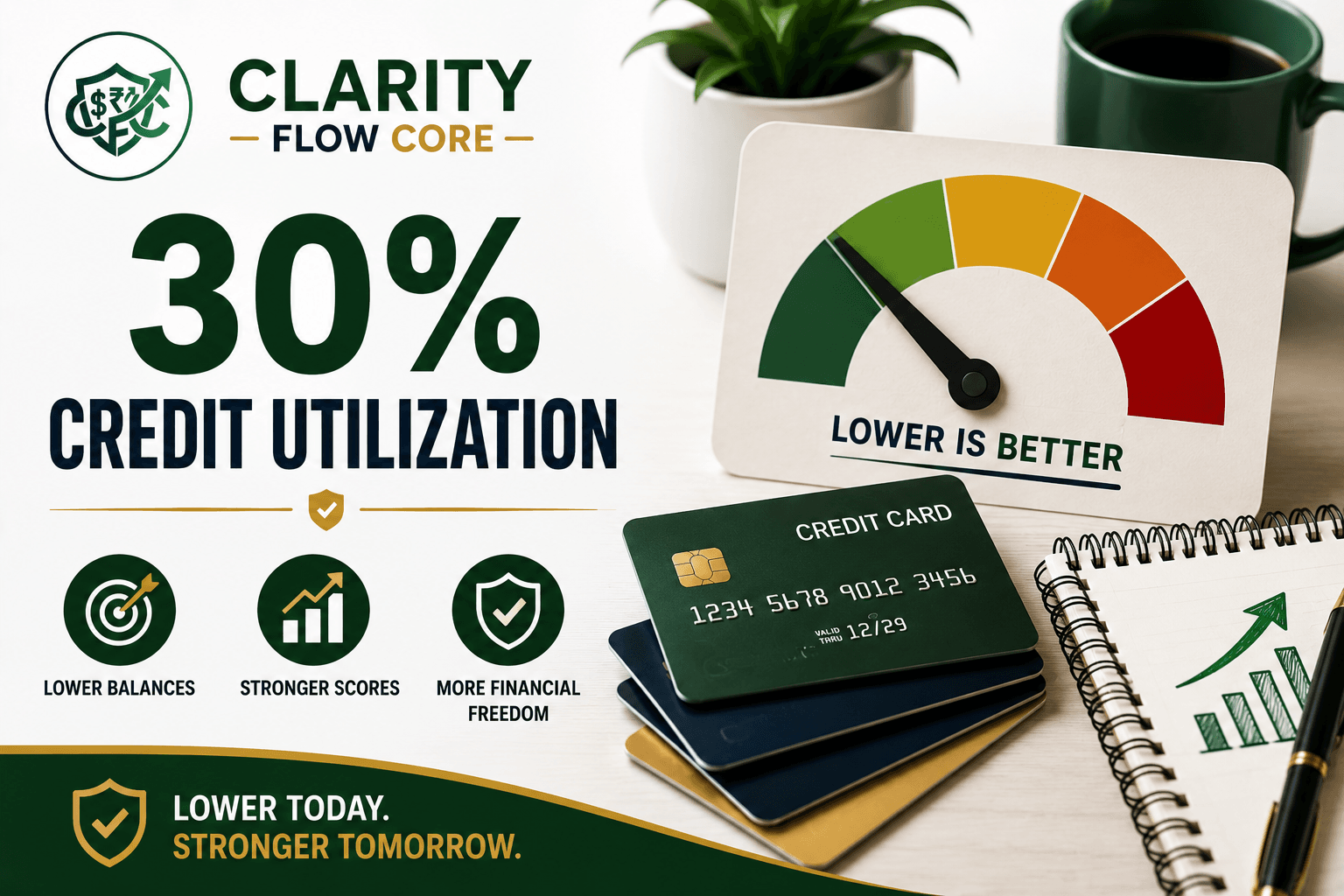

The 30% Credit Utilization Myth: What Actually Matters?

You log into your banking app or Credit Karma, expecting to see a nice, steady number. You pay your bills on time every single month. You’ve never missed a payment in your life.

