Emergency Fund Basics: How Much Cash Should You Keep?

Four years ago, my financial system was running like clockwork. I was finally making decent money, I had aggressively paid off my credit cards, and I was feeling immensely proud of my shiny new investment portfolio. I thought I was invulnerable.

Then, on one wet Tuesday morning, my transmission completely blew up on the interstate. The tow truck driver shook his head, and the mechanic subsequently handed me an estimate for $3,800.

I panicked. All my money was either locked up in the stock market or had been thrown furiously at past debts. I had zero liquid cash on hand. I was forced to put the entire $3,800 repair bill onto a credit card with a 24% interest rate. In a single afternoon, I destroyed months of hard financial effort because I had entirely ignored the most boring, yet most critical rule of personal finance: I did not have a cash buffer.

Investing and budgeting are thrilling, but you cannot build a castle on quicksand. You must construct a concrete foundation first. This is the operational guide to mastering emergency fund basics. Here is exactly how to understand the math, calculate your survival number, and build an ironclad safety net so that a bad Tuesday never ruins your financial life again.

What Actually is an Emergency Fund?

The most common misconception in emergency fund basics is what this money is actually supposed to do. An emergency fund is simply a specific amount of liquid cash set aside exclusively for unanticipated financial shocks. It is the friction layer between you and the inevitable calamities of life.

Consider it a form of self-funded insurance. This cash pile catches you when the transmission dies, the roof leaks, or your company initiates mass layoffs. Because you have this cash, you never have to rely on high-interest credit cards or predatory payday loans just to survive the month.

If you’ve already lost your job and need a step-by-step action plan, I Lost My Job: A 30-Day Financial Survival Plan walks through exactly how to protect your cash, prioritize bills, and stabilize your finances during unemployment.

The Golden Rule: An emergency fund is not an investment. It is not intended to make you rich. It is intended to protect the things that will make you rich.

When discussing emergency fund basics, you must drop the expectation of massive returns. You should never worry about whether this cash is “beating the stock market.” Its only job is to be liquid, mathematically safe, and ready to deploy at a moment’s notice.

