What Is Credit Utilization — And Why Does It Matter?

⚡ Quick Answer:

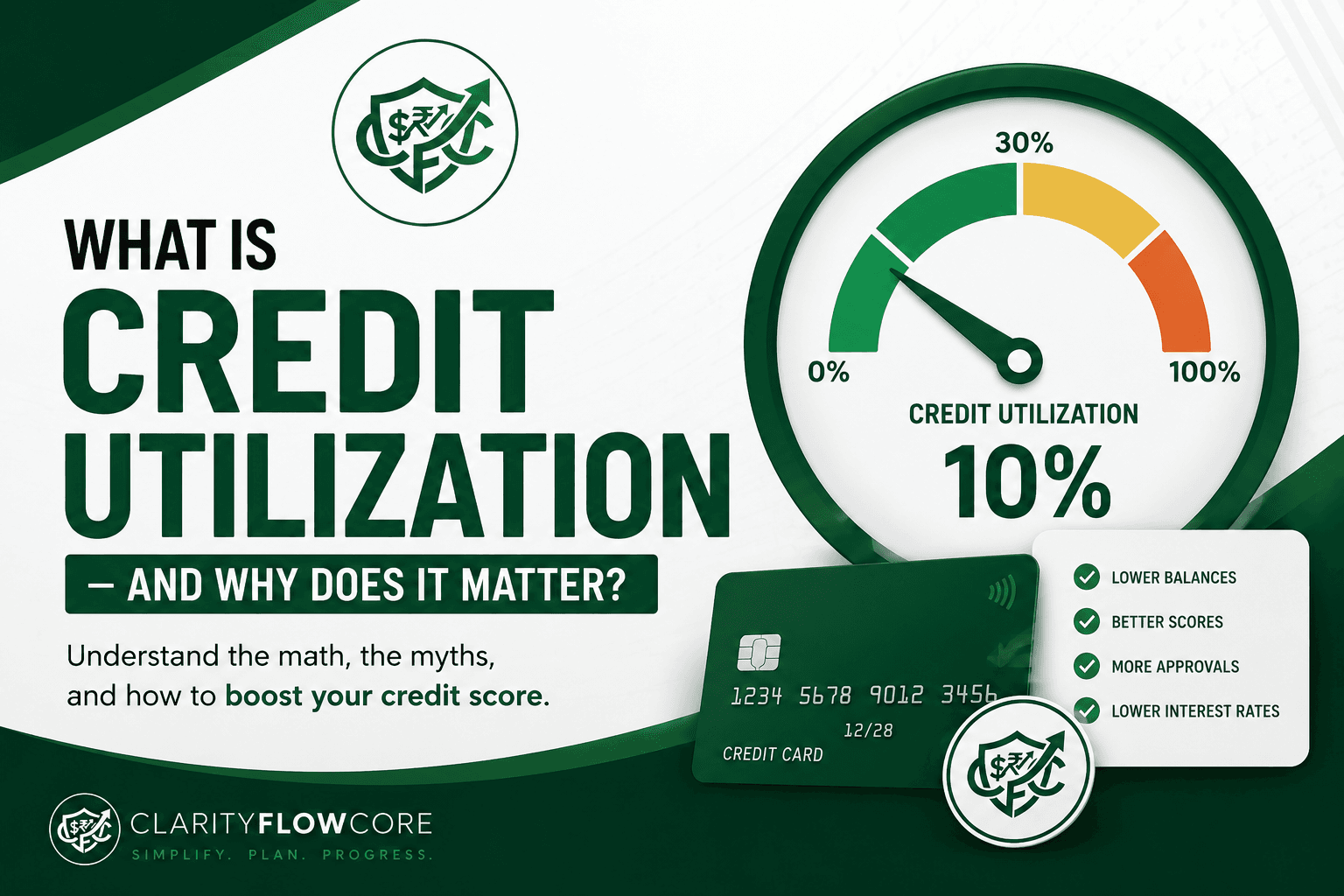

Credit utilization is the percentage of your total available credit limit that you are currently using. It accounts for a massive 30% of your FICO score. Keeping your balances below 30% of your limit prevents score drops, but keeping them below 10% is the secret to unlocking elite, 800+ credit scores.

You log into your banking app, check your credit dashboard, and out of nowhere, your score has plummeted 35 points.

You haven’t missed a single payment. You haven’t applied for a new auto loan. You simply booked a family vacation or bought a new laptop using your primary rewards card.

What you just experienced is the brutal mathematical reality of credit utilization.

