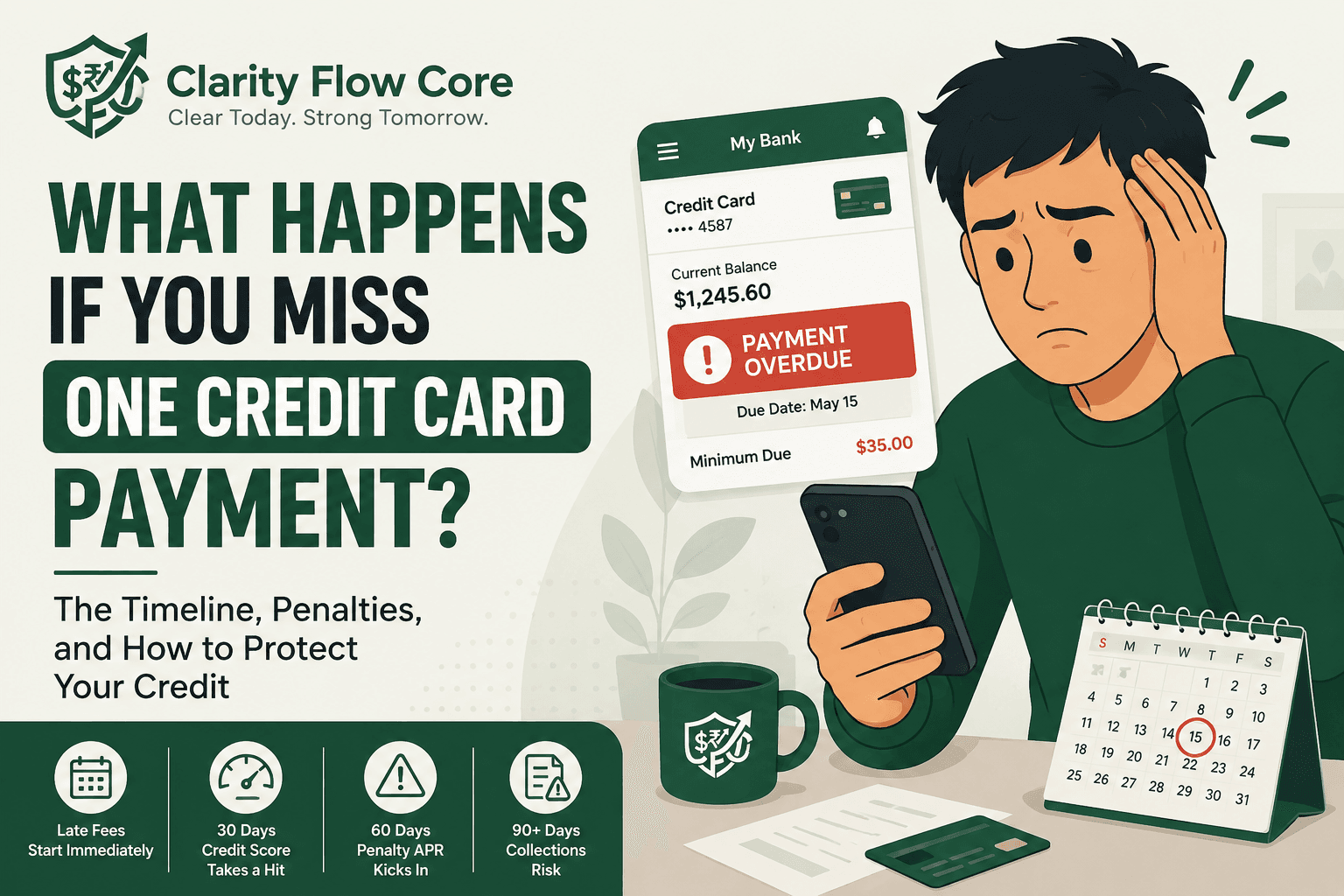

What Happens If You Missed Credit Card Payment?

You log into your banking app, glance at your account dashboard, and your stomach immediately drops. Staring back at you in bright red text is a past-due notice. You missed your payment date.

For anyone who is actively trying to build wealth and maintain a pristine financial reputation, a missed credit card payment feels like a catastrophic failure. The immediate instinct is to panic, assuming your credit score has been permanently destroyed and the bank is about to seize your assets.

Take a deep breath. A missed credit card payment is a highly operational problem, and it has a highly operational fix.

