What Happens After You Pay Off All Your Debt?

Making that final payment on a student loan, credit card, or car note is one of the most exhilarating feelings you can experience. You have likely spent months, or even years, aggressively tracking your spending, making sacrifices, and sending every spare dollar to your lenders.

But if you are wondering what happens after you pay off all your debt, you might be surprised to find that the immediate aftermath can feel a little confusing. The adrenaline wears off, the rigid budget you relied on suddenly feels obsolete, and a sudden influx of unallocated cash sits in your checking account. Many people experience a bizarre sense of aimlessness.

⚡ Quick Answer

After paying off all your debt, your credit score may temporarily dip, but your long-term financial position improves dramatically. Your next priorities should be building a fully funded emergency fund, investing your former debt payments, and preventing lifestyle inflation from consuming your new cash flow.

Paying off your debt is not the finish line; it is simply the starting line for building real wealth.

In this comprehensive guide, we are going to break down exactly what happens to your credit score when an account closes, how to effectively redirect your new cash flow into wealth-building investments, and the critical financial mistakes that cause newly debt-free people to slide right back into the red.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyThe Immediate Impact: Your Net Worth Surges

The most profound shift that happens after you pay off all your debt has nothing to do with your daily budget—it happens on your personal balance sheet.

When you owe money, your liabilities drag down the value of everything you own. Eliminating those liabilities causes an instant, mathematical surge in your actual wealth. Here is a simple example of why becoming debt-free fundamentally changes your financial reality:

| Before Debt-Free | After Debt-Free | |

| Assets (Cash, Car Value, Investments) | $20,000 | $20,000 |

| Debt (Loans, Credit Cards) | $15,000 | $0 |

| Net Worth | $5,000 | $20,000 |

By simply clearing the debt, your net worth quadruples without you having to earn or save a single extra dollar in new assets.

The Credit Score Reality Check: Why Did My Score Drop?

One of the most common and frustrating experiences people face after becoming debt-free is opening their credit monitoring app and seeing their score drop. It feels like a punishment for doing the right thing.

Why does this happen? The US credit scoring system (specifically the FICO model) is designed to measure how actively and responsibly you manage borrowed money, not how wealthy you are. When you pay off a major debt, especially an installment loan like a car loan or a student loan, you alter the underlying data the algorithm uses to grade you.

Here is exactly what changes when you pay off an account:

1. Your Credit Mix Changes

Credit bureaus prefer to see that you can handle a diverse “mix” of credit. They want to see both revolving credit (like credit cards) and installment credit (loans with a fixed end date). If paying off your student loan or auto loan closes your only active installment account, your credit mix becomes less diverse, which can trigger a slight dip in your score.

2. Your Average Age of Accounts Decreases

If the loan you just paid off was one of your oldest credit accounts, closing it can eventually lower the average age of your credit history. While closed accounts in good standing stay on your credit report for up to 10 years, the algorithm may place less active weight on them.

3. Your Total Open Accounts Drop

A portion of your score is based on the sheer number of active accounts you successfully manage. Closing an account reduces that number.

The Good News: This post-debt score drop is almost always temporary. Usually, the dip ranges from 10 to 20 points, and your score will rebound within a few months as long as you continue to pay your remaining active accounts (like monthly utility bills or your standard credit card statement) on time. If you want to see exactly how your current balances and closed accounts are interacting, run your numbers through our Interactive Credit Score Simulator.

Test Your Credit Score Before Making Big Moves

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our simulator.

Launch Credit SimulatorThe First 90 Days Debt-Free Timeline

To prevent that post-debt aimlessness, you need a clear schedule. Here is exactly what you should prioritize during your first three months of total financial freedom.

| Time | Priority |

| Week 1 | Verify accounts report correctly |

| Month 1 | Build emergency fund |

| Month 2 | Automate investing |

| Month 3 | Review long-term goals |

Phase 1: Securing the Perimeter

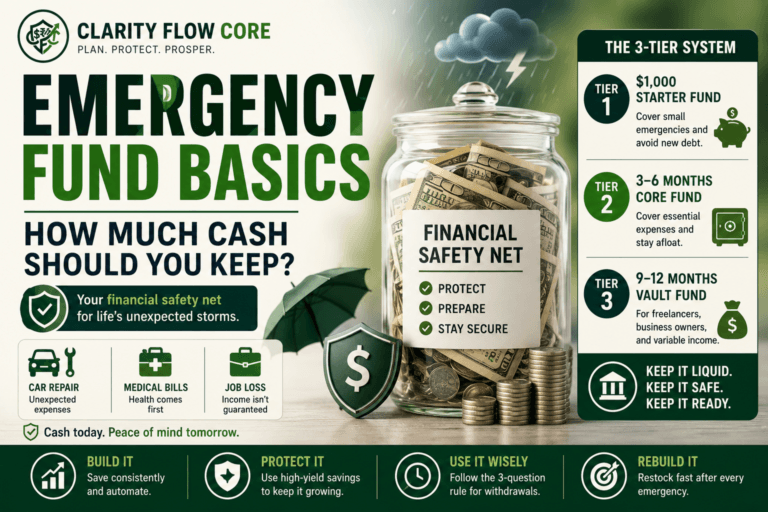

When you were climbing out of debt—whether you used the Debt Avalanche vs. Snowball method—you were likely operating with a bare-bones, $1,000 “starter” emergency fund. Now that your major monthly obligations are gone, your very first step in Month 1 is to secure the perimeter around your finances so you never have to borrow money again.

