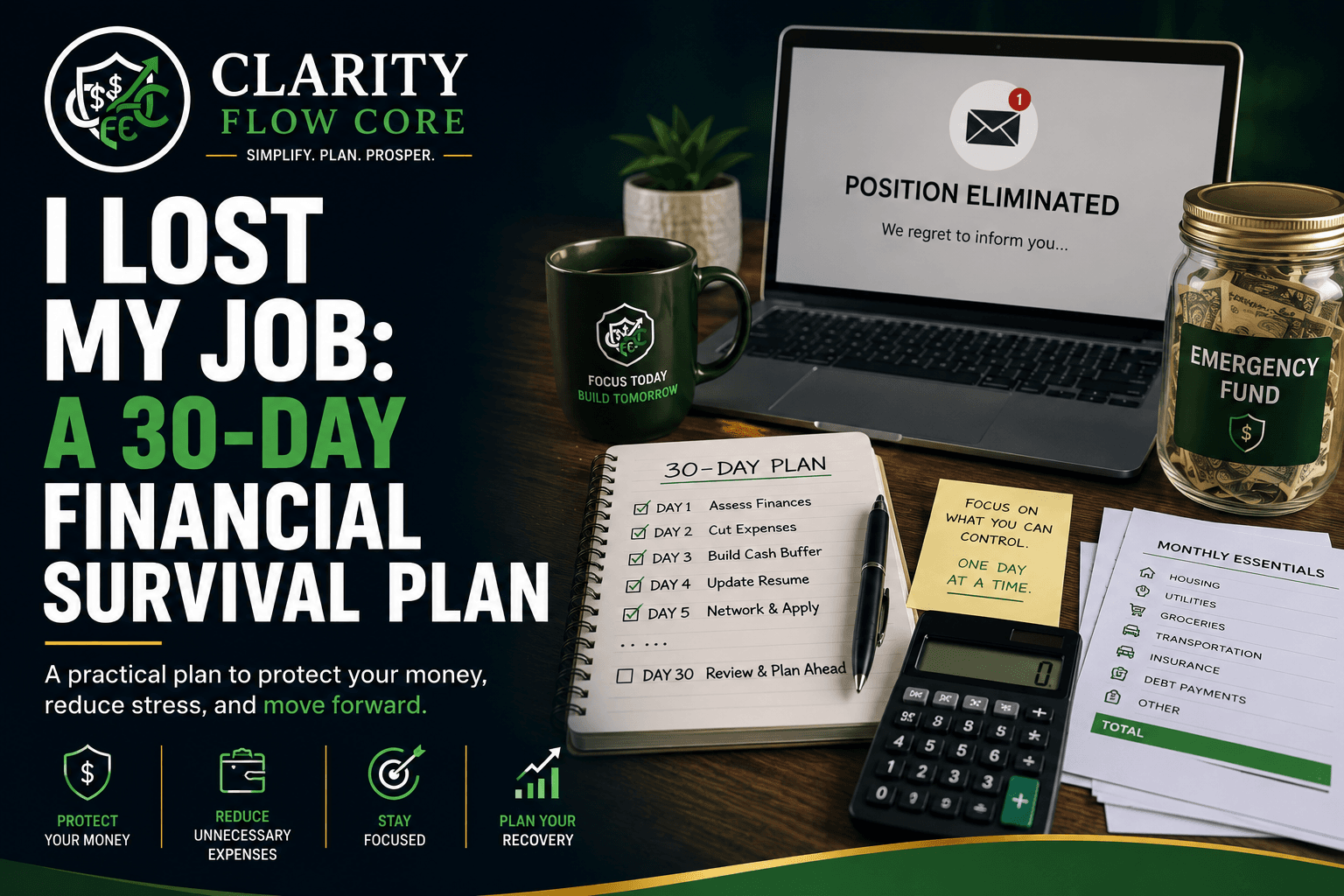

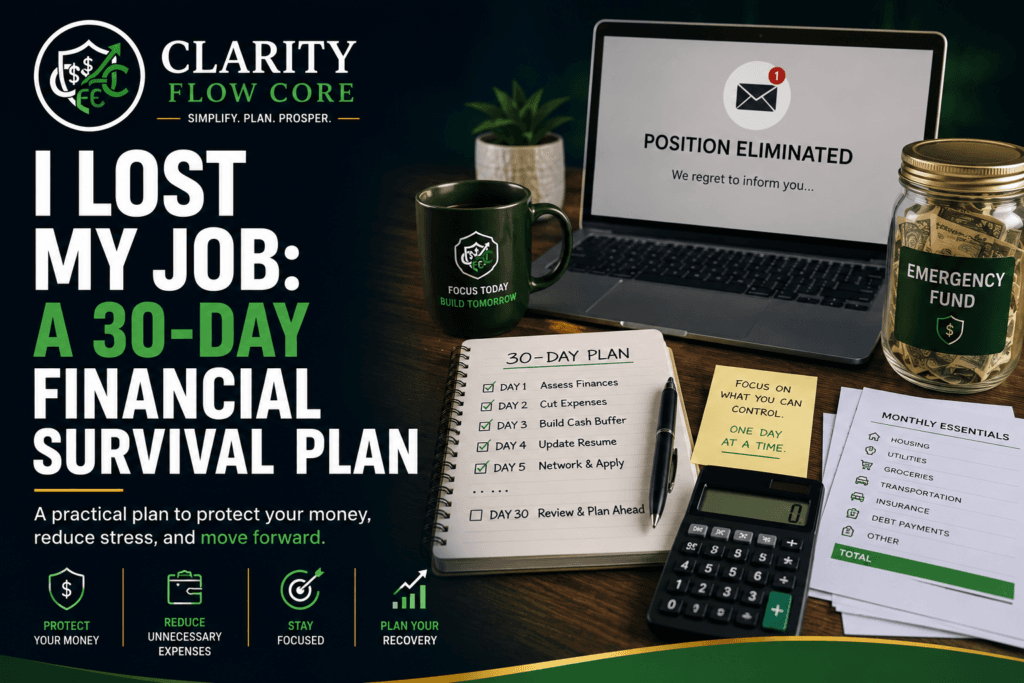

I Lost My Job: A 30-Day Financial Survival Plan

Getting fired, laid off, or suddenly let go feels like the floor just dropped completely out from under you.

You log out of your email for the last time, pack up your desk, and maybe sit in your car just staring at the steering wheel for a good twenty minutes. The shock is physical. Your stomach is in knots, and the very first thought looping in your head is usually some variation of: How on earth am I going to pay my rent?

If you are reading this right now, take a deep breath.

Losing your job is one of the most stressful life events a person can go through. It is entirely normal to feel anxious, embarrassed, angry, or completely overwhelmed. If you feel completely unprepared, you aren’t alone—data consistently shows that over 60% of Americans live paycheck to paycheck, and more than half couldn’t cover a sudden $1,000 emergency with cash.

Right now, panic is your biggest enemy. Panic makes us hide from our bank accounts, ignore our bills, and make impulsive money decisions that haunt us for years.

You don’t need a magical quick fix. You need a practical, step-by-step strategy to stop the financial bleeding and buy yourself time. Consider this your 30-day financial survival plan. We are going to break down exactly what you need to do to protect your cash, handle your bills, and keep your life stable while you figure out your next career move.

The “First 24 Hours” Checklist: What to Do When You Lose Your Job

Before we build your 30-day plan, here is exactly what you need to do in the first 24 hours. Don’t think about next month yet; just check these immediate boxes:

- ✓ Save your HR termination paperwork.

- ✓ Download your recent pay stubs. (You will lose access to the company portal faster than you think).

