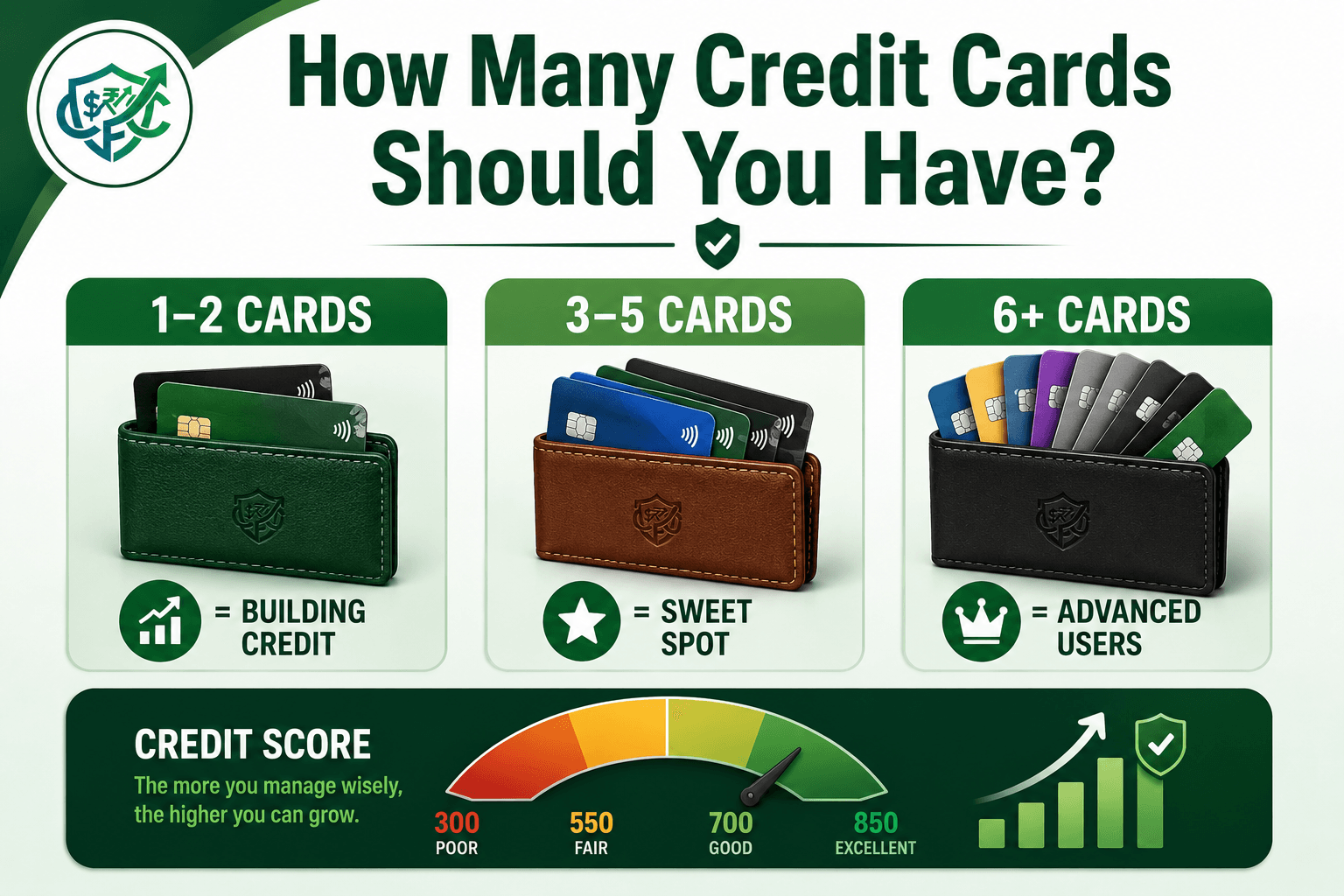

How Many Credit Cards Should You Have for the Best Credit Score?