But today, there’s a bright red arrow pointing down. Your credit score dropped 25 points.

Panic sets in. You immediately start scrolling through your transactions, wondering if your identity was stolen or if a random bill went to collections. Then you see it: an alert saying your credit card balance increased.

Wait. You bought new tires for your car last week, but you were planning to pay the bill in full on payday. Why is the credit bureau punishing you before your bill is even due?

Welcome to the incredibly confusing, highly emotional, and completely misunderstood world of credit utilization.

If you have ever Googled how to fix this, you have probably been hit over the head with the golden rule of credit: “Keep your credit utilization under 30%.” You hear it from bank tellers, financial influencers, and well-meaning family members.

It gets repeated so often that it sounds like a financial law of gravity. But here is the detail many people overlook: the 30 percent credit utilization myth is a massive oversimplification that is causing normal people a lot of unnecessary stress.

Let’s strip away the textbook finance jargon. We are going to look at why this myth exists, how credit scoring actually works behind the scenes, and the exact steps you can take to manipulate this system in your favor.

⚡ Quick Answer

The “30% rule” is a myth because 30% is not a target—it is the absolute maximum limit before your score takes heavy damage. Many credit experts consider utilization between 1% and 9% ideal for maximizing credit scores, while utilization below 30% is generally considered healthy. Furthermore, keeping a 0% balance is actually worse than a small balance, and because utilization has “no memory,” a high balance won’t ruin your credit permanently.

| Credit Utilization | Typical Impact |

| 0% | Good, but may not be optimal |

| 1–9% | Often considered ideal |

| 10–29% | Generally healthy |

| 30–49% | Score may be affected |

| 50–74% | Significant impact possible |

| 75%+ | High risk zone |

The Real Problem Behind the 30 Percent Credit Utilization Myth

To understand why people struggle so much with their credit scores, we have to look at how we are taught to use credit cards.

When you get a credit card with a $1,000 limit, it feels like the bank trusts you with a thousand dollars. If you spend $300 on groceries and gas, you are right at that 30% line. You feel responsible. You are playing by the rules.

The problem is that the 30% rule is taught as if it is a target or a safe zone. People assume that as long as they stay at 29%, their credit score will go up, and if they hit 31%, their financial life is ruined.

Neither of those things is true.

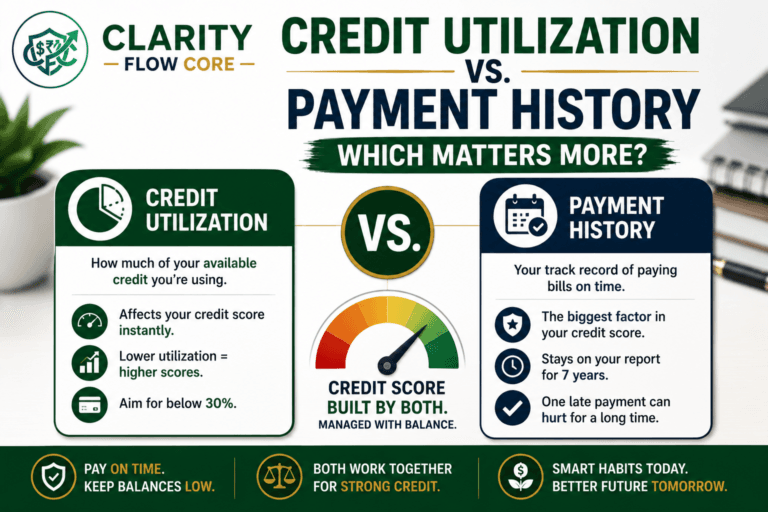

Credit utilization makes up 30% of your total FICO credit score. It is the second most important factor, right behind your payment history. But the scoring algorithm does not look at 30% as a “good” number. In the eyes of the algorithm, the less credit you use, the better.

If you’re wondering which factor has the biggest impact on your score, Credit Utilization vs Payment History: Which Matters More? compares these two major scoring categories and explains how to prioritize them.

