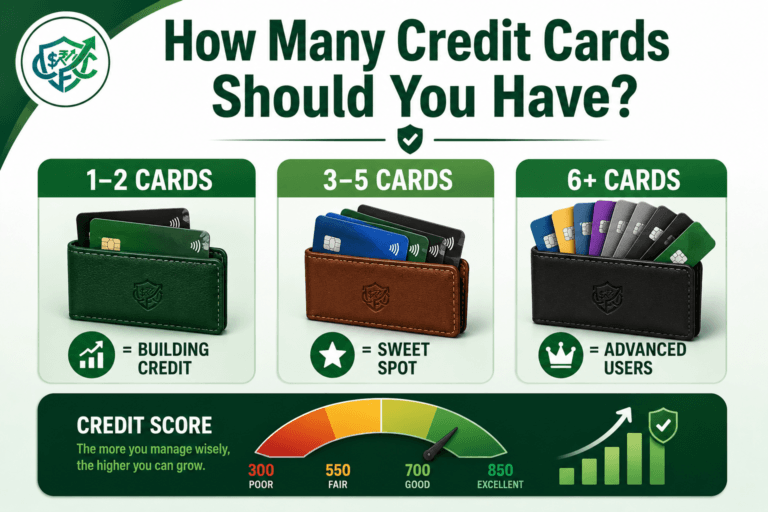

What Credit Score Is Needed for Each Type of Credit Card?

You spend hours researching the perfect cash-back card. You read the reviews, calculate the potential rewards, and finally click the “Apply Now” button. The screen loads for a few agonizing seconds, and then the message appears: Declined.

Getting rejected for a credit card is a frustrating and entirely common experience. It usually happens because there is a massive disconnect between the card you want and the credit score the bank requires. Credit card companies do not explicitly publish the exact minimum scores needed for their products, leaving consumers guessing and risking unnecessary “hard inquiries” on their credit reports.

You do not have to guess. Banks operate on highly predictable risk models. If you understand how they categorize their cards, you can apply with confidence, knowing exactly which products match your current financial profile.

In this guide, we will break down exactly what credit score is needed for credit card, explain the hidden factors lenders look at beyond your score, and show you how to guarantee you are applying for the right card at the right time.

⚡ Quick Answer

A credit score of 670 or higher (Good to Excellent) is generally needed to qualify for standard cash-back and travel rewards cards. Premium luxury cards typically require a score of 740 or above. If your score is below 600, or you have no credit history at all, you will need to start with a secured credit card or a student card to build your foundation.

To help you skip the guesswork, here is a quick breakdown of the exact FICO score ranges and approval odds for the most common credit card tiers:

| Card Type | Required FICO Score Range | Approval Odds | Typical Credit Limit | Best For |

| Secured Cards | 300 – 579 (Or No Credit) | Very High | $200 – $500 (Matches Deposit) | Complete beginners or rebuilding after bankruptcy. |

| Student Cards | No Credit – 669 | High | $500 – $1,000 | College students building first-time credit. |

| Retail/Store Cards | 580 – 669 (Fair) | Moderate | $300 – $1,000 | Rebuilding credit with frequent shopping at one brand. |

| Standard Cash Back | 670 – 739 (Good) | Good | $2,000 – $10,000+ | Everyday spenders wanting 1% to 5% cash back. |

| Premium Travel | 740 – 850 (Excellent) | Strong (If income supports) | $10,000 – No Preset Limit | Frequent flyers utilizing airport lounges and travel credits. |

Understanding the Exact Credit Score is Needed for Credit Card Approval

Before you can match your profile to a credit card, you must understand the scale banks are actually using. While there are many different credit scoring models (like VantageScore, which you often see on free banking apps), 90% of top lenders use your FICO Score to make credit decisions.

The FICO scale ranges from 300 to 850. Here is how banks view you based on your number:

- 300 – 579 (Poor): You are considered a high risk. You will likely be denied standard credit and must rely on secured products.

- 580 – 669 (Fair): You are a moderate risk. You might qualify for high-interest retail cards or starter unsecured cards with low limits.

