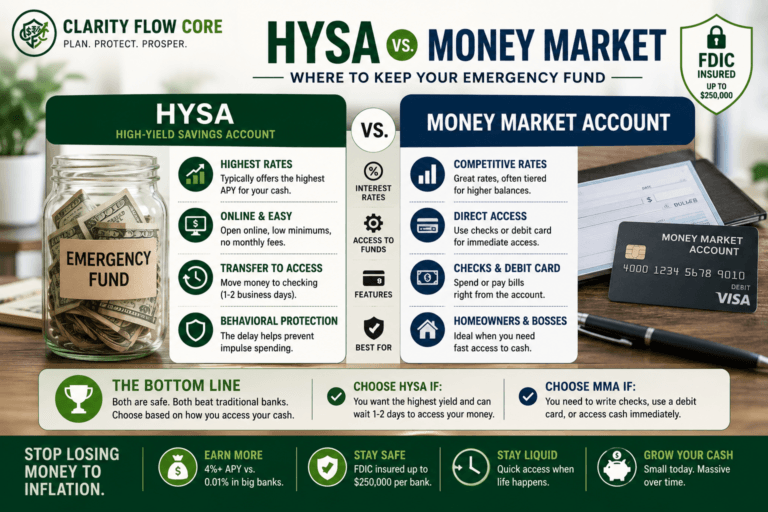

High-Yield Savings Account vs CD: Which Is Better in 2026?

You worked hard for your money, and you finally have a solid cash buffer sitting in your checking account. But keeping thousands of dollars in a standard checking account earning 0.01% interest means your money is actively losing purchasing power. You need to move it into an account that actually pays you for keeping your cash there.

When you start looking for safe, interest-bearing options, you immediately run into the classic banking debate: deciding between a high-yield savings account vs CD. Both are incredibly safe, federally insured ways to grow your cash. However, they are built for entirely different financial timelines and serve entirely different purposes.

Choosing the wrong account can either cost you hundreds of dollars in missed interest or trap your money behind expensive withdrawal penalties exactly when an emergency strikes. The economic landscape in 2026 has made cash management a priority again, and understanding the mechanical differences between these two tools is mandatory for anyone looking to optimize their savings.

This guide will break down the exact differences between a high-yield savings account and a certificate of deposit, explain the hidden math behind early withdrawal penalties, and give you a clear framework for deciding exactly where your money belongs.

⚡ Quick Answer

A high-yield savings account (HYSA) is a flexible bank account that pays an above-average interest rate but allows you to withdraw or add to your money at any time. A Certificate of Deposit (CD) requires you to lock your money away for a specific time period (like 12 or 24 months) in exchange for a fixed, guaranteed interest rate. If you need the money for an emergency, choose an HYSA. If you have a lump sum you absolutely will not need for a set period, choose a CD to lock in the rate.

To help you visualize the differences before you commit your cash, here is a breakdown of how the two accounts compare on a mechanical level:

| Feature | High-Yield Savings Account (HYSA) | Certificate of Deposit (CD) |

| Interest Rate | Variable (Changes with the market) | Fixed (Locked for the entire term) |

| Liquidity | High (Withdraw anytime) | Low (Locked until maturity date) |

| Early Withdrawal Penalty | None | Yes (Usually costs months of interest) |

| Adding Funds | Yes (Add money anytime) | No (One-time lump sum deposit) |

| Best For | Emergency funds, ongoing daily savings | Future planned purchases, rate locking |

Real-World Earnings: How Much Will You Actually Make?

To put these percentages into perspective, here is what your money would realistically earn over a 12-month period based on current market averages:

| Deposit Balance | 4.5% APY HYSA | 5.0% APY CD |

| $5,000 | ~$225 / year | ~$250 / year |

| $10,000 | ~$450 / year | ~$500 / year |

| $25,000 | ~$1,125 / year | ~$1,250 / year |

What Is a High-Yield Savings Account (HYSA)?

A high-yield savings account functions exactly like the traditional savings account you likely opened when you were a teenager, with one massive difference: the math is actually in your favor.

While big brick-and-mortar banks routinely offer a microscopic 0.01% Annual Percentage Yield (APY), high-yield accounts are primarily offered by online banks. Because these digital banks do not have to pay for thousands of physical retail branches, security guards, and tellers, their overhead is drastically lower. They take those operational savings and pass them directly to you in the form of interest rates that are often 10 to 15 times higher than the national average.

If you’ve decided an HYSA fits your needs, the next step is choosing the right one. How to Choose Your First High-Yield Savings Account explains how to compare FDIC insurance, fees, APYs, and transfer features before opening an account.