If you are trying to figure out exactly how many credit cards should you have to get the best possible credit score, you are probably dealing with some severe financial whiplash right now.

On one hand, you have old-school financial advice telling you that credit cards are evil, dangerous traps and you should cut them all up immediately. On the other hand, you log onto social media and see points-hackers bragging about carrying 15 different premium rewards cards in their wallets while flexing a perfect 800+ credit score.

It leaves you completely stuck in the middle, staring at your one or two basic credit cards, wondering if you are doing something fundamentally wrong. Are you missing out on a higher score because you don’t have enough accounts? Will applying for a new card drop your score? Is it possible to look too desperate to a bank?

The banking industry loves to keep this ambiguous. They want you to apply for more cards, but they also want to penalize you if you look like a risk. It feels like a rigged game where nobody will just give you the straight mathematical answer.

Let’s strip away the confusing jargon and look at how the algorithm actually treats the plastic in your wallet. We are going to break down the myth of the “magic number,” the brutal beginner mistakes that will wreck your score, and how to structure your wallet so the math works in your favor.

The Real Problem: The Myth of the “Magic Number”

When people ask how many credit cards they should have, they are usually looking for a single digit. They want a rule: “Have exactly three cards, and your score will go up.”

Here is the frustrating but empowering truth: The FICO scoring algorithm does not care about the raw number of credit cards you have. There is no line of code in the algorithm that says, “If this person hits five credit cards, give them 20 bonus points.” Instead, the algorithm cares about what those cards represent. Every card you add to your wallet affects three massive pillars of your credit profile: your utilization, your payment history, and the average age of your accounts.

You can have a perfect 800 credit score with just two credit cards. You can also have a perfect 800 credit score with twelve credit cards. The number isn’t the secret; how you manage the limits on those cards is what actually moves the needle.

How Your Card Count Actually Affects Your Score

To figure out the right number of cards for your specific life, you have to understand exactly what happens under the hood of your credit report every time you open a new account.

1. It Changes Your “Credit Utilization” (The Big Booster)

This is the single biggest reason why having more than one credit card is generally better for your score. Your credit utilization ratio is how much debt you carry compared to your total available credit limits. FICO heavily weights this factor.

If you’re unfamiliar with how this ratio is calculated or why it has such a significant impact on your credit score, What Is Credit Utilization — And Why Does It Matter? explains the fundamentals with beginner-friendly examples.

Let’s say you have one credit card with a $2,000 limit. If you spend $1,000 on groceries and gas this month, your utilization is a massive 50%. The algorithm will punish your score because you look financially stretched.

Now, imagine you have three credit cards, each with a $2,000 limit (Total limit: $6,000). You still spend that exact same $1,000 on groceries and gas. Now, your utilization drops to just 16%. You didn’t pay down any debt, and you didn’t change your spending habits, but because you had more cards and a higher total limit, your credit score instantly shoots up. This is the mathematical reality behind the 30% credit utilization myth.

2. It Impacts Your “Credit Age” (The Hidden Penalty)

Every time you open a new credit card, you take a temporary hit. First, the bank pulls a “hard inquiry” on your report, which drops your score by a few points. But more importantly, a new card lowers your “Average Age of Accounts.”

If you have one credit card that you have held for ten years, your average credit age is ten years. That looks incredibly stable to a bank. If you suddenly open three new credit cards today, your average credit age drops drastically. The algorithm assumes you are going on a sudden borrowing spree, which suppresses your score until those new accounts age.

3. It Multiplies Your Risk of a Missed Payment

This is the human element that the math doesn’t account for. Payment history is the largest chunk of your credit score (35%). Managing two due dates is easy. Managing seven different due dates across five different banking apps is a logistical nightmare.

All it takes is one forgotten $12 subscription charge on a card you rarely use to trigger a 30-day late mark. And as we know from the list of massive credit score mistakes, a single missed payment can instantly wipe out 100 points of your hard-earned progress.

