20 Expenses You Can Cut Without Feeling Deprived

When you hear the phrase “cut expenses,” what comes to mind? For most people, it triggers instant dread. You picture yourself sitting in a freezing house, eating plain noodles, and saying no to every social invitation for the next five years.

This extreme approach to budgeting is why most people give up after three weeks.

The truth is, saving money does not require misery. If you look closely at your bank statements and apply fundamentals like The 50/30/20 Budget Rule Explained Simply, you will likely see you are bleeding cash on things that add absolutely zero value to your life. You are paying for subscriptions you forgot about, overpaying for basic services, and falling for marketing traps that keep your wallet empty.

You can free up hundreds of dollars a month without drastically changing your lifestyle. You just need to know where to look. In this guide, we will walk through 20 specific, painless expenses you can eliminate right now to keep more money in your pocket—without feeling restricted or deprived.

⚡ Quick Answer

Cut expenses without feeling deprived means eliminating “invisible” spending—like forgotten subscriptions, hidden bank fees, brand-name markups, and energy waste. By auditing your statements and optimizing basic bills, you can redirect hundreds of dollars a month toward your financial goals without sacrificing the things you actually enjoy.

To give you an idea of the immediate impact, here is a quick look at how just five simple cuts can drastically improve your monthly cash flow:

| Expense Cut | Strategy | Potential Monthly Savings |

| Cable TV | Switch to 1-2 targeted streaming apps | $80 – $120 |

| Cell Phone Plan | Switch to an MVNO (like Mint or Visible) | $40 – $60 |

| Gym Membership | Cancel unused plan, workout at home | $30 – $75 |

| Name-Brand Groceries | Swap to store-brand staples | $40 – $80 |

| Bank Fees | Switch to a fee-free online bank | $10 – $25 |

| Total Potential Savings | $200 – $360 per month |

The 80/20 Rule: Biggest Wins First

Before we dive into the list of 20 expenses, we need to talk about prioritization. Many people obsess over saving $3 on a box of cereal while completely ignoring the fact that they are overpaying by $300 on their car loan.

This is where the 80/20 rule of personal finance comes in. Focus on your biggest expenses first. If you can optimize your “Big Four,” you will have massive amounts of breathing room in your budget:

- Housing: Can you appeal your property taxes, rent out a room, or refinance your mortgage? (If you’re unsure of baseline targets, read How Much of Your Income Should Go Toward Housing Costs?).

- Transportation: Do you have an expensive car payment you can eliminate by downsizing to a reliable used vehicle? (If you are debating your options, you must read our deep dive on Leasing vs. Buying Used Cars: Which Actually Costs Less? to see the exact math on how much wealth traditional auto financing destroys).

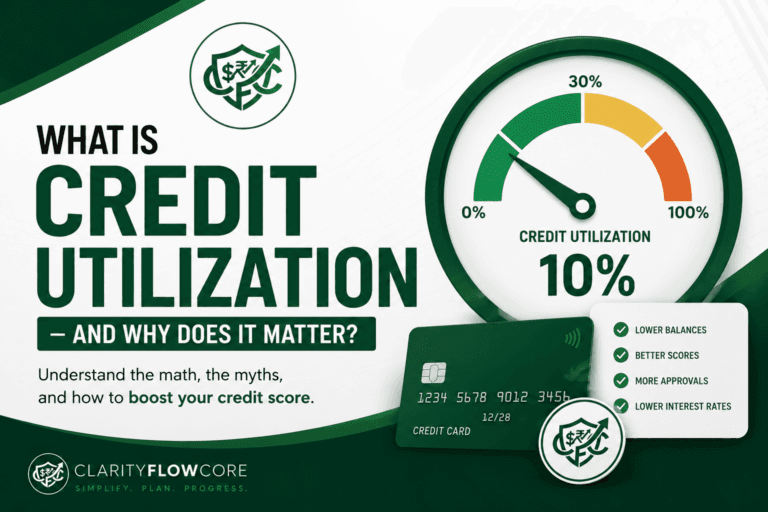

- Debt: Are you losing hundreds of dollars to interest? Using our Debt-to-Income Analyzer & Loan Readiness Planner can help you assess your total debt burden, while our Credit Utilization Calculator & Recovery System is essential for building a strategy to eliminate expensive revolving debt.

