How to Build Credit From Scratch in 2026

If you have never had a credit card or a loan in your name, you are what lenders call “credit invisible.” When a bank, a landlord, or an auto dealership types your Social Security number into their system, nothing comes back. You do not have a bad credit score; you have no credit score.

While having no debt might feel like a financial victory, operating with zero credit history in the United States is incredibly expensive. Without a credit score, you will be forced to pay massive security deposits just to turn on your electricity, landlords will demand double the standard rent deposit, and if you need to buy a car, you will be handed predatory interest rates upwards of 20%.

⚡ Quick Answer

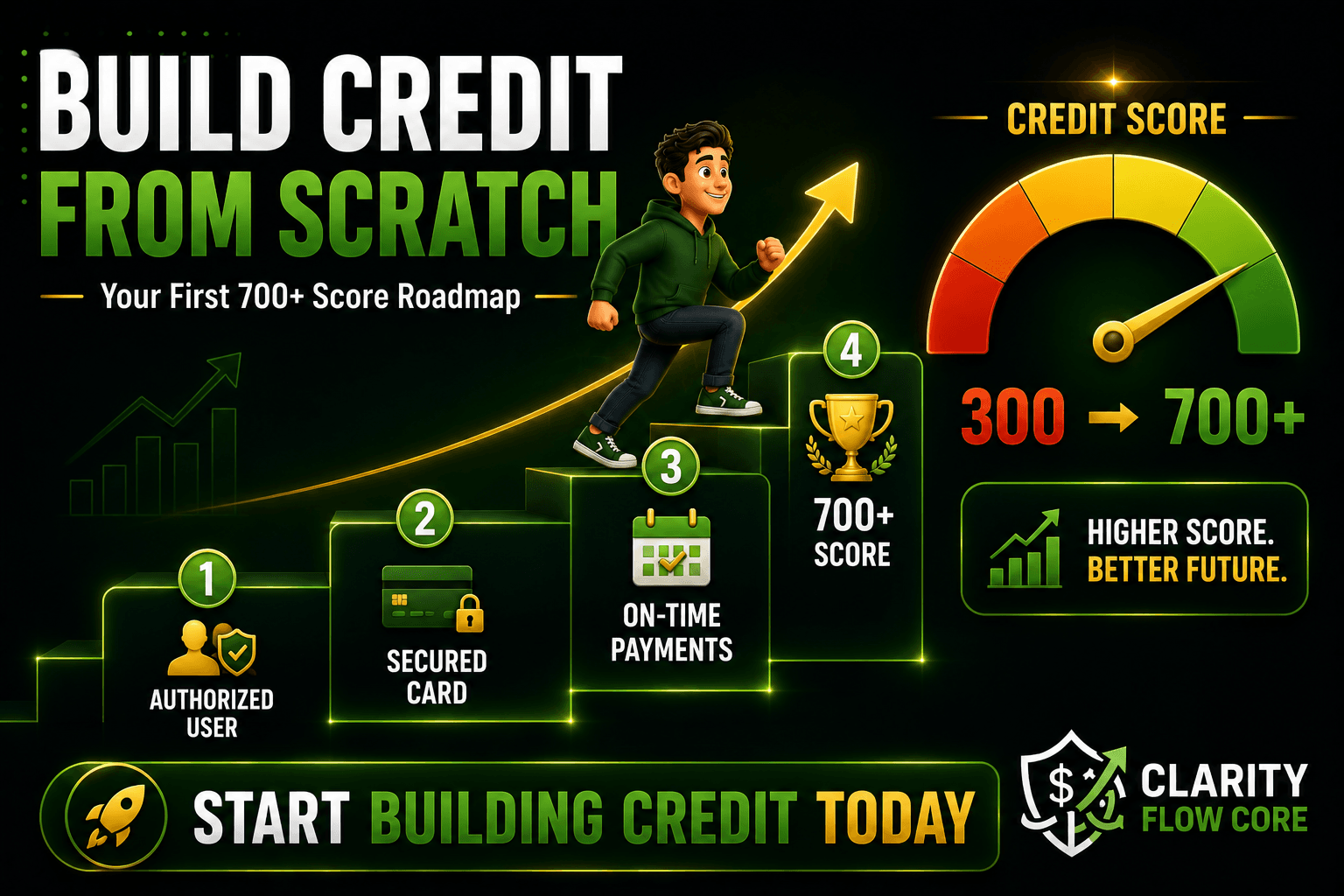

To build credit from scratch, start by becoming an Authorized User on a trusted family member’s credit card to instantly inherit their positive payment history. Next, open a Secured Credit Card by placing a small cash deposit, use it for small everyday purchases, and pay the statement balance in full every single month. Within six months, you will generate your first official FICO credit score.

Learning how to build credit from scratch is not about going into debt. It is about proving to the financial system that you are a reliable, trustworthy borrower. In this comprehensive guide, we will break down the exact mathematical formula behind your credit score, the safest financial products designed for beginners, and the step-by-step timeline you need to follow to achieve an elite 700+ credit score in your first year.

The Core Math: How Your Credit Score is Actually Calculated