4 Brutal Beginner Mistakes When Managing Multiple Cards

When beginners decide they want to “optimize” their credit score, they usually rush into the process and accidentally trigger algorithmic landmines. Avoid these four common traps:

1. The “Application Spree”

You realize having more total credit might help your utilization, so you apply for an airline card, a cash-back card, and a store retail card all in the same weekend. The algorithm sees four hard inquiries and a massive influx of new credit lines. It immediately assumes you lost your job and are desperately trying to access cash to survive. Your score will plummet, and banks will likely auto-deny your last few applications.

2. Closing Cards to “Tidy Up” Your Wallet

You have five cards, but you only use two of them. You decide to be responsible and call the bank to cancel the other three. Do not do this. When you cancel a credit card, you instantly wipe out the available credit limit associated with that card. Your total overall credit limit shrinks, which means any balances you are carrying suddenly take up a much larger percentage of your available credit. Your utilization spikes overnight, and your score crashes. Put the old cards in a drawer, but leave the accounts open.

3. Opening Retail Store Cards for the Discount

You are at the checkout counter buying a laptop or a wardrobe, and the cashier says, “Do you want to save 20% today by opening a store card?” It sounds like free money, but it is a terrible deal for your credit score. Store cards typically have notoriously low limits (like $300 to $500). Because the limit is so low, simply buying the items you are standing in line for will instantly max out the card, spiking your utilization to 100% and crushing your score next month.

4. Getting Distracted by Rewards and Overspending

You open a premium travel card to earn a sign-up bonus, but the card requires you to spend $4,000 in the first three months. To hit the bonus, you start buying things you don’t actually need. Suddenly, you can’t pay the statement balance in full. If you are paying 24% interest just to earn 2% cash back, the bank is winning, and you are losing. (If you are stuck choosing a card type, read our breakdown on Cash Back vs Travel Credit Cards).

So, How Many Credit Cards Should You Have? (The Real Answer)

Because there is no universal magic number, you have to look at your personal financial maturity. Here is the realistic roadmap based on where you are in your journey today:

Level 1: The Beginner or Rebuilder (1 to 2 Cards)

If you are just establishing credit for the first time, or if you are rebuilding your profile after a bankruptcy or a string of missed payments, you only need one or two cards.

- The Goal: Prove you can handle borrowing money responsibly without getting overwhelmed.

- The Strategy: Use one card for gas, use the other for a small monthly subscription (like Netflix). Put them both on auto-pay so the statement balance is paid in full every month. Do not complicate your life with rewards tracking. Just let the on-time payments build your foundation.

If you cannot qualify for a traditional unsecured card yet, Best Secured Credit Cards for Beginners in 2026 compares beginner-friendly secured cards that can help you establish or rebuild your credit while providing a path to graduate to an unsecured card later.

Level 2: The Responsible Optimizer (3 to 5 Cards)

This is the sweet spot for 90% of everyday Americans. If you have a solid credit score (680+), you pay your balances in full every month, and you want to maximize your score while keeping life simple, aim for three to five cards.

- The Goal: Build a massive total credit limit to keep your utilization naturally low, while diversifying your accounts.

- The Strategy: Keep your oldest beginner card open just to anchor your credit age. Then, add a solid everyday cash-back card for groceries, and perhaps a travel card for bigger purchases. This gives you a strong “Credit Mix” without requiring a spreadsheet to track your due dates.

Level 3: The Points Hacker (6+ Cards)

Can you have 10, 15, or even 20 credit cards and still have an 800 credit score? Yes. But it becomes a part-time job.

- The Goal: Squeeze every possible ounce of value out of sign-up bonuses, airport lounge access, and category multipliers.

- The Strategy: You must have flawless financial discipline, substantial cash reserves, and a rock-solid tracking system. If you ever carry a balance and pay interest, the entire mathematical benefit of this strategy collapses.

The Beginner-Friendly Action Plan

If you are looking at your wallet right now and wondering what your next move should be, here is a practical, step-by-step plan to optimize your setup without hurting your score.