When most people start building their financial foundation, they assume that paying their bills on time is the only thing that matters. While payment history is critical, the credit bureaus are tracking another metric just as closely. They are monitoring exactly how much of your available credit you rely on to survive every month.

If you want to secure the lowest possible interest rates for a future mortgage or auto loan, you cannot afford to guess how this algorithm works. Here is the definitive, operational breakdown of credit utilization, the truth about the “30% myth,” the new rules of trended data, and exactly how to manipulate the math in your favor.

The Core Math: What Is Credit Utilization?

At its core, credit utilization (often called your Credit Utilization Ratio or CUR) is a highly specific mathematical equation. It measures the amount of revolving credit you are currently using compared to the total amount of credit the banks have extended to you.

Note: This metric only applies to revolving credit (like credit cards and lines of credit). It does not factor in installment loans like mortgages, auto loans, or student debt.

(Infographic Placeholder: An infographic showing the credit utilization ratio math formula, illustrating how dividing a total balance by the total credit limit to achieve a 10% utilization rate leads to an excellent credit score.)

The Equation:

(Total Credit Card Balances ÷ Total Credit Limits) x 100 = Your Utilization Percentage

(To skip the manual math and map out your recovery, you can use our free Credit Utilization Calculator & Recovery System).

If a bank issues you a credit card with a $10,000 limit, and your current statement balance is $5,000, your credit utilization is 50%.

Why does the banking sector care so deeply about this number? Because your credit utilization accounts for exactly 30% of your entire FICO score (falling under the “Amounts Owed” category).

If you’re wondering how many points utilization can realistically change, How Much Does Credit Utilization Affect Credit Score? breaks down the potential score impact across different utilization ranges.

While utilization is incredibly important, it isn’t the biggest scoring factor. Credit Utilization vs Payment History: Which Matters More? explains how these two factors work together and which deserves your attention first.

Lenders use this ratio as a psychological stress test. If your utilization is sitting at 5%, the algorithm assumes you are financially stable, living within your means, and paying your balances off. If your utilization spikes to 85%, the algorithm assumes you have suffered a massive drop in income and are desperately relying on credit cards just to buy groceries. The algorithm views you as a high-risk liability, and it drops your score immediately to warn other lenders.

While high utilization can reduce your score, missing a payment typically causes even greater damage. What Happens If You Missed Credit Card Payment? explains the financial consequences and recovery process.

The 30% Myth vs. The 10% Reality

(Infographic Placeholder: An infographic comparing different credit utilization tiers, explaining why keeping your balance under 10% builds excellent credit scores while exceeding 30% triggers algorithmic risk and score drops.)

If you search for advice on credit utilization, you will inevitably find the same generic advice regurgitated everywhere: “Keep your utilization under 30%.”

This is the most misunderstood metric in personal finance.

The 30% rule is not a target; it is a ceiling. Staying under 30% simply prevents the algorithm from actively destroying your score. It keeps you in the “acceptable” range. If you want to achieve an elite, 800+ credit score, 30% is far too high.

When analyzing the credit profiles of consumers with the highest possible FICO scores, the data reveals a starkly different reality.

| Target Goal | Utilization Ratio | The Algorithmic Impact |

| Elite Score (800+) | 1% to 9% | Maximum positive point growth. Signals total financial control. |

| Good Score (700+) | 10% to 29% | Neutral to moderate growth. Safe, but not optimized. |

| The Danger Zone | 30% to 49% | Noticeable score drops. Signals potential cash flow issues. |

| High Risk (Default Warning) | 50% to 100% | Severe score damage (-40 to -80 points). Banks may freeze your credit limit. |

If you have a $10,000 limit, carrying a $2,900 balance (29%) keeps you out of trouble. But if you want the absolute best interest rates, you must aggressively engineer your spending, so your reported balance never exceeds $900 (9%).

If you want a deeper breakdown of why the widely repeated 30% rule is often misunderstood, The 30% Credit Utilization Myth: What Actually Matters? explores how modern scoring models actually evaluate utilization.

The Two-Front War: Per-Card vs. Overall Utilization

Another massive operational mistake beginners make is looking only at the big picture. The FICO algorithm actually calculates your credit utilization on two entirely separate fronts simultaneously. You must pass both tests.

1. Overall Utilization

This is the total sum of all your credit cards combined.

2. Per-Card Utilization

This evaluates each credit card individually. A high balance on one single card can actively tank your credit score, even if your overall utilization is near zero.