Before you apply for a single financial product, you must understand the rules of the game. The dominant scoring model used by 90% of top lenders in the US is the FICO Score. FICO scores range from 300 to 850.

FICO Credit Score Ranges

To know exactly where you stand, here is how lenders classify those numbers:

| Score Range | Rating |

| 300–579 | Poor |

| 580–669 | Fair |

| 670–739 | Good |

| 740–799 | Very Good |

| 800–850 | Exceptional |

If you are starting from zero, the FICO algorithm needs exactly six months of continuous payment data before it will generate your first official score. Once generated, your score is determined by five specific categories. If you optimize these five categories, your score will rise on autopilot.

1. Payment History (35%)

This is the single most important factor. Lenders want to know one thing above all else: Do you pay your bills on time? A single late payment (reported 30 days past the due date) can destroy your credit score overnight and remain on your credit report for seven years. To win this category, you must set every single credit account to autopay.

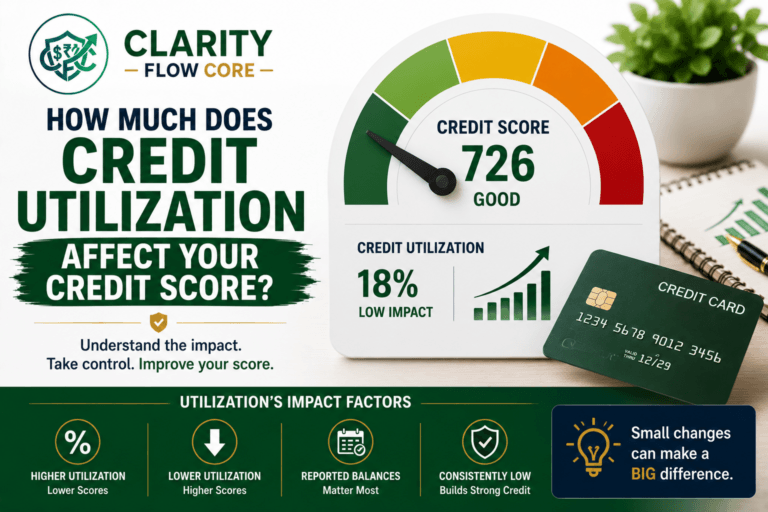

2. Amounts Owed / Credit Utilization (30%)

This measures how much of your available credit you are currently using. If you have a credit card with a $1,000 limit, and you spend $900 on it, your utilization is 90%. To the algorithm, high utilization looks like desperation, and your score will plummet. To achieve a top-tier score, you must keep your reported balance below 10% of your limit.

(To see exactly how your balances manipulate your score, use our Credit Utilization Calculator & Recovery System.)

