the Credit Score Simulator & Improvement Planner.

Test Your Credit Score Before Making Big Moves

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our simulator.

Launch Credit SimulatorThe Hard Pull vs. Soft Pull Trap: Bank-by-Bank Breakdown

Not all banks treat your request equally. Some are notoriously generous and rely entirely on soft pulls, while others are incredibly strict and will ding your credit report just for asking. While internal bank policies can shift, here is the current landscape of how the major US issuers handle requests:

The “Soft Pull” Friendly Banks

These issuers generally allow you to request a higher limit via their app or website using only a soft inquiry. Your score is safe here.

- American Express: Amex is famous for its generosity. They often allow users to ask for a “3X Increase” (triple your current limit) after 61 days of account opening using only a soft pull.

- Discover: Discover has a dedicated, easy-to-use button in their app. They will run a soft pull and give you an instant decision. If they cannot approve you with a soft pull, they will explicitly stop and ask your permission before doing a hard pull.

- Capital One: Capital One relies almost exclusively on soft pulls for limit increases. However, their algorithm is heavily tied to your usage. If you do not actively use your Capital One card, they will deny the request, citing “insufficient use of current credit line.”

- Citi: Citi allows soft pull requests through their portal. Like Discover, they are usually transparent and will ask for formal consent if they require a hard pull to proceed.

The “Proceed with Caution” Banks

- Chase: Historically, Chase required a hard inquiry for any customer-initiated credit limit increase. This terrified point optimizers. However, Chase has recently updated their app to include a “Request Increase” feature that utilizes a soft pull. If you call a Chase representative on the phone to ask for an increase, explicitly ask them: “Will this require a hard pull?” before proceeding.

- Wells Fargo: Depending on your account history and the specific card, Wells Fargo can be a mixed bag. Always request online first to try and trigger the soft pull algorithm before calling a human representative.

What Counts as “Income” When Asking for an Increase?

When you fill out the request form, the bank will ask for your Total Gross Annual Income. A massive mistake beginners make is drastically underreporting the money they have access to.

Under the CARD Act, if you are 21 or older, you are legally allowed to include any income to which you have a reasonable expectation of access. You do not just have to list your base salary. You can legally and ethically include:

- Your spouse or partner’s income (if you share expenses or bank accounts).

- Consistent freelance or side-hustle revenue.

- Court-ordered alimony or child support (though you are not required to disclose this if you do not want to).

- Social Security benefits, pensions, or retirement distributions.

- Trust fund payouts or regular allowances from family members.

If you earn $50,000, but your spouse earns $70,000, and you share finances, you should be putting $120,000 in the income box. This dramatically lowers your Debt-to-Income (DTI) ratio in the bank’s eyes, drastically increasing your odds of approval.

Ensure you actually know your total household numbers by organizing your cash flow in the Financial Freedom Planner.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanCommon Mistakes When Requesting a Higher Limit

Even if you find a soft-pull button, you can still face rejection or trigger unwanted scrutiny if you mishandle the request. Avoid these common traps:

Mistake 1: Asking Too Soon

If you just opened a credit card, do not ask for a higher limit next week. Banks want to establish a pattern of behavior. The absolute minimum waiting period is generally 60 to 90 days (the Amex 61-day rule being a famous exception). For most traditional banks, you should wait a full 6 months before asking for an expansion.

Mistake 2: Lying About Your Income

While you should include all accessible household income, you must never fabricate numbers. Falsifying your income on a credit application is bank fraud. While banks rarely ask for W-2s for a simple limit increase, if you trigger a “Financial Review” by claiming you make $400,000 as a 20-year-old student, the bank will freeze all your accounts and demand tax transcripts from the IRS. If you cannot provide them, they will permanently close your accounts.

Mistake 3: Carrying a Massive Revolving Balance

Banks give credit to people who prove they do not desperately need it. If your current $5,000 credit limit is maxed out, and you are only making the $35 minimum monthly payments, asking for more credit is a massive red flag. The bank’s risk algorithm will view you as financially desperate and spiraling into debt.

Before you ask for an increase, you must aggressively pay down your existing balances. If your debt load is overwhelming, pause your credit limit strategies and run your numbers through our Debt-to-Income Analyzer & Loan Readiness Planner to build a structured payoff map.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI RatioMistake 4: Requesting After a Job Loss

If you recently lost your job and want to increase your credit limit as a makeshift emergency fund, you are walking into a trap. First, updating your income to zero will guarantee a denial. Second, relying on high-interest credit cards for survival is financially devastating.

Credit limits can be slashed by the bank at any time. You cannot rely on them. You must build cash reserves. If you are behind on this step, pivot immediately to the Advanced Emergency Fund Analyzer to secure your baseline.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetWhat to Do If Your Credit Limit Increase Is Denied

Seeing a denial notice can be discouraging, but unlike a full card application rejection, a soft-pull credit limit denial does no damage to your credit report.