You need a fully-funded emergency cash reserve.

A starter fund covers a flat tire or a minor medical bill. A fully-funded emergency reserve covers a job loss, a major home repair, or a severe medical crisis. The rule of thumb endorsed by the Federal Deposit Insurance Corporation (FDIC) is to save three to six months of essential living expenses.

Keep this money in a High-Yield Savings Account (HYSA) where it can earn interest while remaining completely liquid. Do not invest this money in the stock market; it needs to be protected from volatility. Use our Advanced Emergency Fund Analyzer to calculate your exact target number and read our Emergency Fund Guide 2026 for strategies on where to park the cash.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetPhase 2: Redirecting Your Cash Flow Toward Wealth

This is where life after debt gets fun (Month 2 on your timeline). While you were paying off your lenders, they were earning compound interest on your money. Now, it is your turn to earn compound interest.

The most powerful wealth-building tool you have is your income. When you no longer have $500 a month going to a car payment and $300 a month going to student loans, you suddenly have an extra $800 a month in pure cash flow.

Do not let this money sit idle in a standard checking account, where inflation will slowly erode its purchasing power. (If you are unsure how much cash to keep liquid for daily expenses, check out our guide on How Much Should You Keep in Checking vs Savings?).

Instead, you need to ruthlessly redirect your former debt payments into investments.

The Wealth Multiplication Effect

To understand exactly how powerful this is, use the calculator below. Enter the total amount of money you used to spend on debt payments every month, set a reasonable market return rate (historically around 7-8% adjusted for inflation), and see what happens over the next decade.

Post-Debt Wealth Multiplier

See how redirecting your former debt payments into investments builds long-term wealth.

Total Future Wealth

Interest Earned

Where to Invest the Money First

If you are new to investing, follow this standard order of operations:

- Get the 401(k) Match: If your employer offers a match on your workplace retirement plan, contribute enough to get 100% of that match. It is literally free money.

- Fund a Roth IRA: For many newly debt-free households, a Roth IRA is the first investing account worth prioritizing after securing an employer match because future withdrawals can be tax-free. If you meet the IRS income limits, max this out.

- Max the 401(k) or HSA: Once the Roth IRA is full, return to your workplace 401(k) and increase your contributions, or fund a Health Savings Account (HSA) if you have a high-deductible health plan.

To map out your exact timeline to retirement based on your new cash flow, use our Financial Freedom Planner.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanPhase 3: Restructuring Your Daily Budget

When you were actively fighting debt, your budget was likely rigid, restrictive, and focused purely on survival. You cannot maintain an "emergency" budget forever; it leads to financial burnout.

Now that you are debt-free, you need a sustainable budgeting system that allows you to enjoy your money while still hitting your savings goals (Month 3 on your timeline). We highly recommend transitioning to the 50/30/20 Budgeting System.

Here is how it works:

- 50% Needs: Rent, groceries, utilities, and essential insurance.

- 30% Wants: Dining out, vacations, hobbies, and entertainment.

- 20% Savings & Investing: Your Roth IRA, 401(k), and sinking funds.

Because you no longer have minimum debt payments eating up your "Needs" category, you will find it incredibly easy to hit that 20% investment target. Read our complete breakdown of how to automate this system in The 50/30/20 Budget Rule Explained Simply.

If your housing costs are taking up too much of that 50% category, it might be time to evaluate your living situation. Use our Debt-to-Income (DTI) Analyzer to see where you stand, and read our guide on Renting vs Buying a Home in 2026 to decide your next move.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI RatioCommon Mistakes to Avoid After Becoming Debt-Free

The transition from "paying off debt" to "building wealth" is a fragile time. Without a clear plan, many people drift back into bad habits. Here are the three most common mistakes you must avoid:

1. Lifestyle Creep

Lifestyle creep happens when your expenses rise at the exact same rate as your available cash. You pay off your $400 car loan, so you decide you deserve a nicer apartment that costs $400 more a month. You get a $5,000 raise at work, so you take a $5,000 vacation. The money vanishes before it can be invested. To fight lifestyle inflation, automate your investments so the money leaves your checking account before you even see it.

