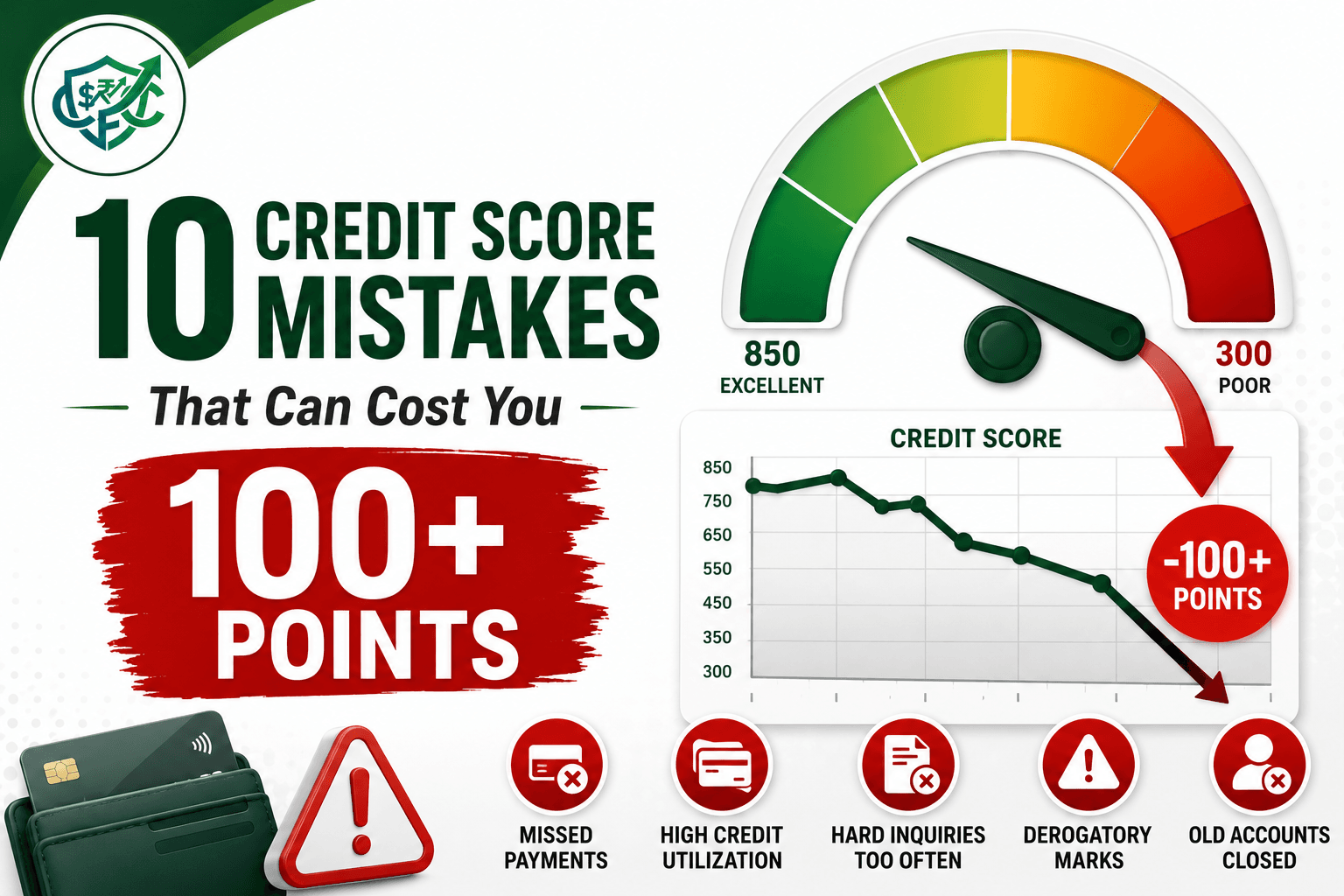

10 Credit Score Mistakes That Can Cost You 100 Points

If you are reading this, you might be staring at a credit monitoring app in total disbelief, wondering how innocent credit score mistakes could have wiped out 100 points of your hard work literally overnight.

It is a terrible, sinking feeling. You spend years diligently paying your bills, keeping your head down, and trying to play by the rules. You check your phone, expecting to see that nice green arrow pointing upward, but instead, you see a massive red downward plunge. A 740 suddenly becomes a 630. Your stomach drops. You instantly start worrying about whether you can still get approved for that apartment, buy that car, or if your current credit card companies are going to slash your limits.

