How Much Down Payment Do You Really Need to Buy a House?

If you are thinking about buying a home, you have probably spent some time looking at real estate listings online. And if you have looked at real estate listings recently, you have likely experienced a moment of sheer financial panic.

For decades, traditional financial advice has repeated the exact same rule: You must save a 20% down payment before buying a house. In 1990, when the median home price in the US was roughly $120,000, saving 20% ($24,000) was a challenging but achievable goal for a dual-income household. Today, with median home prices pushing well past $400,000 in many markets, saving a 20% down payment means scraping together $80,000 to $100,000 in cash. For the average renter, saving that amount of money feels mathematically impossible.

Here is the truth: The 20% down payment rule is a myth. It is outdated, it is inaccurate, and believing it is the primary reason thousands of qualified buyers stay trapped in the renting cycle for years longer than necessary.

In this comprehensive guide, we are going to break down exactly how much cash you actually need to buy a house in today’s market. We will explore the minimum requirements for different loan types, run the real-world math on how a smaller down payment affects your monthly budget, and show you how to accurately calculate your true home buying readiness.

Quick Answer: How much down payment do you really need?

You do not need 20% down to buy a house. First-time home buyers can secure a Conventional mortgage with as little as 3% down, or an FHA loan with 3.5% down. Eligible veterans and rural buyers can even buy a home with 0% down. While putting down less than 20% means you will pay a monthly fee for Private Mortgage Insurance (PMI), it allows you to enter the housing market years earlier.

Down Payment Minimums by Loan Type

The exact percentage you are required to put down depends entirely on the type of mortgage you apply for. Here are the absolute minimum down payments required by the major loan programs in 2026:

| Mortgage Type | Minimum Down Payment | Minimum Credit Score Required | Best For |

| Conventional Loan | 3% (for first-time buyers) | 620 | Buyers with good to excellent credit. |

| FHA Loan | 3.5% | 580 | Buyers with average credit or higher debt. |

| VA Loan | 0% | Varies (often 620+) | Active-duty military and eligible veterans. |

| USDA Loan | 0% | 640 | Low-to-moderate income buyers in rural areas. |

Note: If you are not a first-time home buyer (meaning you have owned a home in the last three years), the minimum down payment for a Conventional loan is typically 5%.

Why the 20% Myth Refuses to Die

If you only need 3% to buy a house, why do financial gurus and older relatives constantly insist you need 20%?

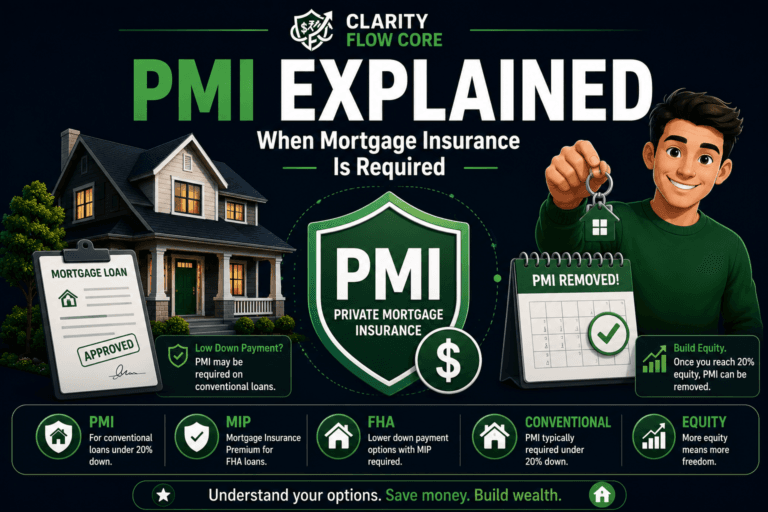

The answer is Private Mortgage Insurance (PMI).

When you borrow hundreds of thousands of dollars to buy a house, the lender is taking on a massive amount of risk. If you lose your job and stop paying your mortgage, the bank has to go through the expensive process of foreclosing on the home and selling it to recoup their money.