- ✓ Save your health insurance information. (Download your group numbers and plan details).

- ✓ Review any severance packages. (Read them thoroughly, but do not sign anything on the spot—you usually have a few days to review).

- ✓ Confirm your unused PTO payout. (Check your state laws and employee handbook to see if you will be paid for unused vacation days).

- ✓ Update your LinkedIn profile. (Turn on the “Open to Work” feature quietly to recruiters).

Phase 1: Days 1 to 3 (The Assessment & Protection Phase)

The first 72 hours after losing your job are mostly about emotional management and basic damage control. Do not immediately start applying for 500 jobs in a blind panic. You need to secure your safety net first.

File for Unemployment Immediately

This is the single biggest mistake people make. They wait. Sometimes it is out of pride—they think, “I’ll find a job next week, I don’t need government help.” Other times, it is just confusion about the system.

Here is the reality: you paid into the unemployment insurance system out of every paycheck you ever earned. It is your money, and it is there for exactly this scenario.

In the United States, unemployment systems are run by individual states, and almost all of them have a “waiting week.” That means you will not get paid for the first week you are unemployed, no matter what. Furthermore, it can take two to three weeks for your claim to be processed and for the money to actually hit your bank account.

If you wait two weeks to file, you are pushing your first check an entire month into the future. Go to your state’s Department of Labor website today, fill out the application, and get the clock started.

Calculate Your Runway

Once the unemployment application is in, you need to look at the math. Sit down and write down exactly how much liquid cash you have right now. Readers often skip this because it is scary, but seeing the real numbers gives you a sense of control.