When this happens, it is incredibly easy to feel embarrassed or angry. You might feel like the financial system is rigged against you.

The honest truth? The credit scoring system is incredibly rigid, and it does not operate on common sense. The algorithms that calculate your score do not know you are a good person. They do not know you lost your job, or that your dog had an emergency vet visit, or that your bank’s autopay system glitched. They only see raw data. And unfortunately, some of the most logical, responsible-sounding financial moves you can make will actually trigger massive penalties in that algorithm.

Let’s strip away the confusing banking jargon and talk about reality. Here is a breakdown of exactly what causes those massive drops, the relatable traps people fall into, and how you can start repairing your financial profile today.

The Real Problem: How the Algorithm Actually Works

Before we talk about the mistakes, you have to understand the judge. Your FICO credit score is fundamentally a risk-prediction tool. It was built for banks, not for you. Its only job is to look at your behavior and predict the likelihood that you will go 90 days late on a bill within the next two years.

When you do something that statistically correlates with “financial stress”—even if you have plenty of cash in the bank—the algorithm panics and drops your score to warn lenders. It doesn’t matter if you have a perfect 10-year track record; certain actions will cause an immediate, harsh reaction.

The good news is that because it is just a mathematical formula, it is completely predictable. Once you know the rules, you can stop stepping on the landmines. Here are the ten most brutal mistakes that can cost you 100 points or more.

1. The Accidental 30-Day Late Payment

This is the most common heartbreaker in personal finance. You have a card you rarely use. Maybe you bought a coffee with it three months ago and completely forgot about the $4 balance. You do not check the app, the email warning goes to your spam folder, and thirty days pass.

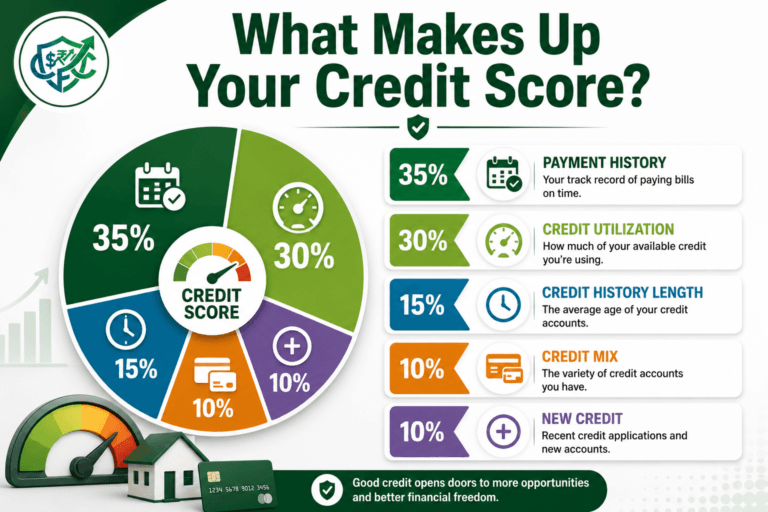

Payment history makes up a massive 35% of your total credit score. It is the heavily weighted factor. A single payment that crosses the 30-day late threshold can instantly incinerate 80 to 110 points from a highly-rated credit profile. The higher your score was to begin with, the further it falls.

The Fix: If you truly just forgot, call the lender immediately. Pay the balance over the phone and politely ask for a “good will deletion” of the late mark. If they say no, don’t panic. Read our guide on exactly what happens if you missed a credit card payment to see how quickly the damage fades.

2. Maxing Out a Card for a Genuine Emergency

Imagine your car’s transmission blows up. It costs $3,500 to fix, and you only have $1,000 in your checking account. You do what you have to do to get to work: you put the remaining $2,500 on a credit card with a $3,000 limit.

You plan to pay it off aggressively, but the very next week, your credit score plummets by 60 or 70 points. Why? Because you just spiked your credit utilization ratio. This ratio measures how much debt you have compared to your available limits. FICO hates when you use more than 30% of a card’s limit, and if you max one out completely, the algorithm assumes you are in a financial tailspin.

If you’re unfamiliar with how credit utilization is calculated or why it has such a significant impact on your credit score, What Is Credit Utilization — And Why Does It Matter? explains the concept with beginner-friendly examples.

The Fix: The damage here is temporary. The moment you pay that balance down below 30%, your score will bounce right back up the following month.

