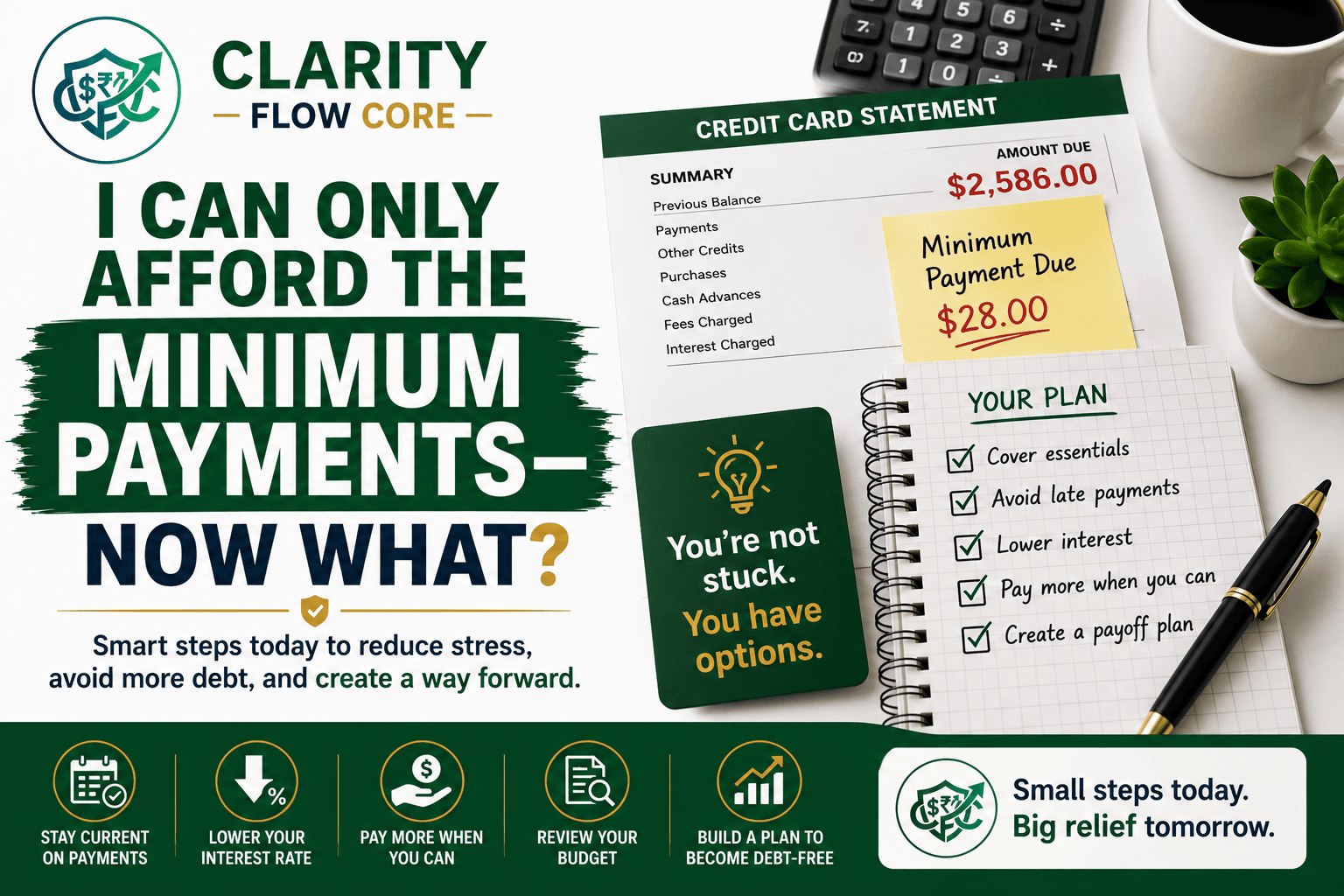

I Can Only Afford the Minimum Payments — Now What?