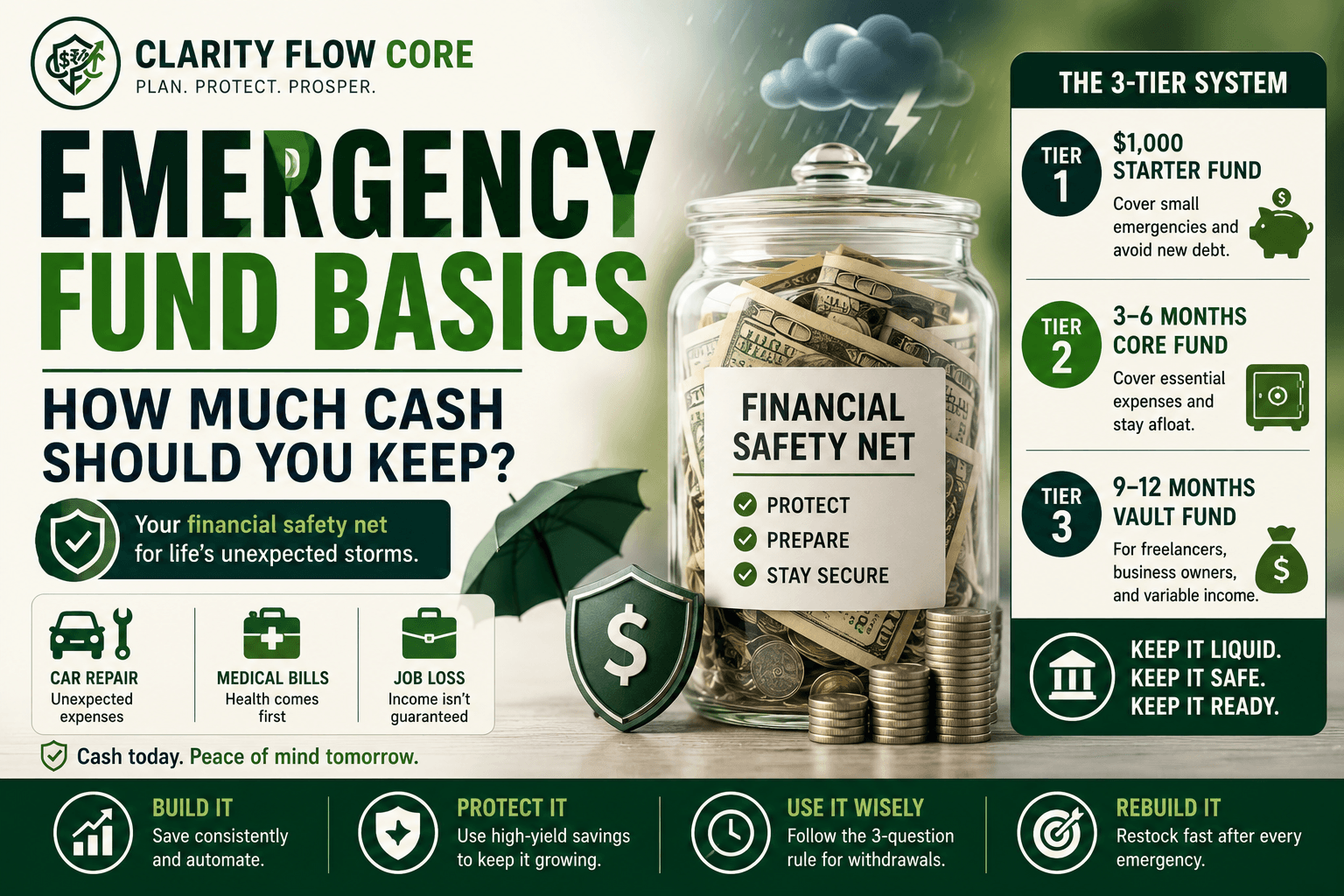

The Tiered System: What Do You Really Need?

If you search online for emergency fund basics, you will discover generic recommendations like “save between one month and one year’s worth of spending.” That advice is paralyzing. Do not guess. Use this strict 3-tiered technique to construct your safety net methodically.

Tier 1: The $1,000 Starter Fund (Your Immediate Protection)

If you have zero savings and you are currently working hard to pay down high-interest consumer debt, your immediate first goal is to build a basic starter fund of $1,000 to $2,000.

Why this specific sum? Because it handles the vast majority of “annoying” emergencies. It covers a broken alternator, a surprise urgent care co-pay, or replacing a dead refrigerator. With this starter fund in place, you can safely execute the Debt Avalanche vs. Debt Snowball: Which Works Better? method to pay off your credit cards. When a minor inconvenience hits, you use the cash instead of borrowing money again.

Tier 2: The Standard (3-6 Month Core Fund)

Once you have eradicated your toxic, high-interest debt, it is time to turn your starter fund into a fully funded safety net. The cornerstone of emergency fund basics is having enough liquid cash to cover 3 to 6 months of living expenses.

Notice the phrase living expenses, not revenue. If you bring home $6,000 a month, but your required survival costs (rent, groceries, basic utilities, health insurance) are only $3,000 a month, your target is based purely on the $3,000.

| Survival Expense Profile | 3-Month Target | 6-Month Target |

| $2,500 / month | $7,500 | $15,000 |

| $3,000 / month | $9,000 | $18,000 |

| $4,500 / month | $13,500 | $27,000 |

How to Choose: If you are single, rent an apartment, and work a highly stable W-2 job (like nursing or teaching), lean closer to 3 months. If you own a home (where the big repairs are), have children, or work in a volatile corporate industry, you must lean closer to 6 months.

If you’re preparing to live independently for the first time, building this safety net should be part of your moving budget. Before signing a lease, read How Much Should You Save Before Moving Out on Your Own? to estimate your upfront costs and the savings you’ll want before making the transition.

Tier 3: The 9-12 Month Vault (The Freelancer Special)

If your income is highly variable—meaning you are a freelancer, a commission-only salesperson, or a small business owner paying Freelance Video Editor Taxes—you need a much wider moat.

You should strive to have 9 to 12 months of survival expenditures. In the gig economy, your income can disappear completely during a slow economic quarter. A massive cash vault ensures you can survive a six-month dry stretch without losing your business or defaulting on your mortgage.

Where Do You Store Your Emergency Fund?

This is where millions of people fail at emergency fund basics. Do not keep this money in your primary checking account, and most importantly, do not invest this money into the stock market.

If the cash sits in your daily checking account, you will accidentally spend it on a weekend getaway. If it sits in an Index Fund or Mutual Fund, there is a massive risk that the stock market crashes the exact same week you lose your job. You would be forced to withdraw your money at a huge loss just to pay rent.

The Operational Fix: The High-Yield Savings Account (HYSA)

You need a specific High-Yield Savings Account at an online-only bank. Institutions like Ally, Marcus by Goldman Sachs, or Capital One 360 do not have the massive overhead costs of physical brick-and-mortar branches. Therefore, they pass their profits directly back to you in the form of higher interest rates.

If you’re opening your first online savings account, How to Choose Your First High-Yield Savings Account explains how to compare APYs, account fees, FDIC insurance, and transfer features before choosing a bank.

Competitive HYSAs often pay significantly more than traditional savings accounts, although rates fluctuate with market conditions., while a traditional mega-bank will offer you a miserable 0.01% APY.

