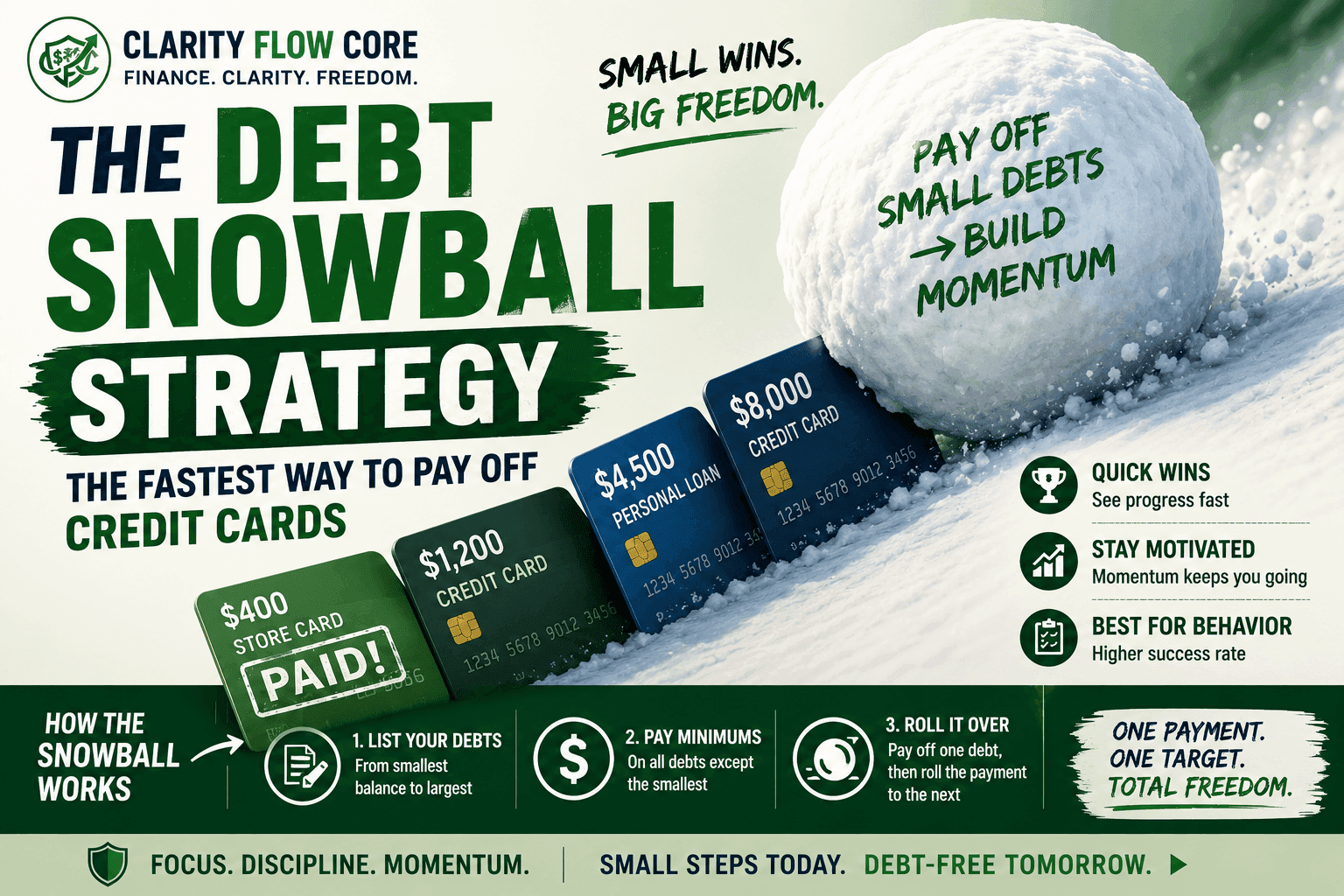

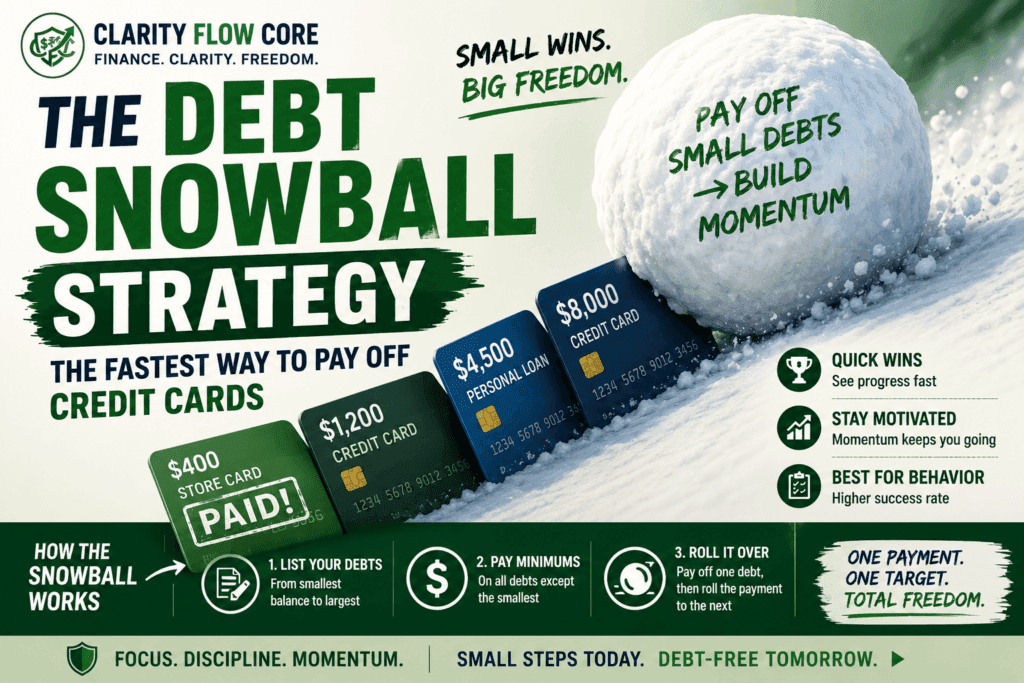

How the Debt Snowball Method Works for Credit Card Debt

Three years ago, before I discovered the debt snowball method, I stared at a spreadsheet on my laptop that made my stomach drop.

I had five different credit cards open. One was from a big-box furniture store, two were standard cash-back cards, and one was a high-limit travel rewards card. The total balance across all of them was just shy of $18,000.

Every month, I was paying the minimums. I watched hundreds of dollars vaporize into interest charges while the principal balances barely moved. It felt like trying to paddle a raft upstream against Class IV white-water rapids—exhausting, terrifying, and getting me absolutely nowhere.

I was paralyzed. Trying to math my way out of it clearly wasn’t working.

If you are carrying high-interest credit card debt, you know exactly what that paralysis feels like. With many credit cards charging interest rates above 20%, the traditional advice of just “paying a little extra” is a recipe for burnout. (Want to understand exactly how the banks are charging you? Read Understanding Credit Card APRs).

That is why I abandoned the math and turned to psychology. I used the debt snowball method, and it completely changed my financial life.

Here is exactly how to execute it, step-by-step.

Math vs. Psychology: Why the Debt Snowball Method Works

If you ask a university finance professor how to pay off debt, they will almost always tell you to use the Avalanche approach. They will tell you to rank your debts strictly by interest rate and aggressively pay off the card with the highest APR first.

Mathematically, the professor is correct. But humans are not perfectly rational calculators. We are highly emotional creatures, especially when it comes to money.

Getting out of debt is a behavioral battle, not an academic one. Let’s say your highest-interest credit card has a massive $15,000 balance. If you scrape together an extra $50 at the end of every month and throw it at that massive balance, you won’t see any real visual progress for over a year. The balance will drop to $14,400, and you will feel completely defeated. You will get bored, lose your motivation, and eventually go right back to your old spending habits.

The debt snowball method ignores interest rates entirely. Instead, it focuses on behavioral economics. It engineers quick psychological wins by targeting your smallest balances first, giving your brain the exact dopamine hit it needs to stay focused.