When I first started building my financial foundation, I accidentally missed a payment by exactly three days because of a banking glitch on a holiday weekend. I was terrified I had ruined years of hard work. The reality I quickly learned is that the credit card industry operates on a very strict, legally mandated timeline. The consequences of a mistake entirely depend on exactly how late your payment actually is.

If you just realized you missed your due date, the clock is ticking. Here is the definitive operational timeline of what actually happens when you have a missed credit card payment, the hidden math behind penalty interest rates, and the exact steps you must take today to protect your FICO score.

⚡ Quick Answer

Missing a credit card payment by less than 30 days usually won’t hurt your credit score, but you will immediately face late fees and lose your interest-free grace period. Once a payment becomes 30 or more days late, it triggers a derogatory mark that can significantly damage your FICO score and stay on your permanent credit report for up to 7 years.

The Immediate Fallout: Days 1 to 29 (The Financial Penalty)

The single most common misconception about a missed credit card payment is that your credit score drops the very next morning. It does not.

Under the strict rules of the Fair Credit Reporting Act (FCRA), a credit card issuer cannot legally report your payment as “late” to the major credit bureaus until it is a full 30 days past due. If your bill was due on the 15th, and you pay it on the 18th, your credit score is mathematically safe. The FICO algorithm will never even know you were late. (If you are unsure how these algorithms work, read FICO vs. VantageScore: Why Credit Scores Differ Between Apps).

However, your wallet is not safe. The moment the clock strikes midnight on your due date, the bank enacts its first line of defense to punish the behavior.

1. The Late Fee Mechanics

If you miss the deadline by a single minute, the bank will hit you with a late fee on your next statement. Historically, massive national banks relied heavily on this fee to generate billions in corporate revenue, frequently charging up to $41 for a single late payment.

While the Consumer Financial Protection Bureau (CFPB) has been fighting intense legal battles to cap these late fees for major issuers, many regional banks and credit unions still charge anywhere between $25 and $40 if you miss your date. It is a direct hit to your monthly cash flow.

2. The Loss of the Grace Period

This is the hidden cost of a missed credit card payment that most beginners completely overlook. By law, credit card issuers must give you a 21-day grace period between the end of your billing cycle and your payment due date. If you pay your statement balance in full by the due date, you pay exactly 0% in interest.

The second you miss that payment, the grace period vanishes. The bank will immediately begin charging you your standard daily interest rate on your entire balance. If you were carrying a large balance, you are now officially bleeding cash every single day the bill goes unpaid.

Day 30: The FICO Strike (The Credit Score Drop)

If you ignore the warnings, assume the problem will fix itself, and allow your missed credit card payment to cross the 30-day threshold, you have crossed the point of no return.

On day 30, the credit card issuer will automatically transmit a “30-Day Late” derogatory mark to Experian, Equifax, and TransUnion. This is where the structural damage to your financial reputation begins. (Learn how to actually locate this mark by reading How to Read and Fix Errors on Your Credit Report).

Your FICO score is simply an algorithmic measurement of risk. The single largest component of that algorithm is your Payment History, which accounts for a massive 35% of your total score. The system is highly sensitive to recent, missed payments because they are the number one statistical predictor of future loan default.

The Algorithmic Impact:

Consumers with excellent credit may experience significantly larger score declines than consumers with already damaged credit profiles. The exact impact varies based on the individual’s overall credit history, utilization, and number of accounts.

A single 30-day missed credit card payment stays on your permanent credit report for exactly seven years. While the algorithmic damage fades slowly over time as you stack up new, positive on-time payments, that red mark will be visible to every mortgage lender, landlord, and auto dealership for nearly a decade.

Late Payment Consequences by Timeline

To visualize the escalating operational danger of ignoring your bill, use this exact timeline:

| Days Late | Late Fee Incurred | Credit Score Impact | Collection Risk |

| 1–29 Days | Usually Yes | Usually No | No |

| 30 Days | Yes | Possible Major Impact | No |

| 60 Days | Yes | Severe Impact | No |

| 90–120 Days | Yes | Very Severe Impact | Increasing |

| 180+ Days | Yes | Devastating | Charge-Off & Collections |

Day 60: The Penalty APR Nightmare

If you think a 30-day credit score drop is brutal, crossing the 60-day mark triggers a financial catastrophe known as the Penalty APR.

A Penalty APR is a massively inflated, punitive interest rate that the bank applies to your account when you prove you are a high-risk borrower. If you have a missed credit card payment that reaches 60 days past due, you legally default on your original cardholder agreement.

Most standard credit cards have an interest rate hovering around 18% to 22%. When you trigger the Penalty APR, the bank will universally spike your interest rate to the legal maximum—often 29.99%.

