FHA vs Conventional Loan: Which Is Better for First-Time Home Buyers in 2026?

If you are reading this, you are probably exhausted by the sheer amount of financial jargon standing between you and the front door of your first home. You likely started this journey scrolling through real estate apps late at night, imagining where you would put your furniture. Then, you clicked on the little “Estimated Monthly Payment” button.

Suddenly, the dream felt a lot heavier.

When you decide to buy a house, you are immediately thrown into an alphabet soup of banking terms. Loan officers toss out acronyms like LTV, DTI, PMI, and MIP as if you have been working on Wall Street your entire life. But out of all the confusing choices you have to make, the very first—and arguably the most important—is choosing the fundamental structure of your mortgage.

For the vast majority of normal, first-time home buyers in 2026, that choice boils down to a heavyweight title fight: FHA vs Conventional Loan.

You might have heard a family member say, “You have to get a conventional loan, FHA is a ripoff!” Or maybe a real estate agent told you, “Just use an FHA loan, it is the only way a beginner can get approved.” Both of these statements are wildly inaccurate oversimplifications.

The finance industry loves to pretend there is a “one-size-fits-all” answer to buying a home. There isn’t. The right loan for your coworker might be a terrible financial trap for you. Making the wrong choice between these two loans can cost you tens of thousands of dollars in hidden insurance fees over the next decade, or it can cause a bank to flat-out deny your application on closing day.

Let’s strip away the corporate banking jargon. We are going to look at the raw mechanics of an FHA vs conventional loan, compare the real-world math of the hidden insurance fees, expose the beginner mistakes that ruin approvals, and help you figure out exactly which path will safely get the keys into your hands.

FHA vs Conventional Loan: Who Is Actually Backing You?

Before we look at the math, you have to understand why banks treat these two loans so differently. When a bank lends you hundreds of thousands of dollars, their biggest fear is that you will lose your job, stop making payments, and force them into a messy foreclosure.

The Conventional Loan (The Standard Private Path)

A conventional loan is not insured by the federal government. It is a private loan created by a private lender, which is eventually sold to massive mortgage corporations (like Fannie Mae or Freddie Mac). Because the government is not offering a safety net, the bank is taking on the full risk. To protect themselves, they require you to have a cleaner financial history, a higher credit score, and a healthy down payment. If you look risky on paper, a conventional lender will simply deny you.

The FHA Loan (The Government Safety Net)

FHA stands for the Federal Housing Administration. The FHA does not actually lend you the money—they just insure the loan. You still go to a normal bank or mortgage broker, but the FHA promises the bank, “If this buyer loses their job and defaults on the loan, the U.S. government will pay you back the money you lost.” Because the bank is practically guaranteed not to lose money, they are willing to drastically lower their standards. They will approve people with lower credit scores, smaller down payments, and bumpier financial histories. It is the ultimate beginner-friendly safety net.

However, the government does not offer this safety net for free. You, the buyer, are the one who pays for that insurance. And that insurance is exactly where the math between these two loans completely diverges.

The Gatekeepers: Credit Score Requirements

When people ask which loan is “better,” the honest answer is that your credit score usually makes the decision for you.

