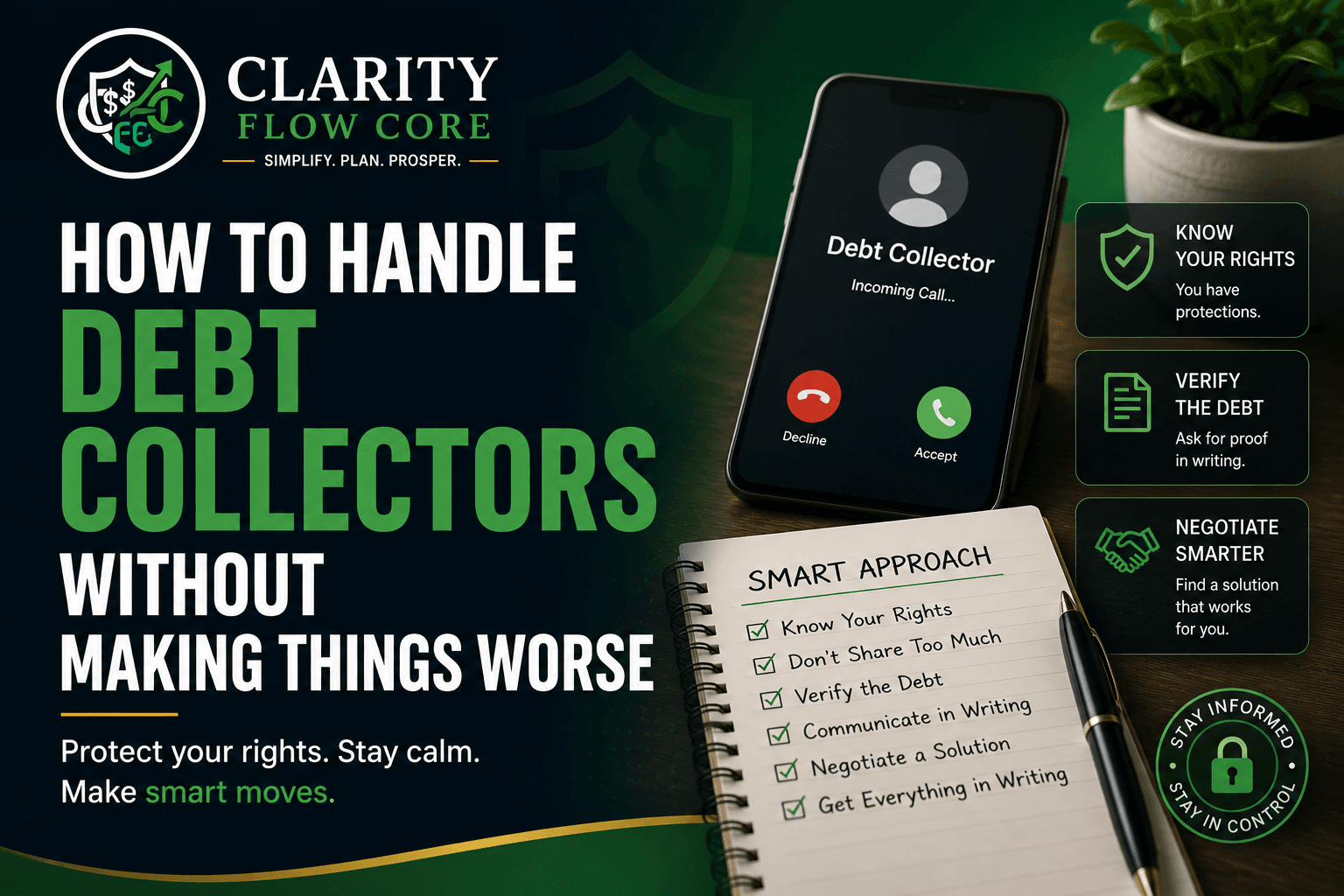

How To Handle Debt Collectors Without Making Things Worse

It usually starts with a phone call from an unknown number. You let it go to voicemail, assuming it is just another spam risk or a robot trying to sell your car insurance. But then the calls keep coming. Every day at 9:00 AM. Again at 2:00 PM. Sometimes right as you are sitting down for dinner.