If you sit at 29% utilization, your score is likely being actively suppressed. You aren’t in the danger zone, but you definitely aren’t getting an A+ either. Lenders look at 30% as the edge of a cliff. You don’t want to live on the edge of the cliff; you want to be safely inland.

Why It Happens: The Math Behind the Curtain

Let’s look at why credit bureaus care so much about this ratio in the first place.

Credit utilization is simply the amount of money you owe divided by your total available credit limit. If you have a credit card with a $5,000 limit, and your current balance is $2,500, your utilization is 50%.

If you’re new to this concept and want a deeper explanation of how the calculation works, What Is Credit Utilization — And Why Does It Matter? breaks down the formula, how lenders evaluate it, and why it plays such a significant role in your credit score.

Why does a computer algorithm care if you use the money they gave you access to? Because credit scores are not a measure of your personal wealth or your moral character. A credit score is just a risk prediction tool.

Data shows that when people start maxing out their credit cards, they are statistically more likely to miss a payment in the near future. Lenders view a high balance as a sign of financial distress. The algorithm assumes that if you are using 80% of your available credit, you might be relying on credit cards to survive because your cash is gone.

Even if you are a millionaire who just bought a bunch of furniture for points and intends to pay it off tomorrow, the algorithm doesn’t know your intentions. It only sees the math.

Common Mistakes People Make with Credit Cards

Because the rules of credit are kept so vague, normal people end up trying to “game” the system using bad advice. Here are the biggest traps you need to avoid.

Mistake 1: The “Leave a Small Balance” Myth

This is perhaps the most toxic piece of financial advice still circulating today. People believe that to build credit, you have to leave a small balance on your card each month and pay a little bit of interest to “show the banks you use it.”

This is 100% false. Carrying a balance from month to month does absolutely nothing to help your credit score. All it does is make the credit card companies richer at your expense. You should pay your statement balance in full, every single month.

Mistake 2: The 0% Ghost Town

On the flip side, some people are so terrified of debt that they pay off every purchase the minute it clears. Their statement closes with a $0 balance every month.

While this is great for avoiding interest, it can actually hurt your credit score slightly. If the credit bureaus see a 0% utilization rate month after month, it looks like you aren’t using the card at all. It is hard to grade someone on how well they manage borrowed money if they never appear to borrow any.

Mistake 3: Closing Old, Unused Cards

Say you finally pay off a credit card that has been stressing you out. Out of relief, you call the bank and close the account so you can never use it again.

The next month, your credit score tanks. Why? Because you just wiped out a chunk of your available credit limit. If you had two cards, each with a $2,500 limit, your total available credit was $5,000. If you close one, your total limit drops to $2,500. Any small balance you carry now takes up a much larger percentage of your remaining limit, skyrocketing your utilization ratio.

Real Consequences: The Timing Trap

So, what happens if your utilization spikes to 60% or 70%?

The emotional consequence is immediate. Waking up to a credit alert telling you your score dropped 40 points feels like a punch in the gut. It makes you feel like you are moving backward, especially if you are working hard to manage your money.

But the practical consequence entirely depends on your timing.

If you are planning to apply for a mortgage, an auto loan, or even a new apartment lease next month, a high utilization rate is a massive problem. Before applying, you should always check where you stand using a Debt-to-Income (DTI) Analyzer & Loan Readiness Planner. A score that drops from 720 to 680 could mean the difference between getting approved or denied. It could mean getting hit with an 8% interest rate on a car loan instead of a 5% rate, costing you thousands of extra dollars over the life of the loan.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI RatioHowever, if you are not applying for any new credit in the next 30 to 60 days, a temporary spike in utilization actually doesn’t matter as much as you think.

Which brings us to the most important secret of the credit industry.

The Best Kept Secret: Credit Utilization Has No Memory

If you only take one thing away from this article, let it be this: Credit utilization has no memory.

If you miss a payment, that black mark stays on your credit report for seven long years. It follows you around like a shadow.

