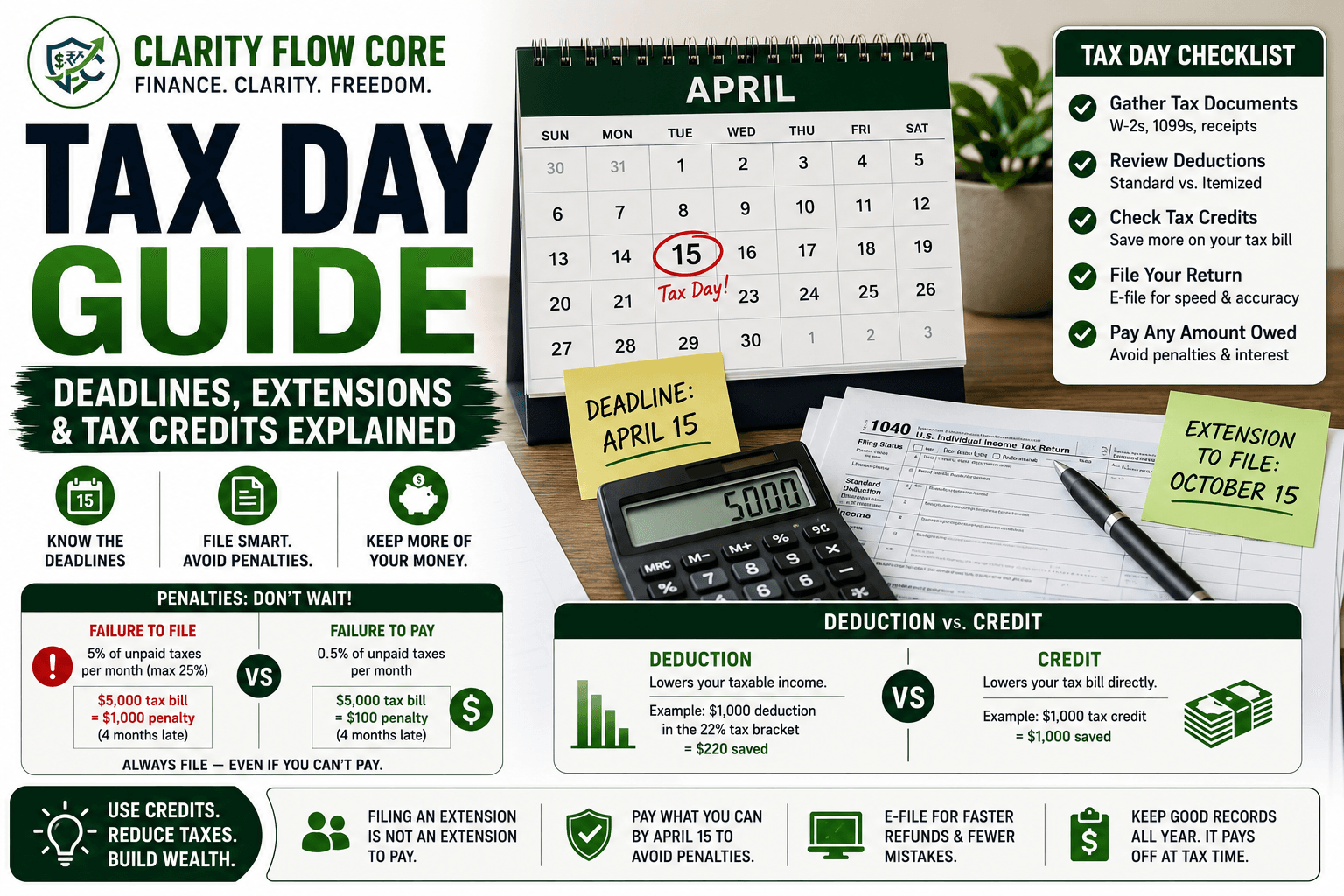

Tax Day Guide: Filing Deadlines, Extensions & Common Tax Credits

With the April 15 deadline approaching, millions of Americans are panicking. They are digging through shoeboxes for receipts, logging into old brokerage accounts for tax forms, and trying to decipher the IRS website.

Filing your taxes does not have to be a frantic, fear-driven event. The tax code is essentially a massive rulebook. If you understand the rules, you can protect your cash flow. If you ignore the rules, you will lose money to completely avoidable penalties and missed write-offs.