Why the Penalty APR is a Death Spiral

The Penalty APR does not just apply to new things you buy moving forward. Under federal law, if you are 60 days late, the bank is legally permitted to apply that 29.99% interest rate to your existing balance as well.

If you are carrying a large balance, this move will absolutely crush your monthly cash flow. Suddenly, the minimum payments you were already struggling to make are barely covering the newly inflated interest charges.

(Note: The CARD Act dictates that if you trigger a Penalty APR due to a 60-day missed credit card payment, the bank must review your account after you make six consecutive, on-time monthly payments. If you prove your reliability, they are required by law to lower your rate back down. However, the initial credit score damage remains).

Days 90 to 180: The Charge-Off and Collections

If your missed credit card payment stretches into the 90-day and 120-day territory, your credit score goes into a complete freefall. The bank views you as a severe, unrecoverable liability. They will likely freeze your credit line so you cannot make new purchases, revoke your accumulated rewards points, and relentlessly call your phone.

At the 180-day mark, the final blow lands: The Charge-Off.

The bank essentially gives up on you. They officially write your debt off their corporate books as a massive loss. They close your account permanently and sell your outstanding debt for pennies on the dollar to a third-party debt collection agency.

Once your debt is transferred to a collection agency, your next steps become extremely important. Before responding to collection calls or agreeing to any payment arrangement, read How To Handle Debt Collectors Without Making Things Worse to understand your rights and avoid costly mistakes.

A “Charge-Off” and a “Collection” account are the two most toxic marks you can possibly have on a credit report, outside of an actual bankruptcy. It will completely lock you out of the housing market, prevent you from securing standard auto loans, and can even cause you to fail background checks for corporate employment.

The Math: The True Cost of One Mistake

To fully understand the severity of a missed credit card payment, you have to look at the operational math. Let’s look at a highly realistic scenario for a modern consumer carrying a balance.

Assume you have a $5,000 balance on a standard credit card with an 18% APR. You miss your payment, cross the 60-day threshold out of fear, trigger the late fees, and get hit with a 29.99% Penalty APR.

| Metric | On-Time Payment Strategy | 60-Day Missed Payment Strategy |

| Initial Balance | $5,000 | $5,000 |

| Interest Rate (APR) | 18% | 29.99% (Penalty APR) |

| Late Fees Incurred | $0 | $75 (Two missed months) |

| Time to Pay Off ($200/mo) | 32 Months | 41 Months |

| Total Interest Paid | $1,315 | $3,075 |

By missing that single payment window, you accidentally forced yourself to pay an extra $1,760 in pure interest and extended your time in debt by nearly a year. If you find yourself trapped in this specific scenario, you must execute a Personal Loan vs. Balance Transfer Strategy immediately to stop the bleeding.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyWhen This Backfires: The Emotional Traps

When people realize they have a missed credit card payment, their embarrassment often causes them to make irrational, emotional decisions. If you execute the wrong strategy out of panic, you will accelerate the financial damage. Here is exactly when your reaction backfires:

1. Burying Your Head in the Sand

The absolute worst thing you can do is ignore the bank. If you know you cannot afford the payment this month, dodging the bank’s phone calls guarantees you will be hit with late fees and permanent credit strikes. The bank wants their money; they do not want to destroy you. If you communicate with them proactively, you have options.

2. The Minimum Payment Myth

A massive trap is thinking that if you just log in and pay the $35 late fee, you are good to go. You aren’t. To stop the 30-day reporting clock, you must pay the late fee plus the actual minimum payment required on your statement. If your minimum payment was $60, and you only send the bank $35, you are mathematically still in default. The 30-day clock keeps ticking.

3. Rage-Closing the Account

When people get hit with a late fee, they often get incredibly angry at the bank, pay the bill, and immediately close the credit card in retaliation. This is financial self-sabotage. Exactly 15% of your FICO score is determined by your “Average Age of Credit.” If you close your oldest credit card out of anger, you artificially shorten your credit history, which will drop your score even further. Leave the card open, lock it in a desk drawer, and walk away.

Triage: What If You Actually Don’t Have the Cash?

It is one thing to miss a payment because you simply forgot. It is a completely different crisis when you have a missed credit card payment because your bank account is literally empty.

If you lost your job or faced a medical emergency, do not wait until Day 29 to act. (This is precisely why we advocate aggressively building a baseline cash reserve. Read Emergency Fund Basics: How Much Cash Should You Keep?).

