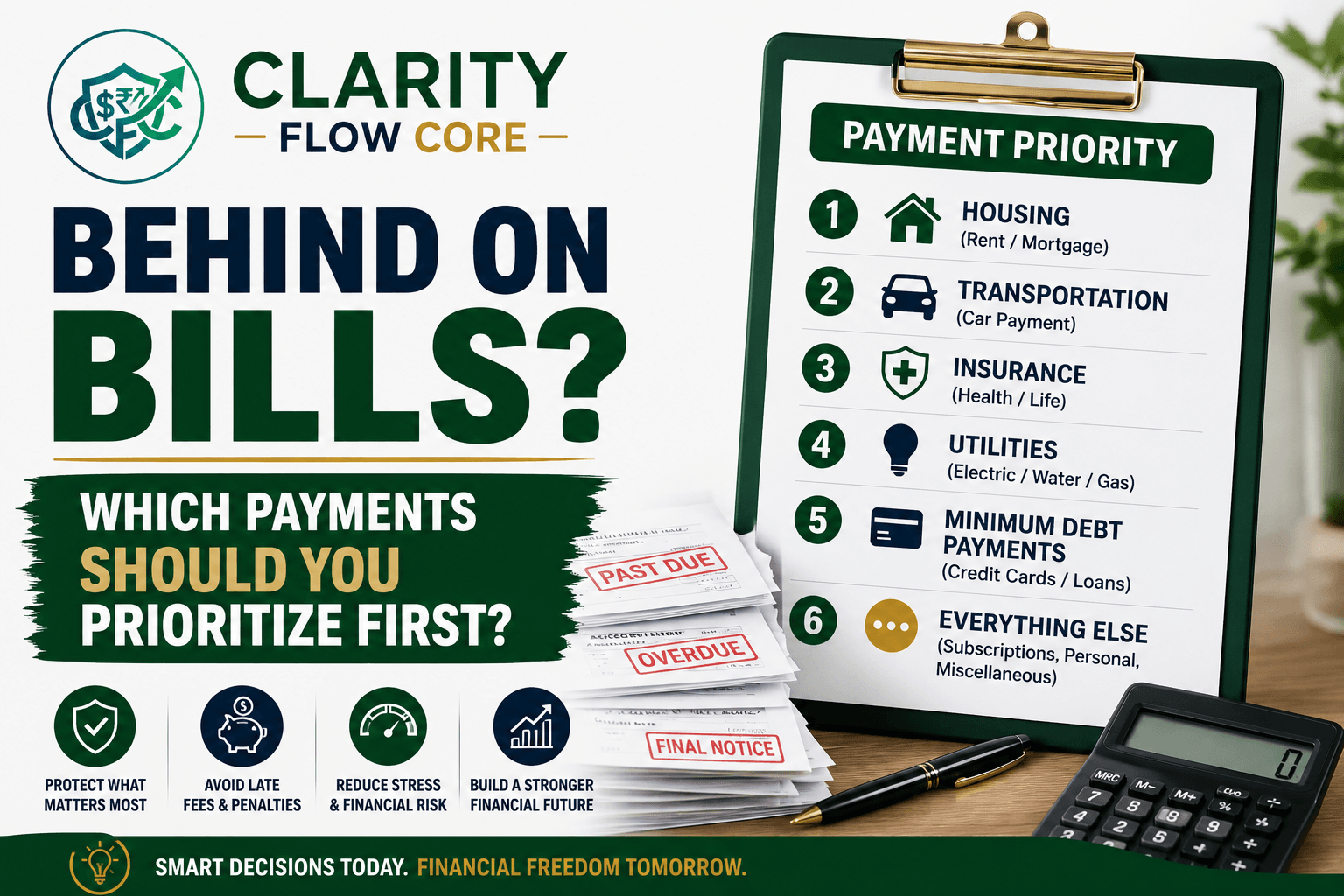

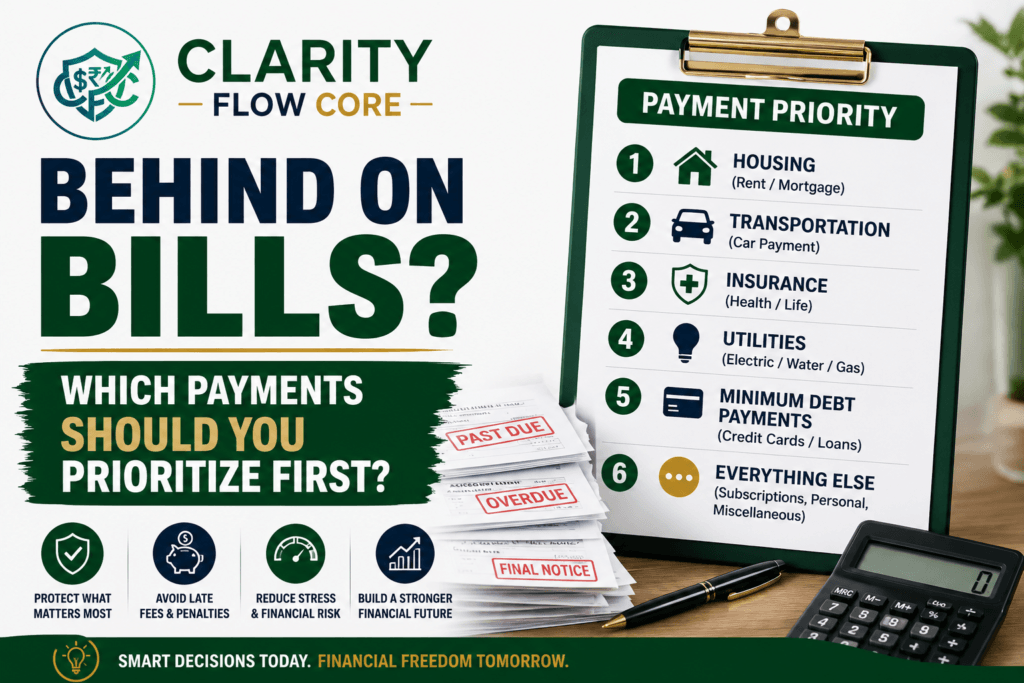

Behind on Bills? Which Payments Should You Prioritize First?

It is 2:00 AM, and you are staring at the ceiling. If you are behind on bills and doing that terrible, frantic math we all know too well, take a deep breath. You have $800 in your checking account, but your rent, your car payment, the electric bill, and two credit card minimums add up to $1,400.

There simply is not enough money to go around this month.

If you are feeling a tight knot of panic in your stomach right now, take a deep breath. You are not alone. Millions of hardworking people find themselves in this exact situation every single year. You are not a failure, you are not bad with money, and this temporary crisis does not define your future.

The Reality of Financial Hardship in the US

According to the Federal Reserve, many Americans would struggle to cover an unexpected $400 expense using cash savings alone. You are experiencing a systemic, common issue—not a personal moral failing.

Whether your hours got cut at work, you were hit with a massive unexpected medical bill, or maybe you are a freelance worker and your biggest client is 30 days late on paying an invoice, the reality is the same: the numbers simply don’t work.

When you don’t have enough money to pay everyone, you are forced into a corner. You have to choose who gets paid and who gets ignored. Making those choices based on fear, pressure, or guilt is the fastest way to make a bad situation significantly worse.

Today, we are going to take the heavy emotion out of it. We are going to build a strategic, realistic plan so you know exactly which bills to pay first, which ones can wait, and how to protect yourself while you get back on your feet.

The Real Problem: Why We Fall Behind

Before we fix the problem, we have to understand the reality of why it happens. Financial stress rarely happens because someone bought too many fancy coffees or avocado toasts. It happens because life is wildly unpredictable and increasingly expensive.

For many normal people, income is not perfectly stable. If you work for tips, run a side hustle, or do freelance work, your paychecks bounce up and down. When a slow month collides with rising grocery prices and climbing rent, the safety net snaps.

There is an intense emotional weight that comes with this. When the bills start piling up, shame sets in. You might start ignoring your mail. You might send all calls from unknown numbers straight to voicemail because you know it is a collector on the other end. Avoidance is a natural human trauma response, but in the financial world, avoidance only adds late fees and interest to your original problem.

The Panic Trap: Common Mistakes to Avoid

When the money runs out, panic takes the steering wheel. If you are stressed, you are highly likely to make one of these three common survival mistakes.