Whether you work a standard W-2 corporate job, operate as a freelancer, or run a small business, you need a mix of operational knowledge and grounded math to navigate the IRS.

This comprehensive Tax Day guide is designed to cut through the government jargon. Here is the exact operational math behind filing deadlines, the massive trap of tax extensions, and how to actually lower your tax bill before the clock runs out.

The Hard Deadlines

The easiest way to lose money to the federal government is to miss a hard deadline. The foundation of any reliable Tax Day guide starts with your calendar.

Missing these dates triggers automatic financial penalties that compound daily.

| Action Required | Exact Deadline | Who It Applies To |

| File Federal Tax Return | April 15 | Everyone |

| Pay Taxes Owed | April 15 | Anyone who owes money to the IRS |

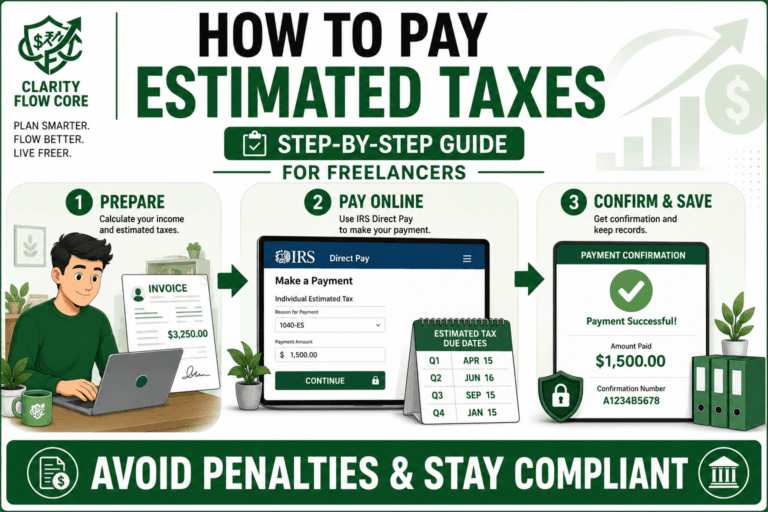

| Q1 Estimated Payments | April 15 | Freelancers, 1099 contractors, business owners |

| IRA / HSA Contributions | April 15 | Anyone wanting to lower their prior year taxable income |

| File Extended Return | October 15 | Anyone who successfully filed Form 4868 |

Note: If April 15 falls on a weekend or a recognized federal holiday (like Emancipation Day in Washington D.C.), the deadline gets pushed to the next business day.

The Biggest Trap: Filing a Tax Extension

The most misunderstood concept in this Tax Day guide is the extension.

Millions of people file Form 4868 to get a six-month filing extension, assuming it gives them until October 15th to pay what they owe. It does not.

An extension to file is not an extension to pay.

The IRS expects you to estimate how much money you owe and pay that exact amount by April 15th. If you file an extension, do not pay, and then finish your paperwork in August, the IRS will back-charge you interest and penalties for every single day you were late since April 15th.

The Math: Failure to File vs. Failure to Pay

If you finish your return on April 14th and realize you owe $5,000 that you do not have, your instinct might be to hide. You might decide to simply not file the return because you cannot afford the bill.

According to every financial professional and this Tax Day guide, that is the worst financial decision you can make. The IRS treats the act of not filing much more severely than the act of not paying.

Look at the brutal mathematical difference between the two penalties:

- The Failure to File Penalty: If you do not file your return or an extension, the IRS charges you 5% of your unpaid taxes for every month you are late, up to a maximum of 25%.

- The Failure to Pay Penalty: If you file your return on time but do not send the money, the IRS only charges you 0.5% of your unpaid taxes for every month you are late.

The Scenario: You owe $5,000 and ignore it for 4 months.

If you did not file, your penalty is 20% (4 months x 5%). You are hit with a $1,000 penalty.

If you filed but couldn’t pay, your penalty is 2.0% (4 months x 0.5%). You are hit with a $100 penalty.

Always file your return or an extension by April 15th, even if your bank account is at zero.

Standard Deduction vs. Itemizing

To lower your tax bill, you get to deduct a certain amount of money from your income before the IRS taxes it. You have two choices: take the government’s flat “Standard Deduction” or “Itemize” your specific expenses.

Because of inflation adjustments, the standard deduction is currently massive. Over 85% of taxpayers simply take the standard deduction.