Debt Snowball vs. Debt Avalanche: A Direct Comparison

Before diving into the steps, here is how the two heavyweights of debt payoff stack up against each other:

| Feature | Debt Snowball | Debt Avalanche |

| Strategy | Pays smallest balances first | Pays highest interest rate first |

| Primary Benefit | Strong psychological motivation | Saves more money mathematically |

| Best For | People needing momentum | Highly disciplined borrowers |

| The Result | Faster emotional wins | Faster interest savings |

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyHow to Execute the Debt Snowball Method

The strategy requires incredible focus, but the actual steps to set up the debt snowball method are beautifully simple. Grab a piece of paper or open a blank spreadsheet, and follow these three steps.

Step 1: The Master List

Sit down, log into all your banking portals, and list every consumer debt you want to eliminate, including credit cards, personal loans, store cards, and other unsecured debts. Rank them from the smallest total balance to the largest total balance. Completely ignore the interest rates. Ignore what the monthly payments are. Just look at the total amount owed.

Step 2: Minimums on Everything, Maximum on the Smallest

You must continue making the minimum monthly payment on every single card so your credit score doesn’t tank. But you take every extra dollar you can find in your monthly budget and throw it entirely at the smallest debt on the list.

Step 3: Roll It Over (The Snowball Effect)

Once that smallest debt is fully paid off, you take the money you were using for it, and you roll it directly into the payment for the next smallest debt on your list. You never lower the amount of money you are dedicating to debt; you just point the firehose at a new target. This is the core engine of the debt snowball method.

A Real-World Example

Let’s look at a typical consumer debt profile to see exactly how the debt snowball method builds unstoppable momentum.

| Target Order | Debt Name | Total Balance | Minimum Payment |

| 1 | Macy’s Store Card | $400 | $25 |

| 2 | Capital One Visa | $1,200 | $40 |

| 3 | Personal Bank Loan | $4,500 | $150 |

| 4 | Chase Sapphire | $8,000 | $200 |

Let’s assume you review your budget, cancel a few streaming services, stop eating out, and manage to free up an extra $100 a month.

Here is how the debt snowball method alters your cash flow over time:

- Month 1: You pay the minimums on everything, but you send $125 ($25 minimum + $100 extra) to the Macy’s card.

- Month 4: The Macy’s card is completely paid off. You celebrate the win and consider whether the account still serves a useful purpose. In many cases, keeping older accounts open can help maintain your credit history and available credit. You feel a massive psychological win. You actually accomplished something!

- Month 5: Now, your snowball gets bigger. You take that $125 you were sending to Macy’s, and you add it to the Capital One minimum payment ($40). You are now sending $165 a month to the Capital One Visa without changing your lifestyle or finding any new money. The speed of your payoff is accelerating.

When Capital One is dead a few months later, you take that entire $165, roll it into the $150 personal loan payment, and suddenly you are attacking your bank loan with over $315 a month. By the time you reach the massive Chase Sapphire bill at the very bottom of the list, your monthly payment snowball is so large that it absolutely crushes the principal balance in record time.

Who Should Use the Debt Snowball Method?

The debt snowball method works best if:

- You feel overwhelmed by multiple debts.

- Motivation has been a bigger problem than budgeting.

- You have several small balances that can be eliminated quickly.

- Previous payoff plans have failed because progress felt too slow.

The debt snowball method may not be ideal if:

- You are highly disciplined and emotionless about your money.

- Your primary goal is minimizing total interest costs.

- One debt carries an exceptionally high interest rate that is causing balances to grow rapidly.

Common Debt Snowball Mistakes to Avoid

While the snowball method is powerful, it requires discipline to execute properly. Many beginners accidentally sabotage their progress by falling into these three common traps:

1. Ignoring Your Budget

The debt snowball method works only if you consistently create extra cash flow. Without a baseline budget, the snowball has nothing to roll with. You cannot simply guess how much extra you can afford to send to your debts each month; you need to assign every dollar a job before the month even begins.

2. Continuing to Use Credit Cards

This is the fastest way to derail your progress. Many people aggressively pay down debt while continuing to swipe their cards for everyday purchases like gas and groceries, attempting to earn rewards points. This creates a toxic cycle where balances never truly disappear. To make the snowball work, you must temporarily stop using credit cards entirely and switch to a debit card or a cash-envelope system.

3. Not Tracking Progress

Debt fatigue is real. If you are blindly sending payments into the void, you will lose motivation. Create a highly visual debt tracker—whether it is a thermometer on your fridge or a colored-in spreadsheet. Seeing those balances physically fall every single month reinforces your motivation, gives you a dopamine hit, and keeps your payoff momentum alive.