Mistake 1: Paying the Loudest Debt Collector First

Credit card companies and collection agencies are incredibly aggressive. They will call you three times a day, send threatening letters, and make you feel like the world is ending. Because they are the “loudest” problem, many people empty their bank accounts to pay a credit card minimum just to make the phone stop ringing. Meanwhile, they short their rent payment. This is incredibly dangerous. A credit card company cannot kick you out of your house; a landlord can. If you are worried about the long-term math of ignoring those cards, read our guide on What Happens If You Only Pay the Minimum on a Credit Card? so you understand exactly what you are up against.

Mistake 2: Draining Your Savings for Non-Essentials

If you have a tiny reserve left, it is tempting to use it to keep every single subscription, credit card, and loan current so your credit score doesn’t drop. But if you drain your last $500 to pay a Visa bill, and then your car needs a new battery so you can get to work, you are completely stuck. Your cash reserves are for survival, not for appeasing creditors. (If you want to understand how to build and protect these reserves in the future, check out Emergency Fund Explained).

Mistake 3: Putting Rent on a High-Interest Credit Card

It feels like a clever loophole. You don’t have the cash for rent, so you use a third-party service to charge your rent to your credit card. While this keeps a roof over your head this month, you are usually hit with a 3% transaction fee, plus the 25% interest rate of the credit card. You are essentially taking out a high-interest payday loan to pay your landlord, which almost guarantees you will be in a deeper hole next month.

The “Four Walls” Survival Strategy

When you are financially drowning, you have to stop worrying about your credit score and start worrying about your actual physical survival.

In personal finance, there is a concept known as the “Four Walls.” Think of your life as a house. If the four walls fall down, you cannot survive. Everything else inside the house—the TV, the furniture, the decorations—is secondary.

When you are short on cash, your income must cover the Four Walls before a single penny goes anywhere else. Period.

Wall 1: Food

You and your family have to eat. This is priority number one. However, this does not mean dining out, ordering delivery, or buying premium organic snacks. This means a bare-bones, survival grocery budget. Think rice, beans, frozen vegetables, pasta, and cheap proteins.

If you literally cannot afford groceries, please leave your pride at the door. Visit a local food bank or apply for SNAP (Supplemental Nutrition Assistance Program) benefits. That is exactly what those programs are there for. Protecting your food budget ensures you have the energy and health to figure out the rest of your financial mess.

Wall 2: Shelter

You must keep a roof over your head. Your rent or your mortgage is the most critical bill you have. If you pay your credit cards but get evicted, your life is going to become infinitely more difficult.

If you are a homeowner, missing a mortgage payment is scary, but the foreclosure process is long. Take a deep breath and read What Happens If You Miss a Mortgage Payment? to understand your timeline. That being said, keeping your mortgage current protects your equity and your living situation. If you rent, evictions can happen rapidly depending on your state laws. Always prioritize your landlord or your mortgage lender over everyone else.

Wall 3: Basic Utilities

A house is unlivable if the lights are off, the water stops running, and there is no heat in the winter. You need your basic utilities to cook your food, keep your family warm, and maintain basic hygiene.

Notice the word basic. Electricity, water, and gas are basic utilities. High-speed fiber-optic internet, premium cable packages, and five different streaming services are not basic utilities. If you are working from home or applying for jobs, a basic internet connection is required, but you should downgrade to the cheapest possible plan immediately.

Wall 4: Transportation

You need to be able to get to work to make the money required to dig yourself out of this hole. Therefore, transportation is your fourth wall.

This means paying your auto loan so the car doesn’t get repossessed. It means keeping basic liability auto insurance so you don’t lose your license or get sued in an accident. And it means keeping enough cash on hand to put gas in the tank. If you live in a major city with excellent public transit, your “transportation wall” might just be a monthly subway pass, which frees up hundreds of dollars in your budget.

Tier 2: Important, But Not Critical

If—and only if—you have completely secured your Four Walls, you can look at the money you have left over. Any remaining funds should fall to Tier 2 priorities. These are things that are highly important for your stability but won’t leave you homeless or starving if they are delayed.

Childcare: If you need day care so you can physically go to your job and earn an income, this borders on being a “Wall.” You cannot lose your job because you have no one to watch your kids.

Essential Insurances: Health insurance and life insurance. Letting health insurance lapse is a massive gamble in the US healthcare system. A single trip to the emergency room without insurance will create a financial disaster that takes decades to fix.

