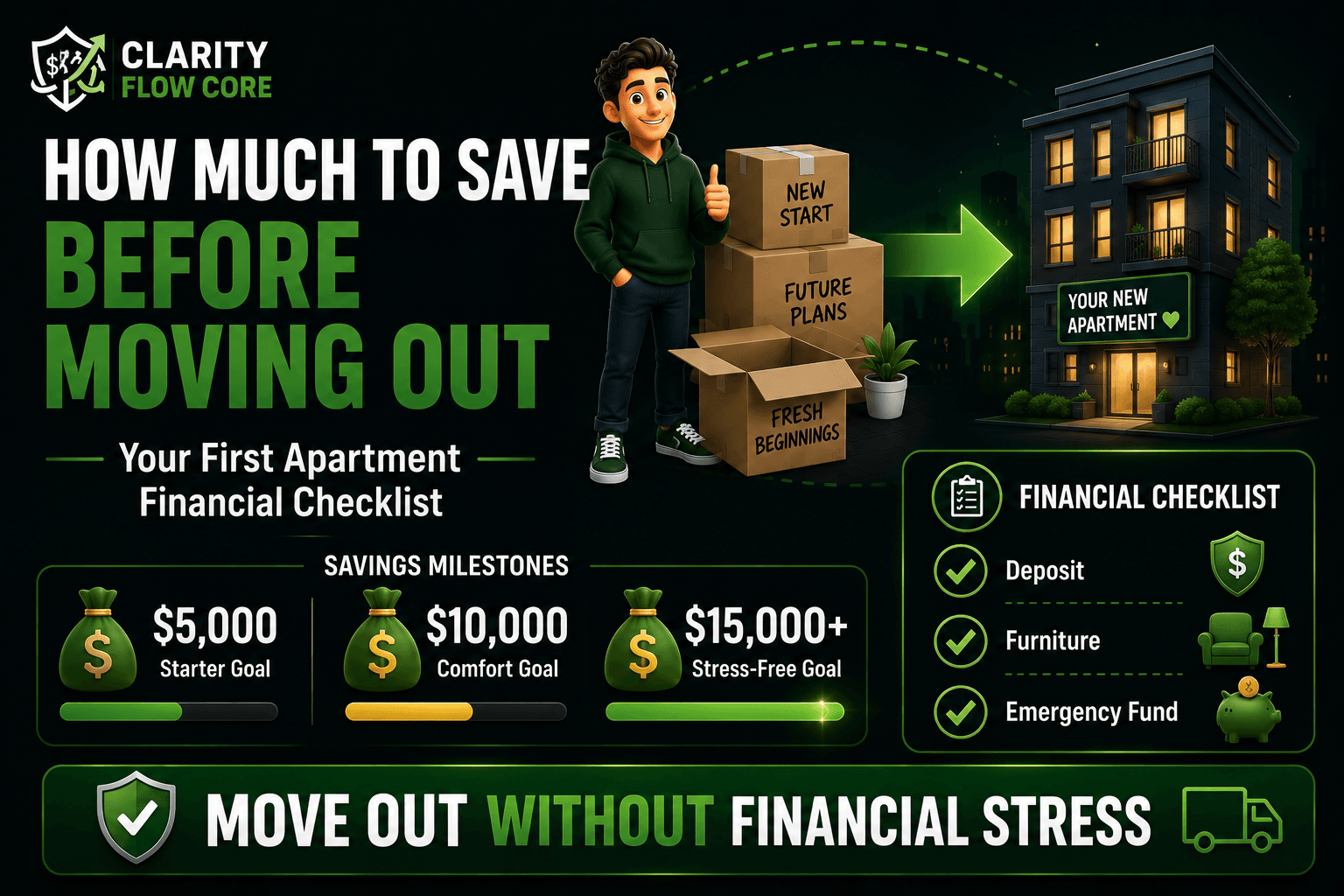

How Much to Save Before Moving Out on Your Own

Moving out on your own is one of the most exciting milestones in life, but it comes with a serious price tag. If you are wondering exactly how much to save before moving out, you are already taking the right first step toward financial independence. Before you start browsing apartment listings on Zillow, touring neighborhoods, and picking out living room furniture, you need a clear financial roadmap. Without enough cash saved up, the excitement of independence can quickly turn into crushing financial stress.

