How Much Should You Save for Retirement Each Month?

⚡ Quick Answer

Financial experts generally recommend saving 15% of your gross monthly income for retirement. This 15% target includes any matching contributions from your employer. If you cannot afford 15% right now, the most important step is to contribute enough to get your full employer match and then increase your contribution by 1% each year.

You are sitting at your kitchen table, looking at your budget, and wondering about the future. You know you need to save for retirement, but every time you try to figure out exactly how much cash to set aside, you are hit with a wave of conflicting advice.

Some financial gurus scream that you need millions of dollars to survive. Others tell you to just put $50 a month in an account and let the stock market do the rest.

When you are trying to balance paying rent, buying groceries, and maybe paying down some credit card debt, setting aside money for an event that is thirty years away feels impossible. You do not want a complicated algebraic formula; you just want a straight answer. How Much Should You Save for Retirement Each Month?

If you guess too low, you risk running out of money in your later years and relying entirely on an unpredictable Social Security system. If you save too aggressively, you might unnecessarily deprive yourself of living a comfortable life today.

In this comprehensive guide, we are going to remove the guesswork. We will break down the industry-standard 15% rule, show you exactly how to calculate your personal monthly savings target, explain how to catch up if you are starting late, and give you a step-by-step action plan to put your retirement savings on autopilot.

