Why Young Adults Keep Falling Into Credit Card Debt (Without Realizing It)

Here is how you can rewrite the very beginning of the article (starting with the Quick Answer and the first paragraph) to immediately clear that warning and turn it green:

⚡ Quick Answer If you are wondering why young adults fall into credit card debt, the answer is rarely about buying luxury cars or taking lavish vacations. It usually happens through a slow accumulation of living expenses, unexpected emergencies, and a misunderstanding of how compounding interest works. By relying on minimum payments and carrying high credit utilization, minor balances can stretch into years of debt. The best way out is to temporarily freeze card usage, confront the total balance, and use strategies like the Debt Avalanche or a balance transfer to minimize interest charges.

Understanding why young adults fall into credit card debt is the first step to breaking the cycle. You open your email, and there it is: your monthly credit card statement is ready.

Instead of clicking the link to view the PDF, you might just swipe the notification away. You tell yourself you’ll look at it tomorrow when you have more time, or maybe after your next paycheck clears. But tomorrow turns into next week, and soon you find yourself just transferring $50 or $100 over to the card account whenever you can, hoping the balance is quietly shrinking in the background.

If this feeling of low-grade financial anxiety sounds familiar, take a deep breath. You are not alone, you are not inherently “bad with money,” and you are definitely not the only person feeling overwhelmed by a banking app.

