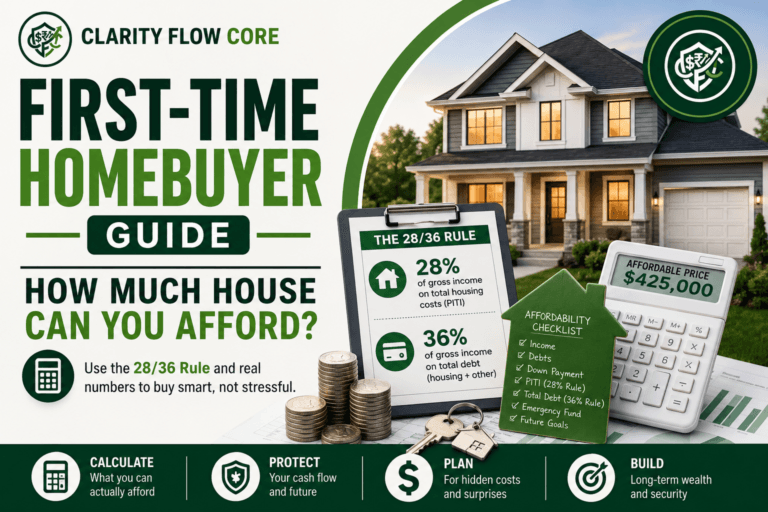

How Much Should You Have Saved Before Buying a House?

If you spend your evenings scrolling through real estate listings, you have probably experienced the sudden wave of anxiety that comes right after falling in love with a property. You look at a beautiful three-bedroom home, check the $350,000 price tag, and immediately pull up your bank account. You stare at your savings balance and wonder: Is this enough? How Much Should You Have Saved to hand over to get the keys?

For decades, the financial industry drilled a very specific, intimidating rule into our heads: you must save a 20% down payment before buying a house. If you are looking at a $350,000 starter home, the old-school math says you need $70,000 in cash. For a normal renter paying record-high monthly leases, saving $70,000 feels completely impossible. Fortunately, that advice is terribly outdated. You do not need a 20% down payment to buy a home today.

However, the down payment is only one piece of the puzzle. Buying a house comes with a flurry of upfront expenses, hidden fees, and transition costs that catch beginners completely off guard. If you want to buy a house safely, you need to stop guessing and start calculating your exact “cash to close” target.

This guide will break down the four specific buckets of money you need to save, show you exactly how much cash a $300,000 home actually requires, outline the beginner mistakes that drain bank accounts, and give you a concrete action plan to hit your savings goal.

Quick Summary: Recommended Savings by Home Price

To give you a baseline target right out of the gate, here is a look at what you should aim to save based on standard entry-level programs.

| Home Price | Recommended Savings Goal |

| $200,000 | $22,000 – $28,000 |

| $300,000 | $32,000 – $40,000 |

| $400,000 | $42,000 – $55,000 |

| $500,000 | $55,000 – $70,000 |

The Simple Cash to Close Formula

Before we dive into the details, memorize this simple equation. Your true “cash to close” is not just the down payment. It is a combination of four distinct factors:

Cash to Close = Down Payment + Closing Costs + Moving Costs + Emergency Fund

The 4 Buckets of Cash You Need to Save

When you buy a house, the money you save does not go into a single pile. It is divided into four very distinct categories. You need to fund all four buckets before you sign the final paperwork.

Bucket 1: The Down Payment

Your down payment is your initial equity in the home. It is the percentage of the purchase price that you pay upfront, which reduces the total amount of money you have to borrow from the bank. Despite what you may have heard, the average first-time home buyer in the US puts down about 6%—not 20%. The exact amount you need depends entirely on the type of mortgage you choose:

- Conventional Loans: First-time buyers with good credit can frequently qualify for conventional programs (like Fannie Mae HomeReady) that require just 3% down. For a standard conventional loan without first-time buyer perks, the minimum is usually 5% down.

- FHA Loans: Backed by the government and designed for buyers with lower credit scores or smaller cash reserves, FHA loans require a flat 3.5% down payment. To see if you qualify, read our guide on FHA vs Conventional Loan: Which Is Better for First-Time Home Buyers in 2026?.

- VA and USDA Loans: If you are an eligible military veteran or are buying a property in a designated rural area, you can actually buy a home with 0% down.

