How Long Does It Really Take To Rebuild Bad Credit?

Imagine this scenario: You finally found the perfect apartment. It has great natural light, it is close to your job, and it fits your budget perfectly. You submit the application, pay the non-refundable background check fee, and wait. A day later, the property manager calls and says the words you have been dreading: “We would love to have you, but your credit score didn’t meet our minimum requirements.”

Your stomach drops. You pull up your banking app, check your free credit score dashboard, and stare at a number somewhere in the 500s.

It is a terrible, heavy feeling. Seeing a low credit score makes you feel embarrassed, trapped, and entirely financially behind. Whether you experienced a sudden medical emergency, went through a period of unemployment, or maybe you are a freelance video editor whose biggest client paid an invoice 60 days late, the reality is exactly the same: the math simply didn’t work that month, and your credit score took the direct hit.

The first question everyone asks in this moment of panic is: How long is this going to ruin my life? How long does it actually take to rebuild bad credit?

If you are currently stressing over a low three-digit number, take a deep breath. You are not alone, you are not a failure, and this is absolutely not a life sentence.

Quick Answer

Most people can start seeing credit score improvements within 30 to 90 days if they lower credit card balances and make all payments on time. Significant recovery often takes 6 to 24 months, while major negative marks such as collections, charge-offs, foreclosures, and bankruptcies can remain on a credit report for 7 to 10 years.

Today, we are going to cut through the confusing, corporate financial jargon. We will break down exactly how long negative marks actually stay on your report, the realistic timelines for recovery, the dangerous mistakes to avoid, and the actionable steps you can take starting today to fix it.

The Real Problem: The Mystery of the Credit Algorithm

Before we talk about the exact timeline to fix your credit, we need to talk about why the credit system feels so incredibly frustrating to begin with.

The real problem with rebuilding credit is that the system operates in the shadows. While the exact scoring formulas are proprietary, the major factors that influence credit scores are well documented. However, because they don’t hand you a simple, transparent formula, it breeds anxiety.

When you do not know how something works, your brain assumes the worst-case scenario. You might think that a single missed payment means you will never be able to buy a house, or that a car repossession will brand you as a financial outcast forever. This lack of transparency makes you feel powerless.

Why We Fall Behind: The Myth of Irresponsibility

There is a toxic narrative in the personal finance world that having bad credit means you are irresponsible, lazy, or simply “bad with money.”

Let’s shatter that myth right now.

In the real world, the vast majority of people with bad credit are hardworking normal people who simply ran out of financial runway. Life is wildly unpredictable and incredibly expensive in the US.

If you work a traditional job and your hours get unexpectedly cut, your income drops instantly, but your rent and credit card minimums stay exactly the same. If you are a freelancer or a side hustler, dealing with a wildly variable income is just part of the job. You might have thousands of dollars owed to you in outstanding invoices, but if the cash hasn’t hit your checking account by the 15th of the month, you cannot pay your Visa bill.

Other common culprits include high-deductible health insurance plans that leave you with massive out-of-pocket bills. (If this sounds familiar, our guide on What To Do If Medical Bills Are Destroying Your Budget can help you navigate it).

When you do not have a massive cash emergency fund to act as a buffer, you are forced to make impossible choices. If you are in this exact situation right now, check out Behind on Bills? Which Payments Should You Prioritize First?. You pay the rent to keep a roof over your head, and you let the credit card payment slide. It is a survival mechanism, not irresponsibility.