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My Utilization3. Length of Credit History (15%)

Lenders trust older accounts. The algorithm averages the age of all your open accounts. Because you are building credit from scratch, your average age of accounts is zero. You cannot speed this up; you simply have to let time pass. This is why you should never close your very first credit card, even years down the line.

4. New Credit / Inquiries (10%)

Every time you apply for a new credit card or loan, the lender pulls your credit report. This is called a “hard inquiry,” and it temporarily drops your score by 3 to 5 points. Applying for five different credit cards in a single weekend makes you look incredibly risky, and the algorithm will penalize you heavily.

5. Credit Mix (10%)

Lenders want to see that you can responsibly handle different types of debt. A perfect credit mix includes both “revolving” credit (credit cards) and “installment” loans (auto loans, student loans, or mortgages). As a beginner, do not stress about this category. Do not take out a car loan just to satisfy the credit mix requirement.

(If you are confused by the different numbers you see on banking apps versus official reports, read our complete breakdown on FICO vs. VantageScore: Why Credit Scores Differ Between Apps.)

Phase 1: The Authorized User Strategy (The Quick Start)

If you need a credit score immediately (for example, you are trying to rent an apartment next month), the fastest way to build credit from scratch is the “Authorized User” strategy. This is commonly referred to as “credit piggybacking.”

How It Works

You ask a parent, a spouse, or a highly trusted family member to add your name to one of their existing, long-standing credit cards. The bank will mail a physical credit card with your name on it, linked to their account.

Here is the magic: the moment you are added as an authorized user, the bank copies that card’s entire payment history and pastes it directly onto your blank credit report. If your mother adds you to a card she has kept open and paid perfectly for 10 years, your credit report instantly looks like you have a 10-year history of perfect payments.

The Rules of Piggybacking

If you use this strategy, you must follow strict boundaries to protect both yourself and the primary cardholder.

- The card must have flawless history: Do not become an authorized user on a card that has late payments. If the primary cardholder misses a payment, that late mark goes on your credit report, too.

- The card must have low utilization: Ensure the primary cardholder pays the balance off every month. If they max out the card, your score will tank because you inherit their high utilization.

- You do not need the physical card: To protect the primary cardholder’s finances, tell them to cut up the physical card with your name on it when it arrives in the mail. You do not actually need to spend money on the card to get the credit-boosting benefits. You just need your name attached to the account data.

Phase 2: The Secured Credit Card (The Bedrock)

While being an authorized user gives you a quick boost, lenders eventually want to see that you can manage your own debt. Because you have no credit history, traditional banks will not approve you for a standard “unsecured” credit card. They view you as too risky.

The solution is a Secured Credit Card.

How Secured Cards Work

A secured credit card requires you to put down a refundable cash deposit upfront. Usually, this deposit is between $200 and $500. The bank takes your cash, locks it in a secure vault, and then hands you a credit card with a limit exactly equal to your deposit.

If you put down a $300 deposit, your credit card limit is $300.

The bank is completely protected. If you max out the card and run away, they simply keep your $300 deposit to cover the debt. However, because you are using the card responsibly, the bank reports your on-time payments to the three major credit bureaus every month, successfully building your credit profile from scratch.

How to Use the Secured Card

To build credit perfectly without paying a single penny in interest, follow this exact formula:

- Buy one small thing a month: Put your Netflix subscription or a single tank of gas on the card. Do not use it for your daily spending.

- Keep the balance tiny: Remember the credit utilization rule. If your limit is $300, never let the reported balance go above $30.

- Pay the statement balance in full: When the bill arrives, pay the “Statement Balance” in full, three days before the due date. Set this up on autopay from your checking account.

After 6 to 12 months of perfect payments, the bank will “graduate” your account. They will mail your original $300 deposit back to you, upgrade your account to a standard unsecured credit card, and likely increase your credit limit.

(Looking for the best options to get started? We have reviewed the top cards with zero annual fees in our guide: Best Credit Cards for Beginners: What Actually Matters.)

