What To Do If Medical Bills Are Destroying Your Budget

You go to the mailbox, flip through a stack of grocery flyers, and there it is. The envelope from the hospital.

Your stomach instantly drops. You tear it open, unfolding three pages of confusing medical jargon, only to let your eyes dart straight to the bottom right corner. The “Amount Due” says $4,350.

A wave of heat washes over you. You are already stretching every single dollar just to cover rent, utilities, and groceries. You might be a freelance video editor staring at your screen, waiting on three different clients to pay their invoices from last month just so you can make your car payment. You simply do not have four thousand dollars lying around.

The panic sets in. You wonder if they are going to sue you. You wonder if your credit score is about to plummet. You might even feel a deep sense of shame, as if getting sick or injured was somehow a financial failure on your part.

Let me stop you right there. Take a deep breath.

Medical debt is not like consumer debt. You did not go to the mall and swipe a credit card for a luxury vacation you couldn’t afford. You experienced a human emergency in a country with one of the most notoriously confusing, expensive healthcare systems in the developed world.

Getting a massive hospital bill does not mean you are bad with money. It means you are dealing with a complex healthcare billing system that many consumers find difficult to navigate. But just because the system is complex does not mean you have to let it bankrupt you.

Quick Answer If medical bills are destroying your budget, don’t put them on a credit card. Request an itemized bill, apply for hospital financial assistance programs, negotiate discounts, and set up an interest-free payment plan. Medical debt is often more flexible and negotiable than most people realize.

Today, we are going to take the fear and mystery out of medical billing. We are going to look at exactly how hospitals price their services, the common mistakes people make out of pure panic, and the actual, realistic steps you can take to slash that bill down to size and protect your budget.

Why Medical Bills Are Destroying Your Budget

To understand how to fight a medical bill, you first have to understand why it is so insanely high to begin with.

Many people assume that if they have health insurance, they are protected. But over the last decade, High Deductible Health Plans (HDHPs) have become the standard. You might pay hundreds of dollars a month just to have the insurance policy, but your insurance company won’t actually pay a dime for your care until you hit a $5,000 or $8,000 deductible.

This creates a brutal reality for normal, working-class Americans. You are essentially self-pay for all routine and minor emergency care, yet you are locked into the inflated pricing structures designed for massive insurance corporations.

The Scale of the Problem According to the Consumer Financial Protection Bureau (CFPB), medical debt has historically been one of the most common sources of debt sent to collections in the United States. If you are struggling with this, you are part of a massive national trend, not an isolated failure.

When you get a bill that is destroying your budget, the real problem is a cash-flow mismatch. Hospitals price their services assuming they are going to be negotiating with a multi-billion-dollar insurance company. They start the opening bid astronomically high because they expect the insurance company to automatically slash the price by 60%.

But when that bill falls to you—the individual patient who hasn’t met their deductible yet—you are suddenly being asked to pay the inflated “opening bid” price. It is completely unrealistic, and the hospital billing departments actually know this. They just don’t advertise it.

Why It Happens: The Element of Surprise

In almost every other area of your financial life, you know the price of something before you buy it. You check the price of eggs at the grocery store. You look at the monthly rent before you sign a lease.

Healthcare is the only industry where you consume the service first and find out the price weeks or months later.

This element of surprise is exactly why medical bills destroy budgets. You cannot plan for a broken arm. You cannot budget for an unexpected appendectomy. (This is precisely why building a cash buffer is so critical once you get back on your feet—read our guide on Emergency Fund Explained for a realistic breakdown).

Furthermore, the billing process itself is highly fragmented. If you go to the emergency room, you might assume you will get one bill from the hospital. Instead, you get a bill from the facility, a separate bill from the emergency room physician (who happens to be an independent contractor), a bill from the radiology department for your X-ray, and a bill from the laboratory that ran your bloodwork.

Suddenly, you are trying to juggle four different invoices from four different billing departments, all with different due dates. It is overwhelming by design. When people get overwhelmed, they freeze. And when they freeze, they miss their window to negotiate.

What If You Have Health Insurance But The Claim Was Denied?

Before we look at common mistakes, we have to address a massive real-world scenario: you actually have good health insurance, but they simply refused to pay the bill.

Insurance claim denials happen constantly, often over simple clerical errors. Do not accept a denial as the final answer.

- Request the Explanation of Benefits (EOB): This is a document from your insurance company explaining exactly why they denied the claim. It might be a simple coding error by the hospital, or they might claim the procedure wasn’t “medically necessary.”