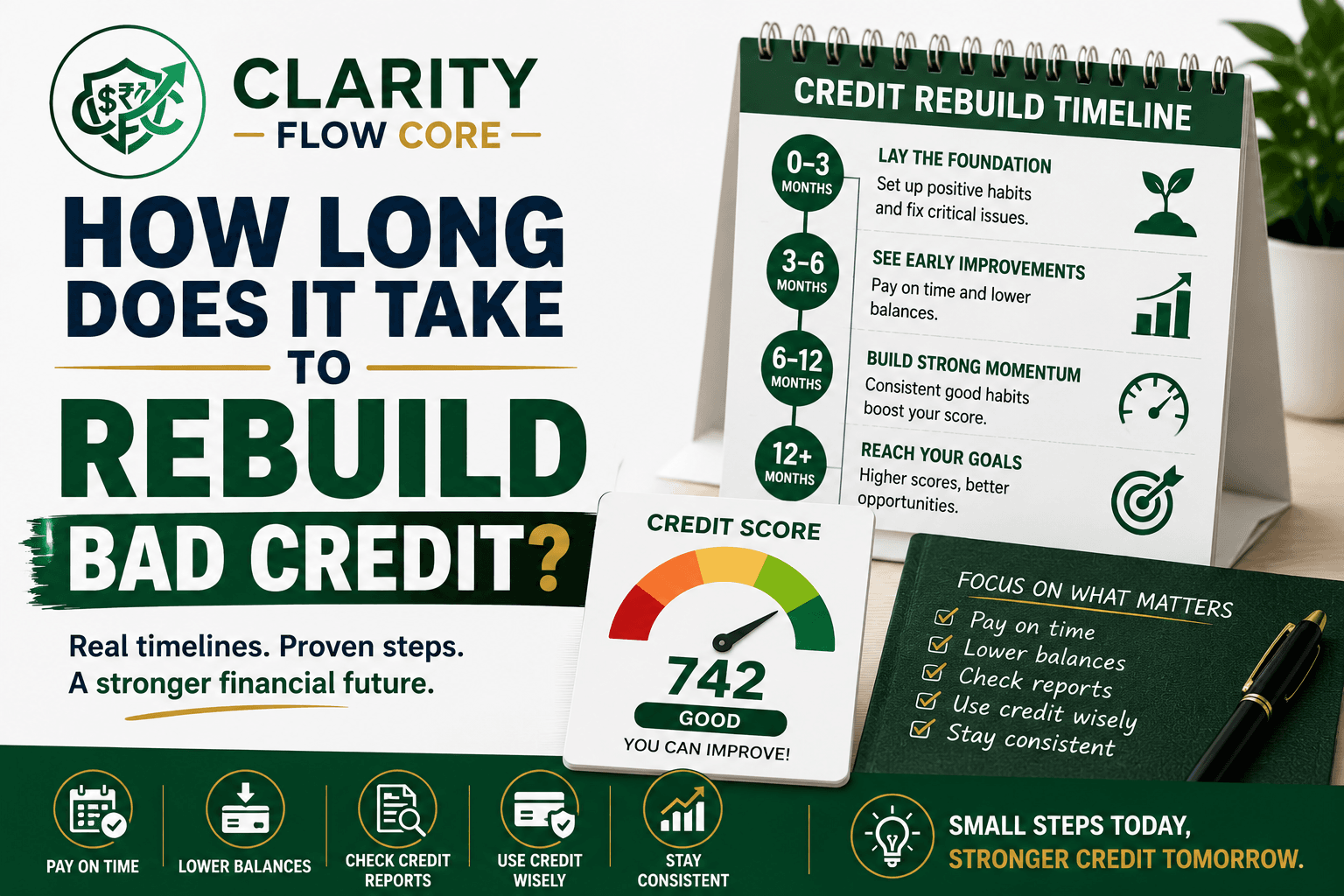

How Long Does It Take To Rebuild Bad Credit?

This is the question that matters most. Rebuilding is not a one-size-fits-all timeline. The speed at which your score increases depends entirely on what dragged it down in the first place.

If high credit utilization (maxed-out credit cards) is your main issue, you may see meaningful improvement within 30 to 60 days after lowering your balances. Because credit card companies report to the bureaus every month, paying down debt offers the fastest potential score boost.

However, more severe issues such as collections, charge-offs, and bankruptcies typically require longer recovery periods. It takes time to bury those negative marks under a mountain of fresh, positive payment history.

Here is a realistic look at how long it takes to recover from various financial setbacks:

| Credit Issue | Typical Recovery Time |

| High Credit Utilization | 1–3 Months |

| Single Late Payment | 6–12 Months |

| Collections | 1–2 Years |

| Charge-Off | 2–4 Years |

| Repossession | 2–5 Years |

| Foreclosure | 3–7 Years |

| Bankruptcy | 3–10 Years |

What Is Considered a Good Credit Score Again?

If you are starting from the bottom, it helps to know exactly what the finish line looks like. While scoring models vary slightly, many lenders consider the following FICO ranges:

- 300–579: Poor

- 580–669: Fair

- 670–739: Good

- 740–799: Very Good

- 800–850: Excellent

Rebuilding from the poor or fair range into the good range is often a realistic goal within 12 to 24 months of consistent positive behavior. You do not need a perfect 850 to secure a great interest rate—hitting that “Good” or “Very Good” tier is exactly where you want to be.