Lenders have determined that if a buyer has at least 20% of their own cash invested in the property (equity), they are highly unlikely to walk away from the loan. Therefore, 20% is the “safe” threshold.

If you put down less than 20%, the lender views you as a higher risk. To protect themselves, they force you to purchase a PMI policy. PMI protects the lender if you default, but you have to pay the monthly premium.

Why Saving 20% Can Actually Hurt You

Older financial advice says that PMI is a “waste of money” and you should save 20% to avoid it. In a rapidly appreciating housing market, this advice is often financially destructive.

Let’s say you want to buy a $350,000 house. You currently have $10,500 saved (3%).

- To reach 20% ($70,000), you need to save an additional $59,500.

- If you save an aggressive $1,000 a month, it will take you 5 years to reach 20%.

What happens to that $350,000 house in 5 years? If home values appreciate at a modest 4% per year, that same house will cost over $425,000 by the time you finish saving. Your target moved.

Paying a $120 monthly PMI fee for a few years is often vastly cheaper than trying to out-save a rising housing market.

Real Dollar Math: How Much Down Payment Do You Really Need?

To see how this actually plays out, let’s look at a concrete example.

Imagine you are buying a $350,000 home with a 30-year fixed-rate mortgage at a 6.5% interest rate. (For this example, we will assume roughly $300/month for property taxes and $100/month for homeowners insurance).