Banks have entirely separate “Hardship Departments” designed specifically for this scenario. Call the number on the back of your card and explicitly ask for the Hardship or Forbearance program. Explain that you have suffered a sudden drop in income.

Many banks will offer to temporarily lower your interest rate, waive your late fees, and most importantly, they will agree to pause your payments for 3 to 6 months without reporting you as late to the credit bureaus. They would rather work with you on a paused timeline than have you default and send the account to collections.

Frequently Asked Questions (FAQs)

How late can a credit card payment be before it affects my credit score?

Generally, most major issuers do not legally report late payments to the credit bureaus until they are at least 30 days past the original due date.

Can I remove a late payment from my credit report?

Accurate late payments usually cannot be removed, although some lenders may occasionally grant goodwill adjustments in limited situations if you have a historically pristine record.

Does paying the balance erase a late payment?

No. Paying the balance in full stops further damage, prevents collections, and avoids penalty APRs, but previously reported 30-day or 60-day late payments may remain on your report.

How long do late payments stay on a credit report?

Under federal law, accurate late payments stay on your report for up to seven years from the original delinquency date.

Will one missed payment ruin my credit forever?

No. While the impact can be significant initially, responsible credit behavior and consistent on-time payments over the next several months generally reduce its algorithmic effect over time.

The Operational Fix: How to Recover Immediately

If you just looked at your statement and realized you have a missed credit card payment due to a simple oversight, you must execute this operational playbook immediately. Time is your only leverage.

Step 1: Pay It Right Now

Do not wait for your next paycheck. Do not wait for Monday morning. Log into your banking portal and pay the minimum balance plus the late fee immediately. If you are sitting at Day 12, paying the bill today entirely prevents the 30-day derogatory mark from ever reaching the credit bureaus. You stop the bleeding before it hits your permanent record.

Step 2: Automate the System

A missed credit card payment is almost always a failure of logistics, not a failure of character. You simply forgot the date. To prevent this from ever happening again, you must remove human error from the equation. Go into your credit card app and turn on Autopay for the “Minimum Balance.” Even if you prefer to manually log in every month to pay the statement in full, having the minimum on Autopay acts as a failsafe so you never accidentally trigger a late fee if you are traveling or sick.

The “Goodwill” Strategy to Remove Late Fees

If you caught the missed credit card payment before the 30-day mark, your credit score is safe, but you still have a $35 late fee sitting on your account, eating into your budget. You do not have to accept that fee.

Credit card companies are highly competitive. It costs them hundreds of dollars in marketing to acquire a single customer. They do not want to lose you over a $35 argument. If you have a historically strong track record, you can use a “Goodwill Request” to get the fee wiped out.

Call the customer service number on the back of your card. When you get a human representative, use this exact, polite script:

“Hi there, I am looking at my recent statement and I noticed I was charged a late fee. I have been a loyal customer with you for three years and I have a perfect payment history. I simply lost track of the date this month, but I just went online and paid the balance in full today. Given my flawless track record with your bank, I would like to request that you waive this late fee as a one-time courtesy.”

90% of the time, the frontline representative has the unilateral authority to click a button and refund the fee immediately. If they say no, politely hang up, call back an hour later, and ask a different representative.

The Bottom Line

A missed credit card payment feels terrifying, but it is not a permanent financial death sentence.

If you catch the mistake within the first 29 days, you will lose a little bit of cash to a late fee, but your FICO score will remain absolutely pristine. If the mistake crosses the 30-day or 60-day threshold, the algorithmic damage is severe, but it is entirely repairable over time.

Stop panicking. Log into your portal, pay the minimum balance right now to stop the clock, set your account to Autopay, and execute the Goodwill strategy. Once the bleeding has stopped, initiate a massive Debt Avalanche vs. Debt Snowball strategy to clear the balance entirely. Protect your payment history relentlessly, because it is the single most valuable asset in your financial portfolio.

If missed payments have damaged your credit and you’re rebuilding from the ground up, Best Secured Credit Cards for Beginners in 2026 compares secured cards that can help you establish fresh positive payment history and gradually rebuild your credit profile.

References & Trusted Sources

To better understand your rights regarding late fees, penalty APRs, and credit reporting timelines, refer to these official consumer protection agencies:

- Consumer Financial Protection Bureau (CFPB) – Credit Cards

- Fair Credit Reporting Act (FCRA) Guidelines

- Federal Reserve – Consumer Credit Guidance

- Experian Credit Education

- Equifax Credit Education Center

- TransUnion Credit Learning Center

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.