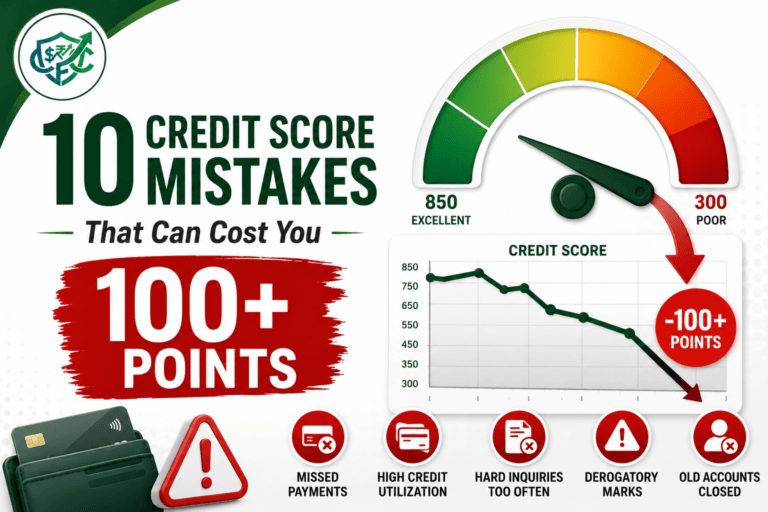

The Panic Trap: Common Mistakes That Reset the Clock

When you realize your credit score is in the tank, panic takes the steering wheel. You want to fix it yesterday. Unfortunately, reacting out of fear almost always leads to decisions that make the problem significantly worse, delaying your timeline to recovery.

If you are actively trying to rebuild your credit, avoid these common traps at all costs.

Mistake 1: Falling for “Quick Fix” Credit Repair Scams

If you search online for ways to fix your credit, you will instantly be bombarded with advertisements from companies promising to “erase bad credit overnight” or “boost your score by 100 points in 30 days.” Do not give these companies a single dime.

Legitimate, accurate negative information (like a payment you actually missed) cannot be magically legally erased by a third party before its expiration date. These predatory companies charge hundreds of dollars for basic dispute letters that you can easily write yourself for free.

Mistake 2: Closing Old, Past-Due Accounts Out of Spite

Let’s say you finally pay off a credit card that caused you endless stress and late fees. Your first instinct is to call the bank, yell at customer service, and close the account forever.

Closing the account actually hurts you in two different ways. First, it completely wipes out a chunk of your available credit limit, which instantly spikes your credit utilization ratio. Second, it eventually reduces the average age of your credit history. Keep the card open, cut the physical plastic card in half with scissors, and throw it in the trash. Let the zero balance work in your favor.

Mistake 3: Applying for “Bad Credit” Loans in a Panic

When your score is low, traditional banks will reject you. In a moment of desperation, you might start applying for payday loans, title loans, or subprime credit cards with exorbitant annual fees and 35% interest rates. Not only do these applications trigger “hard inquiries” that drop your score further, but they trap you in a high-interest cycle that virtually guarantees you will miss another payment in the future.

The Cold Hard Facts: How Long Do Negative Marks Actually Stay?

Rebuilding credit is a marathon. The Fair Credit Reporting Act (FCRA) dictates exactly how long negative information is legally allowed to haunt your credit report. Here is the official timeline for when things naturally “fall off” and disappear from your record completely.

Late Payments: 7 Years

If you go 30, 60, or 90 days late on a payment, that derogatory mark stays on your credit report for seven years from the original delinquency date. Even if you eventually pay the account in full, the record of the late payment remains for the full seven years.

Collections and Charge-Offs: 7 Years

If you ignore a debt long enough that the original lender writes it off as a loss (a charge-off) or sells it to a third-party debt collector, that mark stays for seven years from the date of your first missed payment that led to the default. (If you are dealing with debt collectors right now, it is critical to know your rights. Read How To Handle Debt Collectors Without Making Things Worse).

Foreclosures: 7 Years

If you lose your home because you were unable to keep up with mortgage payments (learn more about What Happens If You Miss a Mortgage Payment?), a foreclosure will remain on your credit history for seven years from the original delinquency date.

