FHA Loan vs USDA Loan vs Conventional Loan: Which Mortgage is Right for You?

When you finally decide you are ready to buy a house, the first thing you probably do is open an app and start looking at properties. You look at kitchens, backyards, and school districts. But very quickly, you realize that finding the house is only the second hardest part of the process. The hardest part is figuring out how to actually pay for it.

When you sit down with a lender, they will throw a handful of acronyms at you: FHA, USDA, Conventional, VA. If you do not know the difference between an FHA loan vs USDA loan vs Conventional loan, you are at a massive disadvantage.

Choosing the wrong mortgage program can cost you tens of thousands of dollars over the life of your loan. It dictates exactly how much cash you need to bring to closing day, what your monthly payment will look like, and whether you are forced to pay for permanent mortgage insurance.

In this comprehensive guide, we are going to strip away the complex banking jargon. We will break down exactly how these three major loan programs work, compare their strict requirements, run real-world math scenarios, and help you determine exactly which mortgage is the smartest financial choice for your specific situation.

Quick Answer: FHA Loan vs USDA Loan vs Conventional Loan

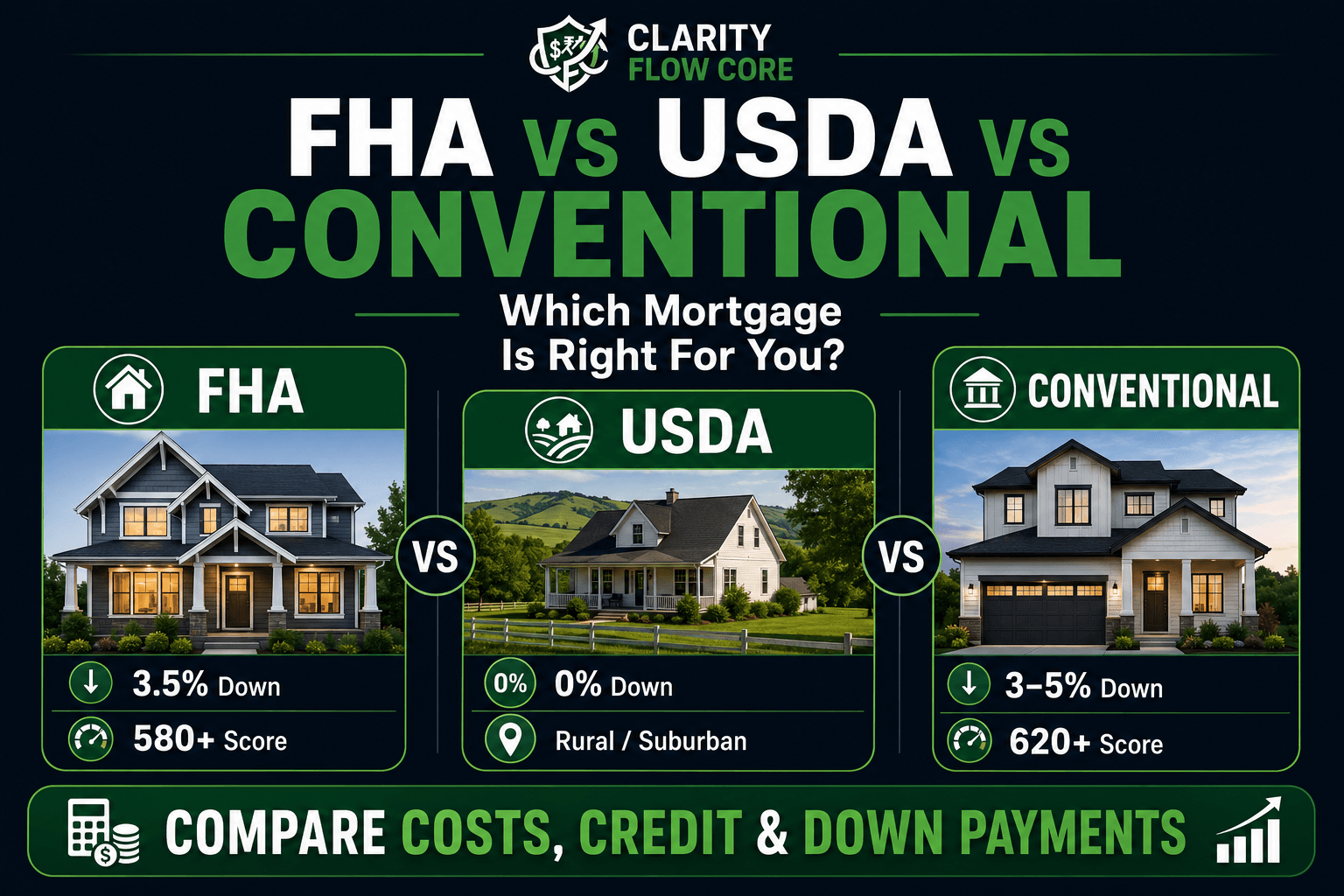

A Conventional loan is best if you have a strong credit score (620+) and want your mortgage insurance (PMI) to eventually fall off. An FHA loan is best if your credit score has taken a few hits (580+) and you need a low 3.5% down payment, though you will pay permanent mortgage insurance. A USDA loan is best if you want to buy a home with a 0% down payment, provided you meet strict income limits and plan to buy in a designated rural or suburban area.

1. The Conventional Loan Explained

When most people think of a standard mortgage, they are thinking of a Conventional loan. Unlike FHA or USDA loans, Conventional loans are not backed or insured by the federal government. Instead, they are backed by private lenders and typically sold to government-sponsored enterprises like Fannie Mae or Freddie Mac.

Because the government is not insuring the loan against default, private lenders take on more risk. To protect themselves, they require borrowers to have stronger financial profiles.

The Core Requirements

- Minimum Down Payment: If you are a first-time homebuyer, you can get a Conventional loan with as little as 3% down. If you have owned a home recently, the minimum is typically 5%.

- Minimum Credit Score: You generally need a minimum credit score of 620 to qualify. However, to get a truly competitive interest rate, lenders usually want to see a score of 740 or higher.