If you park a fully funded $15,000 emergency fund in a 4.5% HYSA, the bank will essentially hand you $675 a year in pure interest just for keeping your money safe. Your money is fully liquid (you can transfer it to your checking account in 1-2 business days), but it generates inflation-fighting cash while it sits.

How to Grow Your Fund Fast (Without Being Miserable)

Saving $15,000 can seem completely unattainable. But mastering emergency fund basics is a marathon, not a sprint. Here is the operational blueprint to build it quickly.

1. Make It Mathematically Automatic

Find your saving margin using the 50/30/20 Budgeting Rule Explained Simply. If you determine you can save 20% of your salary, do not rely on your own willpower to move the cash on the 31st of the month.

Set up an automatic transfer. Better yet, learn How to Automate Savings Using Split Direct Deposit through your employer’s HR portal. Before your paycheck even hits your checking account, a fixed amount ($100, $200, or $500) is routed directly to your HYSA. Treat your emergency fund contribution as a non-negotiable monthly bill.

2. Capture Your Windfalls

A windfall is unexpected money. This includes your annual tax refund, a holiday bonus from work, or selling old electronics on Facebook Marketplace. We are psychologically programmed to view windfalls as “play money.” Do not spend your $1,500 tax refund on a vacation. Route 100% of it directly to your emergency fund. Capturing windfalls will literally shave months off your saving timeline.

3. The 30-Day “Scorched Earth” Sprint

If you are starting from absolute zero and need that $1,000 starter fund immediately, proclaim a 30-day “Scorched Earth” sprint. For one single month: cancel every subscription, eat zero meals at restaurants, and pick up weekend gig labor (like driving Uber or doing freelance video editing). You can survive almost any level of frugality if you know it only lasts for 30 days. Get the cash, secure the shield, and return to your normal life.

The 3-Question Test: When to Actually Spend the Money

A massive pile of cash sitting in the bank is incredibly tempting. When you get bored of driving a ten-year-old car, your brain will try to justify spending your safety net.

A critical pillar of emergency fund basics is protecting the money from your own impulsive wants. You must run every potential withdrawal through the strict 3-Question Emergency Test. If you cannot answer “YES” to all three questions, it is not an emergency.

- Is it Unexpected? Christmas is not unexpected; it happens on December 25th every year. Annual car registration is not unexpected. Those must be budgeted for. However, a tree falling on your roof is genuinely unexpected.

- Is it Necessary? Upgrading to the newest MacBook Pro because your current laptop is “feeling slow” is a want, not a need. Replacing the blown brakes on your commuter car so you can safely get to work is an absolute necessity.

- Is it Urgent? Buying plane tickets for a friend’s wedding next summer is not urgent; you have time to cash-flow it. Booking a last-minute flight for an immediate family funeral is highly urgent.

If the expense is unexpected, necessary, and urgent, that is exactly what the emergency fund is for. Transfer the money, pay the bill, do not feel guilty, and breathe a massive sigh of relief.

The Reconstruction Era

When you finally have to dip into your vault, it is going to feel terrible to watch the number go down. That is a completely reasonable psychological reaction, but you must reframe it: The fund accomplished exactly what it was designed to do. You took a financial hit, and it didn’t ruin your life.

Once the crisis passes, your immediate operational goal is to replenish the fund. Pause your extra debt payments, put your stock market investing on hold, and throw all of your free cash flow back at the HYSA until the shield is fully mended.

Your emergency reserve is the bedrock of all personal finance. Without it, every budget you create and every investment you make is built on a house of cards. Master these emergency fund basics, calculate your 3-month survival number tonight, open a High-Yield Savings Account, and set up your first automatic transfer.

FAQ

How much should I keep in an emergency fund?

Most people target 3–6 months of essential living expenses, though freelancers and variable-income earners may need more.

Should I invest my emergency fund?

Generally no. Emergency funds prioritize safety and liquidity over investment returns.

Where should I keep my emergency fund?

A high-yield savings account is one of the most common options because it offers accessibility and interest income.

Can I use a credit card instead of an emergency fund?

Credit cards can help in a crisis, but relying on debt may create long-term financial problems.

What counts as an emergency?

Unexpected, necessary, and urgent expenses such as medical emergencies, major home repairs, job loss, or essential vehicle repairs.

References & Trusted Sources

To verify current federal regulations regarding credit card fees, interest rates, and promotional terms, consult these official resources:

- Consumer Financial Protection Bureau (CFPB) – Emergency Savings Resources

- Federal Deposit Insurance Corporation (FDIC) – Deposit Insurance Overview

- National Credit Union Administration (NCUA) – Share Insurance Coverage

- Federal Trade Commission (FTC) – Managing Unexpected Expenses

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

13 Comments

Comments are closed.