- The 20% Down Payment: If you can comfortably put down 20%, you absolutely should. Hitting the 20% mark legally eliminates the requirement to pay Private Mortgage Insurance (PMI), which can save you hundreds of dollars on your monthly payment.

Bucket 2: Closing Costs (The Hidden Bill)

This is the bucket that completely blindsides new buyers. Your down payment goes toward the house; your closing costs go to the army of professionals required to process the legal transaction. Closing costs typically range from 2% to 5% of your total loan amount.

These costs include:

- Lender Fees: Origination charges, application fees, and underwriting fees to process your mortgage.

- Property Fees: A $500 appraisal to verify the home’s value and a $400 home inspection to ensure the roof isn’t caving in.

- Title and Legal Fees: Title search fees and title insurance to guarantee no one else secretly owns the property.

- Prepaid Expenses: Lenders require you to pre-fund an “escrow account” by paying several months of property taxes and an entire year of homeowners insurance upfront.

If you buy a $300,000 house, expect your closing costs to be anywhere from $6,000 to $15,000. You must have this cash ready on closing day. For a full breakdown of every single fee, check out Closing Costs Explained: What Home Buyers Actually Pay.

Bucket 3: Moving and Immediate Expenses

Getting the keys is a great feeling until you realize the house is empty and you have to get your belongings inside. You need to budget cash for:

- Movers or Truck Rentals: A local move can cost $500 to $1,500. A cross-country move can easily cost $3,000 to $5,000.

- Utility Deposits: Setting up new water, trash, gas, and electric accounts at a new address often requires upfront security deposits.

- The “First Weekend” Run: When you move from an apartment to a house, you suddenly realize you don’t own a lawnmower, a ladder, garden hoses, or enough trash cans. You will likely spend $500 to $1,000 at the hardware store in your first week just buying basic maintenance supplies.

These expenses aren’t limited to homebuyers. Anyone preparing to live independently should plan for moving costs, utility deposits, and basic household purchases. Read How Much Should You Save Before Moving Out on Your Own? to estimate a realistic savings target before making the move.

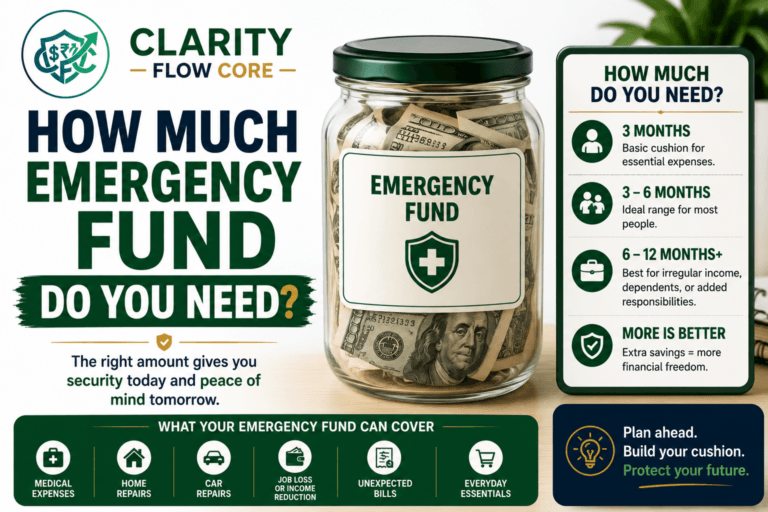

Bucket 4: The Homeowner Emergency Fund

When you rent, a broken water heater is an annoyance. You call the landlord, and they fix it. When you own the house, a broken water heater is a $1,500 emergency that you have to pay for immediately. The absolute worst financial mistake you can make is draining your checking account to exactly $0 on closing day. If you move in and the HVAC breaks the next week, you will instantly fall into high-interest credit card debt just to survive.

Before you buy a house, you must have a safety net intact after paying your down payment and closing costs. To understand exactly how to build this properly, review our comprehensive guide on Emergency Fund Basics: How Much Cash Should You Keep?.

Test your numbers safely using our Advanced Emergency Fund Analyzer to see exactly how much cash you need to keep in reserve.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetReal-World Scenario: The Math on a $300,000 House

To make this feel concrete, let’s look at a buyer named Sarah. Sarah earns a solid salary and wants to buy a $300,000 starter home. She has good credit and is using a Conventional loan. How much cash does Sarah actually need to save before she can comfortably make an offer?