FHA Loans: The Forgiving Path

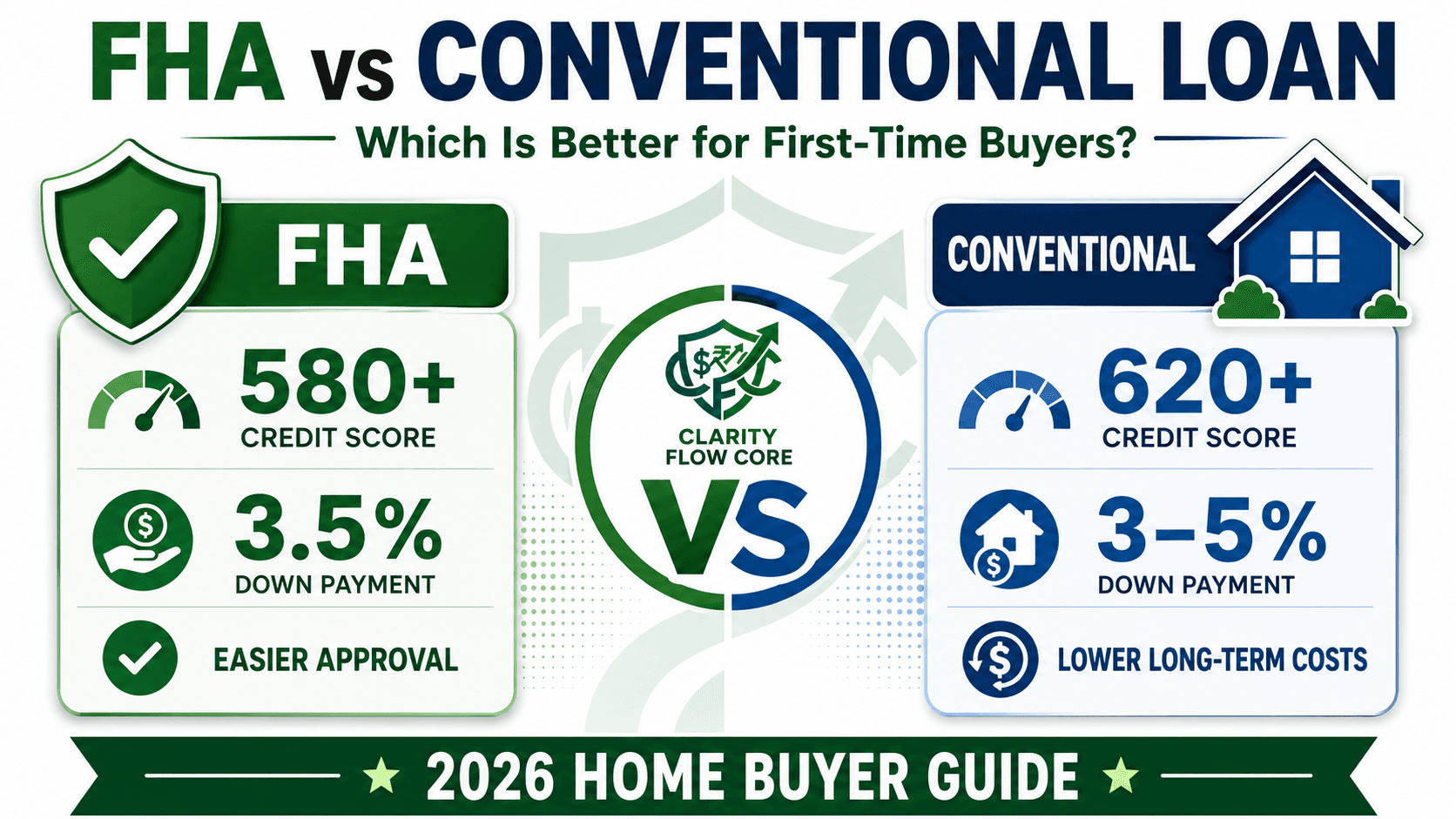

Legally, FHA guidelines allow you to buy a home with a credit score as low as 580 (and technically down to 500 if you have a massive 10% down payment). Because the loan is insured by the government, the underwriter is willing to overlook past mistakes. If you had a medical emergency that dragged your score down, or if you missed a credit card payment two years ago, the FHA path is often the only realistic way to get approved.

Note: While the government allows a 580 score, many individual banks set their own stricter rules (called “overlays”) and require at least a 600 or 620 to process an FHA loan in 2026.

Conventional Loans: The Strict Path

The absolute bare minimum credit score required for a conventional loan is 620. However, having a 620 does not mean a conventional loan is a good idea. Conventional loans use “risk-based pricing.” If your score is sitting at 630, the bank is going to charge you a significantly higher interest rate and massive private mortgage insurance premiums to offset your risk.

To actually get the great interest rates you see advertised on TV for a conventional loan, you typically need a credit score of 680 or higher (with 740+ getting the absolute best pricing).

Pro Tip: Before you start talking to a loan officer, figure out exactly where you stand. If your score is bordering on the 620 mark, run your numbers through ourFree Credit Score Simulator & Improvement Plannerto map out the fastest mathematical path to boost your score before applying.

The Down Payment Reality: How Much Cash Do You Need?

If you talk to an older relative about buying a house, they will inevitably tell you that you must save up a 20% down payment. In 2026, telling a normal young adult or a working family to save 20% of a $400,000 house ($80,000 in cash) while paying record-high rent is financially absurd.