The Golden Rule: The 15% Target

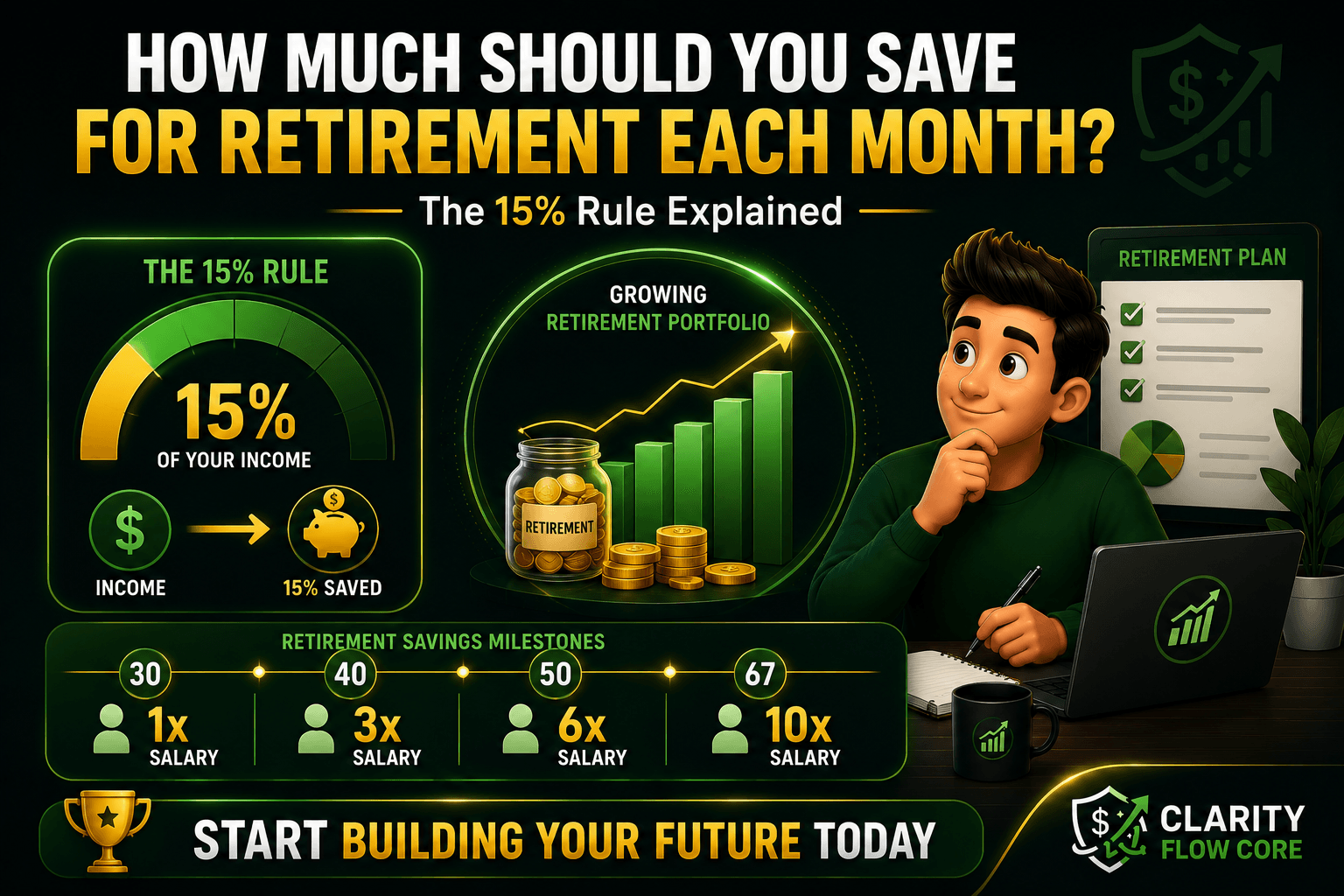

If you want the most universally accepted, mathematically sound rule of thumb in the personal finance world, here it is: You should aim to save 15% of your pre-tax income for retirement every single year.

This is not an arbitrary number pulled out of thin air. Financial institutions and economists have run thousands of market simulations. Assuming you work from age 25 to age 67, saving 15% of your income consistently gives you an incredibly high probability of maintaining your current standard of living throughout your entire retirement, regardless of how the stock market fluctuates over the decades.

How the 15% Math Works

Let’s look at a realistic example to see how this translates into a monthly target.

Suppose you make $60,000 a year.

- Your gross (pre-tax) income is $5,000 per month.

- 15% of $5,000 is $750.

To hit the golden rule, your target is to put $750 into a retirement account every month.

At first glance, taking $750 out of your paycheck might seem completely terrifying. But here is the massive secret that beginners often miss: You do not necessarily have to come up with all 15% by yourself.

The Power of the Employer Match

If you work for a company that offers a 401(k) or 403(b) retirement plan, they likely offer an “employer match.” This means the company will contribute their own money into your retirement account based on how much you put in.

Let’s go back to our $60,000-a-year example.

- Your goal is to save 15% ($750 a month).

- Your employer offers a 5% match. That means if you put in 5% of your salary ($250), your employer will give you another 5% ($250) completely for free.

- Because your employer is contributing 5%, you only need to contribute 10% ($500 a month) from your own paycheck to hit the 15% total target.

Always factor your employer’s match into your 15% goal. It is essentially free compensation that dramatically lowers the burden on your monthly budget.

Savings Benchmarks: Are You on Track by Age?

The 15% rule is fantastic for setting your monthly budget going forward, but how do you know if the money you have already saved is enough?

Fidelity Investments, one of the largest financial services corporations in the world, created a highly regarded set of age-based benchmarks. These benchmarks act as checkpoints to tell you if your retirement portfolio is growing at the right pace.

Here is how much you should have saved by different ages, expressed as a multiple of your current salary:

| Your Age | How Much You Should Have Saved | Example (Based on a $70,000 Salary) |

| Age 30 | 1x your current salary | $70,000 |

| Age 40 | 3x your current salary | $210,000 |

| Age 50 | 6x your current salary | $420,000 |

| Age 60 | 8x your current salary | $560,000 |

| Age 67 | 10x your current salary | $700,000 |

What If You Are Behind?

If you are 40 years old and do not have three times your salary saved, take a deep breath. You are not alone, and you are not doomed to work forever. These benchmarks assume continuous, perfect employment and a steady 15% savings rate since age 25. Very few people have a perfect financial journey.