Let’s look at a real-world scenario:

Assume you have three credit cards. You use one card for all your daily spending to earn points, and leave the other two sitting in a drawer with a zero balance.

| Credit Card | Credit Limit | Current Balance | Individual Utilization |

| Card A (Daily Spender) | $5,000 | $4,500 | 90% (Red Flag) |

| Card B (Drawer Card) | $10,000 | $0 | 0% |

| Card C (Drawer Card) | $5,000 | $0 | 0% |

| TOTAL (Overall) | $20,000 | $4,500 | 22.5% (Safe) |

In this scenario, your overall credit utilization is a very healthy 22.5%. However, because Card A is maxed out at 90%, the FICO algorithm will penalize your score heavily. You cannot hide a maxed-out card behind a massive overall credit limit. You must manage the utilization ratio on every individual account.

The Game Changer: Trended Data (FICO 10T & VantageScore 4.0)

For decades, credit utilization was a static snapshot. It was a game you could easily manipulate.

Under older models (like FICO 8), the algorithm only cared about the exact balance reported on the single day the bank pulled your file. If you carried a severely maxed-out 95% utilization for eleven months, but paid the card completely off the day before applying for a mortgage, your credit score would instantly shoot up. The bank would never know you spent the entire year drowning in debt.

That loophole is officially closing.

The banking sector has introduced newer, highly sophisticated scoring models—specifically FICO 10T and VantageScore 4.0. The “T” stands for Trended Data.

Instead of looking at a one-day snapshot, these new algorithms look backward over the last 24 months of your credit history. They map out your historical credit utilization on a trendline.

- The “Transactor”: If the algorithm sees that you consistently charge $2,000 a month but pay the balance to zero every month, it flags you as a low-risk transactor.

- The “Revolver”: If the algorithm sees that your utilization has been steadily creeping up from 30% to 50% to 70% over the last year, it flags you as a high-risk revolver descending into debt.

Under trended data models, a sudden, temporary spike in utilization (like buying Christmas gifts) won’t destroy your score if your historical average is low. However, you can no longer use a last-minute lump sum payment to hide a history of reckless spending. Consistency is now mandatory.

Since different scoring models evaluate credit behavior differently, FICO vs. VantageScore: Why Credit Scores Differ Between Apps explains why your score may vary depending on where you check it.

When This Backfires: The Operational Traps

Manipulating your credit utilization requires precision. If you do not fully understand the mechanics of the banking reporting system, your actions will actively work against you. Here is exactly when managing your ratio backfires:

1. The Statement Closing Date Miss

⚠ Important: Paying your card before the due date does NOT guarantee low utilization reporting. Most banks report balances on the statement closing date instead.

This is the single most common reason people lose credit score points despite paying their bills in full.

You spend $4,000 on your card this month. Your payment due date is the 25th. You log in on the 24th and pay the $4,000 balance down to zero. You assume your utilization is 0%.

You are wrong.

Banks almost never report your balance to the credit bureaus on your payment due date. They report your balance on your Statement Closing Date (usually 3 to 7 days before your due date). If your statement closes with a $4,000 balance, the bank reports a massive credit utilization spike to the bureaus. The fact that you paid it off three days later doesn’t matter; the high balance is already locked into the algorithm for the next 30 days.

2. The Account Closure Trap

⚠ Closing old credit cards can unexpectedly increase your utilization ratio and lower your credit score.

You finally use the Debt Avalanche vs. Debt Snowball method to pay off a toxic credit card you have held for five years. Out of spite, you call the bank and immediately close the account.

This is financial self-sabotage.

By closing the account, you instantly wipe out that card’s credit limit from your overall profile. If you had $20,000 in total available credit, and you close a card with a $10,000 limit, your total available credit is instantly cut in half. Any small balances you have on your other cards will suddenly take up a much larger percentage of your newly shrunken limit, causing your overall credit utilization to skyrocket and your score to drop.

Always keep old, no-fee credit cards open. Cut the physical plastic up if you have to, but leave the digital limit open to pad your utilization ratio.

3. The Balance Transfer Mirage

If you open a new 0% APR balance transfer card to escape high interest, you must be careful. If you transfer $5,000 of debt onto a new card that only gave you a $5,500 limit, that specific new card is now sitting at a 90% per-card utilization rate. While saving money on interest is always the ultimate priority, you should expect your credit score to take a temporary hit until you aggressively pay that new transferred balance down.

The Operational Fix: How to Lower Your Utilization Fast

If your score just dropped and you need to manipulate your credit utilization back into the elite single digits, execute these three operational strategies immediately:

1. The Mid-Cycle Paydown

Do not wait for your monthly bill to arrive. Find out exactly what day of the month your credit card “Statement Closes” (you can find this on your PDF statement or by calling the bank). Make a manual payment two days before the statement closes to wipe the balance out. When the bank takes their monthly snapshot to send to the credit bureaus, they will report a beautiful 1% or 0% balance.