Phase 3: Alternative Credit Builders

If you do not have the cash upfront for a secured card deposit, or if you want to speed up the process by adding different types of credit to your profile, you can leverage alternative credit-building tools.

1. Credit Builder Loans

A credit builder loan is the exact opposite of a traditional loan. Instead of handing you a lump sum of cash that you pay back, the lender takes the loan amount (e.g., $1,000) and locks it in a savings account that you cannot touch.

You then make monthly payments (e.g., $50 a month) to the lender. The lender reports these on-time payments to the credit bureaus, building your installment loan history. Once you have made all the payments and the “loan” is fully paid off, the lender unlocks the savings account and hands you the $1,000. It is essentially a forced savings plan that builds your credit score.

2. Rent and Utility Reporting

Historically, paying your rent and utility bills on time did absolutely nothing for your credit score. Today, you can use third-party services (like Experian Boost or various rent-reporting platforms) to link your checking account and have your on-time rent, water, electric, and cell phone payments officially reported to the credit bureaus.

This is an excellent, low-risk way to flesh out a thin credit file using bills you are already paying anyway. However, keep in mind that not all scoring models treat rent data equally, so your results may vary depending on which lender is pulling your report.

The Blueprint in Action: Sarah’s Story

Let’s look at a realistic example of how these strategies combine to build a strong profile fast:

- The Profile: Sarah (Age 22), 0 credit history.

- Action 1: Becomes an authorized user on her mom’s oldest, well-managed credit card.

- Action 2: Opens a $300 secured credit card.

- Action 3: Puts her $15 Netflix subscription on the secured card and sets it to autopay the statement balance in full.

- The Result: 8 months later, Sarah has a 710 FICO score and easily qualifies for her own unsecured cash-back rewards card.

The Biggest Myth in Credit Building

If you take only one piece of advice from this guide, let it be this: You never, ever have to carry a balance and pay interest to build your credit score.

There is a toxic, widespread myth that banks want to see you leave a little bit of debt on your credit card every month. People believe that if they leave $50 on their card and pay 25% interest on it, their score will go up faster. This is entirely false.

The credit bureaus do not care if you pay interest. They only care that you use the card and pay the bill on time. If you spend $100 during the month, let the statement close so the $100 balance is reported to the bureaus, and then pay the entire $100 off before the due date, you will build perfect credit and pay absolutely $0 in interest.

Common Mistakes to Avoid When Building Credit

When you are starting from zero, your credit file is extremely “thin.” This means a single mistake will hurt you mathematically worse than it would hurt someone with a 15-year credit history. Avoid these massive pitfalls:

1. Applying for Too Many Cards at Once

When you decide to build credit, the temptation is to apply for five different credit cards in a single afternoon, hoping one approves you. Do not do this. Every application triggers a “hard inquiry” on your report. A flood of inquiries signals to the algorithm that you are in a financial panic, and you will be instantly denied by everyone. Apply for one secured card. Wait six months before applying for anything else.

2. Closing Your First Credit Card

Two years from now, you will likely have a great credit score and premium travel credit cards. You might look at your original $300 secured card and think, “I should close this; I never use it.”

Never close your oldest credit card. Doing so immediately shortens your “Average Age of Accounts” (which makes up 15% of your FICO score) and decreases your total available credit, which spikes your credit utilization ratio. Throw the old card in a sock drawer, put a $2 iCloud subscription on it, and set it to autopay forever.

(For a deep dive into the hidden traps that destroy new credit profiles, read: 10 Credit Score Mistakes That Can Cost You 100+ Points.)

Your Action Plan: The 12-Month Credit Building Timeline

Building credit is a marathon, not a sprint. If you are starting today, here is the exact month-by-month timeline you must follow to guarantee an elite score by next year.

❌ Avoid These Mistakes Along the Way

- Missing a payment

- Maxing out a card

- Applying for multiple cards

- Closing your first account

1.Month 1: Open Your First Account:Establish the foundation.