- Debt-to-Income (DTI) Ratio: Lenders typically want to see a DTI ratio below 43%, though some will stretch to 50% if you have strong compensating factors like a massive savings account.

The Pros of a Conventional Loan

- Cancelable Mortgage Insurance: If you put down less than 20%, you will have to pay for Private Mortgage Insurance (PMI). However, once you build 20% equity in the home, you can legally request that the PMI be removed. This saves you hundreds of dollars a month.

- Fewer Property Restrictions: Conventional appraisers care about the home’s value, not necessarily minor cosmetic defects. You can use a Conventional loan to buy a fixer-upper with peeling paint or a missing handrail.

- Higher Loan Limits: Conventional loans generally allow you to borrow significantly more money than FHA or USDA loans, making them ideal for high-cost housing markets.

The Cons of a Conventional Loan

- Unforgiving of Bad Credit: If your credit score is in the low 600s, a Conventional lender will likely hit you with a very high interest rate and an incredibly expensive PMI premium.

Simulate Your Future Credit Score

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our free simulator.

Launch Credit Simulator2. The FHA Loan Explained

The Federal Housing Administration (FHA) created this loan program specifically to help moderate-income earners and first-time buyers break into the housing market.

FHA loans are insured by the federal government. This means if you lose your job and default on your mortgage, the government pays the lender back. Because the lender has this massive safety net, they are willing to approve loans for buyers who would be immediately rejected for a Conventional mortgage.

The Core Requirements

- Minimum Down Payment: You only need a 3.5% down payment.

- Minimum Credit Score: FHA loans are incredibly forgiving. You only need a 580 credit score to qualify for the 3.5% down payment. If your score is between 500 and 579, you can still get a loan, but you must put 10% down.

- Debt-to-Income (DTI) Ratio: The FHA is much more lenient with debt. Depending on your credit score, you can often get approved with a DTI stretching up to 50% or even higher.

The Pros of an FHA Loan

- Accessible to Almost Anyone: If you have average credit, an FHA loan is often your best and only route to homeownership.

- Better Interest Rates for Lower Credit: Because the loan is government-backed, a borrower with a 620 credit score will almost always get a much lower interest rate on an FHA loan than they would on a Conventional loan.

- Gift Funds Allowed: The FHA allows 100% of your down payment to come from a family member’s financial gift.

