Sole Proprietor vs LLC: Which Is Best for a Side Hustle?

When you start earning money outside of a traditional 9-to-5 job, the feeling is incredibly rewarding. Whether you are driving for a rideshare app, selling handmade crafts online, or taking on freelance graphic design clients, that extra income represents your financial independence.

However, as your side hustle grows from a weekend hobby into a consistent revenue stream, a critical question usually pops up: Do I need to make this official? When you first begin making money on your own, the government automatically views you as a “sole proprietor.” In fact, according to the U.S. Small Business Administration, sole proprietorships remain the most common business structure in the United States.

But as your income and client base expand, you will inevitably hear advice from peers or online forums telling you to form an LLC (Limited Liability Company) to protect yourself.

Choosing the right business structure is a foundational decision. It dictates how much you pay in taxes, what kind of paperwork you have to manage, and how much of your personal money is at risk if something goes wrong.

Quick Answer

- Most new side hustlers start as sole proprietors. It is free, automatic, and requires no state paperwork.

- LLCs provide personal liability protection. This shields your personal savings and property if your business gets sued.

- Taxes are usually the exact same initially. A standard LLC does not automatically lower your tax bill.

- LLCs become much more attractive as your income and legal risks increase.

- You are not locked in. Many successful entrepreneurs start as sole proprietors to test their idea and upgrade to an LLC later.

At a Glance: Sole Proprietor vs LLC

If you want the high-level differences before getting into the details, here is how the two structures compare:

| Feature | Sole Proprietor | LLC (Limited Liability Company) |

| Startup Cost | Very Low (often $0) | Moderate ($50 to $500+ depending on state) |

| State Filing Required? | No | Yes |

| Liability Protection | No | Yes |

| Tax Treatment | Pass-through | Pass-through by default |

| S-Corp Option | No | Yes |

| Credibility | Moderate | Higher |

| Annual Maintenance | Minimal | State requirements |

What Is a Sole Proprietorship?

A sole proprietorship is the simplest business structure in the US. If you are doing business by yourself and haven’t filed any formal legal paperwork to create a company, congratulations—you are already a sole proprietor.

How It Works

The defining characteristic of a sole proprietorship is that there is absolutely no legal separation between you and your business. The law views you and your side hustle as the exact same entity. All the money the business makes belongs directly to you, and all the debts or liabilities the business incurs belong directly to you.

You do not need to register with your state to become a sole proprietor. You just start selling your product or service. (Note: Depending on your industry and city, you might still need a basic local business license or permit, but you don’t need to form a corporate entity).

Pros of a Sole Proprietorship

- Zero Startup Costs: You don’t have to pay state filing fees to create the entity.

- No Administrative Upkeep: There are no annual reports to file with the state and no requirement to hold formal business meetings.

- Simple Taxes: Because you and the business are the same, you simply report your business income and expenses on a Schedule C form attached to your standard personal tax return (Form 1040).

Cons of a Sole Proprietorship

- No Liability Protection: This is the massive trade-off. If your business gets sued or falls into debt, your personal assets—like your home, your car, and your personal savings—are completely exposed and can be seized to cover the business’s obligations.

- Perception: Some larger corporate clients or vendors prefer to do business with an established company rather than an individual, which might limit your growth opportunities.

What Is an LLC (Limited Liability Company)?

An LLC is a formal legal structure created at the state level. It is designed to offer the personal liability protections of a large corporation while keeping the tax simplicity of a sole proprietorship.

How It Works

Unlike a sole proprietorship, an LLC establishes a legal wall between you (the owner, or “member”) and the business itself. The LLC is its own “person” in the eyes of the law. It can open its own bank accounts, sign its own contracts, and take on its own debt.

To form an LLC, you must file “Articles of Organization” with your state’s Secretary of State office and pay a filing fee, which usually ranges from $50 to $500 depending on where you live.

Pros of an LLC

- Personal Asset Protection: If your LLC is sued or goes bankrupt, creditors can generally only go after the assets owned by the LLC. Your personal savings, your home, and your personal investments are shielded from business liabilities.