Eventually, you listen to the voicemail. A stern, urgent voice tells you that this is an attempt to collect a debt, and that it is imperative you call back immediately.

Your stomach drops. The anxiety spikes. Suddenly, you are terrified to open your mailbox, answer your phone, or even look at your bank account.

If you are currently dodging phone calls from debt collectors, take a deep breath.

Dealing with a collection agency is one of the most isolating, shameful, and financially terrifying experiences a person can go through. But you need to know a fundamental truth right now: being in debt does not make you a bad person, and it does not strip you of your legal rights.

Debt collectors rely heavily on the fact that you probably do not know those rights. They use pressure, urgency, and embarrassment to get you to open your wallet. But the moment you understand how the collection industry actually works, their power over you instantly evaporates.

This guide is going to walk you through exactly how to handle debt collectors, the massive mistakes that reset the clock on your debt, and how to logically negotiate your way out of this.

Disclaimer: This article is for educational purposes and is not legal advice. If you are facing a massive lawsuit or bankruptcy, always consult a qualified attorney in your state.

The Real Problem: Understanding the Debt Collection Machine

To beat a debt collector at their own game, you have to understand what they actually are.

When you borrow money from a bank, a hospital, or a credit card company, they expect you to pay it back. But if life happens and you stop paying, the original lender doesn’t want to chase you forever. It costs them too much time and money to keep calling you.

The Typical Collection Timeline

To understand exactly where you stand, it helps to see the standard timeline of an unpaid debt:

- 30 Days Late: Late fees are applied, and your credit score takes a hit.

- 60 to 90 Days Late: The original lender starts calling aggressively.

- 120 to 180 Days Late: The account is “Charged-Off” (written off as a business loss).

- Post Charge-Off: The debt is officially sold to a third-party Collection Agency.

- Months/Years Later: Potential civil lawsuit if the debt is completely ignored.

Here is the secret they do not want you to know: Collection agencies buy your debt for pennies on the dollar.

If you owe a credit card company $5,000, a debt buyer might purchase that account for $200. The math is simple. If they can harass, annoy, or scare you into paying the full $5,000, they just made a massive profit. Even if you only agree to pay them $2,000 to leave you alone, they still made a fantastic return on their investment.

The person contacting you works for a company whose goal is to recover money on behalf of a creditor or debt buyer. Understanding their incentives can help you approach the situation more calmly and strategically. They are not the moral authority. They are simply trying to close a highly profitable deal.

📌 Related Guide: What Happens If You Missed Credit Card Payment?

Why We Fall Behind in the First Place

There is a massive stigma around debt in the United States. Society loves to paint anyone with a collection account as irresponsible, lazy, or foolish with their money.

The reality is entirely different. Most people do not end up in collections because they bought a luxury car they couldn’t afford or went on a wild shopping spree in Europe.

Most people fall behind because life simply stopped cooperating with their bank account.

Maybe you are a freelancer whose biggest client suddenly ghosted you, leaving you with zero income for two months. Maybe you suffered a medical emergency, and even with insurance, the out-of-pocket deductibles drained everything you had. Maybe your transmission blew, and you had to put the $3,000 repair on a high-interest credit card just so you could keep driving to work.