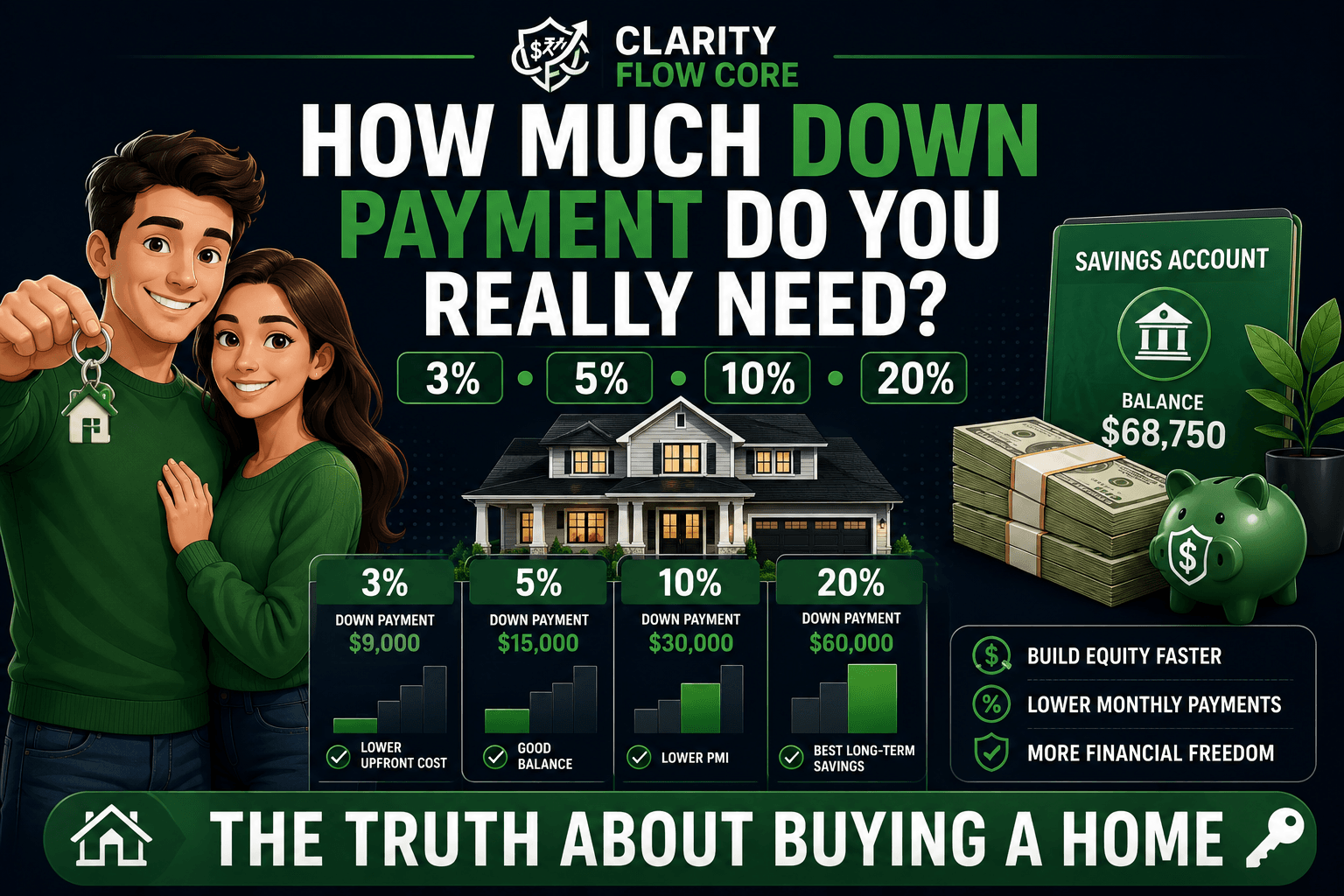

| Down Payment % | Cash Required | Estimated Monthly PMI | Estimated Total Monthly Payment |

| 3% Down | $10,500 | ~$140 | $2,685 |

| 5% Down | $17,500 | ~$125 | $2,625 |

| 10% Down | $35,000 | ~$90 | $2,480 |

| 20% Down | $70,000 | $0 | $2,170 |

As you can see, jumping from a 3% down payment to a 5% down payment requires you to bring an extra $7,000 in cash to the closing table, but it only lowers your monthly payment by about $60.

While a larger down payment can reduce your monthly payment, it’s equally important to ensure your total housing costs fit comfortably within your income. Read How Much of Your Income Should Go Toward Housing Costs? to learn how much of your paycheck should realistically be dedicated to homeownership.

For many buyers, keeping that $7,000 safely in their bank account to cover home repairs or emergencies is much smarter than tying it up in the house to save $60 a month.

Free Tool: Debt-to-Income (DTI) Analyzer

Stop guessing what the bank thinks. Calculate your exact DTI ratio instantly and find out your true loan readiness and maximum borrowing power.

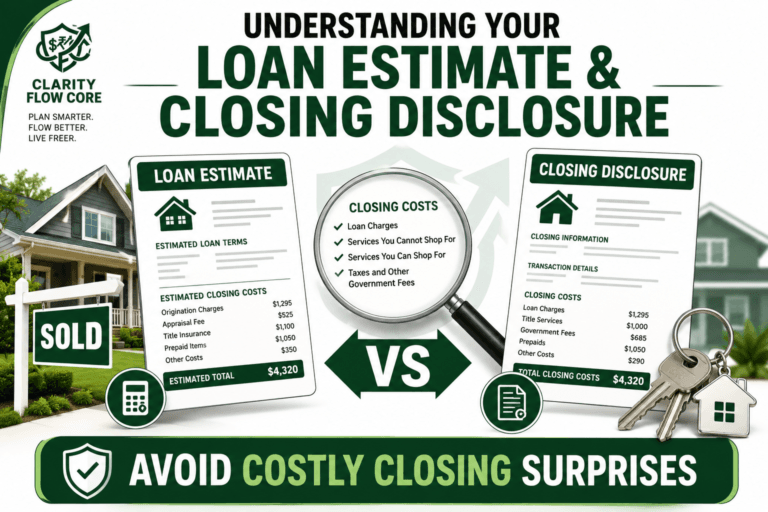

The Hidden Cash Requirements (It Isn’t Just the Down Payment)

This is where thousands of first-time buyers get their hearts broken. They use an online calculator, realize they need $10,500 for a 3% down payment, save exactly $10,500, and go to apply for a loan.

They are immediately denied because they forgot about Closing Costs.

Your down payment is just the equity you are putting into the home. Closing costs are the administrative, legal, and government fees required to actually process the transaction. You must pay for the appraiser, the title search, the loan origination, and prepay your property taxes and homeowners insurance.

Closing costs generally range from 2% to 5% of your total loan amount.