You log into your banking app, and your stomach immediately drops.

You see the total balance on your credit card, and it’s a number you don’t even want to look at. Then, your eyes drift down to the “Minimum Payment Due.” You do some quick mental math, looking at your checking account, your upcoming rent, and your grocery needs for the week.

A wave of panic hits you. You realize that you can’t afford to pay anything extra this month. If you can only afford minimum payments on credit cards, you might be scraping the bottom of your checking account just to keep the account current.

If you are reading this right now and feeling a mix of shame, anxiety, and exhaustion, take a deep breath. You are not alone, you are not a failure, and you are not the only one secretly struggling with this. Millions of Americans are currently treading water, paying just enough to keep the credit card companies off their backs.

⚡ Quick Answer

If you can only afford minimum payments on credit cards, focus on keeping all accounts current while protecting your essential expenses like housing, food, utilities, and transportation. Then explore hardship programs, balance transfers, debt management plans, or extra income opportunities to create room in your budget. Paying only the minimum is not ideal, but missing payments usually creates a much bigger problem.

The Real Problem: The Minimum Payment Trap

To figure out how to get out of this situation, you first have to understand how the trap is built. Credit card companies are not your friends. They are businesses designed to make money, and their favorite customers are the ones who pay only the minimum.

When you make a minimum payment, you might assume you are slowly chipping away at your debt. The harsh reality is that you are mostly just paying for the privilege of holding that debt.

Credit card issuers typically calculate your minimum payment as a tiny percentage of your total balance (usually around 1% to 2%) plus whatever interest was charged that month. Because credit card interest rates (APRs) are notoriously high—often sitting between 20% and 30%—the vast majority of your payment goes straight to interest.

The Math of Minimum Payments

Let’s look at exactly what happens to your money when you only pay the minimum on a card with a typical 24% interest rate.

| Credit Card Balance | APR | Approximate Minimum Payment | Total Interest Paid If Only Minimums |

| $2,000 | 24% | ~$60 | Thousands over time |

| $5,000 | 24% | ~$150 | Nearly $3,000+ |

| $10,000 | 24% | ~$300 | Potentially $7,000+ |

If you pay your $150 minimum on a $5,000 balance, you might feel good that you met your obligation. But behind the scenes, about $100 of that payment went entirely toward interest. Only $50 actually went toward reducing your actual debt.

When you are only making minimum payments, you aren’t paying down debt. You are renting it. And the rent is incredibly expensive.

Why This Happens (And Why You Need to Drop the Guilt)

There is a toxic narrative in personal finance that says if you are in credit card debt, it’s because you lack discipline. People picture someone buying designer clothes or taking lavish vacations they can’t afford.

That is rarely the truth.

Most people end up stuck in the minimum payment cycle because life simply happened. Maybe your car broke down, and you needed it fixed to get to work. Maybe you had an unexpected medical emergency, and the out-of-pocket costs drained your savings. (What To Do If Medical Bills Are Destroying Your Budget). Maybe your rent was raised, but your salary wasn’t, so you started using your credit card to buy groceries just to make it to the end of the month.

When your income no longer covers your basic living expenses, credit cards become the safety net. The problem is that it’s a safety net woven out of high-interest barbed wire. Forgive yourself for doing what you had to do to survive a tough month. Guilt will not pay off your balance. Clear-headed strategy will.

When Paying Only the Minimum Is Actually the Right Move

Personal finance is incredibly nuanced, and it is crucial to recognize that there are specific moments in life where paying the minimum is exactly what you should be doing.

Sometimes, survival comes before optimization.

If you are currently in the middle of a major life crisis, your financial priorities have to shift to self-preservation. You should absolutely drop down to making only minimum payments if you:

- Recently lost your job and need to hoard cash until you secure a new paycheck.

- Are facing a major medical emergency and need liquid cash for treatments or prescriptions.

