What Credit Score Do You Need to Buy a House in 2026?

What credit score do you need to buy a house in 2026? If you’re planning to purchase a home this year, your credit score will play a major role in determining which mortgage programs you qualify for, the interest rate you’ll receive, and how much house you can realistically afford.

Let’s just clear the air right away: buying a house in 2026 is stressful enough. Between saving up a down payment while your rent keeps climbing, trying to decode real estate jargon, and constantly worrying about whether you make enough money, the mortgage process can feel like a mountain you aren’t equipped to climb. And sitting right at the trailhead of that mountain is your credit score.

It feels like a judge. It feels like a report card on your entire adult life. It can make you feel embarrassed, financially behind, or anxious that a mistake you made three years ago is going to keep you renting forever.

But here is the truth that the banking industry rarely explains in plain English: your credit score is not a reflection of your worth, and you do not need a perfect 800 to buy a house. You just need to know the rules of the game.

This guide is going to walk you through exactly what credit score you need to buy a house right now, why certain numbers matter more than others, the beginner mistakes that can accidentally ruin your approval chances, and how to get your financial profile ready for the bank—without the confusing Wall Street jargon.

The Real Problem: Why Your Credit Score Feels Like a Brick Wall

Most of us were never taught how credit actually works. We were told to “pay our bills on time,” but nobody mentioned that keeping a high balance on a credit card could drop your score by 40 points, or that closing your oldest bank account could accidentally make you look like a riskier borrower to a mortgage lender.

When you apply to get pre-approved for a mortgage, the lender is essentially trying to answer one question: If we give this person hundreds of thousands of dollars, what are the odds they will pay us back every single month for the next 30 years?

Your credit score is the mathematical shortcut they use to answer that question.

The problem is that a credit score doesn’t care about context. It doesn’t know that you missed a credit card payment because you were laid off, or that your utilization is high because you had to cover an unexpected medical emergency. It just spits out a number. And in the mortgage world, that number acts as a gatekeeper. It doesn’t just decide if you get the house; it decides exactly how much that house is going to cost you every single month.

What Credit Score Do You Need to Buy a House

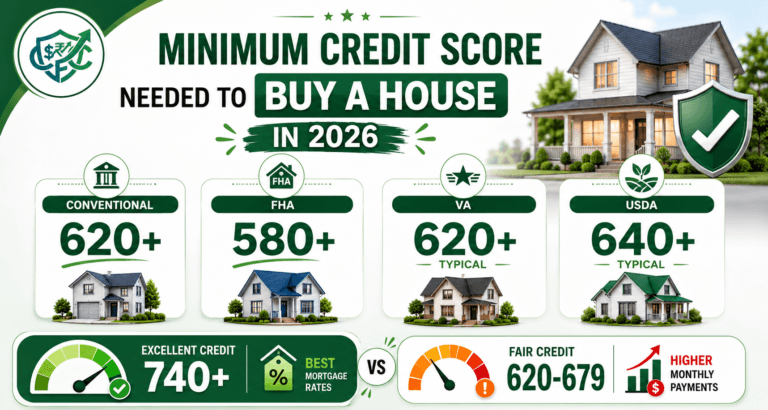

If you are just looking for the baseline numbers, here is the reality of the 2026 housing market. The minimum score you need depends entirely on the type of mortgage you are applying for.

1. Conventional Loans (The Standard Path)

- Minimum Score Needed: 620

- What it is: This is the most common type of home loan. It isn’t backed by a specific government agency, which means lenders are taking on a bit more risk.

- The Reality: While 620 is the absolute technical minimum, many lenders actually prefer to see a 650 or higher to comfortably approve a conventional loan without demanding a massive down payment. If your score is sitting right at 620, you might have to prove you have a lot of cash in the bank or an incredibly low debt-to-income ratio to make the underwriter comfortable.