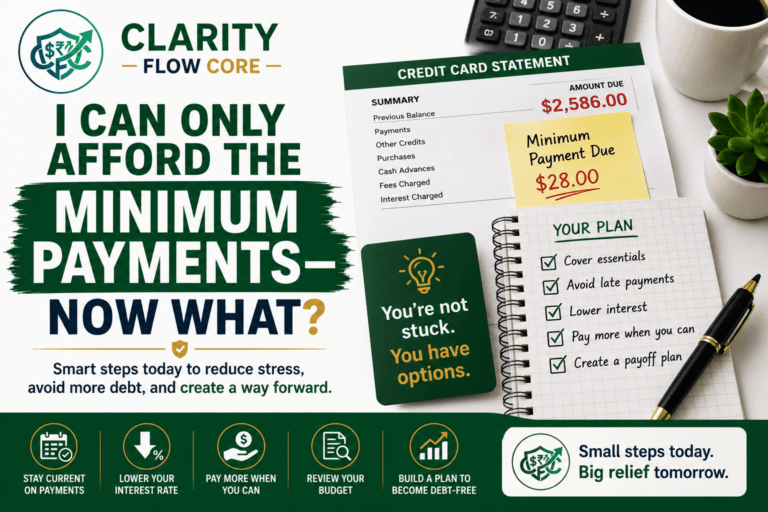

If you’re only able to make minimum payments while trying to stay afloat, our guide I Can Only Afford the Minimum Payments — Now What? explains how to minimize the long-term damage until your finances recover.

When you are living paycheck to paycheck—or managing the incredibly volatile income of a side hustle—one single bad week can throw off your entire financial ecosystem. When forced to choose between buying groceries for your family or paying the minimum balance on a Visa card, you are going to choose the groceries.

If you’re already falling behind on multiple bills, knowing which payments to prioritize first can help you avoid making the situation worse. Read Behind on Bills? Which Payments Should You Prioritize First? before deciding where your next dollar should go.

And you should. But that survival choice is exactly how the snowball of collections begins.

📌 Related Guide: How to Budget as a Freelancer When Income Changes Every Month

4 Massive Mistakes People Make When the Phone Rings

When we are scared, we make rash decisions. Debt collectors know this, and they actively try to push you into making a mistake that legally traps you. If you are dealing with a collector right now, absolutely avoid doing these four things.

1. Making a “Good Faith” Payment of $5

This is the deadliest mistake you can make. The collector will sound sympathetic on the phone. They will say, “Look, I know things are tight. Just send us $10 today to show you are acting in good faith, and we will keep your account from escalating.”

Do not do it.

Every debt has a “Statute of Limitations.” This is a state law that limits how many years a collector has to sue you over a debt. In many states, it is between three and six years. If the clock runs out, they can still ask you for the money, but they can never drag you into court to force you to pay.

However, in some states, making a payment or acknowledging a debt can restart the statute of limitations. Even a small $5 “good faith” payment could potentially reset the clock back to day one. Because these laws vary, check your state’s rules before agreeing to anything.

2. Acknowledging the Debt on the Phone

When a collector calls, they are usually recording the conversation. They will try to get you to admit that the debt belongs to you. They might ask, “So when do you plan on paying this $3,000 balance you owe?”

If you say, “I just can’t afford it right now,” you have legally acknowledged the debt is yours.

Instead, you need to act like a brick wall. Never confirm the debt is yours. Never say, “I know I owe this.” Simply ask who is calling, what company they represent, and request that they send all future correspondence in writing.

3. Handing Over Your Bank Account Information

Never, ever give a debt collector your checking account routing number or debit card number over the phone.

Even if you agree to a payment plan, giving a collection agency direct access to your bank account is like handing a thief the keys to your house. While there are laws against unauthorized withdrawals, shady collection agencies have been known to “accidentally” pull more money than agreed upon, or pull the money on the wrong date.

If that unexpected withdrawal causes your rent check to bounce, the collection agency does not care. If you absolutely must pay them, use a cashier’s check, a money order, or a prepaid debit card that is not linked to your main livelihood.

4. Ignoring the Problem Entirely

While you shouldn’t talk to them on the phone, you cannot just stick your head in the sand. Ignoring a debt collector completely does not make them go away. In fact, silence is what usually pushes them to take real legal action against you. You must respond, but you must do it strictly on your terms, and strictly in writing.

The Real Consequences of Doing Nothing

If you let fear paralyze you and completely ignore letters and calls, the situation will eventually escalate from an annoyance to a genuine crisis.

A collection agency cannot arrest you. There is no such thing as debtor’s prison in the US. However, they can file a civil lawsuit against you.

If they sue you and you do not show up to court (which most people do not, out of sheer panic), the collector automatically wins a “default judgment.” Once they have a judgment signed by a judge, their power goes from annoying to devastating.