The Cons of an FHA Loan

- Permanent Mortgage Insurance (MIP): This is the massive catch. FHA mortgage insurance often remains for the life of the loan when the down payment is less than 10%, unless the borrower refinances into another loan type.

- Strict Appraisals: The FHA requires homes to meet strict minimum health and safety standards. If the house has peeling paint, a damaged roof, or electrical issues, the appraiser will flag it. The seller must fix the issues before the loan can close, which makes some sellers hesitant to accept FHA offers.

(Want to dig deeper into these rules? Read our complete breakdown: FHA Loan Requirements in 2026).

3. The USDA Loan Explained

The United States Department of Agriculture (USDA) offers one of the most powerful, underutilized mortgage programs in the entire country. The USDA loan was created to encourage homeownership and economic development in rural and suburban areas.

If you meet the geographic and income requirements, this loan program allows you to buy a house with absolutely no money down.

The Core Requirements

- Minimum Down Payment: $0. (Yes, 0% down).

- Minimum Credit Score: The USDA does not actually set a strict minimum score, but most lenders require a 640 credit score to run your application through their automated underwriting system.

- Income Limits: This program is strictly for low-to-moderate-income families. You cannot make too much money. The income limit is capped at 115% of the median household income for the specific county where you are buying the home.

- Location Limits: You cannot use a USDA loan to buy a condo in downtown Manhattan. The home must be located in a USDA-eligible rural or suburban area. Many buyers mistakenly assume USDA loans are only for farms. In reality, many suburban communities qualify under USDA eligibility maps.

The Pros of a USDA Loan

- Zero Down Payment: You can keep your savings intact for emergencies and furniture instead of draining it to buy the house.

- Cheaper Mortgage Insurance: While USDA loans do have an upfront guarantee fee and an annual fee (similar to mortgage insurance), the rates are significantly cheaper than FHA MIP.

The Cons of a USDA Loan

- Location Restrictions: If you want to live in a densely populated urban center, this loan is entirely useless to you.

- Income Penalties: If you get a massive promotion at work and your household income pushes past the strict county limit, you are immediately disqualified from using the program.

Head-to-Head Comparison Table

To make comparing an FHA loan vs USDA loan vs Conventional loan easier, here is how the core metrics stack up against each other:

| Feature | Conventional Loan | FHA Loan | USDA Loan |

| Minimum Down Payment | 3% | 3.5% | 0% |

| Minimum Credit Score | 620 | 580 | Typically 640 |

| Mortgage Insurance | PMI (Cancelable at 20% equity) | MIP (Permanent if <10% down) | Guarantee Fee (Permanent) |

| Income Limits | None | None | Strict maximum limits |

| Location Limits | Anywhere | Anywhere | Eligible rural/suburban areas only |

| Property Standards | Standard appraisal | Strict safety appraisal | Strict safety appraisal |

Quick Guide: Best Loan by Situation

- Credit Score Below 620: FHA

- Want 0% Down: USDA

- Strong Credit (740+): Conventional

- Rural/Suburban Area: USDA

- Want Cancelable Mortgage Insurance: Conventional

- Limited Savings: FHA or USDA

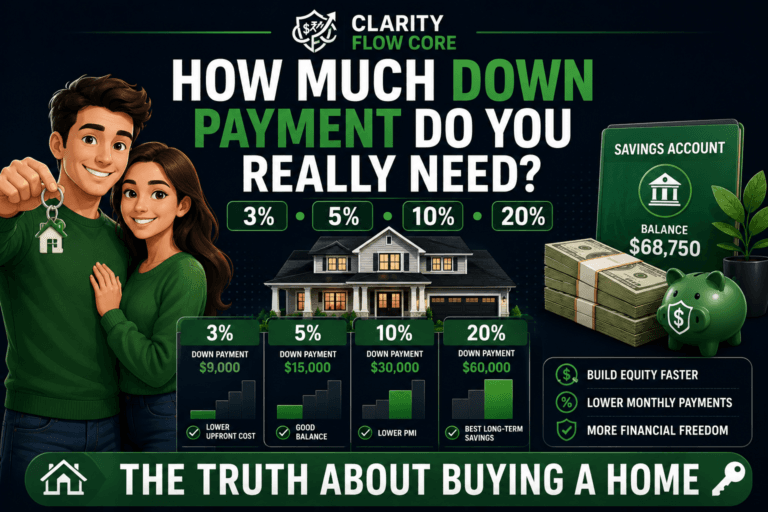

The Math: $300,000 Home Example

While interest rates vary daily, here is a quick look at the upfront cash required and the type of mortgage insurance you will pay based on a $300,000 house:

| Loan Type | Down Payment % | Approx. Cash Required | Mortgage Insurance Type |

| Conventional | 5% | $15,000 | Private Mortgage Insurance (PMI) |

| FHA | 3.5% | $10,500 | Mortgage Insurance Premium (MIP) |

| USDA | 0% | $0 | USDA Annual Fee |

Real-World Scenarios: Which Buyer Are You?

Abstract rules are confusing. Let’s look at three different buyers to see exactly how they should choose their loan program.

Scenario A: The Strong Saver

Marcus and Elena make a combined $120,000 a year. They have excellent credit scores (760) and have saved up $25,000 in cash. They want to buy a $350,000 house in the suburbs.

- The Best Choice: Conventional Loan. Because their credit is excellent, a Conventional lender will give them a top-tier interest rate. They can put down 5% ($17,500). While they will pay PMI, their excellent credit means the PMI premium will be very cheap, and they can cancel it in a few years once they build equity.

Scenario B: The Rebuilder

Sarah makes $75,000 a year. She recently paid off a lot of debt, but her credit score is still sitting at 610. She has $12,000 saved and wants to buy a $250,000 starter home.

- The Best Choice: FHA Loan. If Sarah applies for a Conventional loan with a 610 credit score, the interest rate and PMI costs will be brutally high. By using an FHA loan, she qualifies easily, only needs $8,750 for her 3.5% down payment, and secures a competitive government-backed interest rate.

Scenario C: The Rural First-Timer

David makes $55,000 a year. He has a solid 680 credit score but has struggled to save a large down payment because of high rent costs. He wants to buy a $200,000 house in a quiet town just outside the main city limits.

- The Best Choice: USDA Loan. David checks the USDA eligibility map and sees the town qualifies. Because his income is under the local limit, he can buy the $200,000 house with $0 down, completely bypassing the need to spend years saving up a massive lump sum.

Wondering exactly how much cash you need to safely enter the market regardless of loan type? Check out our guide: How Much Down Payment Do You Really Need to Buy a House?

Common Mistakes When Choosing a Mortgage

Picking the wrong mortgage program is a mistake you will pay for every single month for the next thirty years. Avoid these major blunders:

1. Draining Your Emergency Fund for a Conventional Loan

Some buyers are so terrified of FHA permanent mortgage insurance that they completely empty their savings account just to hit a 5% Conventional down payment. This is incredibly dangerous. If the furnace breaks the day after you move in, you have no cash to fix it. Never buy a house without a safety net. Run your post-purchase budget through our Advanced Emergency Fund Analyzer to figure out how much liquid cash you must keep in reserve.

2. Ignoring Debt Affordability

You might meet the 580 credit score requirement for an FHA loan, but if your auto loans and credit card minimums take up half your monthly income, the lender will still reject you. Lenders care deeply about your debt affordability. Use our Debt-to-Income Analyzer & Loan Readiness Planner to verify that your monthly cash flow is actually strong enough to handle a mortgage payment before you apply.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI Ratio3. Forgetting About Closing Costs

A USDA loan requires $0 down, but it does not mean the house is completely free on closing day. You still have to pay closing costs (appraisal fees, title search, prepaid property taxes). These typically equal 2% to 5% of the loan amount. While you can sometimes negotiate for the seller to pay these costs, you should always have your own cash saved. (Read more in Closing Costs Explained: What Home Buyers Actually Pay).

4. Overlooking Long-Term Wealth Planning

Buying a house is a major financial milestone, but it should not be your only one. Do not take out a mortgage so massive that you have zero dollars left over at the end of the month to invest for retirement. Use our Financial Freedom Planner to ensure your new housing payment aligns with your long-term wealth-building goals.