Here are the baseline numbers you need for this Tax Day guide:

| Filing Status | Standard Deduction Amount |

| Single / Married Filing Separately | $15,750 |

| Married Filing Jointly | $31,500 |

| Head of Household | $23,625 |

You only itemize if your specific, allowable expenses (like mortgage interest, massive medical bills, and state/local taxes) add up to more than the standard deduction. If you are single and your itemized expenses only equal $12,000, you take the $15,750 standard deduction because it gives you a larger mathematical shield. (For a much deeper dive into the math, read Standard Deduction vs. Itemizing: Which Option Saves More?).

Deductions vs. Credits: Know the Difference

Any operational Tax Day guide must clarify the difference between a deduction and a credit. They sound similar, but mathematically, they operate on completely different levels.

A Tax Deduction lowers your taxable income.

If you make $60,000 and get a $1,000 deduction, you are now taxed as if you made $59,000. If you are in the 22% tax bracket, that $1,000 deduction saves you $220 in actual cash.

A Tax Credit is a dollar-for-dollar reduction of your final tax bill.

If your final tax bill is $4,000, and you get a $1,000 tax credit, your bill drops to $3,000. It saves you $1,000 in actual cash. Credits are infinitely more powerful.

Common Deductions & Credits You Should Claim

- Student Loan Interest Deduction: You can deduct up to $2,500 in interest paid on student loans, even if you take the standard deduction. (Note: This phases out if your income is too high).

- The Home Office Deduction: If you are a freelancer or 1099 contractor, and you use part of your home exclusively for business, you can deduct a percentage of your rent and utilities. (W-2 remote employees cannot claim this). Review 1099 Taxes Explained for Freelancers and Side Hustler to ensure you qualify.

- Residential Clean Energy Credit: Did you install solar panels or a high-efficiency heat pump? You can claim up to 30% of the installation cost as a direct tax credit.

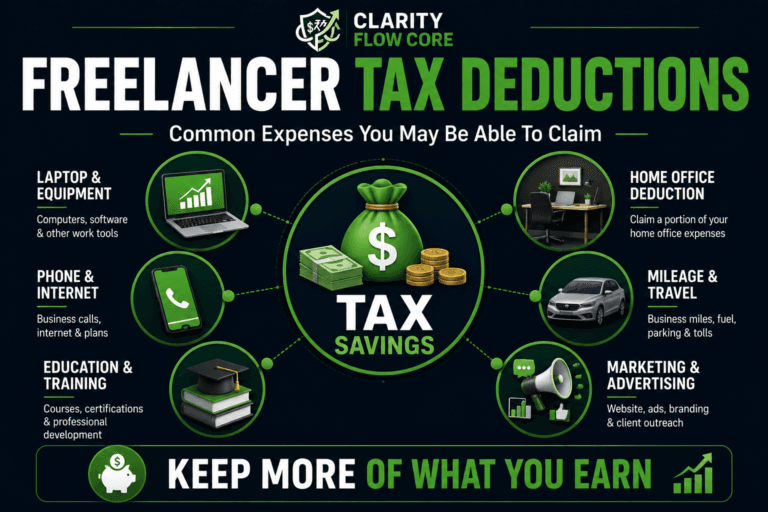

- 1099 Business Expenses: If you run a side hustle, you can write off your software, marketing, and equipment. Read 7 Tax Deductions Many Side Hustlers Overlook before you file.

The IRS Direct File Program

One of the biggest shifts covered in this Tax Day guide is the expansion of the IRS Direct File program.

Historically, you had to pay private companies like TurboTax or H&R Block to file your taxes electronically. The IRS has now rolled out its own free, direct-filing software for eligible taxpayers in participating states (including CA, NY, WA, FL, and many others).

If your tax situation is simple—meaning you only have W-2 income, standard Social Security income, or a minor amount of bank interest—you can likely bypass the $150 software fees and file directly with the government for free.

If you own a business, have complex capital gains from the stock market, or need to claim extensive 1099 deductions (like those outlined in Freelancer Tax Deductions: Common Expenses You May Be Able to Claim), you will still need to use professional software or hire a CPA.

What to Do If You Cannot Pay What You Owe

If you get to the end of your paperwork and realize you owe $8,000, panic sets in. A core purpose of this Tax Day guide is to give you an operational exit strategy when you do not have the cash.