Child Support: The government takes child support incredibly seriously. If you fail to pay it, they can garnish your wages, intercept your tax returns, or even suspend your driver’s license, which directly impacts your ability to earn a living.

Tier 3: The Bottom of the Barrel (Unsecured Debt)

This is the hardest pill to swallow, but it is the most important part of this strategy.

If you have paid for your food, shelter, utilities, and car, and your bank account is now at zero, everyone else has to wait.

What falls into Tier 3? Credit card bills, personal loans, gym memberships, and store charge cards.

These are called “unsecured debts.” They are unsecured because there is no physical asset tied to the loan. If you don’t pay your car loan, they take the car. If you don’t pay your credit card, they cannot come to your house and repossess the groceries and clothes you bought with it.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyThe Bill Prioritization Table

To make this completely clear, here is the exact hierarchy of how your money should flow when you are in a crisis.

| Priority | Bill Type | Consequence If Missed |

| 1 | Food | Immediate hardship |

| 2 | Rent/Mortgage | Eviction/Foreclosure risk |

| 3 | Utilities | Service shutoff |

| 4 | Transportation | Can’t get to work |

| 5 | Child Support | Legal consequences |

| 6 | Health Insurance | Financial risk |

| 7 | Credit Cards | Credit score damage |

| 8 | Medical Bills | Collections later |

| 9 | Personal Loans | Collections later |

What About Medical Bills?

You might have noticed medical bills sitting near the bottom of that table, and that often makes people nervous. Hospitals and doctors send very intimidating invoices. But here is the reality of medical debt:

- Hospitals almost always offer flexible payment plans if you call and ask.

- Many nonprofit hospitals have financial assistance programs (sometimes called “charity care”) that can legally forgive your bill entirely if your income is low enough.

- Medical bills usually aren’t an immediate housing or utility emergency. They won’t freeze your bank account tomorrow.

- Don’t skip rent to pay a hospital bill.

If you are currently drowning in invoices from a recent hospital visit, stop stressing and read our comprehensive guide on What To Do If Medical Bills Are Destroying Your Budget.

Real Consequences: What Actually Happens When You Don’t Pay?

Anxiety usually stems from the unknown. When you don’t know what is going to happen, your brain imagines the absolute worst-case scenario. Let’s ground ourselves in reality and look at what actually happens when you miss payments.

If you miss a credit card payment:

At 30 days late, the credit card company reports you to the credit bureaus. Your credit score will take a sharp hit. You will be charged a late fee (usually around $35). At 60 and 90 days, the calls will increase. At 180 days, they will “charge off” the debt and sell it to a collection agency. You will not go to jail for missing a credit card payment. It is a civil matter, not a criminal one.

Once your debt is sold to a collection agency, your strategy needs to change. Before responding to collection calls or agreeing to any payment plan, read How To Handle Debt Collectors Without Making Things Worse to understand your rights and avoid common mistakes.

If you miss a car payment:

Auto lenders don’t mess around. Depending on your state, a lender can technically repossess your car the day after you miss a payment, though most usually wait 30 to 90 days. Once the car is gone, you still owe the balance on the loan, plus the towing and storage fees. This is why the car payment is part of your Four Walls.

If you miss a utility bill:

Power and water companies usually give you a grace period. Before they shut off your services, they are required by law to send you a shut-off notice, usually giving you 10 to 15 days of warning.

Your Beginner-Friendly Action Plan for This Month

Reading about strategy is great, but let’s turn this into an actual, physical checklist you can execute today to regain control.

Quick Bill Priority Checklist

✅ Food

✅ Rent/Mortgage

✅ Utilities

✅ Transportation

⬜ Credit Cards

⬜ Medical Bills

⬜ Personal Loans

⬜ Subscriptions

Step 1: Triage Your List

Grab a piece of paper. On the left side, write down all the money you currently have to your name. On the right side, list every single bill that is due this month. Now, take a red pen and cross out anything that is not Food, Shelter, Utilities, or Transportation.

Step 2: Calculate the Gap

Subtract your Four Walls from your available cash. Even if you have to miss payments on unsecured debt, keeping your housing, utilities, food, and transportation intact gives you the foundation needed to recover financially.

Calculator Suggestion: Use a free online Budget Planner tool to map out exactly how much cash you need to hit that minimum survival number.