- Appeal the Denial: You have the legal right to appeal an insurance denial. Call your insurance provider and ask for the exact steps to file a formal appeal. Often, simply having your doctor write a letter of medical necessity will overturn the denial.

- Ask the Hospital to Pause Billing: While you are fighting with your insurance company, call the hospital’s billing department. Tell them, “My insurance company improperly denied this claim and I am currently in the appeals process. I need you to place a hold on my account and pause all billing for 60 days.”

The Panic Trap: Common Mistakes to Avoid

When that massive bill arrives and the anxiety spikes, it is very easy to make reactive decisions. If you take away nothing else from this article, please avoid these three incredibly common mistakes that turn a temporary billing headache into a permanent financial disaster.

Mistake 1: Putting the Bill on a Regular Credit Card

This is the single most dangerous thing you can do. Let’s say you get a $2,000 hospital bill. You are terrified of it going to collections, so you log into your portal and pay the entire thing with your Visa or Mastercard.

You just made a fatal financial error. You took a debt that legally carries 0% interest (the hospital bill) and transferred it to a debt that carries 25% interest (your credit card).

Hospitals are incredibly slow to act. They do not charge late fees in the same way consumer banks do. By moving that balance to a credit card, you have instantly forfeited your right to negotiate the price down with the hospital, you have lost your ability to apply for charity care, and you have guaranteed that you will pay hundreds of dollars in unnecessary interest.

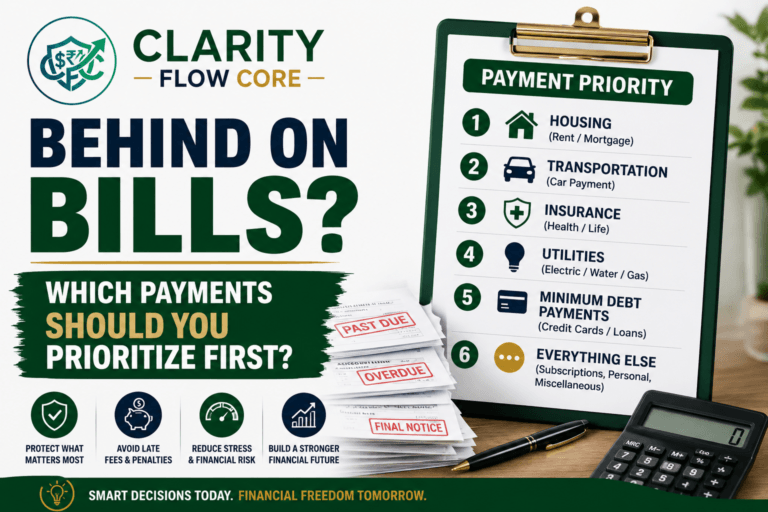

If you are already struggling with your monthly minimums, read our guide on Behind on Bills? Which Payments Should You Prioritize First? to understand why medical debt should always sit at the absolute bottom of your priority list.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyMistake 2: Signing Up for a Medical Credit Card Blindly

When you tell a front desk receptionist or a billing department that you can’t afford the bill, they will almost always hand you a glossy brochure for a medical credit card, like CareCredit. They will pitch it as a “0% interest for 12 months” payment plan.

It sounds like a lifeline, but these cards often use something called “deferred interest.”

If you charge $3,000 to one of these cards and pay off $2,950 by the end of the 12-month promotional period, you might think you only owe interest on that remaining $50. You would be wrong. With deferred interest, if you leave even one single penny unpaid when the promotion expires, they will retroactively hit you with 26% interest on the entire original $3,000 balance going all the way back to day one.

Never sign up for a third-party medical financing card unless you are absolutely, 100% certain you can pay the balance in full before the promotional period ends.

Mistake 3: Ignoring the Mail Until it Hits Collections

Avoidance is a powerful coping mechanism. When you don’t have the money, throwing the hospital bills in a drawer feels safer than looking at them.

While you should never rush to put a hospital bill on a credit card, you also cannot ignore it forever. If you ghost the billing department for 120 to 180 days, they will eventually give up and sell your account to a third-party debt collection agency.

Once your bill is with a debt collector, your options shrink dramatically. The hospital’s financial assistance programs will no longer apply to you, and you will have to deal with aggressive collection tactics. If you are already at this stage, read How To Handle Debt Collectors Without Making Things Worse.

Real Consequences: What Actually Happens If You Can’t Pay?