If you are buying that $350,000 house with 3% down ($10,500), your closing costs will likely add another $8,000 to $12,000 to your bill. You actually need closer to $20,000 in cash to finalize the purchase.

The same principle applies before moving into your own place for the first time. Beyond rent or a down payment, you’ll also need money for deposits, moving expenses, and an emergency cushion. Read How Much Should You Save Before Moving Out on Your Own? to estimate a realistic savings goal before making the transition.

(Want a complete breakdown of exactly who gets this money? Read our deep-dive guide: Closing Costs Explained: What Home Buyers Actually Pay).

Pros and Cons of a Small Down Payment (3% to 5%)

Should you use a low-down-payment program? It depends entirely on your cash flow and financial discipline.

The Pros:

- Faster Entry: You can stop renting and start building equity years earlier.

- Preserves Cash: By putting down the minimum, you keep a larger cash cushion in your bank account to handle emergency home repairs, job loss, or medical bills.

- Higher Return on Investment (ROI): Because you have less of your own cash tied up in the asset, any appreciation on the home represents a higher percentage return on your initial cash investment.

The Cons:

- You Must Pay PMI: You will have an added monthly expense (PMI) until you reach 20% equity in the home.

- Higher Monthly Payments: Because you are borrowing a larger total amount, your principal and interest payments will be higher.

- Risk of Negative Equity: If the housing market dips right after you buy, owing 97% of the home’s value means you could easily end up “underwater” (owing more than the house is worth), making it very difficult to sell the home if you need to move quickly.

Common Mistakes Beginners Make With Down Payments

The home buying process is emotional and complex. Avoid these massive financial traps:

1. Draining Your Savings to Zero

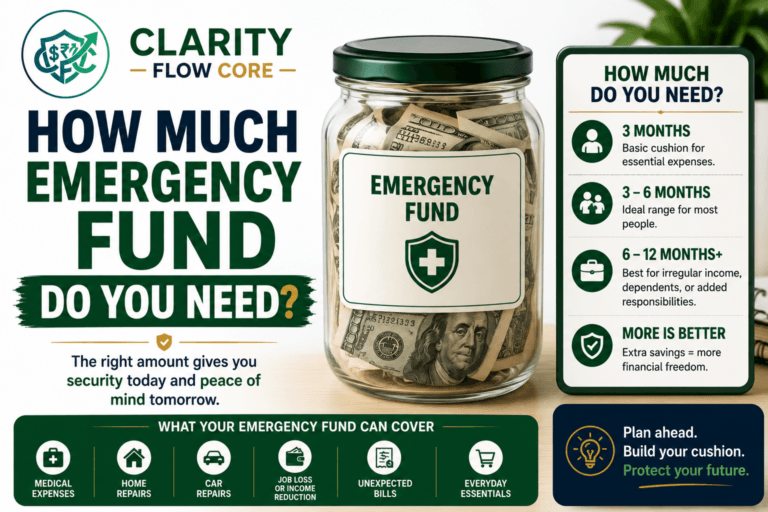

This is the most dangerous mistake a buyer can make. Do not put every single dollar you have into your down payment just to reach 20% or to lower your monthly payment. Once you own a house, the landlord no longer fixes the water heater or replaces the roof. If you have no cash left over after closing day, the first minor repair will force you into high-interest credit card debt. Always maintain an emergency fund. Run your post-purchase budget through our Advanced Emergency Fund Analyzer to ensure you are safe.

2. Assuming FHA is the Only Option for Low Down Payments

Many buyers think FHA loans are the only way to get a low down payment. If you have good credit (680+), a 3% down Conventional loan is often a much better deal. FHA loans charge a 1.75% upfront mortgage insurance fee and have stricter property appraisals. Compare both options by reading our guide: FHA Loan Requirements in 2026.

3. Ignoring Your Debt-to-Income (DTI) Ratio

As mentioned above, you might have a massive down payment saved, but if your monthly debts are too high, the bank will still deny you. Always check your DTI early in the process so you have time to pay off smaller debts before the bank runs your numbers.