- 670 – 739 (Good): You are a low risk. This is the national average, and it opens the door to the vast majority of mainstream cash-back cards.

- 740 – 799 (Very Good): You are a highly dependable borrower. You will qualify for the best interest rates and premium cards.

- 800 – 850 (Exceptional): You have a flawless history. You are virtually guaranteed approval for any consumer credit product on the market.

What If You Have No Credit Score?

If you are entirely new to the US financial system, you might have a “ghost” profile. FICO requires at least six months of payment history to generate a score. If you are starting from absolute zero, applying for standard cash-back cards will trigger automatic rejections.

Here is your immediate action plan to build a score from scratch:

- Open a secured credit card: This is the absolute fastest way to establish a baseline score with nearly guaranteed approval.

- Become an authorized user: Ask a parent or trusted family member with an impeccable payment history to add you to their oldest credit card. Their good history will populate on your report.

- Report your rent and utility payments: Use third-party services that report your ongoing monthly apartment and utility bills to the major credit bureaus.

- Build six months of history: Be patient. After six months of active, responsible credit behavior, your first real FICO score will successfully generate.

Category 1: Secured Credit Cards

FICO Score Needed: 300 – 579 (Or No Credit History)

If you have entirely ruined your credit through past mistakes, or if you are a 19-year-old who has never borrowed a dime, traditional banks view you as a massive risk. A secured credit card bypasses this risk entirely.

How They Work

To open a secured card, you must provide a refundable cash security deposit—usually between $200 and $500. The bank holds this cash in a vault, and that deposit becomes your exact credit limit. Because the bank can simply take your deposit if you fail to pay your bill, their financial risk is zero.

Why You Need One

Secured cards report your monthly payments to all three major credit bureaus (Experian, Equifax, and TransUnion). By putting a small $10 subscription on the card and paying it off completely every month, you systematically build a positive payment history. Within six to twelve months, you can easily graduate from the “Poor” category into the “Fair” or “Good” category.

For a deeper dive into the exact cards we recommend for this stage, read our complete guide on the Best Secured Credit Cards for Beginners in 2026.

Category 2: Student Credit Cards

FICO Score Needed: No Credit History – 669 (Fair)

Banks desperately want to acquire young, educated customers before they enter their peak earning years. Because of this, they are incredibly lenient when approving college students for their first unsecured credit cards.

How They Work

Student credit cards function exactly like standard credit cards, but they do not require a cash security deposit. The catch is that they typically offer very low initial credit limits (often around $500). To qualify, you generally must provide proof of enrollment at a two-year or four-year university.

The Catch on Income

The CARD Act of 2009 strictly regulates how banks issue credit to anyone under 21. If you are under 21, you must prove you have independent income (like a part-time campus job or paid internship) to qualify. If you do not have independent income, you will need a cosigner, which most major banks no longer allow for student cards.

Category 3: Retail and Store Credit Cards

FICO Score Needed: 580 – 669 (Fair)

When you are checking out at your favorite clothing store or big-box retailer, the cashier will inevitably ask, “Would you like to save 20% today by opening a store credit card?”

How They Work

Store cards (often called “closed-loop” cards because they can only be used at that specific retailer) have notoriously low barriers to entry. Because the retailer wants you to spend more money exclusively at their stores, they will often approve applicants with fair or even borderline poor credit scores.

The Massive Danger

While retail cards are easy to get, they are incredibly dangerous for beginners. They typically feature astronomical Annual Percentage Rates (APRs), often exceeding 30%. Furthermore, they come with very low credit limits. If a store gives you a $300 limit, and you spend $250 on a new jacket, your credit utilization instantly spikes to 83%.

High credit utilization will tank your FICO score overnight. If you struggle with balancing limits across multiple retail cards, run your numbers through our Credit Utilization Calculator & Recovery System to build an aggressive payoff and optimization plan.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationCategory 4: Standard Cash-Back and Rewards Cards

FICO Score Needed: 670 – 739 (Good)

This is the sweet spot of the credit card industry. Once your score crosses the 670 threshold, you unlock the ability to earn actual money on your everyday spending without paying exorbitant annual fees.