So, what is the actual worst-case scenario? If you simply do not have the money, what happens?

For decades, unpaid medical bills destroyed credit scores. However, the three major credit bureaus (Equifax, Experian, and TransUnion) recently changed their rules to offer massive protections for consumers.

Here is the reality of medical debt consequences today:

- Under $500: Unpaid medical collections under $500 will no longer appear on your credit report at all. Ever. If your bill is $450, it legally cannot impact your credit score.

- The One-Year Grace Period: Medical debt cannot be reported to the credit bureaus until it has been in collections for a full 365 days. You have a massive one-year window to resolve the issue before your credit score takes a hit.

- Paid Debt is Erased: In the past, if a medical bill went to collections and you eventually paid it, that negative mark stayed on your credit report for seven years. Today, the moment you pay a medical collection, it is completely erased from your credit history.

Medical debt is the most forgiving type of debt in America. Do not sacrifice your rent, your groceries, or your sanity for a hospital bill.

Practical Solutions: How to Fight Back and Win

Now that we have removed the panic, let’s talk strategy. When a massive medical bill hits your mailbox, you are going to treat it like a business negotiation. Here is exactly how to shrink that bill down to a number your budget can actually handle.

Step 1: Demand an Itemized Bill with CPT Codes

The first bill you receive from a hospital is usually a summary. It will just say “Emergency Room Services: $3,500.”

Never pay a summary bill.

Call the billing department and say this exactly: “I am reviewing my account and I need you to send me a fully itemized bill that includes the CPT billing codes for every single charge.”

CPT (Current Procedural Terminology) codes are the universal language of medical billing. Every single band-aid, Tylenol, and minute of a doctor’s time has a specific code.

Why do you want this? Medical billing errors are common enough that consumer advocates routinely recommend reviewing itemized bills for mistakes. When you get the itemized bill, review it like a detective:

- Did they charge you for a medication you refused?

- Did they charge you for a full overnight stay when you were only in a bed for four hours?

- Did they “upcode” your visit? (For example, charging you for a Level 5 severe emergency when you just had a minor cut that required three stitches).

If you see anything suspicious, call them back and dispute the specific line item. Simply asking for the itemized bill often prompts the billing department to automatically review and reduce the charges before they even mail it to you.

Step 2: Hunt Down the Charity Care Application

This is the biggest secret in the American healthcare system.

By law, under Section 501(r) of the Affordable Care Act, non-profit hospitals must offer financial assistance programs (often called “Charity Care”) to keep their tax-exempt status.

These programs are not just for the unemployed. Depending on your state and the specific hospital, you might qualify for massive discounts—or total bill forgiveness—even if you make $60,000 or $80,000 a year, especially if you have dependents.

Hospitals do not advertise this. You have to hunt for it. Go to the hospital’s website and scroll all the way down to the tiny links in the footer. Look for “Financial Assistance,” “Patient Resources,” or “Charity Care.”

Download the application. It will require you to submit your tax returns and recent pay stubs to prove your income. (If you are facing these medical bills because you recently lost your income, this step is absolutely critical. For more immediate survival steps, check out I Lost My Job: A 30-Day Financial Survival Plan).

If you qualify, the hospital will legally wipe away 50%, 80%, or even 100% of your bill. Always apply for this before you ever offer them a dime of your own money.

Step 3: Negotiate the “Self-Pay” or “Medicare” Rate

If you don’t qualify for Charity Care, it is time to negotiate.

Remember how we talked about the hospital’s inflated “opening bid”? If you do not have insurance, or if your insurance denied the claim, you should never pay that sticker price.

Call the billing department and say: “I am paying entirely out of pocket for this, and I cannot afford the current balance. What is your self-pay discount?”

Most hospitals have an automatic 20% to 40% discount they will apply immediately if you just ask.

If you want to be more aggressive, look up what Medicare pays for that specific CPT code. Medicare rates are publicly available online and represent a fair, baseline cost for medical procedures. You can tell the billing department: “I see that Medicare reimburses $400 for this procedure. I am willing to pay you $500 in cash today to settle this account in full.”

They might say no, but they will almost always counteroffer with a significantly reduced number.

Step 4: Demand a 0% Interest Payment Plan

If you have knocked the price down as far as it will go, and you still can’t afford to pay it in one lump sum, do not reach for your credit card.

Tell the hospital you need to set up a payment plan. Almost every hospital in the country will allow you to break your bill into monthly installments, completely interest-free, for anywhere from 12 to 36 months.