By law, the bank must send you an “Adverse Action Notice” (usually via mail or secure digital inbox) explaining exactly why they said no. Do not throw this letter away. It is an invaluable diagnostic tool for your financial health.

Common reasons for denial include:

- “Insufficient experience at current credit line:” You haven’t had the card long enough, or you haven’t been spending enough on it for the bank to justify taking on more risk.

- “Recent late payments:” You have a delinquency on your report. You need 12 to 24 months of perfect payment history to wash this away.

- “Overall utilization across all accounts is too high:” Even if you pay this specific bank perfectly, they pulled your overall credit report and saw you are maxed out on cards from other banks. You are viewed as an overarching credit risk.

If you are denied, do not immediately apply for a new card in frustration. Read the letter, fix the specific behavioral issue they highlighted, wait exactly six months, and submit the request again.

The Concept of “Balance Chasing” (A Warning)

There is a rare but dangerous scenario you must be aware of when asking for a credit limit increase while carrying high debt. It is called “Balance Chasing.”

If you have a $10,000 limit, and you owe $9,500, you might think asking for a $15,000 limit will lower your utilization and fix your score. However, when you click request, the bank runs a soft pull and realizes your financial situation has deteriorated since they first issued the card.

Instead of granting the increase, the algorithm panics. To limit their exposure, the bank might actually lower your credit limit to match your current balance. If you pay down $1,000, they lower the limit by $1,000, literally chasing your balance down to close the account out safely.

Never ask for a credit limit increase to hide from a debt crisis. Only ask from a position of strength—when your balances are low and your payments are on time.

Action Plan: Secure Your Increase Today

Stop micromanaging your purchases and secure the financial breathing room you deserve. Follow this exact operational plan today:

- Audit Your Income: Calculate your total, legal, household gross income. Include side hustles and a partner’s salary if finances are shared.

- Pay Down the Balance: If you are currently carrying a high balance on the target card, pay it down as much as possible and wait for the statement to close before proceeding.

- Log In and Update: Open your banking app, navigate to your profile, and formally update your income and housing payment data.

- Locate the Request Button: Navigate to the “Services” or “Account Management” tab and select “Request Credit Limit Increase.”

- Verify the Pull Type: Read the disclosure text carefully. Ensure it explicitly states the request will not impact your credit score.

- Submit: If approved, your new limit is available instantly, and your credit utilization will drop on your very next statement cycle.

Frequently Asked Questions

Will asking for a credit limit increase drop my credit score?

It depends entirely on how the bank processes the request. If the bank uses a “soft pull,” your score will not change at all. If the bank uses a “hard pull,” your score will temporarily drop by roughly 3 to 5 points. You should always aim for soft pull increases by utilizing your bank’s online portal and reading the disclosures carefully.

How much of an increase should I ask for?

If the bank’s portal asks you to input a requested amount, a good rule of thumb is to ask for a 25% to 50% increase over your current limit. For example, if your limit is $4,000, asking for $6,000 is reasonable. Asking to jump from $4,000 to $20,000 overnight will likely trigger an automatic denial or a request for manual income verification.

How often can I ask for a credit limit increase?

The industry standard is to wait at least six months between requests. If you ask more frequently than every six months, the bank’s system will usually auto-deny you simply for the timing, regardless of how good your credit score is.

Does a higher credit limit mean I have to spend more?

Absolutely not. Your credit limit is a safety net and a mathematical tool to keep your utilization low. You should continue to spend exactly what your monthly budget allows. Treating a limit increase as “free money” is a rapid path to debilitating consumer debt.

Should I just open a new credit card instead?

Opening a new credit card will indeed increase your total available credit, which lowers your overall utilization. However, a new card application always requires a hard pull, and a brand-new account will lower the “Average Age of Accounts” on your credit report, which can drop your score. If you only want the limit increase to lower your utilization, asking your current bank for a soft-pull increase is vastly superior.

Can I transfer my credit limit from one card to another?

Yes, but only within the same bank. If you have two credit cards with Chase or American Express, you can usually call a customer service representative and ask them to shift a portion of your limit from a card you rarely use to your primary everyday card. This is almost always a soft pull because the bank is not extending you any new total credit; they are just rearranging it.

References and Resources

To ensure you are operating with the most accurate, up-to-date consumer rights information, we highly recommend verifying credit reporting rules directly with the agencies that enforce them:

- Consumer Financial Protection Bureau (CFPB): The CFPB offers exceptional, plain-language guides on how credit utilization works and how to dispute errors if a bank unfairly reports a hard inquiry. Visit the CFPB guide on credit reports.

- FICO: Because FICO is the algorithm used by 90% of top lenders, understanding their official stance on credit utilization and hard inquiries is mandatory. Review the official FICO score factors.

- Federal Trade Commission (FTC): The FTC provides robust advice on consumer credit basics, avoiding debt traps, and your rights under the Fair Credit Reporting Act. Explore Consumer.gov credit basics.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.