2. Request a Strategic Credit Limit Increase

You can lower your percentage without paying off a single dime by expanding the denominator of the equation. Log into your banking app and hit the “Request Credit Limit Increase” button. If the bank raises your limit from $5,000 to $10,000, your $2,500 balance instantly drops from a dangerous 50% utilization down to a pristine 25% utilization.

If you’re new to credit and don’t yet qualify for larger credit limits, Best Secured Credit Cards for Beginners in 2026 compares secured cards that can help you establish positive payment history while working toward higher limits over time.

3. Spread Your Expenses Out

If you have a $3,000 planned expense (like new tires or a medical bill), do not put it all on one card with a low limit. Split the payment across two or three different credit cards. This ensures you avoid a devastating 90% per-card utilization strike on any single account.

High utilization is only one of several mistakes that can lower your score. 10 Credit Score Mistakes That Can Cost You 100+ Points covers additional habits that quietly damage your credit profile.

If you’re looking for a card with healthy credit-building features and reasonable credit limits, Best Credit Cards for Beginners: What Actually Matters explains what to prioritize before applying.

As your credit profile grows, How Many Credit Cards Should You Have for the Best Credit Score? explains how multiple accounts can influence utilization, credit history, and overall score.

Frequently Asked Questions (FAQs)

1. Does a 0% credit utilization ratio hurt my score?

It can. The FICO algorithm wants to see that you are actively using credit responsibly, not just letting accounts sit dormant. An absolute 0% utilization across all your cards can sometimes cause a slight dip in your score. The optimal mathematical target is a 1% to 3% reported balance.

2. How fast will my credit score recover if I pay down my balance?

Incredibly fast. Under standard scoring models, credit utilization has no “memory.” The moment your bank reports your newly paid-off balance to the credit bureaus (which happens once a month), your FICO score will rebound instantly. A drop caused by high utilization is completely reversible within 30 to 45 days.

3. Does credit utilization apply to my mortgage or car loan?

No. Credit utilization strictly measures “revolving” debt, which primarily means credit cards and Home Equity Lines of Credit (HELOCs). Your auto loans, student loans, and mortgages are “installment” loans and are calculated in a completely different sector of the FICO algorithm.

4. Should I carry a small balance month-to-month to build credit?

Absolutely not. This is a massive, highly destructive myth. You never need to pay the bank interest to build your credit score. You should use the card, let the statement close with a small balance to show utilization, and then pay the statement balance in full before the due date to avoid all interest charges.

5. How do I know when my bank reports my balance to the credit bureaus?

If your reported balances or credit limits look incorrect, How to Read and Fix Errors on Your Credit Report explains how to review your reports and dispute inaccurate information.

Most major banks report your balance exactly on your Statement Closing Date (not your payment due date). You can confirm this by pulling a free copy of your credit report from AnnualCreditReport.com and looking at the “Date Updated” or “Date Reported” section under your specific credit card tradeline.

The Bottom Line

Understanding the math behind credit utilization is the difference between an average credit score and an elite financial reputation.

Stop aiming for the 30% ceiling and start engineering your cash flow to hit the 10% elite threshold. Pay attention to your statement closing dates, monitor your per-card ratios, and never close your oldest accounts. By treating your credit limit as a boundary rather than a spending target, you guarantee access to the absolute best interest rates the financial sector has to offer.

Credit Education Resources

Understanding credit utilization is one of the fastest ways to improve your credit score. These trusted resources explain how utilization is calculated, how it affects lending decisions, and how to build healthy long-term credit habits.

- FICO® – What’s in Your FICO® Score? – Learn how credit utilization, payment history, and other factors contribute to your FICO® Score.

- Consumer Financial Protection Bureau (CFPB) – Credit Reports and Scores – Official guidance on how credit scores work, how credit information is reported, and what lenders evaluate.

- Experian – Explore educational articles on credit utilization, statement balances, credit reports, and practical strategies for improving your credit profile.

- Equifax – Learn how credit utilization, revolving balances, and responsible credit management influence your overall credit health.

- AnnualCreditReport.com – Request your free credit reports from Equifax, Experian, and TransUnion to monitor account balances, payment history, and reported credit limits.

- VantageScore® – Learn how the VantageScore credit scoring model evaluates credit behavior, including credit utilization and payment history.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.