Your Action Plan: Steps to Take This Week

Ready to stop guessing and start taking action? Follow this exact checklist to prepare your mortgage strategy:

- Pull Your Official Credit Scores: Check your FICO scores from all three major bureaus. If you are below 620, an FHA loan is your most realistic target. If you are above 700, a Conventional loan will likely offer the best long-term value.

- Calculate Your DTI: Total up your minimum monthly debt payments (credit cards, student loans, car loans) and divide that by your gross monthly income. Aim to keep this number below 36%.

- Check the USDA Map: If you are open to living outside the city center, go to the official USDA rural development website and type in your target neighborhoods. You might be shocked to see which areas qualify for 0% down.

- Shop Multiple Lenders: Never accept the first mortgage quote you get. Talk to a local credit union, an online lender, and a mortgage broker. Ask them to run estimates for both a Conventional and an FHA loan so you can compare the actual monthly payments side-by-side.

Frequently Asked Questions (FAQ)

1. Can I use an FHA or USDA loan to buy an investment property?

No. FHA, USDA, and standard VA loans are strictly for primary residences. You must intend to live in the home for at least one year. If you want to buy a rental property, you will typically need to use a Conventional loan and put down 20% to 25%.

2. Do home sellers hate FHA and USDA loans?

“Hate” is a strong word, but in a highly competitive market, sellers often prefer Conventional buyers. This is because FHA and USDA appraisers have strict safety standards. If the appraiser finds peeling paint or a broken window, the seller is often forced to pay for the repairs before the deal can close. Conventional loans do not have these strict repair requirements.

3. Can I refinance an FHA loan into a Conventional loan later?

Yes! This is an incredibly common strategy. Many buyers use an FHA loan to get into a house with a low credit score and a 3.5% down payment. After living in the home for a few years, making on-time payments, and building 20% equity, they refinance into a Conventional loan to drop the permanent FHA mortgage insurance.

4. What is a Jumbo Loan?

If you are buying an expensive house in a high-cost market (like San Francisco or Seattle), you might exceed the federal loan limits for standard Conventional or FHA loans. If you need to borrow more than the limit (which changes annually but is often above $750,000), you must use a “Jumbo Loan.” These loans require pristine credit and usually a massive down payment.

5. Which loan has the lowest interest rate?

Generally, VA loans offer the lowest interest rates on the market, followed closely by USDA and FHA loans. Because these loans are government-backed, lenders take on less risk and pass the savings on to you. Conventional loan rates are highly dependent on your personal credit score.

6. I want to buy a multi-family home. Which loan should I use?

If you want to buy a duplex or triplex, live in one unit, and rent out the others (a strategy called house hacking), you can use an FHA loan with just 3.5% down or a Conventional loan with 5% down. USDA loans cannot be used to purchase multi-family income properties.

7. Can I switch loan types after buying a home?

Yes. Many homeowners refinance from FHA to Conventional once their credit improves and they build sufficient equity, allowing them to remove FHA mortgage insurance.

Pros & Cons Snapshot

Conventional

✅ Cancelable PMI

✅ Best for strong credit

❌ Harder qualification

FHA

✅ Lower credit requirements

✅ Easier approval

❌ Permanent MIP in many cases

USDA

✅ 0% down payment

✅ Lower mortgage insurance costs

❌ Income and location restrictions

Conclusion

Understanding the difference between an FHA loan vs USDA loan vs Conventional loan is the ultimate cheat code to the real estate market. The right loan program can literally be the difference between buying a home this year or staying stuck in a rental for five more years while you try to save an outdated 20% down payment.

If you have great credit, target a Conventional loan to keep your mortgage insurance temporary. If your credit is still recovering, leverage the power of the FHA program to get your foot in the door. And if you are willing to live in a quieter suburban or rural area, let the USDA program completely erase your down payment hurdle.

Take control of your credit, calculate your true debt-to-income ratio, and approach your lender with confidence. Your future home is waiting.

References

- Consumer Financial Protection Bureau (CFPB): Loan Options and Mortgage Types

- U.S. Department of Housing and Urban Development (HUD): FHA Mortgage Limits and Requirements

- U.S. Department of Agriculture (USDA): Single Family Housing Guaranteed Loan Program

- Federal Reserve: Consumer Guide to Mortgages

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.