- Tax Flexibility: By default, a single-member LLC is taxed exactly like a sole proprietorship. However, as your profits grow, an LLC gives you the option to elect S-Corporation tax status, which can potentially save you thousands of dollars in self-employment taxes.

- Professional Credibility: Adding “LLC” to the end of your business name builds immediate trust with clients, lenders, and suppliers.

Cons of an LLC

- Upfront and Ongoing Costs: You have to pay to form the LLC, and most states require an annual fee or franchise tax to keep it active. For example, California LLCs must pay a minimum $800 franchise tax every year, regardless of how much money they make.

- Administrative Rules: You must maintain a strict separation between your personal and business finances. If you treat your LLC bank account like a personal piggy bank (a mistake called “piercing the corporate veil”), a judge can strip away your liability protection.

Real-World Scenarios: Sarah vs. Mike

Sometimes the easiest way to understand business structures is to see them in action. Let’s look at two different side hustlers.

Sarah the Freelance Designer

- Makes $12,000/year

- Works from home

- No employees

- Low liability risk

- The Verdict: A sole proprietorship is likely perfectly sufficient. The cost of forming and maintaining an LLC would eat unnecessarily into her profits without providing much-needed benefit, since her liability risk is so low.

Mike the Mobile Auto Detailer

- Makes $60,000/year

- Works on customer property

- Uses heavy equipment and chemicals

- Higher liability exposure

- The Verdict: An LLC becomes much more compelling. If he damages a vehicle and gets sued, his LLC protects his personal bank accounts. Furthermore, because he makes $60,000 in profit, he can look into electing S-Corp status to lower his tax burden.

Do You Need an LLC for Etsy, Uber, DoorDash, Fiverr, or Freelancing?

This is one of the most common questions beginners ask. If you are signing up for a major gig economy platform, do you need to form a company first?

The short answer is no. Platforms like Uber, DoorDash, Etsy, Upwork, and Fiverr do not require you to have an LLC to use their services. When you sign up, you provide your Social Security Number, and they pay you as an independent contractor (a sole proprietor).

However, whether you should form one depends on what you are actually doing:

- Do I need an LLC for Etsy? If you sell digital printables or basic crafts, a sole proprietorship is fine. But if you manufacture physical products that people ingest or put on their skin (like homemade candles, soaps, or baked goods), an LLC is highly recommended to protect yourself from product liability lawsuits.

- Do I need an LLC for Uber or DoorDash? Most drivers operate as sole proprietors. Your biggest concern here is insurance. You must ensure you have the proper rideshare endorsement on your personal auto insurance policy.

- Do I need an LLC for freelancing? Writers, editors, and digital artists usually start as sole proprietors and only upgrade to an LLC when their income reaches a level where S-Corp taxation makes sense, or when they want to hire subcontractors.

The Big Differences: Liability, Taxes, and Costs

To make the right choice, you need to understand how these two structures handle the most critical aspects of running a side hustle.

1. Personal Asset Protection (Liability)

If you are a freelance writer working from your laptop, your risk of being sued for massive damages is relatively low. But what if you are a wedding photographer who accidentally trips over a power cord, destroying the venue’s expensive audio equipment and injuring a guest?

As a sole proprietor, you are personally on the hook for those damages. As an LLC, assuming you have kept your business operations cleanly separated from your personal life, only the assets inside the LLC are at risk.

LLC Does NOT Replace Insurance

A common misconception among beginners is that forming an LLC means you are fully protected from all risks. This is not true. An LLC is not a substitute for business insurance. Many business owners need both. While an LLC builds a wall to protect your personal savings from business debts, it does not actually pay for the damages if your business gets sued. A general liability insurance policy is still necessary to cover legal fees and settlements.

2. How They Are Taxed

Many side hustlers assume forming an LLC automatically lowers taxes. In reality, most single-member LLCs are taxed exactly the same as sole proprietorships unless additional elections are made.

By default, the IRS treats a single-member LLC as a “disregarded entity.” This means:

- Both are “pass-through” entities. The business itself doesn’t pay taxes. The profits pass through the business and are reported directly on your personal tax return.

- In both structures, you will owe a 15.3% self-employment tax (which covers Medicare and Social Security) on your net profits, plus your standard federal and state income taxes.