While there is no single magic number that applies to every person in every city, a strong baseline rule of thumb is to save three to six months of living expenses, plus your absolute upfront moving costs. Depending on the cost of living in your area, that usually means having anywhere from $5,000 to $10,000 securely in the bank before you pack your first box.

In this comprehensive guide, we will break down exactly what you need to budget for, how to calculate your personal target savings goal, the hidden costs that catch most first-time renters completely off guard, and exactly how to prepare your finances for the big move.

The Big Picture: Categorizing Your Move-Out Fund

When determining how much to save before moving out, your target savings goal needs to cover three distinct buckets of money. The biggest mistake you can make is emptying your checking account just to get the keys to your new place. If you do that, you are putting yourself at massive financial risk from day one.

Here is a detailed breakdown of the three categories you must save for:

1. The Upfront Move-In Costs (The Landlord’s Cut)

This is the required cash you need to physically get into the apartment and turn the lights on. Landlords and property management companies require substantial funds upfront to protect themselves against property damage, unpaid rent, or broken leases.

| Expense Type | Estimated Cost | Details & Nuance |

| Application Fees | $30 to $75 per person | Non-refundable. Covers the cost of the landlord running your background and credit check. |

| Security Deposit | 1 to 2 months’ rent | Refundable (usually). Landlords charge more if you have poor credit or no rental history. |

| First & Last Month’s Rent | Up to 2 months’ rent | Many competitive rental markets require both the first and the final month’s rent upfront. |

| Utility Deposits | $50 to $200 per utility | If you have never had an electric, water, or gas account in your name, they will require a security deposit. |

| Pet Fees/Deposits | $200 to $500 | If you have a dog or cat, expect a non-refundable pet fee, a pet deposit, or monthly “pet rent.” |

2. The Physical Moving & Setup Costs

Getting your belongings from point A to point B costs money. Even if you are just moving out of a childhood bedroom and taking nothing but your clothes, you will likely need to buy the basics to make an empty apartment functional.

- Moving Truck Rental or Movers: Renting a U-Haul or Budget truck locally usually costs around $100 to $150 after mileage and gas. If you are hiring professional local movers, expect to pay between $500 and $1,200 depending on the size of the move and how many stairs they have to climb.

- Packing Supplies: Boxes, heavy-duty packing tape, bubble wrap, and markers. You can often source free boxes from local grocery stores, but if you buy them new, budget $50 to $100.

- Basic Furniture: If you are starting from scratch, you need a place to sleep and a place to sit. A mattress, bed frame, small sofa, and a cheap dining table.

- Household Essentials: This is what shocks most people. Trash cans, cleaning supplies, a vacuum, shower curtains, bath mats, pots, pans, utensils, and enough groceries to stock an empty fridge and pantry from scratch.

3. Your Emergency Fund

This is the most critical and most frequently overlooked step. You should never move into a new place with $0 left in your bank account. If your car breaks down the week after you move in, if you face an unexpected medical bill, or if you lose your job, you need a financial cushion so you do not have to rely on high-interest credit cards to survive.

We highly recommend running your numbers through our Advanced Emergency Fund Analyzer to see exactly how much cash you need to keep safe in a high-yield savings account. For a deeper dive into how to build this cushion, read our comprehensive Emergency Fund Basics Guide.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetStep-by-Step: Calculating Your Custom Savings Goal

Let’s look at a realistic scenario for someone moving into a mid-range apartment that costs $1,500 per month. Figuring out exactly how much to save before moving out means running the math on your specific situation. Here is how a standard budget breaks down:

Phase 1: The Lease-Signing Costs

When you sit down at the property manager’s desk to sign the lease, you need to hand over a cashier’s check or make a wire transfer for the initial move-in costs.

- First Month’s Rent: $1,500

- Security Deposit: $1,500

- Application/Admin Fees: $100

- Total Lease Costs: $3,100

Phase 2: Utility Setup and Moving Expenses

Before you move a single box, you need the internet turned on and the electricity running.

- Electric/Gas Deposits: $150

- Internet Installation: $50

- Truck Rental & Boxes: $150

- Total Setup Costs: $350

Phase 3: Essentials and Furnishings

If you are starting completely from scratch, you will need to buy a lot of boring but strictly necessary items. Plungers, toilet paper, glass cleaner, spices, and basic cookware add up fast.