But utilization is completely different. It is just a snapshot in time. The credit bureaus only care about your current balance.

Let’s say you had a medical emergency and had to max out your credit card. Your utilization hits 95%, and your credit score drops by 60 points. You might feel like your financial reputation is ruined.

But if you manage to pay that card completely off three months later, your utilization drops back down. Within 30 days, your credit score will bounce right back up as if the maxed-out balance never happened. The algorithm does not look at your past utilization, only your present.

This means you can stop stressing over a temporary high balance. If you had to use your card to survive a tough month, let it go. You can fix the math later. (For more advice on this, read What To Do If Medical Bills Are Destroying Your Budget).

Practical Solutions: How to Master the Math

If you want to optimize your score and hit that elite 800+ tier, you need to understand the mechanics of how banks report your data. You don’t need to make more money to have a great credit score; you just need to change the timing of your payments.

1. The Statement Date Strategy (The Secret Hack)

Most people assume that their credit card company reports their balance to the credit bureaus on their due date. That is incorrect.

Banks typically report your balance on your Statement Closing Date. This date is usually 21 to 25 days before your actual payment is due.

If you buy a $1,000 couch on the 10th, and your statement closes on the 15th, the bank tells the credit bureaus you owe $1,000. Even if you pay that $1,000 in full on your due date the next month, the credit bureaus already recorded the high utilization.

To beat the system, find out what your statement closing date is (it is printed on your monthly bill). Then, make your payment two or three days before that date. By the time the bank reports to the bureaus, your balance will look incredibly low, keeping your utilization perfect.

2. The 15/3 Method

If tracking specific statement dates sounds exhausting, use the 15/3 method. Simply pay half of your credit card bill 15 days before your due date, and pay the remaining balance 3 days before your due date.

This guarantees that a massive chunk of your balance is wiped out before the statement closing date ever hits, artificially lowering your reported utilization with almost zero extra effort.

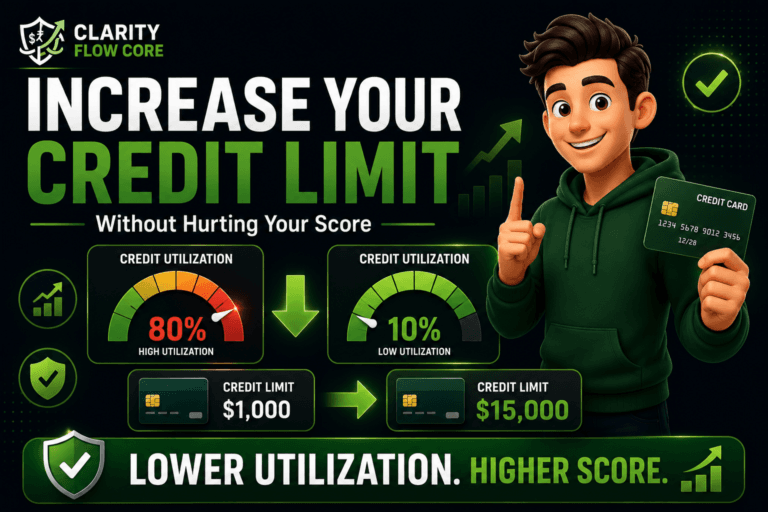

3. Ask for a Credit Limit Increase

If you have a tight budget and your credit card limit is only $500, buying a week’s worth of groceries will push you over the 30% mark instantly. It is exhausting trying to micromanage a tiny limit.

If you have a good payment history, call the number on the back of your card (or click the button in your app) and request a credit limit increase. If they bump your limit from $500 to $2,000, your grocery trips suddenly take up a tiny fraction of your available credit.

The golden rule here: Do not increase your spending just because they increased your limit. The goal is to change the math, not your lifestyle.

If you’re just starting your credit journey and have a very limited credit line, Best Secured Credit Cards for Beginners in 2026 compares secured cards that offer a solid path toward higher credit limits and eventual graduation to unsecured cards.