Your Action Plan: What to Do Next

If you want to buy a house, you need to transition from guessing to planning. Follow these exact steps to build your roadmap:

- Check Your Credit Score: Pull your official FICO scores. Your score dictates which loan programs you qualify for and how much your PMI will cost. If you need to boost it, use our Credit Score Simulator & Improvement Planner.

Test Your Credit Score Before Making Big Moves

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our simulator.

Launch Credit Simulator- Determine Your Target House Price: Look at recent sales in your desired neighborhood to find a realistic baseline price. Alternatively, use our Mortgage Affordability Calculator to see what price range fits your current income.

How Much House Can You Actually Afford?

Stop guessing your home buying budget. Instantly calculate your realistic price range, estimated monthly payments, and overall loan readiness based on your current income and debts.

Calculate My Buying Power- Use the 8% Rule: Add 3% for a minimum down payment and an estimated 5% for closing costs. Multiply your target house price by 0.08. That is roughly the absolute minimum amount of cash you need saved to buy that home.

Example: The 8% Rule on a $400,000 House

- 3% down = $12,000

- 3–5% closing costs = $12,000–$20,000

- Expected cash needed: $24,000–$32,000

- Automate Your Savings: Do not rely on willpower. Set up an automatic transfer from your checking account to a high-yield savings account the day after you get paid. Name the account “House Fund” and do not touch it.

Frequently Asked Questions (FAQ)

1. Can I buy a house with less than 3% down?

Yes. Certain VA and USDA loans allow qualified buyers to purchase homes with no down payment. Some state and local assistance programs may also provide grants that effectively reduce your required cash contribution.

2. Can I use gift money for my down payment?

Yes. For most Conventional and FHA loans, you can use gift money from a family member to cover 100% of your down payment. However, the family member must sign an official “gift letter” legally stating that the money is a true gift and not a secret loan that you have to pay back.

3. Are there programs for first-time home buyers?

Yes, almost every state and many large cities offer Down Payment Assistance (DPA) programs for first-time buyers. These programs offer grants or 0% interest forgivable loans to help cover your down payment and closing costs. You must usually meet specific income limits to qualify. Search your state’s housing finance agency website for details.

4. Do I have to pay PMI forever?

If you use a Conventional loan, PMI is not permanent. Once you reach 20% equity in the home (either by paying down the loan balance or because the home’s value has increased significantly), you can contact your lender and request that the PMI be removed. Warning: If you use an FHA loan and put down less than 10%, your mortgage insurance (MIP) is permanent for the life of the loan.

5. Does paying a 20% down payment guarantee a lower interest rate?

Not always. While a 20% down payment makes you a safer borrower, interest rates are heavily driven by your credit score. A borrower putting 5% down with an 800 credit score will often get a much better interest rate than a borrower putting 20% down with a 620 credit score.

6. Can I take a loan from my 401(k) for a down payment?

Many 401(k) plans allow you to take out a loan of up to $50,000 or 50% of your vested balance to buy a primary residence. You pay the interest back to yourself. However, if you leave your job, the loan may become due immediately. It is generally a risky strategy and should only be used as a last resort.

7. I want to buy a duplex. Does the down payment change?

If you plan to live in one side and rent out the other (a strategy called house hacking), you can still use a 3.5% down FHA loan or a 5% down Conventional loan. If you do not plan to live there and are buying it strictly as an investment property, you will typically need to put down 20% to 25%.

Conclusion

The thought of saving tens of thousands of dollars to buy a home can feel completely overwhelming. But when you strip away the outdated advice and look at the actual math of the modern mortgage market, homeownership is much closer than you think.

You do not need to pause your life for the next ten years to save 20%. By aiming for a 3% or 5% down payment, budgeting accurately for closing costs, and protecting a dedicated emergency fund, you can safely transition from renting to owning. Focus on eliminating your high-interest debt, protect your credit score, and start automatically funding your down payment account today. The math is in your favor.

References

- Consumer Financial Protection Bureau (CFPB): Buying a House Guide

- U.S. Department of Housing and Urban Development (HUD): FHA Loan Requirements

- Federal Reserve: Survey of Consumer Finances (SCF)

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.