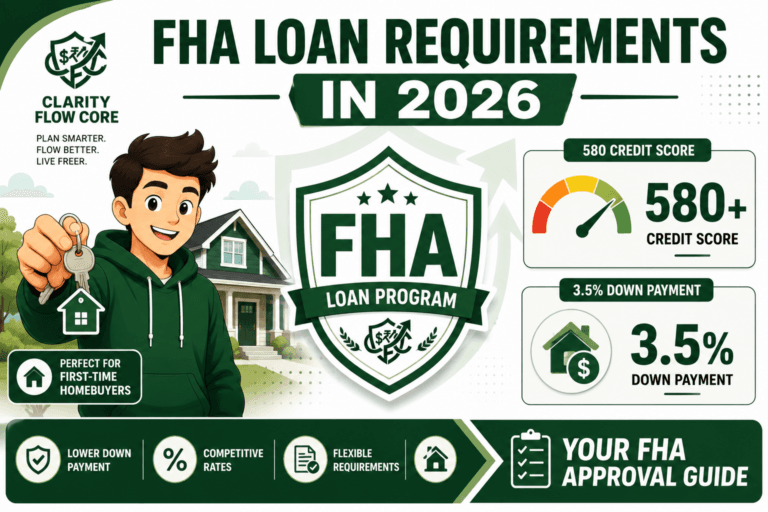

2. FHA Loans (The Beginner-Friendly Option)

- Minimum Score Needed: 580 (with a 3.5% down payment)

- What it is: Federal Housing Administration (FHA) loans are designed specifically to help people with lower credit scores or smaller savings accounts buy homes. Because the government insures the loan, the bank is willing to lower their standards.

- The Reality: You can buy a home with an FHA loan with a score of 580 and only put 3.5% down. Technically, FHA guidelines allow for a score as low as 500 if you can put 10% down. However, finding a lender in 2026 willing to write a mortgage for a 500 credit score is like finding a needle in a haystack. Most banks set their own “overlays” (internal rules) that require at least a 580 or 600 anyway.

3. VA Loans (For Veterans and Military Families)

- Minimum Score Needed: No official minimum (but usually 620)

- What it is: Backed by the Department of Veterans Affairs, this loan is an incredible benefit for eligible service members, allowing them to buy a home with 0% down and no private mortgage insurance.

- The Reality: The VA itself does not mandate a minimum credit score. However, the private lenders who actually hand you the money still want to make sure you are reliable. In practice, most lenders require a minimum score of 620 to process a VA loan, though a few specialized lenders might drop down to 580.

4. USDA Loans (The Rural Secret)

- Minimum Score Needed: No official minimum (but usually 640)

- What it is: Designed by the U.S. Department of Agriculture to encourage people to move to rural and some suburban areas. It offers 0% down.

- The Reality: Similar to the VA loan, there is no official government minimum, but most lenders use an automated underwriting system that greatly prefers a credit score of 640 or higher.

Important Takeaway: If your score is currently below 580, your best immediate move is usually to pause your home search and focus onrenting instead of buyingfor the next six to twelve months while you actively rebuild your credit profile.

Your Credit Score Isn’t the Only Number That Matters (The DTI Reality)

It is easy to read the numbers above and think, “Great, I finally hit a 620, so I am automatically approved!” Unfortunately, that is not how it works. Your credit score is just one half of the puzzle. Even with a stellar 700+ credit score, you can still be denied for a mortgage if too much of your monthly income is already committed to other debt payments.

To figure this out, lenders calculate your Debt-to-Income Ratio (DTI), which compares your mandatory monthly debt obligations (like student loans, car payments, and minimum credit card bills) against your gross monthly income.

Many conventional lenders strongly prefer a DTI below 43%, though some government-backed programs will allow higher ratios if you have other strong financial factors. If half of your paycheck is already going toward a truck payment and maxed-out credit cards, a lender is going to hesitate to add a massive mortgage payment on top of that—no matter how high your credit score is.

Before you start seriously house hunting, it is crucial to see your profile exactly how a bank will see it. Consider using our Free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner to calculate your exact DTI and find out how much house a lender might realistically approve you for.