The LLC Tax Advantage: The major difference arises when your side hustle starts generating serious profit (usually around the $40,000 to $60,000 net profit mark). At that point, an LLC can file paperwork with the IRS to be taxed as an S-Corporation. This allows you to pay yourself a “reasonable salary” subject to self-employment tax, and take the remaining profit as a distribution, which is completely free from self-employment tax. A sole proprietor cannot do this.

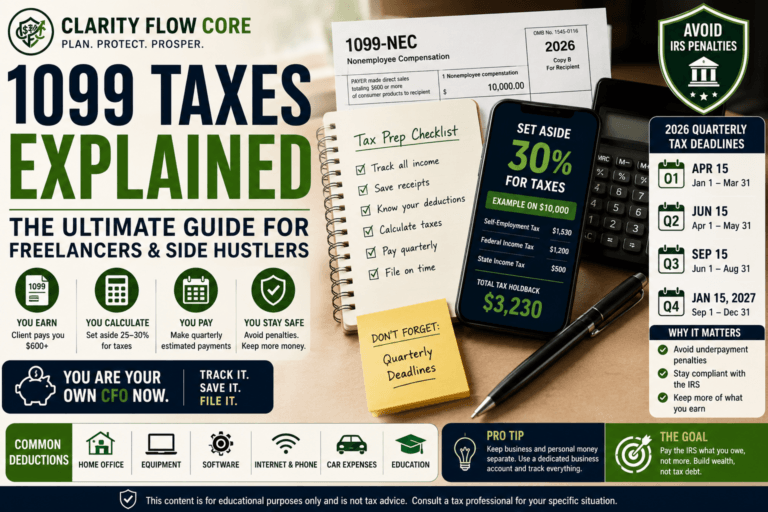

Tax Resources for Freelancers: > Want to make sure you aren’t overpaying the IRS? Check out our guides on 1099 Taxes Explained for Freelancers and Side Hustlers and Freelancer Tax Deductions: Common Expenses You May Be Able to Claim.

3. Administration and Upkeep

A sole proprietorship is completely hands-off. You track your income, you track your expenses, you file your taxes in April, and you are done.

An LLC requires maintenance. You need an Employer Identification Number (EIN) from the IRS. You must file an annual report with your state. You need a dedicated registered agent (an official address to receive legal mail). You also need to keep impeccable records to prove to the government that the LLC is functioning as a standalone entity.

Common Mistakes Side Hustlers Make

Before you rush to your state’s website to form an entity, avoid these common traps:

- Commingling Funds: The fastest way to destroy the legal protection of an LLC is to use your business debit card to buy personal groceries or pay your personal rent. If you form an LLC, you must open a dedicated business checking account and use it strictly for business.

- Ignoring State Minimum Fees: Some states have aggressively high fees for LLCs. Do your research. If your side hustle only makes $2,000 a year, but your state charges a $500 annual LLC fee, you are wiping out a massive chunk of your profit just for paperwork.

- Failing to Budget for Irregular Income: Managing business income can distort how you view your personal wealth. Irregular income requires careful planning. We recommend reading our guide on the Best Beginner Budgeting Method for Irregular Income or learning How to Budget as a Freelancer When Income Changes Every Month.

Your Action Plan: Which Should You Choose?

There is no one-size-fits-all answer, but here is a highly practical framework to help you decide.

When to Stay a Sole Proprietor

You should likely remain a sole proprietor if:

- You are just starting out: If you are testing a new business idea and aren’t sure if it will be profitable, don’t waste money on legal fees. Prove the concept first.

- Your liability risk is very low: If you are a virtual assistant, a freelance copywriter, or an online tutor, the odds of a devastating lawsuit are slim.

- Your income is small: If your side hustle brings in a few hundred dollars a month, the cost of maintaining an LLC likely outweighs the benefits.

When to Upgrade to an LLC

You should strongly consider forming an LLC if:

- Your risk of liability is high: If you work with heavy equipment, serve food, manufacture physical products, or have people visiting a physical location you rent, you need the legal protection an LLC provides.

- You want to hire employees: While sole proprietors can technically hire employees, it is much safer to do so under the umbrella of an LLC to protect yourself from employment-related liabilities.