Bankruptcies: 7 to 10 Years

The timeline for bankruptcy depends entirely on the type of protection you filed for. A Chapter 13 bankruptcy, which involves a structured repayment plan to your creditors, expires from your report after seven years. A Chapter 7 bankruptcy, which involves the total liquidation of assets and discharge of debts, is the most severe mark and remains on your credit report for a full 10 years from the filing date.

The Secret Saving Grace: Impact Fades Over Time

If you just read that list and your heart sank at the phrase “seven years,” please read this next sentence very carefully.

You do not have to wait seven years to have good credit again.

The most important, least-talked-about secret in the credit industry is the concept of “time decay.” While a negative mark legally stays on your physical report for seven years, the impact of that negative information on your actual three-digit score decreases significantly as time passes.

A 60-day late payment that happened last month will absolutely tank your score. But that exact same late payment sitting on your report three years from now will have a much smaller effect. The credit algorithms care vastly more about what you have done recently than what you did half a decade ago.

Practical Solutions: The Mechanics of Rebuilding

Now that we know the timelines, how do we actually speed up the recovery process? We focus on the things we can control today.

Credit scores are simply mathematical reflections of your current behavior. If you want a better score, you have to feed the algorithm better data. Here are the most impactful, realistic ways to do that.

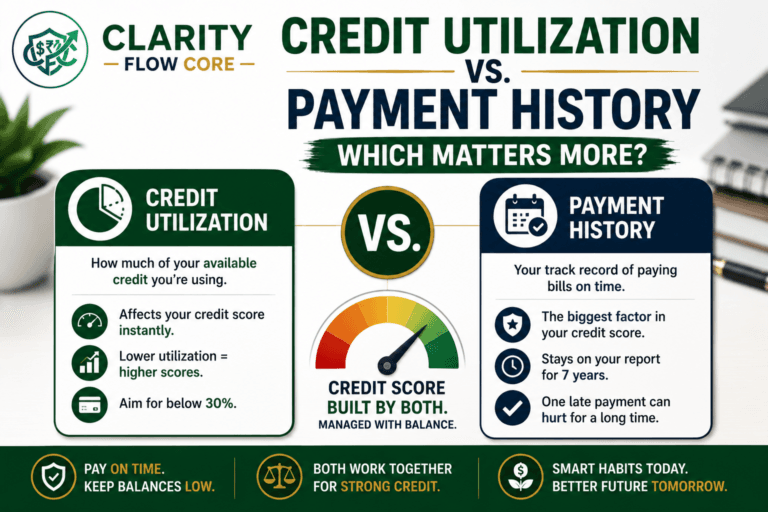

1. Master Your Credit Utilization (The Fastest Fix)

If you want to see a rapid jump in your credit score within a few months, this is where you focus.

Your credit utilization ratio makes up a massive 30% of your total FICO score. It is a simple math equation: how much total credit do you have available across all your cards, versus how much of it are you currently using?

For example, if you have one credit card with a $1,000 limit, and your current balance is $900, your utilization is at 90%. The credit bureaus view anyone utilizing more than 30% of their available credit as a high-risk borrower.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyUse our Credit Utilization Calculator to see how reducing balances could impact your credit profile.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationTo rebuild your credit rapidly, you need to aggressively pay down your existing balances. Getting your overall utilization under 30% will help your score; driving it under 10% will supercharge it. Because lenders report your balances to the credit bureaus roughly every 30 days, improving your utilization is one of the only ways to see a score increase in a matter of weeks.

2. Establish a Flawless Payment History

Payment history is the undisputed king of your credit score, making up 35% of the total calculation.

If you are trying to rebuild, you simply cannot afford to miss another payment. Ever. Even if you can only afford to scrape together the $25 minimum payment, you must send it in before the due date. Consistent, on-time payments are the only way to bury your old negative marks under a mountain of fresh, positive data.

3. Use a Secured Credit Card to Build Fresh Data

If your score is so low that absolutely no traditional bank will approve you for a regular credit card, you need a stepping stone.

A secured credit card is the ultimate rebuilding tool. It works like this: you put down a refundable cash deposit (usually $200 to $500), and that deposit becomes your credit limit. Because the bank is holding your cash as collateral, there is almost zero risk for them, meaning they will approve almost anyone, regardless of how bad their credit history is.