- Insurance: Have you shopped around for new home and auto policies this year? You can learn exactly how to do this safely in Practical Ways to Lower Insurance Costs Without Cutting Coverage.

Fix the big rocks first. Once those are secure, optimizing your subscriptions and grocery bills becomes the icing on the cake.

The Math of Cutting Back

Why bother tracking down $15 or $20 leaks in your budget? Because the math adds up incredibly fast over time.

If you go through the list below and manage to cut just $250 per month out of your budget, you free up:

- $3,000 per year

- $15,000 over five years

And that is before any investment growth. Redirecting that $250 a month into an index fund or using it to wipe out debt changes your entire financial trajectory. Now, let’s find that money.

Category 1: Subscriptions and Digital Services

Digital subscriptions are the silent killers of a modern budget. Companies love them because they know you will sign up, forget, and let them auto-renew for years.

1. The “Ghost” Subscriptions

Pull up your last 30 days of bank and credit card statements. Look for anything that charges you under $10 a month. A premium meditation app you opened twice? A language learning tool you abandoned in January? Cancel them immediately.

2. Overlapping Streaming Services

You do not need Netflix, Hulu, Max, Disney+, Peacock, and Paramount+ all at the same time. You literally cannot watch that much television. Pick one or two services to keep active. When a new show comes out on another platform, pause your current subscription and rotate.

3. Premium Music Subscriptions (If You Only Listen Casually)

If you are an audiophile, keep your Spotify Premium. But if you only listen to music for 20 minutes during your commute, the free ad-supported versions of Spotify or Pandora work perfectly fine. That is $120 to $180 saved per year.

4. Extended Warranties on Electronics

When you buy a $400 television, the cashier will relentlessly push a $60 extended warranty. Decline it. Most modern electronics last well past the extended warranty period, and many credit cards actually offer free extended warranty protection just for using their card to make the purchase.

Category 2: Food and Dining

You have to eat, but you do not have to overpay for the privilege. Adjusting your food habits slightly yields the fastest budget results.

5. Delivery App Markups

Using UberEats or DoorDash is a financial disaster. Not only are you paying a delivery fee and a tip, but the restaurants also mark up the menu prices on the app by 15% to 30%. If you want takeout, call the restaurant directly and go pick it up. You still get the food, but you save $15 to $20 per meal.

6. Name-Brand Grocery Staples

Buying brand-name cereal or snacks is fine if you truly prefer the taste. But for basic ingredients—flour, sugar, canned beans, salt, ibuprofen, and frozen vegetables—the store brand is often made in the exact same factory as the premium brand. Making this switch can lower your grocery bill by 10% instantly.

7. The Daily Coffee Run

If you spend $6 a day on coffee, that is $180 a month. You do not have to quit coffee; just buy a decent travel mug and brew it at home. Treat yourself to a cafe trip once a week instead of every single morning.

8. Pre-Cut Fruits and Vegetables

A whole pineapple costs $3. A plastic container of pre-cut pineapple costs $7. You are paying a 133% markup for someone to use a knife for two minutes. Buy whole produce and take ten minutes on Sunday to prep it yourself.

Category 3: Household and Utilities

Your house is full of invisible expenses. A few one-time changes can lower your monthly bills permanently.

9. Big-Name Cell Phone Providers

If you are paying $80 to $100 a month to AT&T, Verizon, or T-Mobile for a single line, you are overpaying. Look into Mobile Virtual Network Operators (MVNOs) like Mint Mobile, Visible, or Google Fi. They use the exact same cell towers as the big providers, but plans often cost between $15 and $30 a month.

10. Cable Television

The average cable bill in the US is over $100 a month. If you are only keeping it for live sports or local news, you can buy an HD digital antenna for $20 to get local channels for free forever, or subscribe to a much cheaper live-streaming alternative.