Thankfully, the 20% rule is a complete myth. Both loan types are designed to get you into a house with a fraction of that cash.

The FHA Down Payment (3.5%)

The FHA requires a minimum down payment of exactly 3.5% of the purchase price. If you are buying a $300,000 house, you need $10,500 for the down payment. It is a highly predictable, flat requirement. The government also allows 100% of that down payment to be a financial gift from a family member, making it highly accessible for young buyers.

The Conventional Down Payment (3% to 5%)

Surprisingly, conventional loans can actually require less cash out of pocket than an FHA loan. If you are a first-time home buyer, Fannie Mae and Freddie Mac offer specific conventional programs (like HomeReady and Home Possible) that allow you to put down just 3%. For a $300,000 home, that is $9,000.

If you do not qualify for the specialized first-time buyer programs, the standard minimum down payment for a conventional loan is usually 5%.

The Hidden Cost: Mortgage Insurance (PMI vs. MIP)

This is the most critical section of this entire guide. If you understand this, you will know exactly which loan to choose.

Because you are putting down less than 20%, both loans require you to pay monthly mortgage insurance to protect the lender. But the way FHA and conventional loans charge this insurance is drastically different, and it is usually the deciding factor in which loan is cheaper over the long run.

Conventional Loan Insurance (PMI)

On a conventional loan, this fee is called Private Mortgage Insurance (PMI). The cost of PMI is entirely dependent on your credit score and your down payment.

- If you have a 760 credit score, your PMI might only be $50 a month.

- If you have a 630 credit score, that exact same PMI might cost you $250 a month because you are viewed as a higher risk.

The Best Part: Conventional PMI automatically drops off your loan. Once you pay your mortgage down and reach 20% equity in the home, the bank legally has to remove the PMI charge. Your monthly payment instantly gets cheaper, and you never pay for that insurance again.

FHA Loan Insurance (MIP)

On an FHA loan, the insurance is called the Mortgage Insurance Premium (MIP), and it hits you with a brutal one-two punch.

Punch 1: The Upfront Fee (UFMIP)

The moment you close an FHA loan, the government charges you a 1.75% fee on your total loan amount. On a $300,000 loan, that is $5,250. You do not have to pay this in cash; the bank simply rolls it into your total loan balance. But it means you instantly start your mortgage owing thousands of dollars more than the house is worth. Conventional loans do not have this upfront fee.

Punch 2: The Annual Fee (MIP)

FHA also charges an annual insurance fee (divided into 12 monthly payments). Currently, for most standard FHA loans with a 3.5% down payment, the rate is 0.55% of the loan amount.

Unlike conventional PMI, FHA insurance does not care about your credit score. A person with a 580 score and a person with an 800 score will pay the exact same 0.55% rate.

The Worst Part: If you make the standard 3.5% down payment, FHA monthly mortgage insurance never drops off. You will pay that fee every single month for the entire 30-year life of the loan. The only way to get rid of FHA mortgage insurance is to sell the house or eventually refinance the mortgage entirely into a conventional loan.

The Tale of Two Buyers (The Math)

Let’s look at a $350,000 house to see how this actually plays out in the real world.

Buyer 1: Excellent Credit (740 Score)

Because this buyer has a great score, a conventional loan is a no-brainer. Their conventional interest rate is low, and their conventional PMI is incredibly cheap (around $60 a month). They avoid the massive FHA upfront fee, and their PMI will drop off entirely in a few years once they build equity.

Buyer 2: Struggling Credit (640 Score)

If this buyer tries to get a conventional loan, the bank will punish their lower score. Their interest rate will be high, and their conventional PMI could easily be $250+ a month.

For Buyer 2, the FHA loan is dramatically cheaper. Even with the 1.75% upfront fee and the permanent monthly MIP, the FHA system does not penalize their 640 score. The FHA monthly payment will likely be hundreds of dollars cheaper than the conventional option.

FHA vs Conventional: Compare Your Numbers

Don’t guess which loan is better for you. Use our free Mortgage Affordability Calculator to get an instant side-by-side comparison of your FHA and Conventional loan eligibility, including estimated PMI costs.

Property Standards: The “Fixer-Upper” Trap

There is one more massive hurdle that catches beginners completely off guard: the appraisal.