3. Closing Your Oldest Account to “Clean Up”

This mistake is entirely based on bad advice passed down through generations. People often think that having too many open credit cards looks “messy.” So, in an effort to be responsible, they call the bank and close the very first credit card they opened in college because they haven’t used it in years.

This is a massive unforced error. Fifteen percent of your score is based on the length of your credit history. Closing your oldest account eventually wipes out years of good history. Even worse, you immediately permanently lose the available credit limit on that card, which instantly drives your overall credit utilization ratio higher.

The Fix: Leave old, free credit cards open. Buy a pack of gum with them twice a year and pay it off immediately just to keep the bank from closing the account due to inactivity.

4. Co-Signing for Someone Else’s Dream

You love your younger sister, and she needs a reliable car to get to her new job. Because she is just starting out, the dealership requires a co-signer. You have a great 750 credit score, so you sign the paperwork.

Six months later, she loses her job and misses two payments. She doesn’t tell you because she is embarrassed. The next time you check your credit app, your score has dropped by 100 points.

When you co-sign a loan, you are not just a reference. Legally, that loan is 100% yours. If the primary borrower misses a payment, the bank reports it as your missed payment. If they max out the card, it raises your utilization.

The Fix: Never co-sign a loan unless you are entirely prepared to make the monthly payments yourself out of your own bank account.

5. Applying for Too Many Things at Once

You are walking through the mall, and the cashier at your favorite clothing store offers you 20% off your purchase today if you open a store card. Later that week, you apply for a new travel rewards card. The following week, you fill out an application for an auto loan.

Every time you apply for new credit, the lender performs a “hard inquiry” on your report. One inquiry usually only dings your score by 3 to 5 points. But if you rack up four or five inquiries in a single month, the algorithm views you as desperate for cash. The compounded penalty can easily drag your score down by 20 to 40 points.

6. Ignoring a Tiny Medical or Utility Bill

You moved out of your apartment last year and canceled the internet. Two months later, the internet company sends a final closing bill for $38. It gets lost in the mail. You have no idea it exists until you get a notification that a collections agency has hit your credit report, dropping your score by 90 points.

It feels incredibly unfair that a $38 oversight can destroy a decade of perfect mortgage payments, but to the FICO model, an unpaid collection is a massive red flag.

The Fix: If a tiny bill goes to collections, do not just blindly pay it online. Call the collection agency and negotiate a “Pay for Delete” agreement, where you agree to pay the debt in full only if they agree in writing to remove the negative mark from your credit reports entirely.

7. Actually Paying Off a Loan (The Strangest Drop)

This is the one that makes people furious. You work incredibly hard, make sacrifices, and finally send the last $500 payment to clear your auto loan or student loan. You expect a massive boost to your credit score to reward your discipline.

Instead, your score drops 20 points.

The algorithm rewards you for having an active “Credit Mix” (a blend of revolving credit cards and installment loans). When you pay off an installment loan, that account is closed. FICO sees that you now have one less active, positive account contributing to your current mix, and adjusts your score downward.

The Fix: Take a deep breath and do nothing. Being completely debt-free is vastly more important to your real-world wealth than a temporary 20-point dip in an algorithm. Your score will recover naturally in a few months.

8. Relying on “Minimum Payments” for Years

When money is tight, making the minimum payment on your credit cards feels like survival. It keeps the late fees away and keeps your account in good standing. But if you can only afford the minimum payments, you are walking into a slow-motion trap.

Because interest continues to compound every month, your actual balance barely moves. Over time, your utilization stays dangerously close to 100%. Even though you have never missed a due date, the algorithm sees that you are perpetually maxed out, which drastically suppresses your score and makes you look like a severe lending risk.

9. Consolidating Debt and Then Swiping Again

Debt consolidation can be a brilliant move if done correctly. You take out a $10,000 personal loan to pay off your maxed-out credit cards. Your utilization drops to zero, and your credit score shoots up.

The fatal mistake happens three months later. Because you now have a bunch of empty credit cards, the temptation returns. You put a vacation on the card. Then some new furniture. Before you know it, you have a $10,000 personal loan and $10,000 in new credit card debt. You have doubled your debt burden, your utilization spikes again, and your score crashes harder than before.

The Fix: If you clear your cards with a loan, physically cut the cards up. Remove them from your digital wallets. You must address the underlying spending habits, or the cycle will destroy your finances.