With a judgment, they can legally:

- Garnish your wages: They can force your employer to send a percentage of your paycheck directly to them before you ever see it.

- Levy your bank account: They can get a court order to freeze your checking account and drain the funds to pay the debt.

- Place a lien on your property: If you own a home, they can attach the debt to your house, meaning you cannot sell or refinance until they are paid.

For freelancers and side hustlers, bank levies are particularly terrifying. Unlike W-2 employees whose wages are garnished a little at a time, independent contractors can sometimes have their entire bank accounts frozen. You want to stop the process long before it ever reaches a courtroom.

📌 Related Guide: Freelance Video Editor Tax Guide: Deductions, Write-Offs & Basics

Practical Solutions: How to Handle Debt Collectors and Fight Back

Now that you know the rules of the game, it is time to play offense.

🛡️ Know Your Rights: The FDCPA

You have massive federal protection under a law called the Fair Debt Collection Practices Act (FDCPA). Before you deal with a collector, you must know what they are legally allowed to do.

Debt Collectors CANNOT:

- ✓ Threaten you with arrest or jail time.

- ✓ Pretend to be law enforcement or government officials.

- ✓ Call you repeatedly just to harass or annoy you.

- ✓ Discuss your debt with your friends, family, or boss.

- ✓ Use abusive language or profanity.

Debt Collectors CAN:

- ✓ Contact you about legitimate, unpaid debts.

- ✓ Report those debts to the three major credit bureaus.

- ✓ Sue you in civil court to force payment.

- ✓ Seek legal judgments (like wage garnishment) if they win the lawsuit.

Here is how you use your rights to handle these accounts like a professional.

Step 1: Demand Everything in Writing

The absolute golden rule of dealing with debt collectors is: If it is not in writing, it never happened.

When they call, answer the phone exactly once. Say this script:

“I am aware you are trying to reach me. However, I am requesting that you cease all phone communication immediately. I require you to send all future communication regarding this matter to my home address in writing. Do not call this number again.”

While telling them to stop calling is a good first step, a verbal request is hard to prove. Under the FDCPA, you should always follow up with a written “cease and desist” letter sent via certified mail. Once they receive that letter, they are legally restricted from contacting you, except to confirm they are stopping communication or to notify you of specific legal action.

Step 2: Send a Debt Validation Letter

Just because a company says you owe them money does not mean you legally do. Debts are bought and sold in massive spreadsheets. Sometimes the numbers are wrong. Sometimes the debt actually belongs to someone else with the same name. Sometimes the debt is already passed the statute of limitations.

Within 30 days of receiving their first written notice, you need to send them a “Debt Validation Letter” via certified mail.

This letter legally forces the collection agency to hit the pause button. They must completely stop trying to collect the money until they can provide physical proof that you owe the debt, proof of the exact amount, and proof that they legally own the right to collect it.

Because debts are bought in bulk, many agencies don’t actually have your original signed contract. If they cannot properly validate the debt, they must stop trying to collect it from you. In many cases, unverified debts are removed from your credit report if you dispute them with the credit bureaus, though the dispute process can sometimes take patience and persistence.