When you get a conventional loan, the bank sends an appraiser to simply make sure the house is worth the money you are paying for it. If the house needs some cosmetic work, has an ugly kitchen, or has a cracked window, the conventional appraiser generally does not care.

The FHA appraiser is a completely different story. Because the government is insuring the loan, they mandate strict health and safety standards. The FHA appraiser acts more like an inspector.

- If there is peeling paint on the exterior of a home built before 1978 (lead paint hazard), FHA will deny the loan.

- If a staircase has more than three steps and is missing a handrail, FHA will deny the loan.

- If the roof has less than two years of life left, FHA will deny the loan.

If you are planning to buy a cheap, run-down “fixer-upper” property to renovate yourself, an FHA loan will almost certainly be rejected unless the seller agrees to fix all those safety issues before closing day. In a competitive housing market, sellers often refuse to make repairs, which is why sellers sometimes prefer buyers with conventional loans over FHA buyers.

5 Brutal Beginner Mistakes to Avoid in 2026

When beginners jump into the housing market, they often rely on outdated advice or panic-driven decisions. If you want to protect your savings and guarantee your approval, avoid these five massive landmines.

1. Assuming FHA is Only for “First-Time” Buyers

Despite the popular myth, you do not have to be a first-time home buyer to use an FHA loan. If you owned a house five years ago, sold it, rented an apartment, and want to buy again, you can absolutely use an FHA loan. The only major restriction is that an FHA loan must be used for your “primary residence.” You cannot use it to buy a vacation home or a pure investment property.

2. Ignoring the Debt-to-Income (DTI) Ratio Trap

Many people think that if they have a 700 credit score, they are automatically approved for whichever loan they want. This is false. Lenders care deeply about your Debt-to-Income (DTI) ratio, which compares your monthly debt payments against your gross income. If half of your paycheck is already going toward massive truck payments and maxed-out credit cards, neither conventional nor FHA lenders will approve you. FHA is slightly more forgiving on DTI, but a heavy debt burden will crush your borrowing power on both sides.

3. Thinking You Are “Stuck” With FHA Insurance Forever

We established earlier that FHA mortgage insurance never drops off automatically if you put 3.5% down. This terrifies beginners. But in the real world, almost nobody keeps an FHA loan for 30 years. You use the FHA loan to get your foot in the door today. Five years from now, when the house has gone up in value and you have paid down some of your high credit card utilization, your credit score will naturally be much higher. At that point, you simply refinance the house into a conventional loan, and the FHA mortgage insurance disappears forever.

4. Draining Your Checking Account for the Down Payment

The absolute worst thing you can do as a new homeowner is put every single penny you have into the down payment just to avoid mortgage insurance. When you own a house, the landlord no longer fixes the broken water heater. If you move in with $0 in your checking account and the roof leaks, you will immediately fall into high-interest credit card debt just to survive. Before you buy, you must use our Advanced Emergency Fund Analyzer to map out your homeowner safety net. Keep your cash reserves safe; paying $100 a month in mortgage insurance is vastly better than facing a $5,000 emergency with an empty bank account.

5. Forgetting About the Hidden Closing Costs

The down payment is just the entry fee. You also have to pay “Closing Costs” (appraisal fees, title insurance, loan origination fees, property taxes). These usually total an additional 2% to 5% of the purchase price. If you only saved exactly 3.5% for an FHA down payment, you will not have enough cash to actually close the loan. Always budget for closing costs, or read our guide on The Hidden Costs of Buying a Home: What the Bank Won’t Tell You to avoid being blindsided at the closing table.

The Beginner-Friendly Action Plan: How to Choose

If you are staring at a screen right now trying to decide which path to take, you do not need to guess. The math will make the decision for you if you follow this step-by-step roadmap.

Step 1: Check your actual FICO scores.

Do not rely on the free educational app on your phone. Mortgage lenders use specific, older FICO models. Buy your actual mortgage scores. If your middle score is above 680, lean toward Conventional. If it is below 660, lean heavily toward FHA.

Step 2: Map your borrowing power (DTI).

Before a lender tells you what you can afford, figure it out yourself privately. If your monthly debt obligations are dragging you down, a bank will limit your loan size regardless of which program you choose.

⚖️ Wait, What Is My Actual DTI?

