How Much of Your Income Should Go Toward Housing Costs?

The largest single expense in almost every American budget is housing. Whether you are signing a fresh 12-month lease on a downtown apartment or closing on a 30-year fixed mortgage in the suburbs, getting your housing payment wrong has catastrophic ripple effects across the rest of your financial life.

If you commit too much money to your monthly payment, you become “house poor.” You might have a beautiful place to live, but you will have zero cash left over to invest, travel, or handle emergencies. So, exactly how much of your income should go toward housing to keep your finances safe?

⚡ Quick Answer

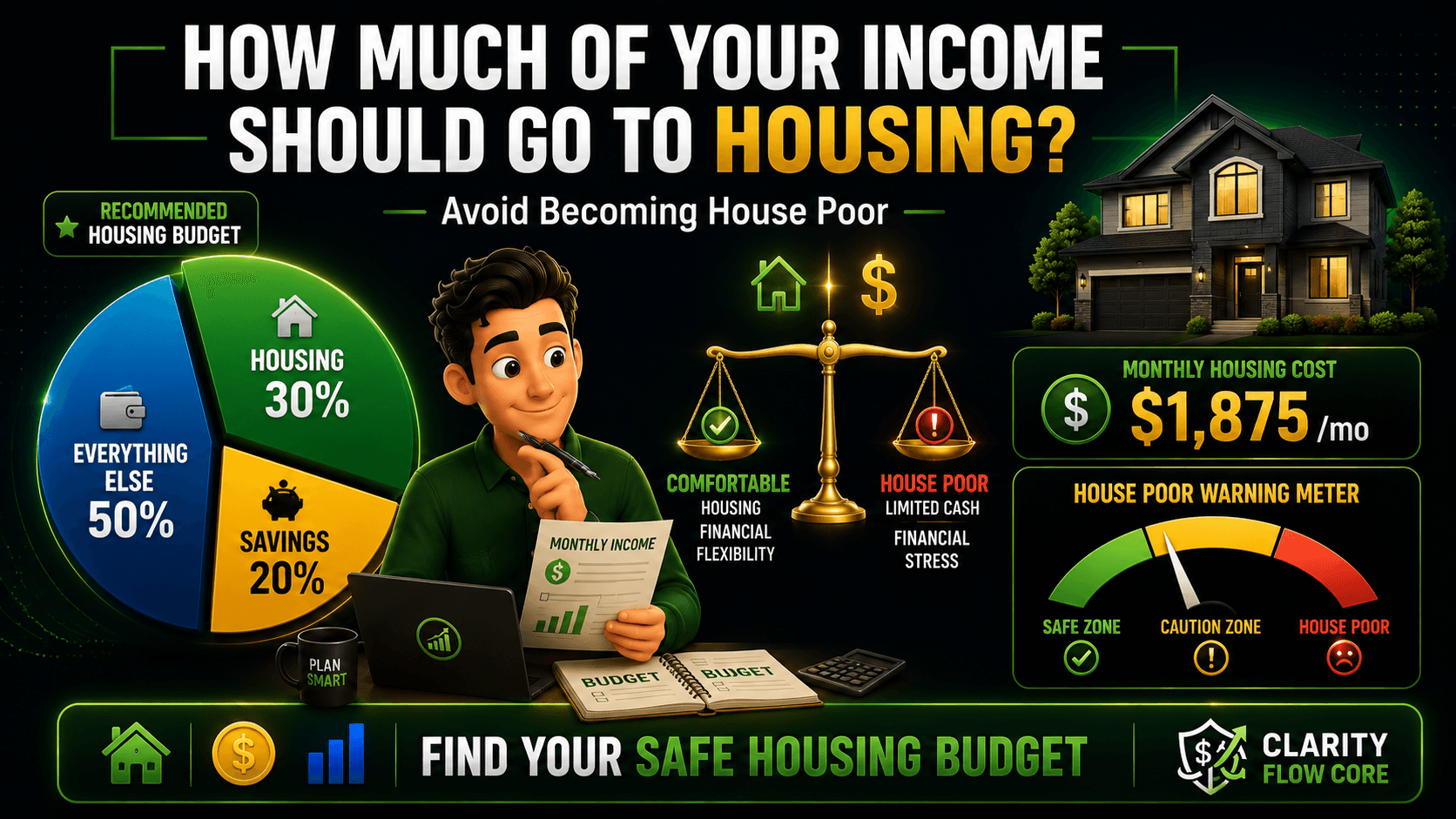

The standard financial rule of thumb is that no more than 30% of your gross monthly income should go toward housing costs. If you are buying a home, lenders look for the 28/36 rule: housing costs should not exceed 28% of your gross income, and total debt (including the mortgage) should not exceed 36%. However, for maximum safety, base your budget on your net (take-home) pay rather than your gross pay.

In this master guide, we will break down the math behind the standard rules, show you how to calculate a safe maximum payment based on your specific debt load, and highlight the hidden homeownership and rental costs that ruin otherwise solid budgets.

The Standard Baseline: The 30% Rule

The most famous housing guideline in personal finance is the 30% rule. Originally developed in the 1960s as a metric for public housing affordability, it has since become the gold standard used by landlords and financial planners nationwide.