11. Phantom Electricity

Electronics draw power even when they are turned off. This is called “vampire” or “phantom” energy. Unplugging your toaster, coffee maker, guest room television, and phone chargers when not in use can lower your electric bill by 5% to 10% a month.

12. High-End Cleaning Products

You do not need a specialized, brightly colored chemical spray for every surface in your house. White vinegar, baking soda, and a little dish soap can clean 95% of your home for pennies on the dollar compared to expensive commercial cleaners.

Category 4: Insurance and Financial Fees

Many people set up their banking and insurance once and never look at it again. This loyalty costs you dearly.

13. Monthly Bank Maintenance Fees

If your bank charges you $12 a month just for having a checking account, close the account immediately. There are dozens of reputable, FDIC-insured online banks that offer completely free checking. Consider comparing your options in our High-Yield Savings Account vs Traditional Savings Account guide to ensure you are maximizing your interest while minimizing your fees.

14. ATM Fees

Paying $3.50 to access your own money is completely unnecessary. If your bank does not reimburse out-of-network ATM fees, either plan ahead and get cash back at the grocery store checkout or switch to a bank that offers universal ATM fee reimbursements.

15. Credit Card Annual Fees (If You Don’t Use the Perks)

Travel credit cards with $95 or $250 annual fees are only worth it if you actively use the airport lounges and travel credits. If that card is just sitting in your wallet, downgrade it to a no-annual-fee version. Need help managing your credit lines? Use our Credit Score Simulator & Improvement Planner to see how downgrading might impact your active credit age and score.

16. “Loyalty” Auto Insurance Rates

Auto insurance companies commonly use a practice called “price optimization,” which means they slowly raise your rates over time simply because they assume you are too lazy to shop around. Spend an hour getting quotes from three different providers; you can often save $200 to $400 a year just by switching.

Category 5: Lifestyle and Shopping

Finally, let’s look at the discretionary spending that slips through the cracks.

17. The Unused Gym Membership

Gyms build their entire business model on people who sign up in January and stop going in March. If you have not been to your gym in the last 45 days, cancel the membership. You can always work out at home, run outside, or sign up again later if you actually commit.

18. Fast Fashion Upgrades

Buying a $15 shirt that falls apart after three washes is more expensive in the long run than buying a $40 shirt that lasts for years. Stop buying cheap, trendy clothing just for the sake of having something new.

19. App In-Game Purchases

Spending $1.99 for extra lives in a mobile game or buying virtual currency seems harmless, but it is engineered to be addictive. Remove your credit card information from your phone’s app store to create friction before you make these impulse buys.

20. Professional Car Washes

Paying $20 to run your car through a premium wash every two weeks adds up to $520 a year. Buy a bucket, some car soap, and a sponge. Washing your car in your driveway is easy and costs almost nothing.

When Expense Cutting Goes Too Far

There is a fine line between being frugal and being cheap. While cutting expenses is a necessary step to building wealth, cutting the wrong things will actually cost you much more in the long run. Watch out for these pitfalls:

- Canceling Insurance Coverage: Dropping your health insurance, renters insurance, or lowering your auto insurance liability limits to the state minimum to save $40 a month is a terrible gamble. One accident or emergency will wipe out a decade of savings.

- Ignoring Maintenance: Skipping a $60 oil change will eventually destroy a $5,000 engine. Delaying a roof repair will lead to structural water damage. Maintenance is not an expense you can cut; it is an investment in protecting your assets.

- Buying Cheap Products Repeatedly: Buying a $10 pair of shoes that lasts two months is far more expensive than buying a $60 pair that lasts three years. Focus on value, not just the lowest price tag.

- Eliminating All Entertainment: If you cut out every dinner with friends, every movie night, and every hobby, you will burn out. Budgeting is about sustainability. Allocate a reasonable amount of money for joy.