Why Your Score Might Be Lower Than You Think (The App Illusion)

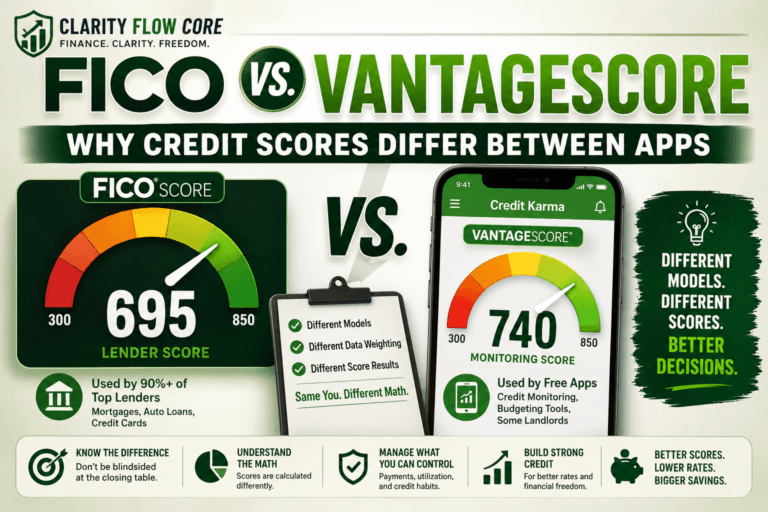

Have you ever looked at your free credit tracking app, celebrated seeing a 680, and then had a mortgage lender pull your credit only to tell you your score is actually a 640?

You didn’t do anything wrong, and the lender isn’t lying to you. You just fell victim to the most common beginner misunderstanding in personal finance: Not all credit scores are the same.

When you log into popular free apps to check your credit, you are almost always looking at your VantageScore. This is an educational score designed to give you a general idea of your financial health.

Mortgage lenders do not care about your VantageScore. They use much older, stricter scoring models—specifically FICO Score models 2, 4, and 5. These older models are notoriously harsher. They penalize you more severely for carrying credit card debt and can take longer to reflect positive changes.

When you apply for a mortgage, the lender pulls your specific mortgage FICO score from all three major credit bureaus (Experian, Equifax, and TransUnion). You will have three different numbers. The lender throws out the highest number, throws out the lowest number, and uses the middle score to determine your fate.

If you want to know where you truly stand before walking into a bank, you need to purchase your actual mortgage FICO scores directly from a consumer credit bureau.

The Financial Impact: What a Lower Score Actually Costs You

A credit score isn’t just a pass/fail grade. It is the ultimate pricing factor for your entire mortgage. Even if you qualify for the loan with a 620, the difference between having a 620 and a 740 is staggering when you look at the math.

Lenders use a system called “Loan-Level Price Adjustments” (LLPAs). Basically, the lower your score, the more extra fees and higher interest rates they tack onto your loan to offset their risk.

Let’s look at a realistic example:

Imagine you are buying a $350,000 home with a 30-year conventional mortgage.

- Buyer A (The 760 Credit Score): Because they have excellent credit, they qualify for the best interest rate—let’s say 6.5%. Their monthly principal and interest payment is about $2,212.

- Buyer B (The 630 Credit Score): Because they are considered a higher risk, the lender gives them a rate of 7.5%. Their monthly principal and interest payment is about $2,447.

Buyer B is paying $235 more every single month just because of their credit score. Over the course of a 30-year loan, Buyer B will pay roughly $84,000 more in interest for the exact same house.

This is exactly why figuring out how much house you can afford requires looking at your credit score first. A lower score shrinks your buying power because the higher interest payment eats up a massive chunk of your monthly budget.

See the Math on Your Score

Don’t just guess how much your credit profile will cost you. Use our free Mortgage Affordability Calculator to input your estimated credit score and see the exact impact on your PMI and monthly payments.

5 Brutal Beginner Mistakes That Sabotage Mortgage Approvals

When people get excited about buying a house, they tend to make rapid financial moves to “prepare.” Unfortunately, making the wrong moves in the six months leading up to a mortgage application can completely destroy your chances of closing on a home.

Here are the five most common traps to avoid:

1. Buying a Car (or Furniture) Right Before Applying

It is shocking how often this happens. Someone gets pre-approved for a mortgage, signs the contract on a house, and then realizes they need a new couch for the living room. They walk into a furniture store, open a store credit card to get “0% financing for 12 months,” and unknowingly tank their credit. Any new hard inquiry or new monthly payment added to your credit profile before your house closes can cause the lender to deny the loan at the absolute last minute. Do not buy a car, open a credit card, or finance a toaster until the keys are in your hand.