The rule states that your total housing costs should not exceed 30% of your gross income (your income before taxes, 401(k) contributions, or health insurance premiums are deducted).

How the Math Works

Let’s say you earn a salary of $75,000 per year.

- Annual Gross Income: $75,000

- Monthly Gross Income: $6,250

- Maximum Housing Budget (30%): $1,875 per month

If you are a renter, that $1,875 should ideally cover your base rent plus essential utilities. If you are a buyer, that $1,875 needs to cover your mortgage principal, interest, property taxes, and homeowners insurance (often referred to as PITI).

The Flaw in the 30% Rule

While it is an excellent starting point, the 30% rule has a massive blind spot: it ignores your other debts. If you have zero student loans and no credit card debt, spending 30% of your gross income on an apartment is incredibly comfortable.

However, if you have a $500 monthly car payment and $400 in minimum credit card payments, spending another 30% of your gross income on rent is going to push you to the brink of financial disaster. This is why mortgage lenders use a more sophisticated calculation.

The Mortgage Standard: The 28/36 Rule

If you are transitioning from renting to buying, the bank is not going to rely on a generic 30% rule. When determining how much of your income should go toward housing, mortgage underwriters use the 28/36 rule to calculate your Debt-to-Income (DTI) ratio.

Here is how the two halves of the rule work:

1. The Front-End Ratio (28%)

Lenders want your projected housing costs to be no more than 28% of your gross monthly income. This includes:

- Mortgage Principal

- Mortgage Interest

- Property Taxes

- Homeowners Insurance

- Private Mortgage Insurance (PMI, if your down payment is under 20%)

- Homeowners Association (HOA) Fees

2. The Back-End Ratio (36%)

Lenders want your total debt obligations—which includes the new mortgage plus all your existing monthly debt payments—to be no more than 36% of your gross monthly income. This includes the new housing payment, auto loans, student loans, minimum credit card payments, and personal loans or child support.

Seeing the Math in Action

Let’s use our previous example of someone making $6,250 a month in gross income, but this time they have a $400 car payment and a $200 student loan payment.

| Metric | Target Percentage | Maximum Dollar Amount |

| Gross Monthly Income | 100% | $6,250 |

| Max Housing Payment (Front-End) | 28% | $1,750 |

| Max Total Debt Allowed (Back-End) | 36% | $2,250 |

Even though the 28% rule says they can afford a $1,750 mortgage, their existing debts ($600 total) push them over the limit.

- $1,750 (Mortgage) + $600 (Existing Debt) = $2,350 Total Debt.

Because $2,350 is greater than their 36% limit ($2,250), the lender will likely force them to buy a cheaper house, requiring their mortgage payment to drop to $1,650 to fit the math.

To see exactly where your numbers currently stand and map out your purchasing power, run your financials through our Mortgage Affordability Calculator & Home Buying Planner.

How Much House Can You Actually Afford?

Stop guessing your home buying budget. Instantly calculate your realistic price range, estimated monthly payments, and overall loan readiness based on your current income and debts.

Calculate My Buying PowerThe Reality Check: Net Income vs. Gross Income

Both the 30% rule and the 28/36 rule rely on gross income. But you do not pay your mortgage with gross income; you pay it with the actual cash that hits your checking account.

If you are aggressively saving for retirement by putting 15% of your paycheck into a 401(k), and paying high premiums for a great family health insurance plan, your take-home (net) pay might only be 65% of your gross income. If you then spend 30% of your gross income on a mortgage, it could easily consume nearly half of your actual take-home pay.

The 50/30/20 Budgeting Solution

A much safer, more modern approach to determining how much of your income should go toward housing is to use The 50/30/20 Budget Rule Explained Simply.

This system breaks your net income into three categories:

- 50% Needs: Housing, groceries, utilities, minimum debt payments, and basic insurance.

- 30% Wants: Dining out, travel, hobbies, and subscriptions.

- 20% Savings: Retirement accounts, emergency funds, and extra debt payoff.

Under this model, your housing payment must fit comfortably inside that 50% “Needs” bucket alongside your groceries and car payment. By basing your budget on the cash you actually take home, you guarantee that you will always have money left over to build wealth and enjoy life.

The Hidden Costs That Wreck Housing Budgets

When people ask, “How much of your income should go toward housing?”, they almost always forget that the lease or the mortgage is just the baseline. To build an accurate housing budget, you must account for the hidden costs of shelter.

Hidden Costs for Renters

If you are stretching your budget to sign a lease for exactly 30% of your income, you will likely overdraft your account due to:

- Pet Rent and Fees: Often $25 to $50 extra per month, plus non-refundable deposits.

- Parking Fees: In major cities, an assigned spot can cost $100 to $300 a month.

- Renter’s Insurance: Required by most landlords ($10 to $20/month).

- Utility Deposits: If you are a first-time renter, utility companies may charge hefty upfront deposits to turn on the power and water.