Turbocharging Your Snowball with Side Hustles

The baseline math of the debt snowball method is great, but the real magic happens when you start turbocharging the early stages.

Because you are laser-focused on that tiny $400 Macy’s card at the top of the list, your brain starts looking for ways to kill it faster. This is when you start selling old electronics on Facebook Marketplace, picking up weekend shifts, or taking on freelance gigs. Because businesses are desperate for digital content, a highly lucrative avenue is producing high-quality Instagram reels or social media assets. If you can learn the basics, you can check out How to Start a Video Editing Side Hustle (Even as a Beginner) to turn those creative skills into fast cash.

If you can generate a quick $500 from a weekend side hustle, you can instantly vaporize the first debt on your list and move your snowball to the second rung. The adrenaline of watching entire accounts disappear is what keeps you going during the long haul.

When the Debt Snowball Method Backfires

The debt snowball method is highly effective, but it is not flawless. If you are not careful, this strategy can completely blow up in your face. Here is exactly when and why it backfires:

1. The Phantom Debt Trap

You pay off the Macy’s card. You feel amazing. A month later, your car needs new tires, and because you don’t have a cash reserve, you put the $600 charge right back on the Macy’s card. You have just reversed your progress. Before starting the debt snowball method, you must have a basic cash buffer. Read up on Emergency Fund Basics: How Much Cash Should You Keep? so you never have to swipe a card for an emergency again.

2. Dealing with Predatory 29% APRs

I am a die-hard advocate for ignoring interest rates and focusing on balances, but there is one mathematical exception. If your largest debt has an absurdly high penalty APR (like 29.99%) and the interest charges are literally making the balance grow faster than your minimum payments, the debt snowball method might stall out. The math will outpace your psychology.

In this specific scenario, you need a defensive strategy. You should look into transferring that specific high-interest balance to a promotional card. As explained in How 0% APR Balance Transfers Work — And When They’re Worth It, you can pay a flat 3% fee to freeze the interest for 15 to 21 months. Once that toxic interest is paused, you go right back to executing the debt snowball method on your smaller cards, knowing your largest debt isn’t actively working against you in the background.

3. Stopping After the First Win

The first account is always the easiest to pay off. When you get to Target 3 or Target 4, the balances are much larger, and the dopamine hits are spread further apart. Many people lose focus here. You have to treat the rolled-over payments as non-negotiable fixed expenses. If you lower your payment amount just because you “feel like taking a break,” the debt snowball method collapses.

Frequently Asked Questions (FAQs)

How long does the debt snowball method take?

The timeline depends on your balances, interest rates, and monthly payments. Some people eliminate smaller debts within months, while larger debt payoffs can take several years.

Does the debt snowball method hurt your credit score?

No. Making on-time payments and reducing balances generally helps credit over time.

Is debt snowball better than debt avalanche?

Neither is universally better. Snowball emphasizes motivation and momentum, while avalanche minimizes interest costs.

Should I close credit cards after paying them off?

Not necessarily. Keeping older accounts open can help maintain your credit history and utilization ratio.

References & Trusted Sources

For further reading and official guidance on managing consumer debt, explore these trusted financial resources:

- Consumer Financial Protection Bureau (CFPB) – Credit Card Debt Resources

- Federal Trade Commission (FTC) – Dealing with Debt

- National Foundation for Credit Counseling (NFCC) – Debt Management Guidance

- Consumer Financial Protection Bureau (CFPB) – Credit Card Interest and Fees

The Bottom Line

Getting out of debt requires intense, sustained momentum. The debt snowball method provides immediate, undeniable evidence that your sacrifices are working.

The day you log into your banking portal and see a balance hit $0.00, it permanently rewires your brain. You stop feeling like a victim of compounding interest and start feeling like an operator in control of your cash flow. Once your balances are gone, your next priority should be building credit responsibly and avoiding future debt cycles by understanding exactly what credit utilization is—and why it matters.

If you are tired of the math beating you up every month, the debt snowball method is the circuit breaker you need. Stop trying to spread your extra money evenly, get your smallest balance written down on a piece of paper, and commit to crushing it this week.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

8 Comments

Comments are closed.