It is important to note the broader economic picture: even though HYSAs and CDs earn interest, inflation can still reduce your purchasing power if the national inflation rate exceeds your APY. However, keeping your money in a high-yield account provides the strongest defense against this slow loss of wealth.

How It Works

When you open an HYSA, you link it to your primary checking account. You can transfer money in and out whenever you want. The bank calculates your interest daily based on your account balance and pays that interest into your account at the end of every month. Your interest then begins earning its own interest, a process known as compounding.

The Pros of an HYSA

- Total Liquidity: You have immediate access to your cash. If your roof leaks or your car breaks down, you can transfer the funds to your checking account instantly (or within 1 to 2 business days) without paying a dime in penalties.

- Ongoing Contributions: You can set up automated weekly or monthly transfers to continuously build your balance.

- Zero Risk: As long as the bank is FDIC-insured (or NCUA-insured for credit unions), your money is federally protected up to $250,000. You cannot lose your principal.

The Cons of an HYSA

- Variable Interest Rates: This is the critical catch. The APY on a high-yield savings account is strictly tied to the Federal Reserve’s benchmark interest rate. If the Federal Reserve announces a rate cut on a Tuesday, your bank can legally lower your HYSA interest rate on Wednesday. For example, a 5% HYSA today could become 3.5% next year if the Federal Reserve cuts rates to stimulate the economy. You are entirely at the mercy of the broader economic market.

- Transfer Limits: While the federal regulation known as Regulation D (which limited savings account withdrawals to six per month) was paused in 2020, some banks still impose their own internal limits or fees if you treat the savings account like a daily checking account.

What Is a Certificate of Deposit (CD)?

A Certificate of Deposit is a time-bound deposit account. When you open a CD, you enter into a strict, binding contract with the bank. You agree to leave a specific lump sum of money with them for a predefined amount of time, known as the “term.” In exchange for giving up access to your cash, the bank guarantees you a specific, fixed interest rate for the entire duration of the term.

Common CD terms range from as short as 3 months to as long as 5 years.

How It Works

You deposit $5,000 into a 12-month CD offering a 5% APY. The second you click “Submit,” your money is locked. Over the next 12 months, the bank pays you interest. When the 12 months are over, the CD reaches its “maturity date.” At this point, the contract is fulfilled, and you have a brief grace period (usually 7 to 10 days) to withdraw your original $5,000 plus all the interest you earned.

The Pros of a CD

- The Rate Lock: This is the single biggest advantage of a CD. Because the rate is fixed, you are completely shielded from market volatility. If the Federal Reserve aggressively cuts interest rates, HYSA rates will plummet. Your CD rate will not budge. You get exactly what you signed up for.

- Forced Financial Discipline: Because your money is physically locked away, a CD creates artificial friction. You cannot impulsively drain your savings account to buy a new television because the money is literally inaccessible without triggering a penalty.

The Cons of a CD

- The Liquidity Trap: Life is unpredictable. If you lose your job four months into a 12-month CD term and need cash to pay rent, you cannot simply transfer the money out.

- No Additions Allowed: Once you fund a traditional CD, you cannot add more money to it. If you save an extra $500 next month, you cannot top off your existing CD; you would have to open a brand new one.

- The Early Withdrawal Penalty: If you absolutely must break the glass and access your money before the maturity date, the bank will hit you with a harsh fee.

Who Should Avoid CDs?

While locking in a high guaranteed rate sounds appealing, a CD is not for everyone. A CD may NOT be ideal if:

- You have less than 3 months of emergency savings.

- Your job income is unstable or unpredictable.

- You expect major expenses (like medical bills or auto repairs) soon.

- You frequently need to access your cash for daily living expenses.

The Math Behind Early Withdrawal Penalties

Understanding exactly what happens when you break a CD contract is vital when comparing a high-yield savings account vs CD. Banks do not want you withdrawing money early because they use your deposit to fund long-term loans for other customers. To deter you, they implement an Early Withdrawal Penalty (EWP).

The penalty is rarely a flat dollar fee. Instead, it is usually calculated as a loss of interest.

While every bank has different specific policies in their fine print, the industry standard for penalties generally looks like this:

- CD terms of 12 months or less: Penalty equals 60 to 90 days of earned interest.

- CD terms of 1 to 3 years: Penalty equals 180 days (6 months) of earned interest.

- CD terms over 3 years: Penalty equals 365 days (12 months) of earned interest.

Let’s Run the Math

Assume you deposit $10,000 into a 24-month CD with a 4.5% APY. Your bank’s policy dictates a penalty of 180 days of interest if you withdraw early.