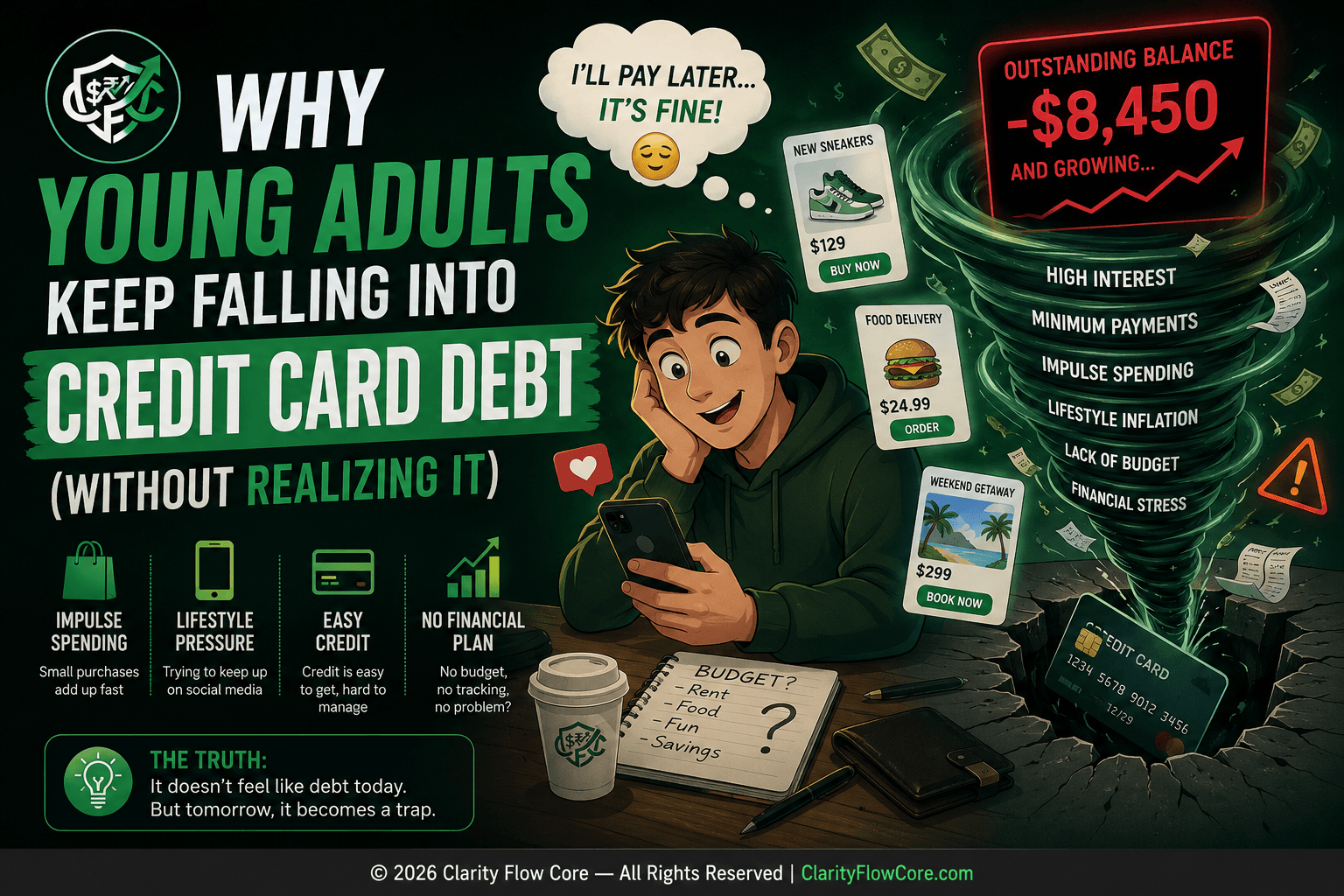

Millions of young Americans currently carry consumer debt, and very few of them planned for it. Nobody wakes up on their 22nd birthday and decides to take on high-interest loans. Instead, credit card debt often sneaks into your life through a series of practical, everyday decisions.

Society sometimes pushes the narrative that debt is purely the result of reckless spending. But in the real world, most young adults fall into credit card balances just trying to navigate the baseline cost of living.

If you are currently carrying a balance, the best thing you can do right now is remove the shame. We need to strip the emotion out of the equation and look at the realistic mechanics of what is actually happening. Here is an honest look at exactly why young adults fall into credit card debt how the compounding math actually works, and a realistic blueprint to help you climb out.

The Disconnect Between Plastic and Pain

To understand why credit card debt accumulates so easily, it helps to look at human psychology.

Behavioral economists often talk about a concept called the “pain of paying.” If you go to a grocery store, pull a crisp $100 bill out of your wallet, and hand it to a cashier, your brain registers a physical loss. You literally watch your resources leave your hand. That slight psychological friction naturally forces you to pause and ask, “Do I really need this?”

Credit cards bypass that friction entirely.

When you tap a piece of plastic or double-click the side button on your phone for Apple Pay, nothing physically leaves your possession. The transaction is seamless, silent, and instantaneous.

Because the reality of the purchase is delayed until the bill arrives weeks later, your brain categorizes the transaction differently. It doesn’t feel like you are spending real currency today; it feels like a problem for “future you”—and we almost always assume “future you” will have more money and better discipline.

The Real-Life Scenario: Why Young Adults Fall Into Credit Card Debt

When older generations give financial advice, they sometimes assume young adults are going into debt buying designer wardrobes. In reality, modern credit card debt is rarely caused by massive, deliberate splurges. It is usually a slow build.

Let’s look at a very common, realistic scenario.

Meet Jake.

Jake is 24 years old and makes $52,000 a year working a steady job. He brings home roughly $3,400 a month after taxes.

- In March, Jake moves into a new apartment. He has to pay a security deposit and buy a moderately priced couch, putting $800 on his credit card.

- In April, his car needs a sudden brake repair that costs $600. He doesn’t have an emergency fund, so he swipes the card again.

- Between May and July, Jake attends two friends’ weddings, covering travel and hotel splits, adding another $1,400.

Jake isn’t living a lavish lifestyle. He is just navigating normal young adult milestones and minor emergencies. But suddenly, Jake is carrying a $2,800 balance. Because his rent and groceries take up most of his paycheck, he can only afford to send the bank about $80 a month.

Jake is now officially caught in the cycle.

The Most Common Beginner Credit Card Mistakes

Banks are highly optimized institutions. Their systems are designed with the understanding that many consumers will make a few predictable, very common missteps.