If your cash covers the Four Walls, you are going to be physically okay this month. Take a breath. If it doesn’t, you have an extreme income emergency and need to sell things around the house or pick up gig work immediately.

Step 3: Make the Hard Phone Calls

Do not ghost your creditors. Pick up the phone, call the companies you cannot pay, and read this exact script:

“I am currently experiencing a severe financial hardship. I cannot make my minimum payment this month. Are there any hardship programs, forbearance options, or skipped-payment plans available for my account?”

You would be shocked at how many companies have hidden hardship programs. Utility companies often have budget billing or low-income assistance programs. Credit card companies might lower your interest rate or pause your payments for 60 days without reporting you as late if you ask before you miss the payment.

Step 4: Stop the Bleeding

Go through your bank statements for the last 30 days. Cancel every single recurring subscription. Netflix, Spotify, the gym you haven’t been to in three months, the software you forgot you subscribed to. Every $15 you get back is gas in your car or food on your table.

Frequently Asked Questions (FAQs)

Should I borrow from family to pay bills?

Proceed with extreme caution. Borrowing money from family changes the dynamic of your relationship. If you borrow money to pay an unsecured debt (like a credit card) and then later can’t pay your family member back, you have ruined a Thanksgiving dinner over a Visa bill. Only consider family loans for absolute emergencies (like keeping a roof over your head), and always put the repayment terms in writing.

Should I use a balance transfer card to cover overdue bills?

A 0% APR balance transfer card can be a great tool if your income is stable and you just need breathing room from high interest rates. However, if you are actively behind on bills because you simply do not make enough money to survive, opening new credit is a dangerous game. You are likely to max out the new card and double your problem.

Should I use a payday loan to cover my bills?

Absolutely not. Under no circumstances should you ever take out a payday loan. The interest rates can exceed 400%, trapping you in a cycle of debt that is mathematically almost impossible to escape from. It is better to deal with a late fee from a creditor than to sign a contract with a payday lender.

Can debt collectors show up at my work or home?

The Fair Debt Collection Practices Act (FDCPA) gives you rights. Debt collectors cannot legally harass you, threaten you with violence, or lie to you. If they call you at work and you tell them your employer doesn’t allow such calls, they must stop calling you there by law. They are not police officers, and they cannot arrest you.

Will missing one payment ruin my credit score forever?

No. A late payment will sting your credit score significantly in the short term, but its impact fades over time. Credit scores are fluid. Once you get back on your feet and resume on-time payments, your score will eventually recover. Do not let the fear of a temporary credit score drop dictate your survival.

A Final Word

Financial stress is exhausting. It drains your energy, strains your relationships, and makes you feel like you are trapped in a room with no doors.

But you have to remember that this is just math. It is just numbers on a screen. By prioritizing your Four Walls, you are taking the power back. You are making sure that no matter how loud the phone rings or how many angry letters arrive in the mail, you are safe, you are fed, and you have a place to sleep.

Give yourself some grace this month. Make a bare-bones budget, cut out the noise of the unsecured creditors, and focus on generating income and protecting your physical well-being. It is going to take time, and it is going to be uncomfortable, but you have the strength to weather this storm.

If you’re struggling because of a recent job loss, read our guide on I Lost My Job: A 30-Day Financial Survival Plan. If debt collectors are already contacting you, learn How To Handle Debt Collectors Without Making Things Worse.

Sources & References

- Consumer Financial Protection Bureau (CFPB) – Managing Debt – Learn practical strategies for prioritizing bills, communicating with creditors, and navigating financial hardship.

- Federal Trade Commission (FTC) – Coping with Debt – Official guidance on dealing with financial hardship, prioritizing payments, and avoiding debt relief scams.

- Federal Reserve – Report on the Economic Well-Being of U.S. Households – Annual research on emergency savings, financial resilience, and how Americans manage unexpected expenses.

- Benefits.gov – Find federal and state assistance programs, including SNAP, utility assistance, housing support, and other benefits available during financial hardship.

- National Foundation for Credit Counseling (NFCC) – Access nonprofit credit counseling, budgeting assistance, and Debt Management Plan (DMP) resources.

- Consumer Financial Protection Bureau (CFPB) – Mortgage Help – Information on mortgage payment assistance, foreclosure prevention, and communicating with your mortgage servicer if you’re struggling to make housing payments.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.