How They Work

Standard cash-back cards typically offer anywhere from 1% to 5% cash back on specific categories like groceries, gas, and dining. They usually do not charge an annual fee, and they come with reasonable credit limits ($2,000 to $10,000+).

What You Need to Know

At this level, your credit score is not the only thing that matters. Even if you have a 710 FICO score, banks will look closely at your income and your existing debt burden. If you are preparing to apply for a major cash-back card, ensure your monthly obligations are balanced by using our Debt-to-Income Analyzer & Loan Readiness Planner.

Category 5: Premium Travel and Luxury Cards

FICO Score Needed: 740 – 850 (Excellent)

If you want access to airport lounges, massive sign-up bonuses, free hotel upgrades, and hundreds of dollars in annual travel credits, you are looking for a premium travel card.

How They Work

Premium cards require impeccable credit. They also come with steep annual fees, ranging from $395 to $695. In exchange, they offer luxury travel perks and flexible points that can be transferred to airline and hotel partners.

The Hidden Rules

Getting approved for these cards requires more than just a 750 credit score. Premium lenders look for a long, established credit history (usually at least 3 years of clean history) and significant income.

If you are torn between chasing travel points or sticking to simple cash rewards, read our breakdown: Cash Back vs Travel Credit Cards: Which Should You Choose?

The “Hidden” Factors That Cause Rejections

Your FICO score is the primary filter, but it is not the only metric banks use. You can easily get denied with an 800 credit score if you fail these secondary checks.

1. Your Debt-to-Income Ratio (DTI)

Banks want to know you can afford to pay them back. If you earn $4,000 a month, but you spend $3,000 a month paying off student loans, auto loans, and an expensive apartment, the bank views you as overextended. Even with a perfect credit history, they will deny you because your cash flow is too tight.

2. The 5/24 Rule (and Recent Inquiries)

When you apply for a credit card, the bank performs a “hard inquiry” on your credit report. This temporarily drops your score. If a bank sees that you have applied for six different credit cards in the last three months, they assume you are desperate for cash and will deny you.

Chase Bank famously enforces the unofficial “5/24 Rule.” If you have opened 5 or more personal credit cards (from any bank) in the last 24 months, Chase will automatically deny your application, regardless of how high your credit score is.

3. High Credit Utilization

If you currently have $10,000 in available credit across three cards, and you owe $9,000, your credit utilization is 90%. Even if you have never missed a payment, banks will see you as a high risk because you are maxing out your existing lines. You need to pay those balances down before applying for a new card.

You can map out how lowering your utilization will specifically boost your approval odds by utilizing our Credit Score Simulator & Improvement Planner.

Test Your Credit Score Before Making Big Moves

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our simulator.

Launch Credit SimulatorCommon Mistakes When Applying for Credit Cards

Applying for credit blindly can trigger a cascade of negative effects on your financial profile. Avoid these frequent beginner traps.

- Mistake 1: The “Shotgun” Approach: Getting denied for one card and immediately applying for five others out of frustration is a terrible idea. Every application triggers a hard inquiry. Racking up five hard inquiries in one day will severely damage your score and guarantee universal rejection.

- Mistake 2: Relying on VantageScore: The free credit score provided by your banking app or a free tracking website is almost always a VantageScore, not a FICO score. While educational, it can be wildly inaccurate. Your app might say your score is 700, but the bank pulling your FICO score might see a 640.

- Mistake 3: Closing Old Accounts Before Applying: The age of your credit history accounts for 15% of your total FICO score. If you close your oldest credit card right before applying for a new one, you shorten your credit history and drop your score exactly when you need it to be at its highest. Read our guide on Credit Score Mistakes That Are Dropping Your Score to learn more.

Credit Score Target Timeline

Building your credit is a marathon, not a sprint. To help you set actionable goals, here is a quick look at the baseline FICO scores you should target for major financial milestones:

| Financial Goal | Target FICO Score |

| Qualifying for a First Credit Card | 580+ |

| Securing a Good Cash Back Card | 670+ |

| Unlocking a Premium Rewards Card | 740+ |

| Building a Strong Mortgage Profile | 740+ |

A strong credit score is not just about getting travel perks or cash-back rewards. Most conventional mortgage programs require a deeply established credit history, which is why many first-time homebuyers begin with secured or student credit cards years before ever applying for a home loan. If you plan to buy real estate in the future, securing your credit foundation today is mandatory. To see exactly how your score impacts a home purchase, review our breakdown on FHA vs Conventional Loan Requirements.