Six months in, your furnace breaks, and you need the $10,000.

At 4.5%, your money earns roughly $37.50 per month.

After six months, you have earned $225 in interest.

You contact the bank to break the CD. The bank applies the 180-day (6-month) penalty. This means they confiscate 6 months’ worth of interest, which is $225. You get your original $10,000 back, but you walk away having earned absolutely nothing for the half-year your money was sitting in the bank.

Even worse, if you break a CD after only two months, but the penalty is six months of interest, the bank will actually eat into your principal balance to satisfy the penalty. You will walk away with less money than you originally deposited.

This is exactly why your primary safety net should never be housed in a CD. If you are unsure exactly how much cash you need completely liquid and accessible, run your numbers through the Advanced Emergency Fund Analyzer.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetHigh-Yield Savings Account vs CD: Scenario Planning

To make the right choice, you have to align the mechanical features of the account with your actual life goals. Here are the most common scenarios you will face and the optimal account for each.

Scenario 1: The Emergency Fund

The Winner: High-Yield Savings Account

Your emergency fund exists to prevent financial disaster when the unexpected happens—medical bills, sudden job loss, or major auto repairs. By definition, you do not know when an emergency will strike. Therefore, liquidity is non-negotiable. Putting an emergency fund into a CD is a massive strategic error because you risk paying steep penalties exactly when you are financially vulnerable. An HYSA keeps your cash liquid while still fighting inflation.

Scenario 2: The House Down Payment (In 2 Years)

The Winner: Certificate of Deposit (CD)

If you are aggressively saving for a down payment and you know definitively that you will not buy the house for at least 24 months, a CD is the vastly superior choice. By locking your down payment into a 2-year CD, you guarantee your rate of return. You can calculate exactly down to the penny how much interest you will have on the exact day you are ready to apply for your mortgage. If you leave that money in an HYSA, a sudden drop in federal interest rates could cost you thousands of dollars over a two-year span.

If you’re still in the earlier stages of preparing to live independently, you’ll first need to determine how much cash to accumulate before choosing where to keep it. Read How Much Should You Save Before Moving Out on Your Own? to estimate your savings target before signing a lease.

Scenario 3: Saving for Next Year’s Taxes

The Winner: High-Yield Savings Account

If you are a freelancer or side-hustler setting aside 25% of every paycheck for quarterly estimated taxes, you need an account that allows continuous deposits. Because traditional CDs only allow a single, initial lump-sum funding, they are useless for ongoing, paycheck-by-paycheck savings strategies. An HYSA allows you to constantly funnel cash in while keeping it safe for the IRS.

The Best of Both Worlds: Building a CD Ladder

If you are torn between the high, guaranteed rates of a CD and the flexible liquidity of an HYSA, the financial industry has a built-in strategy to give you both. It is called a CD Ladder.

Instead of taking a large sum of money and locking it into a single, massive CD, you break the money up and buy multiple smaller CDs with staggered maturity dates. This ensures that a portion of your money becomes liquid and available on a regular, rolling basis.

How to Build a Simple CD Ladder

Imagine you have $20,000 in cash that you want to grow, but you are nervous about locking it all away for a year. You build a ladder by dividing it into four $5,000 chunks.

- Rung 1: Buy a 3-month CD with $5,000.

- Rung 2: Buy a 6-month CD with $5,000.

- Rung 3: Buy a 9-month CD with $5,000.

- Rung 4: Buy a 12-month CD with $5,000.

Now, wait three months. When Rung 1 matures, you have a choice. If you need the cash, you take it. If you do not need the cash, you reinvest that $5,000 into a brand new 12-month CD.

Three months later, Rung 2 matures. You do the exact same thing.

Once your ladder is fully operational, you will have a 12-month CD maturing every single quarter (every three months). You are capturing the high interest rates associated with long-term 12-month CDs, but because of how you staggered them, you are never more than 90 days away from accessing a quarter of your cash without penalty.

If this level of organization sounds overwhelming, step back and map your total financial picture using the Financial Freedom Planner to see if you even have enough excess capital to justify building a ladder.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanCommon Mistakes When Choosing Between a HYSA and a CD

The mechanics of these accounts are simple, but banks rely on human error to maximize their profit margins. Avoid these frequent traps.

Mistake 1: Ignoring the Auto-Renewal Trap

When your CD reaches its maturity date, the bank does not automatically mail you a check. They give you a brief grace period (usually 7 to 10 days) to withdraw your funds. If you forget to log in and claim your money, the bank will automatically renew the CD for the exact same time period.