You use the secured card just like a regular card—buy groceries, put gas in the car—and pay the balance off in full, every single month. The bank reports this responsible behavior to the credit bureaus, generating fresh, positive payment history that actively repairs your score.

If you’re ready to open a secured card, Best Secured Credit Cards for Beginners in 2026 compares the best options based on security deposits, annual fees, graduation policies, and overall credit-building value.

Your Beginner-Friendly Action Plan

Reading about credit strategy is great, but taking physical action is what changes your life. If you are ready to rebuild, here is your step-by-step checklist to execute this week.

Step 1: Face the Music and Pull Your Reports

You cannot fix what you cannot see. Go to AnnualCreditReport.com (the only federally authorized site for this) and download your free reports from Equifax, Experian, and TransUnion. Do not pay for a subscription service; just get the free statutory reports.

Step 2: Hunt for Errors and Dispute Them

Comb through your reports with a highlighter. Look for accounts you do not recognize, late payments you know you paid on time, or debts that are listed twice. Credit bureaus make mistakes constantly. If you find an inaccuracy, use the bureau’s online portal to file a formal dispute. If they cannot verify the negative mark, they are legally required to delete it.

Step 3: Automate the Minimums

To protect your 35% payment history factor, log into your banking app right now and set up automatic payments for the minimum due amount on every single one of your debts. This ensures that no matter how chaotic your life gets, you will never accidentally trigger a 30-day late mark again.

Step 4: Attack the Balances

Pause all non-essential spending. Cancel the subscriptions, stop eating out, and throw every spare dollar you have at your credit card balances to drive your utilization ratio down below 30%.

Frequently Asked Questions (FAQs)

Can a credit score recover after a charge-off?

Yes. A charge-off remains on your credit report for up to seven years, but its impact decreases over time. Consistent on-time payments, lower credit utilization, and positive new credit activity can help your score recover long before the charge-off disappears.

Does checking my own credit score lower it?

No. Checking your own credit score or pulling your own credit report is considered a “soft inquiry.” It has absolutely zero impact on your credit score, no matter how many times you check it. You should monitor it regularly.

Can I pay to have accurate negative marks removed early?

No. If a late payment or a collection is 100% accurate, no company can magically force the credit bureaus to remove it before the seven-year timeline is up. Any company promising to do this is lying to you.

Is it better to pay off a collection or leave it alone?

Paying a collection will update the account status to “Paid,” which looks much better to future lenders who manually review your report. Under newer credit scoring models (like FICO 9), paying off a collection account will actually stop it from negatively impacting your score. However, under older models, the paid mark still stings. Regardless, paying it prevents the debt collector from eventually suing you.

How long does it take to build credit from scratch if I have no history?

If you have a completely blank slate and have never used debt before, it typically takes about six months of consistent, reported activity (like using a secured card) to generate your very first FICO score.

A Final Word of Encouragement

Rebuilding bad credit is incredibly frustrating because it requires patience in a world that demands instant gratification. It can feel like you are pushing a boulder up a hill, trying to prove to a faceless algorithm that you are trustworthy again.

But you have to remember this: your credit score is just a math formula. It is a reflection of your past relationship with debt. It is not a reflection of your character, your intelligence, your worth as a person, or your future potential.

The negative marks currently weighing you down have an expiration date. The clock is already ticking. By taking control of your credit utilization, automating your payments, and refusing to give up, you are taking your financial power back.

It takes time, but time is going to pass anyway. You might as well spend it building a foundation that will eventually open doors for you. Stay consistent, give yourself some grace for past mistakes, and keep moving forward. You’ve got this.

Sources & References

The information in this article is based on guidance from the following authoritative sources:

- FICO® – What’s in Your FICO® Score?

- Consumer Financial Protection Bureau (CFPB) – Credit Reports and Scores

- Consumer Financial Protection Bureau (CFPB) – How do I get and read my credit reports?

- AnnualCreditReport.com – Official website authorized by federal law for free credit reports from Equifax, Experian, and TransUnion.

- Federal Trade Commission (FTC) – Repairing Your Credit

- Experian – How Long Do Negative Items Stay on a Credit Report?

- Equifax – Understanding Credit Scores and Credit Reports

- TransUnion – Credit Education Center

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.