2. Closing Your Oldest Credit Card to “Clean Up”

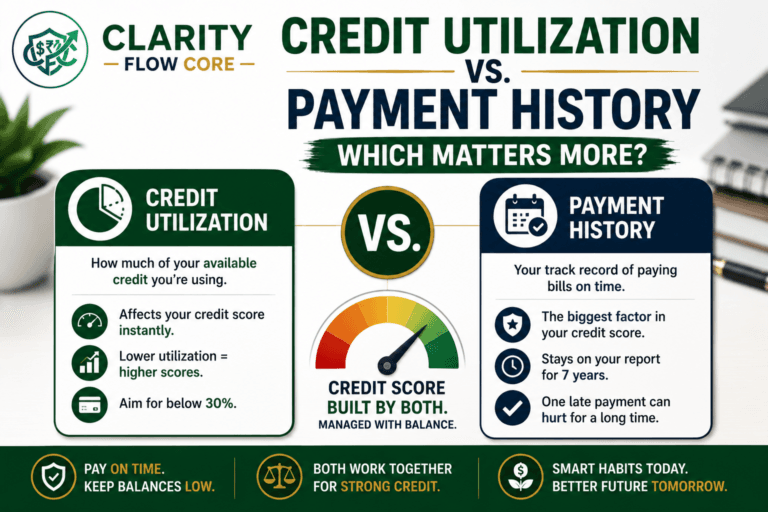

Many beginners think that closing an old, unused credit card makes them look responsible. In the credit scoring world, it actually does the exact opposite. Fifteen percent of your FICO score is based on the length of your credit history. If you close your oldest account, you artificially shorten your credit age and immediately lower your total available credit, which can cause your score to drop by 20 or 30 points overnight. Put the old card in a drawer, but leave the account open.

3. Maxing Out Cards for Wedding or Moving Expenses

Your “Credit Utilization Ratio” makes up 30% of your total credit score. This is the amount of debt you have compared to your total credit limits. If you have a credit card with a $5,000 limit and you put $4,500 of moving expenses on it, your utilization on that card is 90%. Mortgage FICO models absolutely hate high utilization. Even if you pay your bill on time every single month, simply carrying a balance that is close to your limit will suppress your score.

4. Assuming Your Partner’s Perfect Score Cancels Out Yours

If you are buying a house with a spouse or partner, you might think their perfect 800 credit score will average out your struggling 620. This is not how it works. When you apply jointly, the lender pulls all three scores for both of you. They find the middle score for Person A, and the middle score for Person B. Then, they use the lowest of those two middle scores to underwrite the loan. If your middle score is 620, the entire loan is priced as if both of you have a 620.

5. Ignoring Your Credit Report Until the Last Minute

Around 20% of Americans have a verifiable error on their credit report. This could be a medical bill you actually paid that was sent to collections by mistake, or a late payment reported by a cell phone company that belongs to someone with the same name as you. If you wait until you are sitting in a loan officer’s chair to find out about these errors, you won’t have time to fix them. Disputing errors can take 30 to 60 days to resolve.

The Beginner-Friendly Action Plan: How to Prep Your Score

If you are planning to buy a house in the next year and you feel overwhelmed by everything above, take a deep breath. You do not need to fix everything today. You just need a practical, step-by-step plan to get your profile in shape.

Step 1: Pull your actual reports and face the music.

Go to AnnualCreditReport.com (the only federally authorized site for this) and pull your full, free reports from Equifax, Experian, and TransUnion. Do not look at the scores; look at the data. Highlight anything that looks incorrect, unfamiliar, or negative. Facing the reality of your debt is emotionally taxing, but it is the required first step.

Step 2: Ruthlessly attack your credit card balances.

The fastest, most effective way to artificially boost your credit score in a short amount of time is to pay down revolving credit card debt. Your goal should be to get the balance on every single credit card under 30% of its limit—ideally under 10%. If you have a card with a $1,000 limit, do whatever it takes to get the balance below $300 before you apply for your mortgage.