If you have:

- $2,500 in your checking account

- $4,000 in your savings account

- $1,500 coming from your final paycheck and severance

Your total cash survival fund is $8,000. Do not include your 401(k) or investments yet. We are only looking at cash you can access tomorrow without paying a penalty.

Once you’re employed again, reviewing your overall debt burden is a smart next step. How Much Debt Is Too Much? A Simple Debt-to-Income Ratio Guide explains how lenders evaluate your financial obligations.

The Quick Runway Formula

Now that you know your cash total, you need to figure out exactly how long that money will last. You do this by calculating your “runway.”

First, add up your Monthly Essentials (we will talk more about cutting non-essentials in Phase 2):

- Rent or Mortgage: $1,200

- Food & Groceries: $350

- Utilities & Phone: $200

- Transportation/Gas: $250

- Total Bare-Bones Budget: $2,000/month

Now, apply the simple runway formula: $8,000 (Cash Available) ÷ $2,000 (Monthly Essentials) = 4 Months of Runway.

Knowing you have exactly four months to find a job takes a massive weight off your chest.

📌 Related Guide: Emergency Fund Basics: How Much Cash Should You Keep?

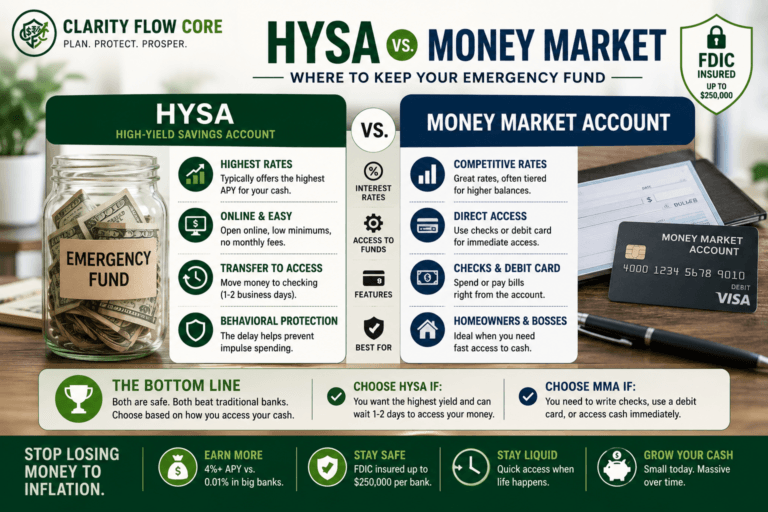

If you don’t already have an emergency fund, storing it in the right account can help it grow while remaining easily accessible. How to Choose Your First High-Yield Savings Account explains what to look for before opening an account.

⚙️ Free Tool: Check our Emergency Fund Analyzer to calculate your exact financial runway and see exactly how long your savings will last.

Phase 2: Days 4 to 10 (Building the Bare-Bones Budget)

Now that you know your runway, your goal is to stretch it as far as humanly possible. When you have a steady paycheck, you operate on a “lifestyle budget.” When you lose your job, you must immediately switch to a “bare-bones budget.”

Once your income returns, rebuilding your finances becomes much easier with a structured spending plan. The 50/30/20 Budget Rule Explained Simply provides a simple framework for balancing necessities, savings, and discretionary spending.

If you were planning to move into your own apartment before losing your job, now is the time to pause and reassess your finances. Our guide How Much Should You Save Before Moving Out on Your Own? explains the savings you’ll want in place before taking on rent and other living expenses independently.

Secure the “Four Walls” First

When money is tight, you prioritize the Four Walls:

- Food: Basic groceries. Not takeout, not restaurants, just what you need to eat at home.

- Housing: Your rent or mortgage payment.

- Utilities: Electricity, water, and essential internet (you need the internet to job hunt).

- Transportation: Enough gas to get to interviews or a side hustle, plus basic car insurance.

If a bill does not fall into one of these four categories, it goes to the bottom of the priority list. That random subscription box? Canceled.

If you’re unsure which bills should be paid first when money is limited, Behind on Bills? Which Payments Should You Prioritize First? explains how to protect your essentials while minimizing long-term financial damage.

The Subscription Purge

Log into your bank account and look at the last 30 days of transactions. Cancel the streaming services, the gym membership, the premium app subscriptions, and the meal kit deliveries.

People often resist this step. They think, “It’s only $15 a month, and I need some entertainment to stay sane.” The problem isn’t just the $15. The problem is the psychological shift. By cutting these expenses, you are signaling to your brain that you are in a financial emergency and you need to act accordingly. You can always resubscribe the exact minute you sign an offer letter for your next job. For now, pause everything.