Do not let them dictate the terms. If they say, “We need $200 a month,” and you look at your budget and realize you only have $45, you hold your ground. “I have reviewed my finances, and I can commit to paying $45 a month on the 15th of every month. That is the maximum my budget allows.”

Hospitals want cash flow. They would much rather accept $45 a month from a cooperative patient than spend money sending your account to a collections agency that will take a 30% cut of whatever they recover.

Your Beginner-Friendly Action Plan

If you have a scary medical bill sitting on your kitchen table right now, here is exactly what you are going to do this week.

The Medical Bill Defense Checklist

- Step 1: Do NOT pay it with a credit card. Keep your cash exactly where it is.

- Step 2: Call the billing department and request a fully itemized bill with CPT codes.

- Step 3: Go to the hospital’s website and print out the Financial Assistance / Charity Care application.

- Step 4: Fill out the application, attach your income proof, and mail it in. (The billing process pauses while they review your application).

- Step 5: If denied, call the billing department and ask for the “self-pay discount.”

- Step 6: Set up a 0% interest payment plan based entirely on what you can afford, not what they ask for.

Frequently Asked Questions (FAQs)

Can medical debt hurt my credit score? It can, but recent rule changes have made it much harder. Unpaid medical collections under $500 are no longer reported to credit bureaus at all. Furthermore, medical debt cannot be reported until it has been in collections for a full year (365 days), giving you a massive grace period. Finally, if a medical collection does hit your report, it will be completely erased the moment you pay it off.

Can I go to jail for not paying a medical bill? Absolutely not. There is no such thing as debtor’s prison in the United States. Unpaid medical bills are a civil matter, not a criminal one.

What is the No Surprises Act? Enacted in 2022, this federal law protects you from unexpected out-of-network bills. For example, if you go to an in-network hospital for surgery, but the anesthesiologist happens to be out-of-network, they can no longer send you a massive surprise bill for the difference. If you receive a surprise out-of-network bill from an emergency room visit, dispute it immediately citing the No Surprises Act.

Should I hire a medical billing advocate? If your bill is massive (e.g., $50,000+) and you are completely overwhelmed, hiring a professional medical billing advocate can be worth it. They are experts who audit your bill for coding errors and negotiate with the hospital on your behalf. They usually charge an hourly fee or take a percentage of the money they save you. However, for bills under a few thousand dollars, you can usually handle the negotiation yourself using the steps above.

What do I do if the bill is already in collections? If the hospital has already sold the debt, you now negotiate directly with the collection agency. Ask them for “debt validation” in writing to prove you actually owe the money. Because collection agencies buy debt for pennies on the dollar, they are highly motivated to settle. You can often offer them 30% or 40% of the total balance to settle the debt permanently in a single lump sum.

A Final Word on Your Health and Wealth

When you are stressed about money, it bleeds into every other aspect of your life. It ruins your sleep, it strains your relationships, and it makes it incredibly difficult to focus on your work or your side hustles.

But you have to keep a clear head. Medical bills are highly negotiable, highly prone to errors, and carry the absolute lowest consequence of any type of debt in America.

Do not let a hospital’s automated billing system dictate your family’s financial stability. Protect your four walls—your housing, your food, your utilities, and your transportation. Review your bills with a critical eye, ask for financial assistance, and advocate for yourself over the phone.

Medical billing can feel confusing and overwhelming, but understanding your options can help you regain control. Take it one phone call, and one itemized line, at a time.

Patient Resources & Financial Assistance

If you’re dealing with unexpected medical bills, these trusted organizations provide guidance on billing rights, financial assistance programs, insurance appeals, and consumer protections.

- Consumer Financial Protection Bureau (CFPB) – Learn about medical debt, debt collection protections, and your rights as a consumer.

- Centers for Medicare & Medicaid Services (CMS) – Information about the No Surprises Act, patient protections, and healthcare billing requirements.

- U.S. Department of Health & Human Services (HHS) – Find resources explaining the No Surprises Act, medical billing protections, and dispute resolution options.

- Consumer Financial Protection Bureau (CFPB) – Medical debt collection resources and consumer guidance.

- Healthcare.gov – Learn about health insurance coverage, Marketplace plans, and financial assistance programs that may help reduce future medical expenses.

- National Association of Healthcare Advocacy Consultants (NAHAC) – Find professional patient advocates who can help review medical bills, resolve billing disputes, and negotiate healthcare charges.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.