- Experienced a sudden, temporary income reduction (like a cut in hours or a freelance dry spell).

- Are going through a major life disruption, such as recovering from a divorce or a death in the family.

In these scenarios, aggressively paying down debt leaves you with zero cash buffer. If an emergency pops up, you’ll be forced to borrow that money right back, usually at a higher cost. Protect your four walls first: housing, food, basic transportation, and keeping the lights on. (Behind on Bills? Which Payments Should You Prioritize First?). Keep the credit card companies happy with the bare minimum until the storm passes.

Before using every available dollar to pay debt, Emergency Fund Basics: How Much Cash Should You Keep? explains why even a small cash buffer can prevent you from relying on credit cards again.

Common Mistakes People Make in the Minimum Payment Phase

If you aren’t in a temporary crisis and are just stuck in the cycle, panic usually takes over. And panic leads to decisions that can turn a stressful situation into a disaster. Before we talk about how to fix the problem, make sure you aren’t accidentally making it worse.

Mistake 1: Hiding from the numbers.

When money is tight, the natural human instinct is to avoid looking at bank accounts. You know it’s bad, so you don’t log in. But avoiding the numbers doesn’t change them; it just robs you of the information you need to make a plan. You cannot fix a problem if you refuse to look at it.

Mistake 2: Using credit to pay credit.

If you are taking cash advances from one credit card to make the minimum payment on another, the alarm bells should be ringing. Cash advances come with exorbitant fees and even higher interest rates that start accruing immediately. This is financial quicksand.

Mistake 3: Turning to payday loans.

If you are short on cash for a minimum payment, a payday loan might look like a quick fix. Do not do it. Payday loans have equivalent interest rates of 300% to 400%. They are predatory products designed to trap you in a cycle of borrowing that is incredibly difficult to escape.

What Happens If You Only Keep Making Minimum Payments?

If you stay in the minimum payment phase for too long, things start to quietly break down in the background.

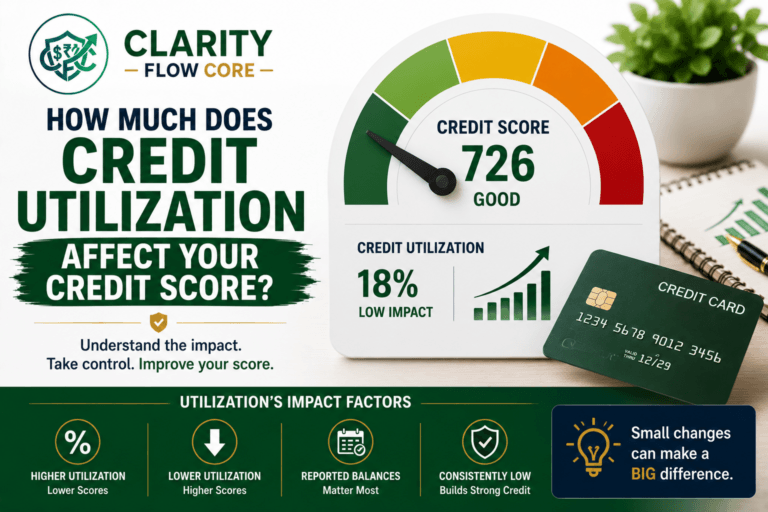

First, your credit utilization ratio will likely spike. Wondering how many points high utilization can actually cost you? How Much Does Credit Utilization Affect Credit Score? breaks down the real-world impact across different utilization levels. This is the amount of credit you are using compared to your total available credit. When your balances sit near your limits because you are only paying the minimum, your credit score takes a massive hit. (How Long Does It Really Take To Rebuild Bad Credit?). A lower credit score makes it harder to get approved for apartments, better loan rates, or sometimes even jobs.

If your score has already fallen because of high balances or missed payments, How Long Does It Really Take To Rebuild Bad Credit? explains what recovery realistically looks like.