The trap is that they will renew it at the current market rate, which might be terrible. If you had a 5% 12-month CD, and rates have dropped, you might get auto-renewed into a 2% CD, and your money is instantly locked away for another year. You must set a calendar reminder one week before your CD matures to log in and direct the bank on what to do.

Many lesser-known online banks will advertise a massive 6% HYSA rate to get you to open an account. However, read the fine print. Often, this is a promotional “teaser rate” that only applies for the first three months, after which the rate drops down to a mediocre 1.5%. Alternatively, the high rate might only apply to the first $1,000 of your balance, while the rest earns virtually nothing. Stick to highly reputable online banks with a long history of maintaining competitive rates.

Mistake 3: Forgetting About Taxes

Whether you choose a high-yield savings account or a CD, the interest you earn is not free money. The IRS classifies bank interest as ordinary income. At the end of the year, your bank will send you a 1099-INT tax form if you earned more than $10. You must claim this on your tax return, and you will pay taxes on it at your standard income tax bracket rate. Do not let a massive tax bill surprise you in April just because you moved a large sum of cash into a 5% CD.

Action Plan: Where Should You Put Your Money Today?

Paralysis by analysis is the enemy of financial growth. Leaving your money in a zero-interest checking account because you cannot decide between a CD and an HYSA guarantees you lose money to inflation. Follow this exact operational plan to optimize your cash today.

- Secure the Baseline First: Calculate exactly how much money you need to survive for three to six months if you lost your job. That exact dollar amount is your emergency fund.

- Open the HYSA: Open a high-yield savings account with a reputable online bank. Transfer your entire emergency fund into this account. Do not put this money in a CD under any circumstances.

- Audit Your Timelines: Look at any cash you have remaining above your emergency baseline. Are you buying a car in eight months? Are you paying for a wedding next year?

- Deploy the CD: For any specific, planned expenses that are at least six months away, open a CD matching that specific timeline to lock in your interest rate and protect the cash from your own impulsive spending.

Frequently Asked Questions

Can I lose money in a high-yield savings account or a CD?

No. Both HYSAs and CDs are incredibly low-risk vehicles. As long as you open the account with a bank that is FDIC-insured (or a credit union that is NCUA-insured), your deposits are protected by the federal government up to $250,000 per depositor, per institution. The only way to lose money is if you incur an early withdrawal penalty on a CD that eats into your principal.

Are there “No-Penalty” CDs?

Yes. Some banks offer a “No-Penalty CD,” which allows you to withdraw your money before the maturity date without paying a fee. However, the catch is that the bank will offer a significantly lower interest rate on a No-Penalty CD compared to a traditional CD. Often, a standard high-yield savings account will offer a better rate than a No-Penalty CD, making them largely unnecessary for most savers.

Can I have both a high-yield savings account and a CD?

Absolutely. In fact, utilizing both is the smartest financial strategy. You should use a high-yield savings account to house your liquid emergency fund and daily savings, while simultaneously opening CDs to lock in high interest rates for specific, long-term savings goals.

Is a Money Market Account better than an HYSA?

A Money Market Account (MMA) is very similar to a high-yield savings account. It offers competitive interest rates but usually comes with debit card access and check-writing privileges, which most HYSAs do not offer. However, MMAs frequently require much higher minimum balances (often $5,000 or $10,000) to avoid monthly fees. If you meet the minimums and want check-writing ability, an MMA is great. If you just want simple, fee-free savings, an HYSA is usually better.

What happens if the bank goes out of business while I have a CD?

Because your CD is FDIC-insured, the federal government steps in immediately. Usually, the FDIC sells the failed bank to a healthy bank, and your CD simply transfers over intact. The new bank is legally obligated to honor the fixed interest rate and the original maturity date of your CD contract. You will not lose your money or your locked-in rate.

References and Resources

To ensure you are operating with the most accurate, up-to-date consumer protection information, we highly recommend verifying banking terms and insurance limits directly with the agencies that enforce them:

- Federal Deposit Insurance Corporation (FDIC): Verify that your bank is officially insured and understand exactly how the $250,000 coverage limit works across different account types. Visit the FDIC BankFind Suite.

- Consumer Financial Protection Bureau (CFPB): The CFPB offers exceptional, plain-language guides on how banking fees work and how to dispute unfair early withdrawal penalties. Visit the CFPB guide on bank accounts.

- Federal Reserve: Track the baseline federal interest rates to understand where HYSA and CD APYs are likely heading in the upcoming months. Review the Federal Reserve economic data.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.