10. Waiting Until the Last Minute to Check Your Report

Far too many people never look at their actual credit reports until the day they sit down in a loan officer’s office to buy a house. Roughly one in five Americans has a verifiable error on their credit report.

It might be a late payment belonging to someone with the same name, or a fraudulent account opened by an identity thief. If you wait until the last minute to find out about these errors, you will not have time to fix them. The dispute process can take 30 to 45 days, which is enough time to lose the house you wanted to buy.

The Fix: Pull your free official reports from AnnualCreditReport.com at least six months before you plan to apply for any major loan.

The Beginner-Friendly Action Plan: How to Recover

📊 Map Out Your Credit Score Recovery

Don’t just guess what will happen to your score if you pay off a specific card, close an old account, or take out a new loan. Safely test your next financial move using our Free Credit Score Simulator & Improvement Planner before you actually make it.

If you read through that list and realized you just made one of those mistakes, do not panic. Your financial life is not ruined. Credit scores are highly fluid, and with the right strategy, they bounce back faster than you think.

Step 1: Stop the bleeding. Put your credit cards on ice. Do not apply for anything new. If you missed a payment, get your account current today. Time is the only thing that heals a late payment, and the clock doesn’t start until the past-due balance is paid.

Step 2: Attack the balances. If your score dropped because of high utilization, you have total control. Every single dollar you pay down on your credit card balances will systematically push your score back up when the bank reports to the bureaus next month.

If your credit history has been damaged and you’re rebuilding from the ground up, Best Secured Credit Cards for Beginners in 2026 compares secured cards that can help you establish positive payment history while keeping your credit utilization under control.

Step 3: Build a real safety net. The number one reason people max out credit cards or miss payments is a lack of cash reserves. You cannot protect your credit score without protecting your checking account first. Figure out exactly how much emergency fund you really need and start saving automatically every payday.

Frequently Asked Questions (FAQs)

How fast can a credit score recover from a 100-point drop? It entirely depends on what caused the drop. If you lost 100 points because you maxed out three credit cards for a medical emergency, your score will recover in just 30 to 45 days the moment you pay those balances back down. However, if your score dropped 100 points because you missed two mortgage payments, it will take 12 to 24 months of perfect payment history to slowly rebuild that trust.

Will checking my own credit score lower it? No, absolutely not. Checking your own credit via an app, your bank, or AnnualCreditReport.com is considered a “soft inquiry.” Soft inquiries are completely invisible to lenders and do not affect your score by a single point. You can check your own score every day if you want to.

Does carrying a small balance help my credit score? This is one of the most stubborn myths in personal finance. You do not need to carry a balance and pay interest to build credit. Paying your statement balance in full, down to $0.00, every single month is the absolute best thing you can do for your credit profile.

Final Thoughts: Give Yourself Some Grace

If you are staring at a damaged credit profile today, it is so important to take a step back and look at the bigger picture. We attach so much morality and self-worth to that three-digit number, but a credit score is not a reflection of your character. It is simply a tool that banks use to make money.

Mistakes happen. Emergencies happen. Sometimes you have to sacrifice your credit score to keep the lights on or fix the car so you can get to work. That is just the messy reality of being a human being navigating the financial world.

If you made one of the credit score mistakes above, forgive yourself. You cannot rewrite the past, but the beauty of the credit system is that it heavily favors your most recent behavior. By setting up automatic payments today, refusing to take on new debt, and slowly chipping away at your balances, you force the algorithm to trust you again. It might take a few months, or it might take a year, but the math will eventually work in your favor. You’ve got this.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

Sources & References

Articles published on Clarity Flow Core are researched and reviewed using publicly available information from official government agencies, financial institutions, consumer protection organizations, credit bureaus, and trusted educational resources.

Reference sources may include:

- Internal Revenue Service (IRS)

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve

- U.S. Department of the Treasury

- Federal Trade Commission (FTC)

- Bureau of Labor Statistics (BLS)

- Federal Deposit Insurance Corporation (FDIC)

- Securities and Exchange Commission (SEC Investor.gov)

- Experian

- Equifax

- TransUnion

- myFICO

- AnnualCreditReport.com

- Official banking, lending, insurance, and financial institution websites

- Public consumer finance studies and educational resources

Additional editorial references may include reputable financial publications, academic research, behavioral finance studies, housing and credit market data, and publicly available consumer finance resources where relevant.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.