- The Down Payment (5%): $15,000

- Estimated Closing Costs (3% of loan): $8,550

- Moving Costs & Utility Setup: $1,500

- Homeowner Emergency Buffer: $10,000 (kept safely in a high-yield savings account)

Total Target Savings Goal: $35,050

If Sarah only listened to generic advice, she might think she needs $60,000 (a 20% down payment) just to get started. By understanding how the math actually works, she realizes she can safely buy the home with $35,050—and $10,000 of that doesn’t even leave her bank account.

Minimum vs. Comfortable Savings Example

Depending on your risk tolerance, your final goal might shift. Here is how different preparation levels look.

| Scenario | Savings Needed | Details |

| Bare Minimum | ~$23,500 | Down payment, Closing costs |

| Comfortable | ~$35,000 | Down payment, Closing costs, Moving costs, Emergency fund |

| Very Safe | ~$45,000+ | All of the above, plus extra padding |

To calculate your own exact numbers, use our Mortgage Affordability Calculator & Home Buying Planner to estimate your required cash-to-close based on your local market.

How Much House Can You Actually Afford?

Stop guessing your home buying budget. Instantly calculate your realistic price range, estimated monthly payments, and overall loan readiness based on your exact income and debts.

Calculate My Buying Power5 Common Mistakes That Drain Home Buyer Savings

When you are tired of renting and desperate to buy, it is easy to make emotional financial decisions. Avoid these five massive beginner traps that can sabotage your savings and your mortgage approval.

1. Draining Your Savings to Avoid PMI

Many buyers are terrified of Private Mortgage Insurance (PMI). They will empty their 401(k)s, sell their cars, and drain their emergency funds entirely just to scrape together a 20% down payment so they don’t have to pay a $100 monthly PMI fee. This is incredibly dangerous. Being cash-poor with a house is vastly more stressful than paying a temporary PMI fee. Protect your liquidity.

2. Forgetting About “Prepaids” in Closing Costs

When a lender quotes you closing costs, pay close attention to “prepaids”. Depending on what month you close, the lender might require you to put six months of property taxes into an escrow account upfront. In high-tax states like New Jersey, Texas, or Illinois, this single requirement can increase your required cash-to-close by thousands of dollars overnight. See more hidden traps in The Hidden Costs of Buying a Home: What the Bank Won’t Tell You.

3. Financing Furniture Before Closing Day

You get an accepted offer on a house. You get excited. You go to a furniture store and finance a new $3,000 living room set on a “0% for 12 months” credit card. Do not do this. The lender will pull your credit report one final time a few days before closing. If they see a new credit inquiry and a new monthly debt payment, your Debt-to-Income (DTI) ratio will spike. They can—and will—deny your mortgage right before you get the keys. Check where your limits are using the Debt-to-Income (DTI) Analyzer & Loan Readiness Planner, and do not buy a single item on credit until the house is officially yours. Read exactly what you can and cannot do during this waiting period in What Happens After Mortgage Pre-Approval? A Step-by-Step Timeline.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI Ratio4. Ignoring Your Credit Score Until the Last Minute

Your credit score dictates your interest rate and the cost of your PMI. If you have a 640 credit score, you will pay significantly more in interest and insurance than someone with a 740 score. That higher monthly payment means you can afford less house. Do not wait until you apply for a mortgage to check your score. Spend the six months prior optimizing your credit profile. Run your numbers through the Credit Score Simulator & Improvement Planner to map out the fastest way to boost your score before the bank pulls it.

Simulate Your Future Credit Score

Wondering how applying for a new card, missing a payment, or paying off a loan will impact your credit? Stop guessing and run risk-free financial scenarios instantly through our free simulator.

Launch Free Credit Simulator5. Assuming Your Pre-Approval is Your Actual Budget

A bank might hand you a pre-approval letter for $450,000. That does not mean you should buy a $450,000 house. The bank calculates your maximum approval based on your gross income before taxes. They do not care about your grocery bills, your daycare costs, or your desire to take a vacation. If you spend every dime the bank offers you, you will become “house poor”. Map out your own budget before the bank tells you what to spend. Test your real-world lifestyle budget using our First-Time Homebuyer Guide: How Much House Can You Really Afford?.

Your Step-by-Step Action Plan to Start Saving

Ready to stop guessing and build a real roadmap to homeownership? Follow these steps to calculate your exact savings target.

Step 1: Define Your Realistic Home Price Look at the neighborhoods you want to live in. What is a realistic price for a starter home? Let’s say it is $250,000.