Building better spending habits now can make your emergency savings last much longer. 7 Everyday Saving Habits That Can Make a Real Difference covers practical ways to reduce expenses without feeling deprived.

Phase 3: Days 11 to 20 (Dealing with Creditors and Debt)

This is the phase that gives people the most anxiety. If your bare-bones budget reveals that you don’t have enough cash to cover your credit card bills, your auto loan, or your student loans, you have to face the music.

Never Ghost Your Lenders

The absolute worst thing you can do when you can’t pay a bill is to ignore it. Throwing past-due notices into a drawer and ignoring phone calls from the bank will destroy your credit score and add hundreds of dollars in late fees to your balances.

If you’re worried about the long-term impact of missing payments, How Long Do Late Payments Stay On Your Credit Report? explains how long late payments remain on your credit history and how recovery works.

If your missed payments eventually lead to collection agencies contacting you, How To Handle Debt Collectors Without Making Things Worse explains how to communicate with collectors, verify debts, and protect your rights.

Banks and lenders deal with job loss every single day. They have systems in place for this, but they can only help you if you talk to them before you miss a payment.

The Hardship Phone Call Script

Call the customer service number on the back of your credit card or loan statement. When you get a human on the line, use a variation of this script:

“Hi, I have been a loyal customer for a while, but I recently lost my job unexpectedly. I am calling to see what hardship programs you have available. I want to keep my account in good standing, but I need to temporarily pause or reduce my payments while I secure new employment.”

Many credit card companies and auto lenders will offer forbearance (letting you skip a month or two of payments) or waive late fees if you explain your situation early. It feels embarrassing to make this call, but the customer service representative is just a regular person sitting in a cubicle. They do not judge you. They just click a button on their screen to authorize the hardship program.

⚙️ Free Tool: Check our Credit Utilization Calculator & Recovery System to map out your balances.

Phase 4: Days 21 to 30 (Healthcare and Income Bridging)

By the third week, your bare-bones budget is running, your creditors have been contacted, and your unemployment is hopefully processing. Now, we look at keeping you afloat long-term. The average unemployment duration in the US hovers around three to five months, so you need a plan for the long haul.

The Health Insurance Dilemma

In the US, health insurance is tragically tied to employment. If you lost your benefits, you will likely receive a packet in the mail about COBRA.

COBRA allows you to stay on your former employer’s health insurance plan, but there is a massive catch: you now have to pay the entire premium yourself, including the portion your employer used to cover. For many people, COBRA costs upwards of $600 to $800 a month just for a single person.

Do not blindly sign up for COBRA. Losing your job counts as a “Qualifying Life Event,” which means you are legally allowed to enroll in a new health insurance plan through the government marketplace (Healthcare.gov) outside of the normal enrollment period. Because your income has drastically dropped, you will likely qualify for heavy subsidies that make marketplace insurance significantly cheaper than COBRA.

What Happens to Your FSA and HSA?

If you have a Flexible Spending Account (FSA), that money is usually tied to your employer. If you don’t spend it before your termination date (or the end of your coverage month), you lose it entirely. If you have funds sitting there, go buy new glasses, schedule a dental cleaning, or restock your medicine cabinet immediately.

A Health Savings Account (HSA), however, is yours to keep forever. You can use that tax-free money to pay for medical expenses, prescriptions, or even COBRA premiums while you are unemployed.

Can You Keep Your Doctor?

This is a massive fear for people switching off their employer plan. If you switch to a marketplace plan, your current doctor might not be in-network. Before you purchase a Healthcare.gov plan, call your doctor’s office directly and ask exactly which marketplace insurance plans they accept. Do not assume; verify with the front desk.

Generating “Bridge Income”

While you are interviewing for your next full-time role, consider finding bridge income. This isn’t a career move; it is just a way to keep cash flowing into your checking account so you don’t have to rack up credit card debt.

This could mean:

- Taking a temporary retail or warehouse job.

- Driving for a rideshare or delivery service.

- Offering freelance skills online (like graphic design, writing, or video editing).

Be aware of how bridge income interacts with your state’s unemployment benefits. In many states, you can work part-time and still collect partial unemployment, but you must report your earnings truthfully.

📌 Related Guide: 1099 Taxes Explained for Freelancers and Side Hustlers.

3 Massive Beginner Mistakes to Avoid During Job Loss

When people are scared about money, they often make rash decisions to feel secure in the short term, accidentally destroying their financial future in the process. Avoid these three traps at all costs.

1. Raiding Your 401(k) or Retirement Accounts

When you see your checking account dwindling, it is incredibly tempting to look at your retirement account and think, I have $20,000 sitting right there.