Summary of Potential Savings

When you add it all up, the results are staggering. By attacking these five categories, here is a conservative look at what an average household can save over a year:

| Category | Potential Annual Savings |

| Subscriptions | $300 – $800 |

| Food | $500 – $2,000 |

| Utilities | $200 – $800 |

| Insurance | $200 – $600 |

| Lifestyle | $300 – $1,500 |

Action Plan: Audit Your Expenses Today

Reading a list of 20 items is helpful, but taking action is what changes your bank account. Follow these steps today.

- Print Your Statements: Print out the last two months of checking account and credit card statements. Physical paper works best.

- Grab a Highlighter: Go line by line. Highlight any expense that is a subscription, a recurring fee, or a purchase you regret making.

- Make the Phone Calls: Pick three things to cancel immediately. It might require sitting on hold for ten minutes, but it is worth the effort. (Note: If you’re cutting expenses because you’ve recently lost your income, I Lost My Job: A 30-Day Financial Survival Plan provides a step-by-step strategy for prioritizing bills, preserving cash, and navigating the first month of unemployment).

- Negotiate One Bill: Call your internet provider or cell phone company. Ask them if they have any current promotions or if they can lower your rate to match a competitor.

- Track Your Progress: Log into your Financial Freedom Planner and adjust your monthly spending targets down based on the cuts you just made.

Next Steps

Once you have stopped the financial bleeding and freed up your cash flow, what should you do with the extra money? Your next priorities should be:

- Building a Full Emergency Fund: Redirect the saved money until you have 3 to 6 months of living expenses saved. Unsure how much that is? Use the Advanced Emergency Fund Analyzer.

- Eliminating High-Interest Debt: Attack any lingering balances with your newly found cash flow using the mathematical logic found in our Debt Avalanche vs Debt Snowball guide.

- Automating Your Savings: Put your money to work before you have a chance to spend it. Learn How to Automate Savings Using Split Direct Deposit.

- Increasing Your Savings Rate: Build wealth by directing those cut expenses directly into your investment accounts.

Frequently Asked Questions

How do I track all my subscriptions easily?

The most foolproof method is to look at your bank statements. Alternatively, your smartphone’s app store (Apple ID or Google Play) has a specific “Subscriptions” menu where you can view and cancel anything billed through your phone.

Will canceling my credit card to avoid an annual fee hurt my credit score?

Yes, it can. Closing a credit card reduces your total available credit, which increases your credit utilization ratio. It also lowers your average age of accounts. Instead of closing the card, call the issuer and ask to “downgrade” to a free version of the card. This keeps the account open and protects your score.

Is it really worth the effort to save $5 a month on a small subscription?

Absolutely. Five dollars a month is $60 a year. If you find five small things to cut, that is $300 a year. More importantly, it trains your brain to stop accepting recurring charges as inevitable.

How do I say no to friends when they want to do expensive activities?

Be honest but offer alternatives. Instead of saying, “I’m broke,” say, “I’m working on some major financial goals right now. Let’s do a potluck dinner at my place instead of going out to that expensive steakhouse.” True friends will respect your boundaries.

I negotiated my bill down, but it went back up after a year. Why?

Most promotional rates expire after 12 months. Put a reminder in your calendar for 11 months from now. When it goes off, call the company again and ask them to reapply the promotional rate, or simply threaten to switch to a competitor.

References and Resources

To ensure you have the most accurate and up-to-date consumer protection information regarding hidden fees and subscription cancellations, we recommend exploring these official resources:

- Federal Trade Commission (FTC): Provides excellent guidelines on your rights regarding auto-renewing subscriptions and how to stop unauthorized charges. Read the official FTC guide here.

- Consumer Financial Protection Bureau (CFPB): Offers practical tools and worksheets to help you track your spending and find hidden leaks in your budget. Visit the CFPB spending tracker.

- Consumer.gov: Managed by the FTC, this site offers straightforward, plain-language advice on managing your money and making a realistic budget. Explore Consumer.gov budgeting basics.

- Federal Deposit Insurance Corporation (FDIC): If you are switching banks to avoid monthly fees, always ensure your new institution is federally insured. Check bank insurance status via the FDIC.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial, legal, or tax advice. Every individual’s financial situation is unique. Always consult with a qualified financial professional before making major decisions.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.