If you are behind, it simply means you need to adjust your monthly strategy today. You might need to temporarily increase your savings rate from 15% to 18% or 20%, or plan to work a couple of extra years. To map out exactly what your required monthly contribution should be to catch up, we highly recommend plugging your specific numbers into our Financial Freedom Planner. This tool will project your portfolio’s growth and show you exactly what age you can safely retire based on your current savings rate.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanHow to Calculate How Much Should You Save for Retirement

While the 15% rule is the best starting point, personal finance is highly personal. Some people want to retire to a luxury condo in Florida, while others want to live a quiet, frugal life in a paid-off cabin in the Midwest.

To figure out exactly how much you need to save each month, you first need to calculate your ultimate “Retirement Number”—the total amount of cash you need in your portfolio on the day you stop working.

Step 1: Estimate Your Annual Retirement Expenses

First, estimate how much money you will need to live on each year during retirement. A common rule of thumb is that you will need about 80% of your pre-retirement income to maintain your lifestyle. (You no longer have to pay payroll taxes, commute to work, or save for retirement).

If you make $80,000 a year right now, you can estimate you will need about $64,000 a year in retirement to be comfortable.

Step 2: Use the 25x Rule

Once you have your annual expense number, multiply it by 25. This is based on the famous “4% Rule,” a study showing that if you withdraw 4% of your portfolio each year, your money should easily last for a 30-year retirement without running out.

- $64,000 x 25 = $1,600,000

In this scenario, your ultimate Retirement Number is $1.6 million.

Step 3: Work Backwards to Your Monthly Target

Now that you know you need $1.6 million, you can work backwards using a compound interest calculator to find your exact monthly target.

Assuming an average annual stock market return of 7% (adjusted for inflation):

- If you are 25 years old (40 years to grow), you need to save roughly $650 a month.

- If you are 35 years old (30 years to grow), you need to save roughly $1,400 a month.

- If you are 45 years old (20 years to grow), you need to save roughly $3,200 a month.

The math tells a clear, undeniable story: the earlier you start, the cheaper it is to retire. Compound interest does the heavy lifting for you if you give it enough time.

Where Should You Put Your Monthly Savings?

Once you decide to save $500 or $1,000 a month, you cannot just leave it in your checking account. Inflation will eat its purchasing power, and it will not grow enough to support you. You must invest it in tax-advantaged retirement accounts.

Here is the ideal hierarchy for where to place your monthly retirement savings:

1. The 401(k) Employer Match

If your company offers a 401(k) match, this is your absolute first priority. Contribute exactly enough to get the maximum match. If they match up to 5%, you put in 5%. This is a 100% immediate return on your investment. Declining the match is the mathematical equivalent of turning down a pay raise.