💳 Is High Utilization Tanking Your Score?

When you only pay the minimum, your credit utilization ratio stays dangerously high, which actively drags down your FICO score. Plug your current balances and limits into our free Credit Utilization Recovery System to calculate your exact ratio and build a strategic payoff timeline.

If you’re unfamiliar with how credit utilization is calculated or why lenders care so much about it, What Is Credit Utilization — And Why Does It Matter? explains this important credit score factor in detail.

Second, the psychological weight becomes exhausting. Waking up every day knowing that a chunk of your paycheck is already promised to a bank creates a low-level, constant hum of anxiety. It strains relationships, destroys your focus at work, and makes it impossible to sleep.

You have to break the cycle.

Practical Solutions: How to Get Unstuck

If you can only afford the minimums, your current budget is completely maxed out. You cannot simply “budget better” when there is zero money left over. You need structural changes to your debt.

1. Stop the Bleeding (The Credit Card Freeze)

Before you do anything else, you have to stop adding to the balances. You cannot dig your way out of a hole while still holding a shovel. Take your credit cards out of your wallet. Delete the saved card numbers from Amazon and your food delivery apps. If you are using the cards for daily living expenses because you have no cash, you have a severe income-to-expense crisis that has to be addressed before you can tackle the debt.

2. Call the Credit Card Company and Ask for Hardship

People are terrified of calling their creditors, assuming the bank will demand immediate payment. But credit card companies actually have entire departments dedicated to keeping you from defaulting.

Call the number on the back of your card and say, “I am experiencing a financial hardship, and I am struggling to make my minimum payments. What hardship programs do you have available?” Many issuers offer short-term programs that lower your interest rate drastically (sometimes down to 0% to 5%) for 6 to 12 months, waive late fees, or temporarily lower your minimum payment. The catch is they will usually freeze your card so you can’t make new purchases. If your goal is to pay off the debt, freezing the card is exactly what you need.

3. Look into a Balance Transfer

If you have been making your minimum payments on time, your credit score might still be in decent shape. If so, you could apply for a balance transfer credit card.

These cards offer a 0% introductory APR for a set period (usually 12 to 21 months). You move your high-interest debt onto this new card. Suddenly, 100% of your minimum payment is actually going toward your principal balance. However, you usually have to pay a 3% to 5% transfer fee. And if you don’t pay off the balance before the 0% period ends, the high interest comes roaring back.

4. Debt Management Plans (DMPs)

If your credit score has already dropped, or you feel completely overwhelmed, a Debt Management Plan might be your lifeline.

You work with a non-profit credit counseling agency (look for agencies affiliated with the NFCC). A counselor reviews your finances and negotiates with your creditors to get your interest rates slashed and late fees dropped. You then make one single monthly payment to the credit counseling agency, and they distribute the money to your creditors. It usually takes 3 to 5 years, and your credit cards will be closed, but it gives you a structured, manageable path out of the trap.

If you’re considering multiple ways to deal with overwhelming debt, Debt Consolidation vs Debt Settlement: Which Actually Saves More Money? compares two of the most common debt relief strategies.

A Beginner-Friendly Action Plan

Reading about options is one thing; actually doing it is another. If you are paralyzed by anxiety, here is your step-by-step survival plan for this week.

Step 1: Face the Monster

Write down every single credit card you have. Write the total balance, the interest rate (APR), and the minimum payment due. Total it all up. It will probably hurt to look at, but clarity is the antidote to anxiety.

⚖️ How Much of Your Paycheck is Trapped?

Don’t do the math in your head. Plug your total minimum payments and gross income into our free Debt-to-Income (DTI) Analyzer to see exactly where you stand, so you can build a realistic, math-based escape plan today.