If you’re rebuilding your credit from scratch or recovering after past financial mistakes, Best Secured Credit Cards for Beginners in 2026 compares beginner-friendly secured cards that can help establish positive payment history before you apply for a mortgage.

Step 3: Put your credit on ice.

From the moment you decide you are going to buy a house until the day you sign the closing papers, your credit is frozen. No new inquiries. No new loans. No co-signing for a family member’s apartment. Pay every single existing bill on time, in full, every month.

Step 4: Use the right tools to plan. Don’t just guess what will happen if you pay off a certain debt. Use our Free Credit Score Simulator & Improvement Planner to safely map out exactly which debts to pay down first to get the maximum point increase for your mortgage application.

Helpful Tools & Resources for Your Journey

If you are ready to take the next step but still feel a little unsure about where your numbers stand, we highly recommend utilizing these resources:

- Calculate Your Readiness: Use our Free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner to make sure your monthly debt obligations meet conventional lending standards.

- Simulate Your Score: See how paying down specific debts will boost your mortgage odds with our Free Credit Score Simulator & Improvement Planner.

- Keep Reading: Learn exactly what happens when you finally get that approval letter in our guide on How Mortgage Pre-Approval Actually Works.

- Watch Out For Traps: Don’t let surprise fees blindside you. Read up on The Hidden Costs of Buying a Home: What the Bank Won’t Tell You.

Frequently Asked Questions (FAQs)

Can I really buy a house with a 500 credit score?

Legally? Yes, FHA guidelines permit it if you put 10% down. Practically? Almost never. Lenders take on the actual risk of giving you the money, and finding a lender in 2026 willing to approve a 500 credit score is incredibly rare. If your score is 500, your focus should be entirely on rebuilding your credit before applying.

Does paying my rent on time help my credit score?

Traditionally, no. Rent payments are not automatically reported to credit bureaus like auto loans or credit cards are. However, there are now third-party services you can use to report your positive rent payments to the bureaus. This can give you a slight bump, but it will not magically fix a history of missed credit card payments.

How long does it take to improve my score enough to buy a house?

It depends on why your score is low. If your score is low simply because your credit cards are maxed out, paying them down can boost your score significantly in just 30 to 45 days. If your score is low because of a recent bankruptcy, foreclosure, or a string of missed payments, it will take at least 12 to 24 months of perfect payment history to rebuild trust with a lender.

If I pay off a collection account, will my score instantly go up?

Not necessarily. Older FICO mortgage models often still view a paid collection as a negative mark. However, many mortgage lenders will require you to pay off outstanding collections before they will clear your loan to close anyway.

Final Thoughts: You Are More Than Your Score

Trying to buy a home when your finances feel messy is one of the most vulnerable things you can do. It requires handing over your bank statements, tax returns, and credit history to a stranger and asking for their approval. If you have made financial mistakes in the past, that process can trigger a lot of shame and anxiety.

Please remember this: the banking system is a machine, and your credit score is just a data point to them. It does not measure your work ethic, your ability to provide for your family, or your future success.

If your score is a 580 today, that does not mean you will never own a home. It just means you have a bit of homework to do before you get the keys. Focus on what you can control today—pay down that one credit card, dispute that one old error, and keep your head up. Homeownership is a marathon, not a sprint, and you have plenty of time to cross the finish line.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

Sources & References

Articles published on Clarity Flow Core are researched and reviewed using publicly available information from official government agencies, financial institutions, consumer protection organizations, credit bureaus, and trusted educational resources.

Reference sources may include:

- Internal Revenue Service (IRS)

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve

- U.S. Department of the Treasury

- Federal Trade Commission (FTC)

- Bureau of Labor Statistics (BLS)

- Federal Deposit Insurance Corporation (FDIC)

- Securities and Exchange Commission (SEC Investor.gov)

- Experian

- Equifax

- TransUnion

- myFICO

- AnnualCreditReport.com

- Official banking, lending, insurance, and financial institution websites

- Public consumer finance studies and educational resources

Additional editorial references may include reputable financial publications, academic research, behavioral finance studies, housing and credit market data, and publicly available consumer finance resources where relevant.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.