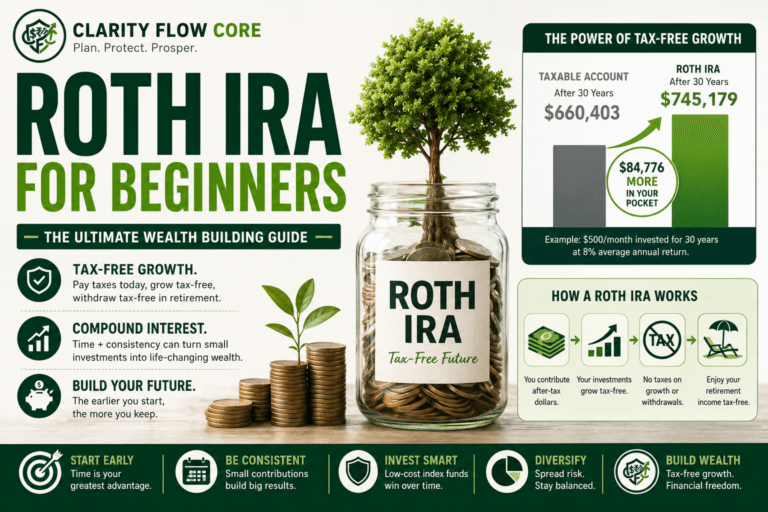

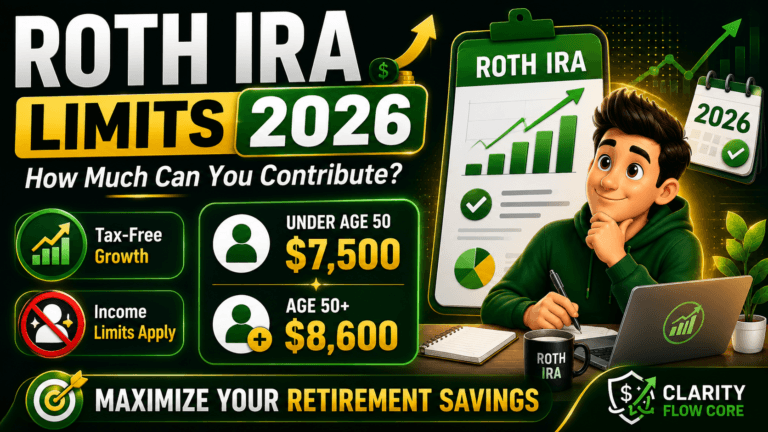

2. The Roth IRA

Once you have secured your employer match, direct your remaining monthly savings into a Roth IRA. A Roth IRA is an individual retirement account that you control completely. You fund it with after-tax dollars, but every dollar of growth and every withdrawal you make in retirement is 100% tax-free.

If you put $5,000 into a Roth IRA and it grows to $50,000, you get the entire $50,000 tax-free. If you aren’t sure how these accounts work, read our comprehensive guide on Traditional IRA vs Roth IRA: Which Is Better for Beginners? and Roth IRA for Beginners: How It Works and Why People Use One.

3. Back to the 401(k)

If you max out your Roth IRA for the year (the limit is $7,500 for those under 50 in 2026) and you still have money left over in your 15% budget, go back to your workplace 401(k) and increase your contributions there until you hit your target.

What If You Cannot Afford 15% Right Now?

If you are looking at your budget and realizing there is absolutely no way you can save 15% of your income right now, do not panic. Do not let the perfect be the enemy of the good. Saving 3% is infinitely better than saving 0%.

Here is the beginner strategy for ramping up to the 15% target without shocking your checking account:

The “Match and 1%” Strategy

- Start with the Match: Contribute just enough to get your employer match. Even if things are tight, this free money is too valuable to pass up.

- Auto-Escalate by 1%: Log into your 401(k) portal and look for a feature called “Auto-Escalation” or “Auto-Increase.” Set it to increase your contribution by 1% every year, ideally timing it with your annual raise.

- Absorb the Difference: Because you are only increasing your savings rate by 1% per year (e.g., from 5% to 6%), the difference in your actual paycheck will likely be less than $20 a week. You will hardly notice the missing money, but over five years, you will seamlessly transition into a 10% or 15% savings rate.

If high-interest debt is preventing you from investing, you must stop the bleeding first. Use our Free Credit Utilization Calculator & Recovery System to build a strategy to wipe out your credit card balances, freeing up hundreds of dollars in monthly cash flow that can be redirected toward your retirement.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationCommon Mistakes Beginners Make When Saving for Retirement

Building long-term wealth is actually quite boring and systematic, but beginners often fall into massive traps that derail their progress.

Mistake 1: Leaving Your Retirement Money in Cash

An IRA or a 401(k) is not an investment; it is just a protective basket. Many beginners transfer $500 a month into their Roth IRA and assume they are investing. They are not. If you do not log in and use that cash to purchase assets (like broadly diversified index funds or Target Date Funds), your money will sit there in cash, earning practically 0% interest.

You must actively choose investments inside the account. If you do not know the difference between asset classes, check out our guide on Index Funds vs. Mutual Funds: What Beginners Should Know.

Mistake 2: Waiting Until You Are Debt-Free to Start

Unless you are drowning in 25% interest credit card debt, you should not put off saving for retirement just to pay off low-interest debt like a car loan or student loans. The stock market historically returns an average of 7% to 10% per year. If your student loan interest rate is 4%, mathematically, your money works harder for you in the stock market. Do not lose a decade of compound interest waiting for a perfect debt-free balance sheet.

Mistake 3: Skipping the Emergency Fund

Do not pour every spare penny into a retirement account if you have $0 in your checking account. Retirement accounts are legally protected and designed to be locked away until age 59 ½. If you put all your cash into a 401(k) and then your transmission blows, you will be forced to take on high-interest credit card debt to survive.