Ask a trusted family member to add you as an authorized user to an old, perfectly-paid credit card. Simultaneously, apply for one Secured Credit Card with no annual fee from a major issuer like Discover or Capital One. Provide your $200 deposit.

2.Month 2: Set the Autopay Trap:Automate the habit.

When your secured card arrives, link it to a single small recurring subscription (like Spotify). Log into the banking portal and set up automatic payments for the “Full Statement Balance.” Put the physical card in a desk drawer and do not carry it in your wallet.

3.Months 3 to 5: The Waiting Game:Wait for the algorithm.

Do absolutely nothing. Let your automatic payments process. Do not apply for store cards, do not apply for auto loans, and do not manually spend on the secured card. You are currently in the FICO “incubation” period.

4.Month 6: Your First FICO Score:The score generates.

Congratulations! At the six-month mark, your official FICO score will generate. If you followed the steps above, keeping utilization low and never missing a payment, your score should debut between 680 and 720. Check your score using your banking app’s free tracker.

5.Month 7 to 12: Graduation:Graduate and expand.

Continue your flawless payment history. Around month 8 to 12, your bank should automatically graduate your secured card, returning your initial deposit and upgrading you to an unsecured card. At this point, your credit profile is strong enough to apply for a standard cash-back rewards card.

To map out exactly how your new credit score will allow you to access favorable loan terms, use our Credit Score Simulator & Improvement Planner.

Test Your Credit Score Before Making Big Moves

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our simulator.

Launch Credit SimulatorFrequently Asked Questions (FAQ)

Can I build credit if I don’t have a Social Security Number (SSN)?

Yes. Many major credit card issuers and secured card providers allow you to apply using an Individual Taxpayer Identification Number (ITIN) or even a passport. You do not need to be a US citizen to establish a US credit profile, provided you find a lender that accepts alternative documentation.

How long does it take to get a 700 credit score from scratch?

If you use the Authorized User strategy with a highly qualified family member, you can theoretically debut with a 700+ score the moment the algorithm generates your score at the 6-month mark. If you are building entirely on your own with a secured card, it typically takes 12 to 18 months of perfect, low-utilization payments to consistently hold a 700+ FICO score.

Do debit cards build credit?

No. Debit cards pull money directly from your checking account. Because you are spending your own money, no bank is extending you a line of credit, and therefore the activity is never reported to the credit bureaus.

Is a 650 credit score good for a beginner?

A 650 is considered “Fair.” While it is a very common starting point for beginners whose scores have just generated, it is not high enough to secure the best interest rates on auto loans or mortgages. Keep your credit utilization below 10% and wait a few more months to push it into the “Good” range (670–739).

What happens if I miss a payment on my secured card?

It will devastate your new credit score. Payment history is 35% of your total score. Because your file is thin, a single 30-day late payment can drop your score by up to 100 points and will remain on your credit report for seven years. Always use autopay.

Conclusion

Figuring out how to build credit from scratch can feel like a frustrating catch-22: banks will not give you credit until you have credit. But by understanding how the system works, you can bypass the traditional gatekeepers.

By strategically using Authorized User status to inherit positive history, opening a no-fee Secured Credit Card to establish your own data, and rigorously defending your payment history and utilization ratios, you take complete control of the algorithm. Building an elite credit score doesn’t require wealth or high income; it simply requires patience, automation, and a strict adherence to the rules of the game. Put your first step into motion today, and by this time next year, your “credit invisible” status will be gone forever.

References

- Consumer Financial Protection Bureau (CFPB): Official consumer guidelines on understanding credit reports, secured credit cards, and the impact of authorized user status.

- Federal Deposit Insurance Corporation (FDIC): Recommendations on safe banking practices, avoiding predatory lending, and building a financial foundation.

- Fair Isaac Corporation (FICO): The mathematical breakdown of the five factors that constitute a standard FICO credit score.

- Federal Trade Commission (FTC): Consumer advice on disputing credit report errors and protecting personal information while building credit.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.