Step 2: Build a “Bare Bones” Survival Budget

Strip your budget down to the absolute essentials. Housing, basic utilities, basic groceries, transportation to work, and essential medications. Cut the subscriptions and the takeout. You don’t have to live like this forever, but you need to see exactly how much cash you actually have to work with right now.

Step 3: Hunt for Immediate Cash

You need breathing room. What can you sell on Facebook Marketplace or eBay? Can you do gig work (DoorDash, Uber, TaskRabbit) for just a few weekends? If you can generate a quick $500, that is money that can either give you a buffer in your checking account or be thrown at your smallest debt to eliminate one minimum payment entirely.

Step 4: Pick Your Target

If you manage to scrape together an extra $50 a month, pick one target. Use the Debt Snowball method (put the extra money toward the card with the smallest total balance). Eliminating your smallest debt entirely frees up that minimum payment, giving your monthly budget instant relief.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyFrequently Asked Questions

Does paying only the minimum hurt my credit score?

Making the minimum payment on time keeps you from getting a “missed payment” mark on your credit report. However, because your balance isn’t really going down, your credit utilization stays high, which drags your score down over time.

Can I negotiate my credit card interest rate?

Yes. Many credit card issuers offer hardship programs, temporary interest-rate reductions, fee waivers, or payment assistance plans if you contact them before falling seriously behind. If you’ve generally paid on time, it’s often worth asking what options are available.

What happens if I just miss a payment?

You will be hit with a late fee (often up to $40). If you are more than 60 days late, the credit card company can impose a “penalty APR,” jacking your interest rate up to 30% or more. Once a payment is 30 days late, it is reported to the credit bureaus, which can tank your credit score by 50 to 100 points instantly.

If your missed payments eventually lead to collection agencies contacting you, don’t ignore them or rush into an agreement. How To Handle Debt Collectors Without Making Things Worse explains how to verify the debt, understand your legal rights, and negotiate confidently.

Should I drain my emergency fund to make more than the minimum payment?

Generally, no. You should keep a small starter emergency fund (usually $1,000 or one month of basic expenses). If you drain your savings completely to pay off the credit card, what happens when your tire blows out next week? You will just have to put it right back on the credit card.

You Can Get Through This

Feeling trapped by minimum payments is exhausting. It makes you feel like you are working hard every single day just to hand your paycheck over to a bank.

But please remember this: Your current financial situation is a season, not a life sentence.

You are not the first person to feel overwhelmed by debt, and you will not be the last. Credit card debt can be difficult to escape because high interest charges slow down progress and make balances harder to reduce. By looking at your numbers, calling your lenders, or reaching out to a non-profit credit counselor, you are taking your power back.

It might take some uncomfortable phone calls, a few months of a painfully tight budget, and a lot of patience. But there is a day in your future where you will log into your banking app, look at your credit card balance, and see a beautiful, stress-free zero.

Where to Learn More

If you’re currently struggling to keep up with minimum payments, the following organizations provide reliable information on credit card debt, hardship options, credit counseling, and consumer rights. These resources can help you make informed decisions while working toward becoming debt-free.

- Consumer Financial Protection Bureau (CFPB) — Credit Cards & Debt

Learn about managing credit card debt, understanding interest charges, and exploring repayment options. - National Foundation for Credit Counseling (NFCC) — Find a Certified Credit Counselor

Access nonprofit credit counseling services, debt management plans (DMPs), and financial education resources. - Federal Trade Commission (FTC) — Coping with Debt

Consumer guidance on prioritizing bills, communicating with creditors, and avoiding debt relief scams. - Consumer Financial Protection Bureau (CFPB) — Debt Collection

Information about your rights when dealing with creditors and debt collectors, including protections under federal law. - FICO® — What’s in Your FICO® Score?

Understand how payment history and credit utilization influence your credit score while you’re repaying debt. - AnnualCreditReport.com — Request Your Free Credit Reports

Review your credit reports from Equifax, Experian, and TransUnion to monitor payment history and identify potential reporting errors.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.