1. The Short-Term Extension

If you just need a little extra time to gather the cash, you can apply for a short-term payment plan. The IRS will give you up to 180 additional days to pay your balance in full. You will still accrue minor interest and penalties, but it keeps the IRS from taking collection actions against you.

2. The Installment Agreement

If you cannot pay the balance in 180 days, you need a long-term installment agreement. You can set this up directly on the IRS website. The IRS will look at what you owe and put you on a monthly payment plan for up to 72 months (6 years). There is a setup fee (around $31 to $130 depending on how you apply and pay), but it makes a massive tax bill manageable.

3. The Credit Card Trap

You can legally pay your taxes with a credit card. You should almost never do this. The payment processor charges a convenience fee of around 2%, and if you do not pay off the credit card immediately, you will be hit with 24% compounding interest from your bank. The IRS’s 0.5% failure-to-pay penalty is mathematically much cheaper than credit card interest.

When This Backfires

The advice in this Tax Day guide will protect you during April, but the tax system backfires on people who fail to plan for the rest of the year. Here is where most people ruin their cash flow:

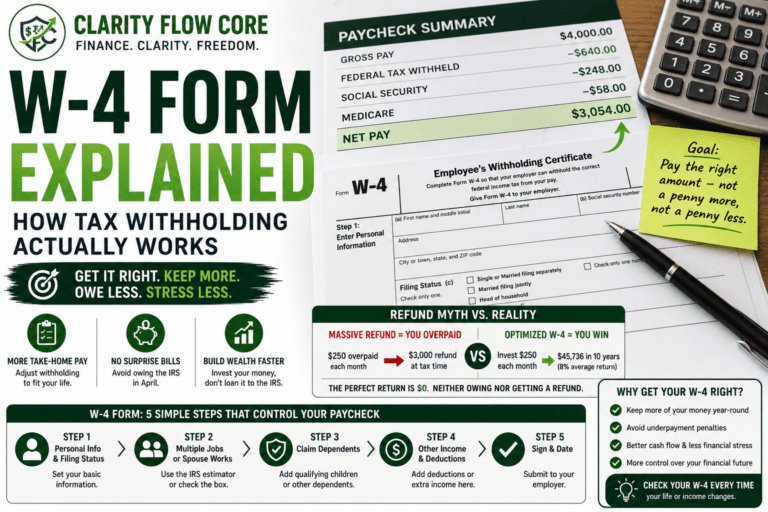

- Ignoring Your Withholdings: If you owe $5,000 to the IRS on Tax Day, it means your employer did not withhold enough taxes from your paychecks all year. You must file a new W-4 with your HR department immediately to fix the math for next year. Read W-4 Form Explained: How Tax Withholding Actually Works so you don’t make the same mistake twice.

- The “Write-Off” Fallacy: Buying a $3,000 laptop just because it is a “tax write-off” is terrible math. A write-off does not make an item free; it just means you aren’t taxed on the money used to buy it. You are still out the cash.

- Falling for Scams: As April 15th approaches, phishing emails and fake “IRS” phone calls skyrocket. The IRS will never text you, email you, or message you on social media demanding payment. They communicate via physical letters in the mail.

The Bottom Line

It is completely normal to feel stressed as April 15th approaches. However, the best way to protect your money is to substitute that stress with operational knowledge.

Use this Tax Day guide to build your checklist. Gather your forms early. File an extension if you absolutely need more time to get your paperwork right, but ensure you pay what you estimate you owe. Do not hide from a tax bill you cannot afford. Claim the deductions you are legally entitled to, set up a payment plan if necessary, and take control of your financial relationship with the government.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

Sources & References

Articles published on Clarity Flow Core are researched and reviewed using publicly available information from official government agencies, financial institutions, consumer protection organizations, credit bureaus, and trusted educational resources.

Reference sources may include:

- Internal Revenue Service (IRS)

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve

- U.S. Department of the Treasury

- Federal Trade Commission (FTC)

- Bureau of Labor Statistics (BLS)

- Federal Deposit Insurance Corporation (FDIC)

- Securities and Exchange Commission (SEC Investor.gov)

- Experian

- Equifax

- TransUnion

- myFICO

- AnnualCreditReport.com

- Official banking, lending, insurance, and financial institution websites

- Public consumer finance studies and educational resources

Additional editorial references may include reputable financial publications, academic research, behavioral finance studies, housing and credit market data, and publicly available consumer finance resources where relevant.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.