Step 2: Calculate Your Target Down Payment If you have excellent credit, aim for a 3% to 5% conventional down payment. If your credit is in the high 500s or low 600s, calculate a 3.5% FHA down payment. (Example: 5% of $250,000 = $12,500)

Step 3: Estimate Your Closing Costs To be incredibly safe, calculate 4% of the remaining loan amount. (Example: 4% of a $237,500 loan = $9,500)

Step 4: Add Your Moving and Emergency Buffer Decide exactly how much cash you refuse to part with. You need an emergency fund that can cover a sudden job loss or a blown furnace. (Example: $8,000 emergency fund + $1,000 moving costs = $9,000)

Step 5: Set Your Finish Line Add those numbers together. ($12,500 + $9,500 + $9,000 = $31,000). You now have an exact, mathematical finish line. Divide that number by your monthly savings capability to see exactly how many months away you are from buying a house.

Frequently Asked Questions (FAQs)

Can I buy a house with less than $10,000 saved?

In some situations, yes. Certain FHA, VA, USDA, and down-payment assistance programs allow qualified buyers to purchase homes with very little cash upfront. However, having additional savings for emergencies is strongly recommended.

Can I use money from my 401(k) or IRA to buy a house? Yes, but you have to be careful. The IRS allows first-time homebuyers to withdraw up to $10,000 from a traditional IRA without paying the standard 10% early withdrawal penalty (though you will still pay income taxes on it). Many 401(k) plans also allow you to take out a “401(k) loan” against your own retirement savings. However, borrowing against your future to buy a house today slows down your compound interest and should only be used as a last resort.

Can I use gift money for my down payment? Yes! Both FHA and Conventional loan programs allow you to use financial gifts from family members to cover 100% of your down payment. However, the person giving you the money must sign a legal “gift letter” stating that the money is truly a gift, not a secret loan you have to pay back.

Does the seller ever pay closing costs? They can. In real estate, this is called “seller concessions” or “seller credits”. You can structure your purchase offer so that the seller pays 2% to 3% of your closing costs out of their profit. However, in a highly competitive “seller’s market,” asking for concessions can make your offer look weaker compared to buyers who are paying their own fees.

How much money should I have left in my checking account after closing? At an absolute minimum, you should have three months of essential living expenses (including your new mortgage payment) sitting safely in a high-yield savings account the day you get your keys. This protects you against immediate layoffs or massive home repair surprises.

Do I have to pay the real estate agent’s commission? Traditionally, the seller pays the real estate commission for both the seller’s agent and the buyer’s agent out of the profits of the home sale. However, real estate commission rules have recently changed in the US, meaning buyers might have to negotiate their agent’s compensation directly. Always clarify commission structures with your agent before you start looking at houses.

Is it better to pay off debt or save for a down payment? Mathematically, high-interest credit card debt will always drain your wealth faster than a house will build it. Aggressively pay down your credit cards first. This drops your Debt-to-Income (DTI) ratio and boosts your credit score, which will ultimately get you a better mortgage interest rate anyway.

Conclusion: How Much Should You Have Saved Before Buying a House

Figuring out how much you need to save to buy a house can initially feel like an overwhelming math problem. When you start adding up down payments, title fees, inspections, and emergency buffers, the finish line can feel miles away.

But clarity brings calm. When you break the total cost down into four distinct buckets, you remove the mystery from the process. You realize that you don’t need a massive $80,000 windfall to become a homeowner. You just need a realistic target, a tight budget, and a little bit of patience.

Do not let the massive numbers intimidate you. Automate your savings, protect your credit score, and focus on building your cash reserves one paycheck at a time. The real estate market isn’t going anywhere, and when you finally hit your target number, you will be able to sign those closing papers with total financial confidence.

References & Trusted Resources

When you are planning a massive financial purchase, you should rely on data from the organizations that actually regulate the housing market. The guidelines in this article are based on standards from:

- Consumer Financial Protection Bureau (CFPB): The federal agency that regulates mortgage estimates, closing disclosures, and safe lending practices.

- Federal Housing Administration (HUD/FHA): The government body that sets the standard 3.5% down payment rules and seller concession limits for FHA borrowers.

- Fannie Mae / Freddie Mac: The government-sponsored enterprises that set the baseline down payment minimums (like the 3% first-time buyer programs) for conventional mortgages.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.