- Household Essentials & First Grocery Run: $400

- Basic Furniture (Thrifted or Budget Retailers): $800

- Total Setup Costs: $1,200

Phase 4: The 3-Month Emergency Fund

Your living expenses are not just rent. They include groceries, car insurance, gas, phone bills, internet, and minimum debt payments. Let’s assume your total monthly living expenses come out to $3,000.

- 3 Months of Living Expenses: $9,000

- Note: If you want to learn more about balancing this cash across different accounts, check out our guide on How Much Should You Keep in Checking vs Savings?

The Final Target Number

Adding it all together:

- Lease Costs: $3,100

- Setup Costs: $350

- Furnishings: $1,200

- Emergency Fund: $9,000

- Total Savings Goal: $13,650

While $13,650 might seem like a daunting, unreachable number, remember that $9,000 of that is your protective safety net. If you are willing to take on a bit more risk and live exceptionally lean, you could move out with a 1-month emergency fund instead, bringing your target down to around $7,650.

Room-by-Room: The “First Apartment” Shopping List

When calculating how much to save before moving out, people often forget the sheer volume of small items required to run a household. Here is a breakdown of the hidden expenses you need to budget for:

The Kitchen

You can’t eat takeout every night if you want to afford rent. You need: a trash can, trash bags, dish soap, sponges, paper towels, a basic set of pots and pans, spatulas, oven mitts, a cutting board, a decent chef’s knife, silverware, plates, bowls, glasses, and Tupperware for leftovers.

- Estimated starter cost: $200 – $300

The Bathroom

A shower curtain, shower curtain rings, bath towels, hand towels, a bath mat, toilet paper, a toilet brush, a plunger, hand soap, and a bathroom trash can.

- Estimated starter cost: $100 – $150

The Cleaning Supplies

Broom and dustpan, mop, multi-surface cleaner, glass cleaner, toilet bowl cleaner, laundry detergent, and a laundry basket.

- Estimated starter cost: $75 – $100

How Much Rent Can You Actually Afford?

Saving up the cash to move out is only half the battle. Before you sign a 12-month lease, you need to ensure the ongoing monthly rent payments fit seamlessly into your long-term budget.

The 30% Gross Income Rule

The standard financial rule of thumb utilized by most landlords is that your rent should not exceed 30% of your gross monthly income (your total income before taxes are taken out).

For example, if you make $60,000 a year, your gross monthly income is $5,000. Under the 30% rule, your absolute maximum rent should be $1,500. In fact, most property management companies require you to prove that your gross income is at least 3x the monthly rent before they will approve your application.

The Take-Home Pay Reality Check

However, gross income can be highly misleading because it does not account for income taxes, health insurance premiums, or 401(k) retirement contributions. A much safer and far more practical approach is to keep your rent under 30% of your take-home pay (the actual net amount that hits your checking account after all deductions).

If you have student loans, heavy car payments, or credit card debt, your housing budget might need to be even lower than 30%. To see exactly how a new rent payment will affect your overall financial health, use our Free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI RatioYou can also use The 50/30/20 Budget Rule Explained Simply to structure your new monthly spending plan and ensure you still have money left over for investing and entertainment.

Common Mistakes to Avoid When Moving Out

1. Forgetting About Renter’s Insurance

Many first-time renters falsely assume that their landlord’s property insurance covers their personal belongings. It does not. The landlord’s insurance only covers the physical building structure. If there is a fire, a burst pipe that floods your unit, or a break-in, you are entirely responsible for replacing your laptop, clothes, and furniture. Renter’s insurance is incredibly cheap—usually between $10 and $20 a month—and covers tens of thousands of dollars worth of property. Never skip it.

2. Ignoring Your Credit Score

Landlords will pull your credit report when you apply for an apartment. If you have a low credit score, no credit history at all, or a history of late payments, you might be denied the apartment entirely. Alternatively, the landlord might approve you but charge a double security deposit.

Take time to build your credit before applying. Keeping your credit card balances low is crucial. To understand how your balances impact your score, utilize our Interactive Credit Utilization & Score Simulator. If you aren’t sure where your credit stands or how to start building it, learn more in our Best Credit Cards for Beginners guide.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My Utilization3. Rushing the Furniture Process

You do not need to fully furnish a two-bedroom apartment on day one. A common financial trap is putting thousands of dollars of brand-new furniture on a high-interest credit card just to make the place look “aesthetic” immediately. Start with a mattress and a cheap table. Buy the rest slowly with cash over your first year using Facebook Marketplace, thrift stores, and clearance sales.