- Your profits are growing rapidly: If your side hustle net profit is approaching $50,000, an LLC gives you the ability to elect S-Corp status and strategically lower your self-employment tax burden.

- You are landing corporate clients: Larger companies often refuse to cut checks to individuals and require a W-9 with a registered LLC name and EIN.

Next Steps for Today

- Assess Your Risk: Write down everything that could reasonably go wrong in your daily operations. If the worst happened, could you financially survive a lawsuit? If not, lean toward an LLC.

- Check Your State Fees: Go to your state’s Secretary of State website and look up the filing fee and the annual renewal fee for an LLC. Make sure your current cash flow can easily cover it.

- Open a Business Bank Account: Regardless of whether you choose a sole proprietorship or an LLC, open a separate checking account today. Keep all your side hustle income and expenses completely isolated from your personal money.

- Protect Your Personal Baseline: A fluctuating side hustle income requires a solid safety net. Run your numbers through our Advanced Emergency Fund Analyzer to ensure your personal finances are secure while you build your business. If you are ready to map out your long-term goals, use the Financial Freedom Planner to see how your side hustle income impacts your future.

Frequently Asked Questions (FAQ)

1. Can I switch from a sole proprietor to an LLC later?

Yes. In fact, this is the most common path. Many entrepreneurs start as sole proprietors to test their business idea and then form an LLC once they have consistent revenue and proven product-market fit.

2. Do I need an EIN for my side hustle?

If you are a sole proprietor with no employees, you can use your Social Security Number for tax forms. However, getting an Employer Identification Number (EIN) from the IRS is free and highly recommended, as it prevents you from having to hand out your Social Security Number to clients. If you form an LLC, you will almost certainly need an EIN to open a business bank account.

3. Does having an LLC give me a tax break?

Not by default. A standard single-member LLC is taxed exactly like a sole proprietorship. The tax break only comes if your LLC generates enough profit to justify electing S-Corporation tax status.

4. How much does it cost to start an LLC?

It varies widely by state. Forming an LLC in Kentucky might cost $40, while forming one in Massachusetts costs $500. Additionally, many states require an annual report fee to keep the LLC active, which can range from $10 to $800 annually.

5. What happens if I get sued as a sole proprietor?

Because there is no legal separation between you and your business, a lawsuit against your side hustle is a lawsuit against you. If a court rules against you, creditors can pursue your personal assets, including your bank accounts and property, to settle the debt.

6. Will the new Corporate Transparency Act (CTA) affect my LLC?

As of recent 2025 and 2026 FinCEN guidance, most U.S.-formed companies are currently exempt from the CTA’s Beneficial Ownership Information (BOI) reporting requirements under an interim final rule. While the rules heavily target foreign entities and shell companies right now, U.S. business owners should still monitor FinCEN updates. Sole proprietorships are generally unaffected since they are not registered entities.

7. Can I have a business name as a sole proprietor?

Yes. You can file a “Doing Business As” (DBA) or Fictitious Business Name with your county or state. This allows you to operate under a name like “Sunrise Web Design” instead of your legal personal name, even without an LLC.

Conclusion

Deciding between a sole proprietorship and an LLC does not have to be a stressful hurdle. Think of it as a natural progression of your business journey. If you are just starting to explore a side hustle and want to keep costs and paperwork to an absolute minimum, a sole proprietorship is a perfectly acceptable way to begin.

However, as your revenue grows, your client list expands, and your operations become more complex, the legal protection and professional credibility of an LLC become invaluable. The goal of any side hustle is to improve your financial life, not jeopardize it. By understanding the risks, analyzing your state’s costs, and keeping your business funds strictly separated, you can confidently build a profitable business that serves your long-term goals.

References & Trusted Resources

The following official government resources provide additional guidance on business structures, taxation, and compliance requirements for side hustlers and small business owners.

- Internal Revenue Service (IRS): Sole Proprietorships

- Internal Revenue Service (IRS): Limited Liability Company (LLC)

- U.S. Small Business Administration (SBA)

- Financial Crimes Enforcement Network (FinCEN): BOI Reporting Guidance

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.