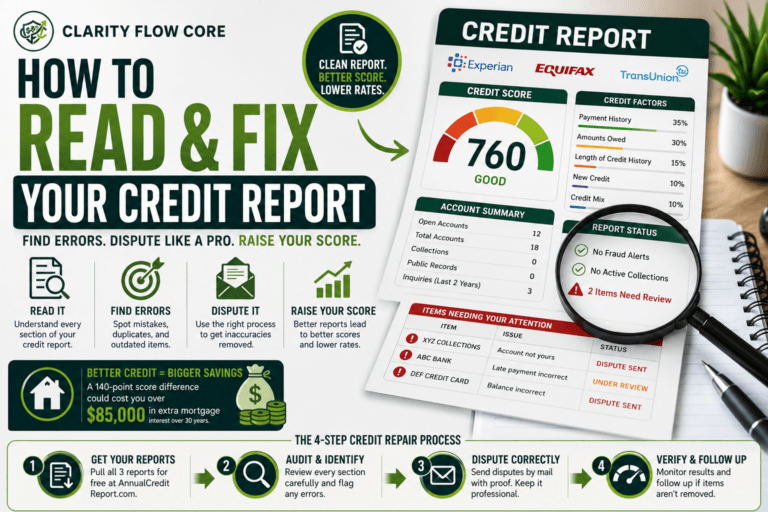

After resolving a collection account, it’s important to verify that your credit reports accurately reflect the changes. How to Read and Fix Errors on Your Credit Report walks through how to review your reports and dispute mistakes.

Step 3: Negotiating a Settlement

If they validate the debt, and you confirm that you do actually owe the money, your next step is negotiation.

Remember, they bought your $5,000 debt for a few hundred dollars. They do not need you to pay $5,000 to make a profit.

If you have a little bit of cash saved up, you can offer a lump-sum settlement. Start incredibly low. Tell them, “I am facing severe financial hardship, but I can borrow $1,000 from a family member to settle this account today in full.”

They will counteroffer. Stand your ground. Many collection accounts can be settled for much less than the full balance, depending on the age of the debt, the specific collector, and your financial circumstances.

Before agreeing to any settlement offer, understand how debt settlement compares with other repayment strategies. Debt Consolidation vs Debt Settlement: Which Actually Saves More Money? explains the advantages, trade-offs, and when each option makes the most sense.

Crucial Step: If they agree to settle for a lower amount, you must get the agreement in writing before you send a single dime. The letter must explicitly state that the payment will satisfy the account “in full.” If you don’t get this in writing, they will take your $1,000 and then immediately start harassing you for the remaining $4,000.

Step 4: Ask for a “Pay for Delete”

When you negotiate your settlement, ask for a “Pay for Delete” agreement. This means that in exchange for your payment, the collection agency agrees to completely remove the collection account from your credit reports at Equifax, Experian, and TransUnion.

Not all agencies will agree to this, but if they do, it can be one of the fastest ways to reduce the long-term impact of a collection account on your credit profile. Get this in writing alongside your settlement agreement.

How to Recover Your Credit After Collections

A massive fear people have is that a collection account will ruin their financial life forever. It won’t.

Recovering from collections takes time, but rebuilding your credit is absolutely possible. How Long Does It Really Take To Rebuild Bad Credit? explains what to expect during the recovery process and which milestones matter most.

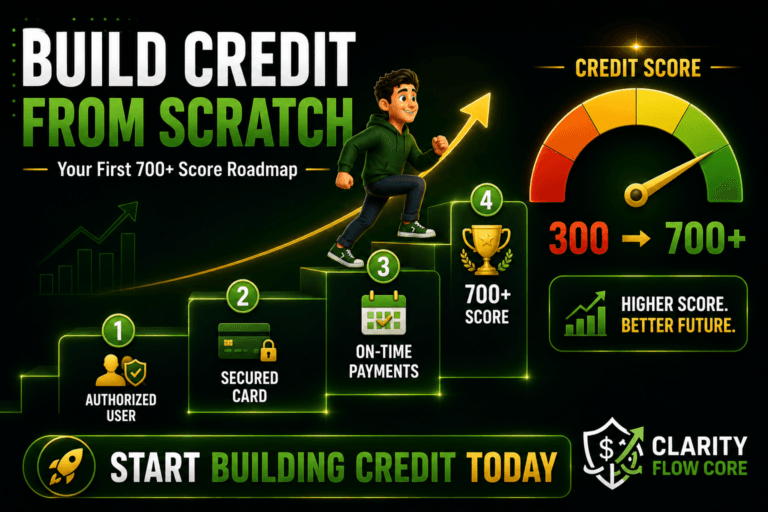

Once your collection accounts are resolved and you’re ready to rebuild, Best Secured Credit Cards for Beginners in 2026 compares secured cards that can help you establish fresh positive payment history and gradually strengthen your credit profile.