Hidden Costs for Homebuyers

Rent is the maximum you will pay for housing in a given month. A mortgage is the minimum you will pay. If you buy a house, you must budget for:

- Maintenance & Repairs: The rule of thumb is to save 1% of the home’s value every year for maintenance. If you buy a $400,000 home, you need to set aside roughly $333 a month for inevitable roof repairs, broken HVAC systems, and plumbing issues.

- Rising Property Taxes: Your mortgage principal is fixed, but property taxes can (and usually do) go up every year, driving your monthly payment higher.

- HOA Special Assessments: Beyond your monthly HOA fee, the board can levy thousands of dollars in surprise assessments if the neighborhood needs a new roof or structural repairs.

If you are torn between these two paths, read our complete breakdown on Renting vs Buying a Home in 2026.

Common Mistakes When Budgeting for Housing

1. Maxing Out the Bank’s Pre-Approval

When you apply for a mortgage, the bank will give you a pre-approval letter stating the absolute maximum amount they are willing to lend you based on the 36% debt limit. Do not spend the maximum. The bank does not care if you want to take a vacation, send your kids to summer camp, or save for retirement. They only care that you can technically survive while paying them. Always buy less house than the bank says you can afford.

2. Ignoring Credit Score Impact

Your credit score dictates your mortgage interest rate. A low score can easily add hundreds of dollars to your monthly housing payment, destroying your budget even if you buy a modestly priced home. Before entering the housing market, test different financial moves using our Interactive Credit Utilization & Score Simulator to maximize your score and secure the lowest possible interest rate.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My Utilization3. Forgetting About Lifestyle Inflation

If you get a 10% raise at work, your immediate reaction might be to upgrade to a luxury apartment that eats up that entire raise. This is lifestyle inflation. Just because your income goes up does not mean the percentage of your income going toward housing needs to increase. Keeping your housing costs flat while your income grows is the fastest way to build massive wealth.

Your Step-by-Step Action Plan

Before you sign a lease or make an offer on a house, follow this strict chronological sequence to ensure the payment fits your life.

1.Calculate Your True Net Income:Ignore the gross number.

Look at your last three paystubs. Add up the exact amount of cash that actually hit your checking account. This is your true baseline.

2.Map Your Mandatory Needs:Find the 50% limit.

Take your monthly net income and multiply it by 0.50. This is your maximum budget for all needs combined. Subtract your current groceries, utilities, car payments, and minimum debt payments from this number. What remains is your true maximum housing budget.

3.Take the ‘Practice Rent’ Challenge:Feel the weight of the payment.

If your current rent is $1,500 and you want to buy a house with a $2,200 payment, you have a $700 gap. For the next three months, transfer exactly $700 into a savings account on the 1st of the month. If your budget feels suffocating, you cannot afford the house.

4.Build a Dedicated Maintenance Fund:Protect the property.

If you are buying a home, ensure you have a fully funded 3-to-6-month emergency reserve separate from your down payment. Run your numbers through our Emergency Fund Calculator before closing.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings Target

Frequently Asked Questions (FAQ)

Does the 30% rule still work in high-cost-of-living (HCOL) areas?

In cities like New York, San Francisco, or Miami, strictly adhering to the 30% rule is incredibly difficult for average earners. In these markets, people often spend 40% or even 50% of their income on rent. If you must exceed the 30% threshold to find safe housing, you have to drastically cut your “Wants” category (dining out, travel, car payments) to keep your overall budget balanced.

Should I pay off all my debt before buying a house?

While you do not need to be 100% debt-free to buy a house, eliminating high-interest consumer debt (like credit cards and personal loans) is highly recommended. Not only does it lower your Debt-to-Income ratio (making it easier to qualify for a mortgage), but it frees up vital cash flow to handle the inevitable maintenance costs of homeownership.

Are utilities included in the 30% housing rule?

Traditionally, yes. When calculating how much of your income should go toward housing as a renter, the 30% limit should encompass your base rent plus essential utilities (water, electricity, gas, and trash). It generally does not include internet or cable subscriptions.

What happens if my Debt-to-Income ratio is too high?

If your DTI exceeds 36% (or up to 43% for certain FHA loans), mortgage lenders will view you as a high-risk borrower. They will either deny your loan application entirely, require you to make a much larger down payment, or force you to pay off specific debts (like a car loan) before they will clear you to close on the home.

Conclusion

Deciding how much of your income should go toward housing is the financial linchpin of your entire budget. While the 30% gross income rule and the lender’s 28/36 rule provide excellent mathematical guardrails, the ultimate test is your net income.

Your home should be a place of safety and comfort, not the source of your daily financial anxiety. By capping your housing costs, aggressively managing your other debts, and factoring in the hidden expenses of maintenance and utilities, you ensure that you control your house—instead of letting your house control you.

References

- Consumer Financial Protection Bureau (CFPB): Guidelines on understanding the Debt-to-Income (DTI) ratio and mortgage readiness.

- U.S. Department of Housing and Urban Development (HUD): Historical definitions of housing affordability and the origins of the 30% rule.

- Federal Deposit Insurance Corporation (FDIC): Recommendations on budgeting for housing and maintaining an adequate emergency savings buffer.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.