Always secure a 3 to 6-month safety net first. Run your living expenses through our Advanced Emergency Fund Analyzer to find your exact cash target, and read our Emergency Fund Basics Guide to learn exactly where to store it.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetYour Step-by-Step Action Plan

Ready to put your retirement savings on autopilot? Follow this precise timeline this week to secure your financial future.

- Fund Your Baseline Emergency Savings: Ensure you have at least 3 months of essential living expenses parked in a High-Yield Savings Account.

- Locate Your Match: Ask your HR department or log into your benefits portal to find out exactly what your 401(k) matching rules are.

- Calculate Your 15% Goal: Multiply your gross monthly income by 0.15. Subtract your employer’s match from this number to find your personal target.

- Set Up Automated Transfers: If using a 401(k), set your contribution percentage in your payroll system. If using a Roth IRA, log into your brokerage (like Fidelity or Vanguard) and set up an automatic monthly transfer from your checking account on the day you get paid.

- Select Your Investments: Ensure your automated deposits are set to automatically purchase a low-cost, broadly diversified S&P 500 Index Fund or a Target Date Retirement Fund.

- Increase Slowly: If you cannot hit the 15% target today, set up an auto-escalation to raise your contribution by 1% every year.

Frequently Asked Questions (FAQ)

Is saving $500 a month for retirement enough?

It depends entirely on your age and your income. If you start saving $500 a month at age 25 and earn an average 7% return, you will have nearly $1.3 million by age 65. If you start saving $500 a month at age 45, you will only have about $260,000 by age 65. The earlier you start, the more powerful $500 becomes.

Does my employer match count toward the 15% rule?

Yes. Most financial experts agree that the 15% target includes both your contributions and your employer’s match. If you contribute 10% and your employer matches 5%, you are successfully hitting the 15% goal.

What if I am starting late in my 40s or 50s?

If you are behind, 15% will likely not be enough. You will need to calculate your Retirement Number using the 25x rule and aggressively ramp up your savings to 20% or 25% of your income. The government helps with this: once you turn 50, the IRS allows you to make “catch-up contributions,” letting you put significantly more money into your 401(k) and IRA than younger workers.

How does inflation affect my retirement savings?

Inflation reduces the purchasing power of your money over time. When projecting retirement needs, experts usually assume a 7% stock market return instead of the historical 10% average. That 3% difference accounts for inflation, meaning the $1.6 million target you calculate today is adjusted to have the same buying power in the future.

Can I just rely on Social Security?

Absolutely not. Social Security was designed to replace roughly 40% of your pre-retirement income, not 100%. Today, the average Social Security check barely covers basic living expenses and rent in most major US cities. You must treat Social Security as a supplemental bonus, not your primary retirement plan.

Should I save for my kids’ college or my retirement first?

You should always prioritize your retirement. Your children can get scholarships, grants, and take out student loans to fund their education. You cannot take out a loan to fund your retirement. Secure your own financial mask before assisting your children.

Conclusion

Determining how much you should save for retirement each month does not need to involve complex spreadsheets or financial anxiety. The math is clear: aim for a 15% total savings rate, capture every penny of your employer match, and utilize tax-advantaged accounts like the Roth IRA.

The biggest mistake you can make is waiting for the “perfect time” to start saving. There will always be another bill, another vacation, or another expense competing for your paycheck. Start today, even if it is just 3% or $50 a month, and let the relentless power of compound interest build the financial freedom you deserve.

References & Sources

- Consumer Financial Protection Bureau (CFPB): Educational resources on planning for retirement and understanding different types of investment accounts.

- Internal Revenue Service (IRS): Official guidelines on IRA and 401(k) contribution limits, catch-up contributions, and tax deduction rules.

- Investor.gov (U.S. Securities and Exchange Commission): Free tools, compound interest calculators, and information regarding asset allocation and index funds.

- Federal Deposit Insurance Corporation (FDIC): Recommendations on establishing baseline savings habits before entering the stock market.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.