How Long Does a Collection Stay on Your Credit Report? A collection account stays on your credit report for up to seven years from the date of the original missed payment. However, the impact of that negative mark heavily declines over time. A collection from four years ago hurts your score significantly less than a collection from four months ago.

Additionally, many newer credit scoring models view paid collections much more favorably than unpaid ones. While a “Pay for Delete” is the holy grail, simply getting the balance to $0 and marking it “Paid in Full” or “Settled” is a massive step toward credit recovery.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationWhen Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyThe Beginner-Friendly Action Plan

If you are overwhelmed, stop looking at the big picture and just focus on your immediate next steps. Here is your survival checklist for the next 48 hours:

- 1. Stop answering the phone. Let it go to voicemail until you are emotionally prepared to read the script telling them to communicate only in writing.

- 2. Check your credit reports. Go to AnnualCreditReport.com (the only legally free site) and pull your reports. See exactly who claims you owe them money and how old the debt is.

- 3. Draft your validation letter. There are hundreds of free templates online. Find a standard Debt Validation Letter, fill in your details, and print it out.

- 4. Go to the Post Office. Mail the validation letter using “Certified Mail with Return Receipt.” This provides a legal paper trail proving exactly what day they received your demand.

- 5. Do not empty your savings. Never pay a debt collector if it means you will not be able to pay your rent or keep the lights on. Your basic survival always comes before an old debt.

Frequently Asked Questions (FAQs)

Can a debt collector call my family, friends, or my boss? Under the FDCPA, a collector is allowed to contact third parties, but only for the purpose of trying to locate you (e.g., asking for your current address or phone number). They are strictly forbidden from discussing your debt, telling your boss you owe money, or harassing your family members.

What happens if the statute of limitations expires? If a debt passes your state’s statute of limitations, it becomes “time-barred.” The debt still exists, and collectors can technically still ask you to pay it, but they lose the legal right to sue you in court or garnish your wages over it.

Will paying off a collection account instantly fix my credit score? No, unfortunately. Even if you pay the collection account in full, the fact that it went to collections will remain on your credit report for seven years, unless you successfully negotiate a “Pay for Delete” agreement. However, a paid collection account looks much better to future lenders than an unpaid one.

Can I just explain my situation to them and hope they forgive the debt? No. Remember, you are talking to a commissioned salesperson, not a therapist or a charity. They will use your financial vulnerabilities to figure out exactly how to squeeze money out of you. Keep your conversations strictly professional, emotionless, and ideally, entirely in written letters.

A Final Word of Encouragement

Opening a letter from a collection agency feels like a punch to the gut. The industry is specifically designed to make you feel small, helpless, and panicked.

But you are not helpless. Your net worth is not your self-worth.

Financial mistakes, unexpected job losses, and medical emergencies happen to millions of incredibly smart, hardworking people every single day. Having a debt in collections does not mean you failed; it just means the math didn’t work out for a season of your life.

By demanding everything in writing, exercising your federal rights, and refusing to be bullied on the phone, you take the power back immediately. Protect your four walls—your food, your housing, your utilities, and your transportation. Let the collectors wait. You can handle this logically, methodically, and on your own timeline.

Sources & References

- Consumer Financial Protection Bureau (CFPB) – Debt Collection – Learn about your rights when dealing with debt collectors, including communication rules and protections under the Fair Debt Collection Practices Act (FDCPA).

- Federal Trade Commission (FTC) – Debt Collection – Official consumer guidance on recognizing illegal collection practices, disputing debts, and protecting yourself from harassment.

- AnnualCreditReport.com – The federally authorized website where you can request free credit reports from Equifax, Experian, and TransUnion to review collection accounts and other credit information.

- Consumer Financial Protection Bureau (CFPB) – Disputing Errors on Your Credit Reports – Learn how to dispute inaccurate collection accounts and other credit reporting errors.

- National Foundation for Credit Counseling (NFCC) – Find certified nonprofit credit counselors who can help you evaluate debt repayment options and Debt Management Plans (DMPs).

- Experian – Collections and Your Credit Report – Educational resources explaining how collection accounts affect your credit and what happens after a debt is paid.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.