Step 1: Inventory what you have. Log into your banking apps and write down the total credit limit and the age of every card you currently have. Identify your oldest card—you will protect this card at all costs, even if it doesn’t earn good rewards.

Step 2: Check your utilization. Add up all your current balances and divide them by your total credit limits. If that number is over 30%, do not apply for any new cards right now. Focus entirely on paying down those balances. Adding a new card when your utilization is high will make you look risky to the underwriter.

Step 3: Space out your applications. If your score is healthy and you want to add a new card to improve your total limit, go ahead and apply. But make it a strict rule to wait at least six months before applying for another one. This gives your score time to recover from the hard inquiry and prevents you from looking desperate to the algorithm.

Step 4: Use technology to prevent human error. If you manage more than two cards, human memory is no longer a reliable financial strategy. Set up automatic payments for the “Minimum Amount Due” on every single card you own. You should still log in and pay the full statement balance manually to avoid interest, but having that auto-pay safety net guarantees you will never accidentally suffer a 100-point drop because you forgot a due date.

Frequently Asked Questions (FAQs)

Does having zero credit cards give you a perfect credit score?

No. Having zero credit cards often leads to a score of zero, or an “unscorable” profile. A credit score is a measurement of how well you handle borrowing money. If you do not borrow money, the algorithm has no data to grade you on. You need at least one active credit account to maintain a FICO score.

Is it bad to have $0 balances on all my cards?

Absolutely not. Paying your cards down to $0 every month is the smartest financial move you can make. The credit bureaus will see that the accounts are active and paid on time, and your 0% utilization will push your score to its maximum potential.

Should I cancel a card if it has an annual fee but I don’t use it?

This is the one exception to the “never close a card” rule. If you are paying a $95 annual fee for a travel card you haven’t used in two years, it is usually better to stop bleeding cash. Before canceling, call the bank and ask if they can “downgrade” the card to a free, no-annual-fee version. This allows you to keep the credit line open and preserve your credit age without paying the fee.

Is having 10 credit cards bad?

Not necessarily. Many people with excellent credit scores have 10 or more cards. The key is keeping utilization low and making every payment on time.

How many credit cards do people with 800 credit scores have?

There is no fixed number. Some people reach 800 with only two cards, while others have more than ten. The score depends on credit history, utilization, payment history, and account age rather than card count alone.

Should I open another credit card to improve my score?

Only if you can manage it responsibly. A new card can increase available credit and lower utilization, but it may temporarily lower your score because of the hard inquiry and reduced average account age.

Final Thoughts: Keep It Simple

When you are stressed about your financial future, it is easy to overcomplicate things. You start thinking that if you just unlock the perfect combination of five different credit cards, your financial life will magically fall into place.

The truth is, building a great credit profile is profoundly boring. It does not require a wallet bulging with heavy metal cards. It just requires consistency.

If you are happy with two credit cards, stick with two. If you have five and you can manage them responsibly without paying interest, keep five. The best number of credit cards is simply the number you can comfortably manage while paying your balances in full every single month. Master your spending habits first, let your accounts age naturally, and the high credit score will follow. You’ve got this.

Sources & References

- FICO® – What’s in Your FICO® Score? – Learn how payment history, credit utilization, length of credit history, and new credit accounts influence your FICO® Score.

- Consumer Financial Protection Bureau (CFPB) – Credit Cards – Official guidance on choosing, managing, and using credit cards responsibly while avoiding unnecessary fees and debt.

- Experian – How Many Credit Cards Should You Have? – Educational resources explaining how multiple credit cards can affect utilization, credit history, and overall credit scores.

- Equifax – Credit Card Management & Credit Scores – Learn how opening and closing credit cards, credit utilization, and payment history can influence your credit profile.

- AnnualCreditReport.com – Request your free credit reports from Equifax, Experian, and TransUnion to review account history, credit limits, and payment records.

- Federal Trade Commission (FTC) – Credit, Loans, and Debt – Consumer information on responsible credit use, borrowing decisions, and protecting your financial health.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.