You know the limits, but are you worried that your credit score or current debt load might disqualify you? Stop guessing the math. Run your numbers through our free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner to calculate your true borrowing power and see exactly where you stand today.

Calculate My Loan Readiness →Step 3: Ask a broker for a side-by-side comparison.

When you finally talk to a mortgage broker, do not ask them to “pick” for you. Ask them to print out two Loan Estimates for the exact same house—one for an FHA loan, and one for a Conventional loan. Look directly at the “Estimated Monthly Payment” and the “Cash to Close” lines. The cheaper math will be staring right back at you.

Step 4: Understand the next steps.

Once you pick your loan path, the real work begins. Read our step-by-step timeline on exactly What Happens After Mortgage Pre-Approval so you know exactly what the underwriter is going to demand from you next.

Frequently Asked Questions (FAQs)

Can I switch from an FHA loan to a Conventional loan later?

Yes, absolutely. This is incredibly common. Buyers often use an FHA loan to get into the house because it is forgiving of lower credit scores. A few years later, when their credit has improved and they have built at least 20% equity in the property, they refinance into a conventional loan to permanently drop the FHA mortgage insurance.

Do home sellers prefer buyers with conventional loans?

In a highly competitive “seller’s market,” yes. Sellers often prefer conventional buyers because conventional appraisals are less strict. The seller knows that an FHA appraiser might flag peeling paint or a missing handrail, forcing the seller to pay for repairs before the deal can close.

Is an FHA loan only for low-income home buyers?

No. FHA loans do not have any income limits. You can make $300,000 a year and still use an FHA loan. They are designed for people with lower credit scores or smaller down payments, regardless of how high their annual income is.

Can I buy a multi-family home with an FHA loan?

Yes! This is one of the most powerful wealth-building strategies available. You can use an FHA loan to buy a 2, 3, or 4-unit property with just 3.5% down, as long as you live in one of the units as your primary residence. You can then rent out the other units to help cover the mortgage.

Do my student loans disqualify me from getting an FHA loan?

No, but they do heavily impact your borrowing power. When calculating your Debt-to-Income ratio, the FHA underwriter has to include your student loan payments. If your loans are in deferment or on an income-driven repayment plan, the FHA uses specific guidelines (usually 0.5% of the total loan balance) as your assumed monthly payment to make sure you can still afford the mortgage safely.

What is the maximum amount of money I can borrow with an FHA loan?

FHA sets strict loan limits that change every year based on the housing costs in your specific county. In 2026, the loan limit in a low-cost, rural county is significantly lower than the loan limit in a high-cost metropolitan area like Los Angeles or New York City. You can look up your exact county’s limit on the HUD.gov website.

References & Trusted Resources

When you are signing a 30-year financial contract, you should only trust data directly from the authorities who regulate the housing market. We verified the policies and calculations in this guide using the following sources:

- U.S. Department of Housing and Urban Development (HUD): The federal department that oversees and administrates the FHA loan program and sets the annual MIP limits. (HUD.gov)

- Consumer Financial Protection Bureau (CFPB): The government agency that regulates mortgage lenders and provides unbiased tools for comparing loan estimates. (ConsumerFinance.gov)

- FICO: The analytics software company that creates the exact credit scoring models that mortgage lenders use to evaluate conventional and FHA applications. (MyFICO.com)

Final Thoughts: Give Yourself Permission to Begin

Looking at the difference between an FHA vs conventional loan can easily make you feel paralyzed by analysis. You start worrying about insurance percentages, credit score brackets, and whether you are making a thirty-year mistake.

Here is the truth that experienced homeowners know: your first mortgage is just a tool. It is a temporary vehicle to get you out of the renting cycle and into an asset that belongs to you.

Do not let the fear of a perfect decision keep you from making a good decision. If a conventional loan makes the math perfectly affordable for your family today, take it. If you need the safety net of an FHA loan because life got messy a few years ago, embrace it without shame. The banking system thrives on making you feel unqualified, but thousands of normal, everyday people navigate this exact same math and close on their homes every single day.

Take a deep breath. Calculate your true borrowing power, plan your long-term wealth goals, and stop waiting for a perfect moment. Your future home is out there, and you are entirely capable of figuring out the math to get the keys. You’ve got this.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.