Action Plan: Apply with Confidence Today

Do not let fear keep you from utilizing the financial tools you need. Follow these exact steps to ensure your next application is a success.

- Check Your Real Credit Report: Go to AnnualCreditReport.com. It is the only federally mandated website that allows you to pull a free, comprehensive credit report from all three bureaus. Look for errors or accounts in collections you didn’t know about.

- Find Your FICO Score: Check if your current bank or credit card provider offers a free FICO® Score update. If they do not, you can purchase it directly from myFICO.com.

- Optimize Your Utilization: If you have balances on existing cards, pay them down so your overall credit utilization is below 10%. Wait 30 days for the new, lower balances to report to the bureaus.

- Use Pre-Qualification Tools: Almost all major banks offer a “Pre-Qualify” or “See if You’re Approved” button on their websites. This uses a “soft pull” on your credit, which does not hurt your score. It will tell you with high accuracy whether you will be approved before you formally apply.

Next Steps

Once you secure your new credit card, your priority shifts from getting approved to optimizing how you use it. To avoid debt and maximize your new financial tool, your next steps should be:

- Building a cash buffer so you never have to carry a credit card balance. Unsure of your target? Run the Advanced Emergency Fund Analyzer.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings Target- Creating a monthly spending plan using the Financial Freedom Planner.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom Plan- Learning the exact strategies to safely raise your limits in our guide: How to Increase Your Credit Limit Without Hurting Your Credit Score.

Frequently Asked Questions

Can I get a credit card with a 500 credit score?

Yes, but your options are limited. A score of 500 falls into the “Poor” category. You will almost certainly be denied for standard unsecured cards. Your best and safest option is to apply for a secured credit card, which requires a refundable cash deposit.

Does checking my own credit score hurt it?

No. Checking your own credit score or pulling your own credit report is considered a “soft inquiry” and has zero impact on your FICO score. Only “hard inquiries,” which occur when a lender checks your credit to approve an application, will temporarily lower your score.

Why was I denied a credit card with a 750 credit score?

A high credit score is not a guarantee of approval. You may have been denied because your income is too low to support the credit line, your debt-to-income ratio is too high, or you have opened too many new credit accounts recently (violating internal bank rules like the 5/24 rule).

How long do hard inquiries stay on my credit report?

A hard inquiry remains on your official credit report for 24 months. However, the negative impact on your FICO score usually diminishes significantly after the first six months, and FICO entirely ignores the inquiry in its calculation after 12 months.

What is the easiest unsecured credit card to get approved for?

Student credit cards and basic retail store cards are generally the easiest unsecured cards to obtain. If you are not a student and want to avoid high retail interest rates, look for cards specifically marketed as “credit-building” cards or starter cards from banks like Capital One and Discover.

References and Resources

To ensure you have the most accurate, up-to-date information regarding your credit and consumer rights, we highly recommend exploring these official resources:

- Consumer Financial Protection Bureau (CFPB): The CFPB offers exceptional guidance on your rights regarding credit reporting and what to do if you are unfairly denied credit. Visit the CFPB guide on credit cards.

- FICO: Since FICO is the mathematical model used by 90% of top lenders, reviewing their official breakdowns of score components is mandatory for serious planners. Review the FICO score factors.

- AnnualCreditReport.com: The only federally authorized website where you can pull your complete credit reports from Equifax, Experian, and TransUnion for free. Visit AnnualCreditReport.com.

- Federal Trade Commission (FTC): Provides robust, plain-language advice on recovering from bad credit safely and disputing errors on your credit report. Explore Consumer.gov credit basics.

- Federal Deposit Insurance Corporation (FDIC): The FDIC provides excellent educational materials on navigating credit card offers and avoiding predatory lending practices. Explore FDIC Consumer Assistance.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.