Do not touch it unless you are literally facing eviction and homelessness.

If you withdraw money from a traditional 401(k) or IRA before age 59½, the IRS will hit you with a 10% early withdrawal penalty. On top of that, the money you withdraw is taxed as regular income. If you pull $10,000 out to cover your bills, you might lose 20% to taxes and 10% to penalties. You will only walk away with $7,000 in your pocket. Worse, you just robbed your future self of decades of compound interest. Leave the retirement money alone.

2. Using Credit Cards to Maintain Your Lifestyle

It is very easy to swipe your credit card for dinners out, new clothes, or weekend trips while telling yourself, “I’ll pay it all off as soon as I get a new job.”

Job hunts often take much longer than we anticipate. If you rack up $5,000 in credit card debt at a 24% interest rate, that debt will act like an anchor dragging you down long after you find a new job. A credit card is a tool, not an emergency fund.

Relying on minimum payments for extended periods can become extremely expensive. What Happens If You Only Pay the Minimum on a Credit Card? shows how interest compounds and why balances become so difficult to eliminate.

3. Paying Off Debts in the Wrong Order

If you receive a little bit of severance pay, you might be tempted to make a massive payment on your credit card just to clear the balance and feel productive.

If you don’t have a fully funded emergency savings account, do not do this. Cash is king when you are unemployed. You cannot pay your rent with a credit card. Keep your cash in the bank to cover your Four Walls, and only make minimum payments on your debts until your income is stable again.

If making only minimum payments is your only option for now, I Can Only Afford the Minimum Payments — Now What? explains how to minimize the damage while you rebuild your income.

📌 Related Guide: What Happens If You Missed Credit Card Payment?

Frequently Asked Questions (FAQs)

How long does it take to get my first unemployment check? In most US states, it takes a minimum of two to three weeks to receive your first payment after filing. This includes a mandatory one-week waiting period and the time it takes the state to process and verify your claim with your former employer.

Should I use my emergency fund right away? Yes, this is exactly what an emergency fund is built for. However, you should still cut your expenses down to a bare-bones budget immediately to make that emergency cash last as many months as possible.

Once you’re back on your feet financially, How Much Emergency Fund Do You Really Need? can help you rebuild the right-sized emergency fund based on your income and monthly expenses.

Do I have to pay taxes on unemployment benefits? Yes. Unemployment benefits are considered taxable income by the federal government. When you apply, you can choose to have a percentage of taxes withheld from your weekly checks upfront so you aren’t hit with a massive tax bill in April.

Can my credit card company lower my interest rate if I lost my job? Often, yes. If you call and ask for a hardship program, lenders will frequently offer a temporarily reduced interest rate or allow you to defer payments for 30 to 60 days to keep your account from going into default.

A Final Word of Encouragement

Losing your job is a massive blow to the ego. Our society incorrectly ties our personal worth to our job titles and our paychecks.

When the dust settles, remember this: You are not your job. A layoff is a business decision made on a spreadsheet, not a reflection of your character, your talent, or your value as a human being.

Financial stress will try to convince you that everything is falling apart. By taking immediate control of your cash flow, setting up a survival budget, and dealing with your lenders honestly, you are taking your power back. It will be tight, and it will require some uncomfortable sacrifices for a few months, but you can navigate this. Take it one day at a time, protect your Four Walls, and give yourself the grace to figure out your next step.

When your income stabilizes again, rebuilding your savings should become one of your highest priorities. How to Build a $10,000 Emergency Fund: Step-by-Step provides a practical roadmap for getting there.

Job Loss & Financial Recovery Resources

Losing a job can affect everything from your income and health insurance to your debt payments and emergency savings. These trusted organizations provide guidance on unemployment benefits, healthcare coverage, financial assistance, and consumer protections.

- U.S. Department of Labor (DOL) – Learn about unemployment insurance, worker rights, and employment resources.

- CareerOneStop – Sponsored by the U.S. Department of Labor, this resource helps job seekers find employment opportunities, career training, unemployment information, and local workforce services.

- Healthcare.gov – Explore health insurance options after losing employer coverage, including Special Enrollment Periods and premium subsidies.

- Consumer Financial Protection Bureau (CFPB) – Find guidance on managing debt, communicating with lenders, and navigating financial hardship after a loss of income.

- Benefits.gov – Search for federal and state assistance programs, including food assistance, healthcare, housing support, and other benefits you may qualify for during unemployment.

- National Foundation for Credit Counseling (NFCC) – Access nonprofit credit counseling, budgeting assistance, and debt management resources if you’re struggling financially after losing your job.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.