2. Closing Old Credit Cards Just Because They Are Zero

When you finally pay off a credit card that caused you years of stress, the temptation is to call the bank and cancel the account out of spite. Do not do this. Closing old revolving credit lines will drastically lower your total available credit, which instantly spikes your credit utilization ratio. This will cause a sharp drop in your credit score.

Instead, keep the accounts open, put a small recurring subscription (like Netflix) on them, and set them to autopay in full every month. If you need a refresher on how to manage credit safely without carrying a balance, check out our guide on the Best Credit Cards for Beginners.

If you're rebuilding your credit history or don't currently have an active credit card, Best Secured Credit Cards for Beginners in 2026 compares beginner-friendly secured cards that can help you maintain positive payment history without carrying debt.

3. Fearing All Debt Unnecessarily

While consumer debt (credit card balances, high-interest personal loans) is toxic to wealth building, not all debt is bad. A fixed-rate mortgage on a property that appreciates in value is a standard tool for building net worth. Do not let the trauma of paying off high-interest credit cards prevent you from making strategic, calculated financial moves in the future.

Your Step-by-Step Action Plan for a Debt-Free Life

To ensure you never slide backward, follow this chronological sequence immediately after making your final debt payment.

1.Pull Your Official Credit Reports: Wait for the accounts to settle.

Wait 30 to 45 days after your final payment, then pull your official reports from AnnualCreditReport.com. Verify that the balances officially read $0 and that the lenders have reported the accounts as "Paid in Full" or "Closed in Good Standing."

2.Automate Your New Savings: Redirect the cash flow immediately.

Before you get used to seeing the extra cash in your checking account, log into your payroll provider and increase your 401(k) contributions, or set up an automatic monthly transfer from your checking account to your brokerage account.

3.Fully Fund the Emergency Reserve: Build the permanent safety net.

If your emergency fund is currently sitting at the $1,000 starter level, pause your heavy investing just long enough to build that cash reserve up to three to six months of living expenses.

4.Plan a Cash-Funded Celebration: Acknowledge the sacrifice.

You worked incredibly hard to achieve this. Budget a specific amount of cash—whether it is $100 for a great dinner or $1,000 for a weekend trip—and celebrate the milestone without using a credit card.

Frequently Asked Questions (FAQ)

Does paying off debt lower your credit score permanently?

No. While you may see a temporary drop of 10 to 20 points due to a change in your credit mix or the closure of an old installment loan, your score will recover within a few months as long as you continue to pay your remaining active accounts on time and keep your credit utilization low.

Should I close my credit cards after I pay them off?

Generally, no. Closing credit cards reduces your total available credit, which increases your overall credit utilization ratio. This will negatively impact your credit score. The only time you should close a card is if it carries a massive annual fee that you no longer want to pay, or if keeping it open presents a genuine temptation to overspend.

What should I do with my extra money after paying off debt?

Your exact priorities should be: 1) Build a 3-to-6-month emergency fund in a high-yield savings account, 2) Secure any available employer match in your 401(k), 3) Max out a Roth IRA if eligible, and 4) Save for mid-term goals like a house down payment or a replacement vehicle.

How do I stop myself from getting into debt again?

The two strongest defenses against returning to debt are a fully-funded emergency cash reserve and a realistic, automated budget. Most people fall back into credit card debt because they face an unexpected emergency without a cash buffer, or because they try to follow a budget that is too restrictive and eventually "binge" spend.

Is it better to invest or pay off my mortgage early?

This is a mathematical and emotional debate. Mathematically, if your mortgage interest rate is very low (e.g., 3-4%), you will historically earn a higher return by investing extra money in the stock market (which averages 7-10%). Emotionally, many people prefer the profound security of owning their home free and clear, regardless of the math. A balanced approach is to invest heavily while making one or two extra mortgage principal payments a year.

Conclusion

Reaching a zero balance on your debts is a monumental achievement that the vast majority of people never accomplish. But knowing what happens after you pay off all your debt is what separates those who simply survive from those who build generational wealth.

Expect a slight, temporary dip in your credit score, but do not let it discourage you. Your primary job now is to protect your new cash flow from lifestyle inflation, build a bulletproof emergency fund, and aggressively redirect your former debt payments into compounding investments. You have spent years working for your lenders; starting today, your money works for you.

References

- Consumer Financial Protection Bureau (CFPB): Guidelines on understanding credit reports, credit scores, and the impact of paying off installment loans.

- Federal Deposit Insurance Corporation (FDIC): Official recommendations for building and maintaining liquid emergency savings funds.

- Federal Reserve Board: Data on average consumer debt burdens and the historical long-term averages of market returns.

- Internal Revenue Service (IRS): Current contribution limits and tax advantages for 401(k) and Roth IRA retirement accounts.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.