4. Co-Signing With the Wrong Roommate

If you are moving in with a roommate to lower your costs, understand that in most leases, you are “jointly and severally liable.” This means if your roommate loses their job and stops paying their half of the rent, the landlord can and will come after you for the full amount. Only sign a lease with someone whose financial habits you trust implicitly.

Your Action Plan: Preparing for the Big Move

If you are planning to move out in the next 6 to 12 months, do not just guess at your savings. Follow this step-by-step action plan to get your finances rigorously prepared.

1.Track Your Current Spending:Establish your baseline.

Before you add rent and utilities to your life, you need to know exactly where your money goes right now. Look at your last three months of bank statements to find your baseline spending on food, gas, subscriptions, and entertainment.

2.Take the ‘Practice Rent’ Challenge:Test your budget reality.

If you currently live rent-free with family, calculate your target rent and utility cost (e.g., $1,500). For the next three months, transfer that exact amount into a high-yield savings account on the first of every month. If you struggle to make it to the end of the month without dipping back into those savings, you cannot afford that rent yet. If you succeed, you just added $4,500 to your move-out fund!

3.Check and Protect Your Credit:Fix errors before landlords see them.

Pull your free credit reports from AnnualCreditReport.com. Check for errors, pay down high credit card balances, and ensure you have a solid history of on-time payments. Fix any issues at least 60 days before you apply for apartments.

4.Build a Lean Moving Budget:Source cheap supplies.

Start gathering quotes for moving trucks and mapping out the cost of essential furniture. Look at local thrift stores, Craigslist, and clearance sections to keep your day-one costs as low as possible.

5.Map Your Financial Future:Look beyond the lease.

Moving out is just step one. You still need to plan for retirement, vacations, and future goals. Use our Financial Freedom Planner to see how your new living expenses will impact your long-term wealth building.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanFrequently Asked Questions (FAQ)

How much should a $20-an-hour worker pay in rent?

If you make $20 an hour working full-time (40 hours a week), your gross monthly income is roughly $3,466. Following the standard 30% rule, your maximum rent should be around $1,040 per month. In many major US cities, you will likely need a roommate to find safe housing at this price point.

Can I move out with only $2,000 saved?

It is highly risky and generally not recommended. In most areas, $2,000 will barely cover the first month’s rent and the security deposit, leaving you with absolutely zero money for groceries, utility deposits, moving costs, or emergencies.

Does paying rent build my credit score?

Traditionally, rent payments are not reported to the major credit bureaus (Equifax, Experian, TransUnion). However, you can use third-party rent-reporting services (some charge a small fee, while others are offered directly by property managers) to have your on-time rent payments added to your credit file, which can help build your score.

What happens if I break my lease early?

Breaking a lease usually triggers a severe financial penalty. Most standard leases require you to pay a fee equivalent to one or two months of rent, or they require you to keep paying the monthly rent until the landlord finds a new tenant to replace you. Always read the “early termination” clause in your lease before signing.

Should I use a credit card to pay for moving expenses?

Using a credit card is fine if you already have the cash sitting in your checking account and plan to pay the statement balance in full immediately to avoid interest (and earn cash-back rewards). However, putting moving expenses on a credit card that you cannot pay off will trap you in high-interest debt right as you take on a new, massive monthly rent payment.

Conclusion

Moving out on your own is incredibly rewarding, but rushing the process can ruin your financial foundation for years to come. Take the time to build a robust savings buffer that covers your first month’s rent, security deposits, basic furniture, and at least a three-month emergency fund.

By planning ahead, budgeting for the hidden costs, and doing a rigorous “practice rent” run, you can sign your first lease with total confidence. Take control of your numbers today so you can actually enjoy your new space tomorrow. If you are torn between signing a lease or trying to buy a small place, read our detailed breakdown on Renting vs Buying a Home in 2026.

References

- Consumer Financial Protection Bureau (CFPB): Guide to finding affordable rental housing and understanding tenant background checks.

- Federal Deposit Insurance Corporation (FDIC): Recommendations on building a practical emergency savings fund.

- Federal Trade Commission (FTC): Consumer advice on renting an apartment, understanding leases, and avoiding rental scams.

- U.S. Department of Housing and Urban Development (HUD): Resources for tenants regarding fair housing laws and tenant rights.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.