A Beginner-Friendly Action Plan

Credit scores can feel like a rigged game, but once you know the rules, it is incredibly easy to play. If you want to optimize your score this week and map out a full recovery, test different scenarios using our free Credit Score Simulator & Improvement Planner.

Test Your Credit Score Before Making Big Moves

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our simulator.

Launch Credit SimulatorThen, follow these steps:

- Step 1: Check your total limits. Log into your accounts and add up the total credit limits across all your open cards. Write that number down.

- Step 2: Find the 9% Sweet Spot. Multiply your total credit limit by 0.09 (9%). That is your absolute optimal target balance across all cards. If your total limit is $10,000, you want the banks to report a balance of around $900 or less. (Need help doing the math for your specific situation? Use our free Credit Utilization Calculator & Recovery System to see exactly how much you need to pay down to hit the optimal tier).

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My Utilization- Step 3: Locate your statement dates. Open a recent PDF statement from your credit card company. Look for the “Statement Period” or “Closing Date.” Put a reminder in your phone’s calendar to make your payments three days before that date every month.

- Step 4: Stop carrying debt for the sake of your score. If you have been leaving $50 on your card every month to “help your credit,” pay it off today. Stop paying interest to a multibillion-dollar bank based on a financial myth. If you need help prioritizing this over other financial goals, read Emergency Fund vs. Paying Off Debt: Which Should You Do First?.

Frequently Asked Questions

How long does it take for credit utilization changes to affect my score?

Most credit card issuers report balances to the credit bureaus once per month, often around the statement closing date. After a lower balance is reported, credit score changes may appear within a few days to several weeks depending on the scoring model and reporting schedule.

Does credit utilization apply to individual cards or my overall credit?

It actually applies to both. The credit scoring model looks at your overall utilization (all your balances combined divided by all your limits combined) and your per-card utilization. If you have five empty credit cards, but one card is 100% maxed out, your score will still drop. Try to keep the balances on every individual card relatively low.

Is it better to have a 0% utilization rate?

Surprisingly, no. A 0% utilization rate can result in a slightly lower score than a 1% or 2% rate. The algorithm wants to see that you are actively using credit and managing it responsibly. Leaving a tiny balance of $10 to report on your statement date (and then paying it off in full before the due date) is the best way to optimize your score.

What happens if I cross 50% utilization? Your credit score will take a noticeable hit (read more on How Long Does It Really Take To Rebuild Bad Credit? ), often dropping 20 to 50 points depending on your credit history. However, remember that utilization has no memory. If you cross 50% this month to pay for an emergency, don’t panic. (If you are strapped for cash, read I Can Only Afford the Minimum Payments — Now What? ). When you pay it down next month, your score will recover instantly.

Conclusion: It Is Just a Snapshot, Not Your Identity

Watching your credit score bounce around can feel incredibly stressful, especially when you are doing your best to manage your money. It is easy to take a score drop personally, feeling like the financial system is grading you and telling you that you are failing.

But your credit score is not a reflection of your worth, your work ethic, or your financial future. It is just a mathematically flawed algorithm trying to guess your risk level on any given Tuesday. (To see the big picture of your finances, try utilizing our Financial Freedom Planner instead of just obsessing over your credit score).

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanThe 30% rule is not a magic barrier you have to stress over every time you buy groceries. By understanding the difference between your statement date and your due date, you take the power back from the banks. You get to decide what numbers they see.

Take a breath, check your statement dates, and start playing the game on your terms. You’ve got this.

References & Continue Exploring This Topic

If you’d like to better understand how credit utilization affects your credit score, these trusted resources provide additional insights into credit scoring, responsible credit card use, and how lenders evaluate revolving debt.

- FICO® – What’s in Your FICO® Score?

- Experian – Credit Utilization Ratio: What It Is and Why It Matters

- Consumer Financial Protection Bureau (CFPB) – Credit Reports and Scores

- Equifax – Understanding Credit Utilization and Credit Scores

- AnnualCreditReport.com – Review your credit reports from Equifax, Experian, and TransUnion to monitor balances and account activity.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.