Mistake 1: Treating the Credit Limit as “Available Cash”

When you log into your banking app and see “Total Available Credit: $5,000” in bright green letters, your brain can easily subconsciously register that as your money.

It isn’t. That is simply the maximum amount of risk the bank is willing to take on you. Many young adults inadvertently scale their lifestyle to match their credit limit, rather than their actual checking account balance. It is very easy to accidentally live a $4,000-a-month lifestyle on a $3,000-a-month income if the plastic keeps approving the transactions. This phantom safety net is a massive reason why young adults fall into credit card debt early in their careers.

Mistake 2: Falling for the Minimum Payment Math

When your statement arrives, the bank usually highlights your “Minimum Payment Due.” It is often a very manageable number, like $35 or $80.

Relying on this number is one of the most expensive mistakes you can make. The Consumer Financial Protection Bureau (CFPB) frequently warns that making only the minimum payment stretches your debt out over years, exponentially increasing the cost of your original purchases.

Let’s look at Jake’s $2,800 balance to see exactly how this math plays out in the real world. Assuming his card has a standard 24% Annual Percentage Rate (APR), here is what happens if he only pays an $80 minimum every month:

| The Debt Math | The Minimum Payment Reality |

| Starting Balance | $2,800 |

| Interest Rate (APR) | 24% |

| Monthly Payment | $80 |

| Time to Pay Off | 5 Years and 4 Months |

| Total Interest Paid | $2,311 |

| True Cost of the $2,800 Debt | $5,111 |

By paying only $80 a month, Jake ends up handing the bank over $2,300 in pure interest. That is why the minimum payment exists—it is a mathematical formula designed to keep your account in good standing while maximizing the bank’s profit over the long haul.

Editorial Note: To dive deeper into the exact formulas banks use to calculate these fees, you can read our breakdown on what happens if you only pay the minimum on a credit card.

Mistake 3: Chasing Rewards Points While Carrying a Balance

“But I’m getting 2% cash back!” Credit card rewards can be a great financial tool, but they usually only work in your favor if you pay your bill in full every single month. If you are carrying a balance that is charging you 24% in interest, and you are swiping the card to earn 2% in cash back, you are often operating at a mathematical net loss. The interest charges will typically erase the value of your points within the first few days of the billing cycle.

Interactive Tool: The Real Cost Credit Card Calculator

Enter your own numbers below to see exactly how your interest rate affects your payoff timeline, and notice how adding just a little extra cash each month changes the math entirely.

Advanced Credit Card Payoff Planner

Map out your exact debt-free date and see what your balance is really costing you.

*Educational estimates only. Results may vary based on your specific compounding method and card terms.

The Real Consequences of the Debt Trap

The impact of credit card debt goes beyond just the numbers. It can actively affect your broader financial profile.

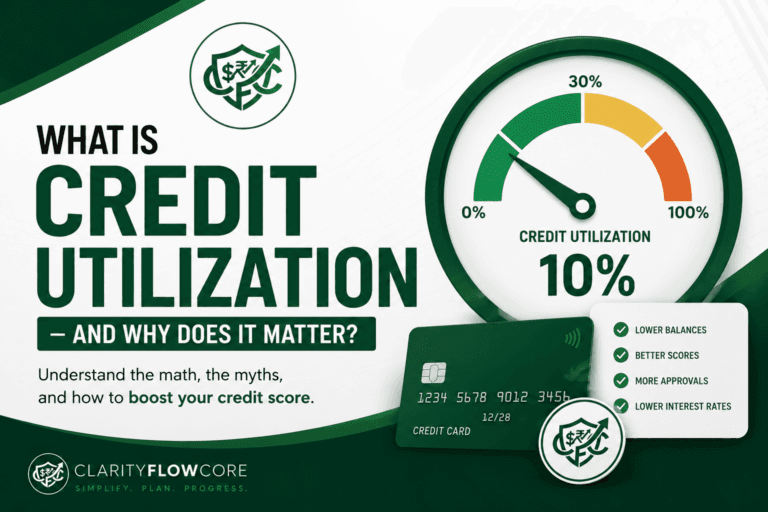

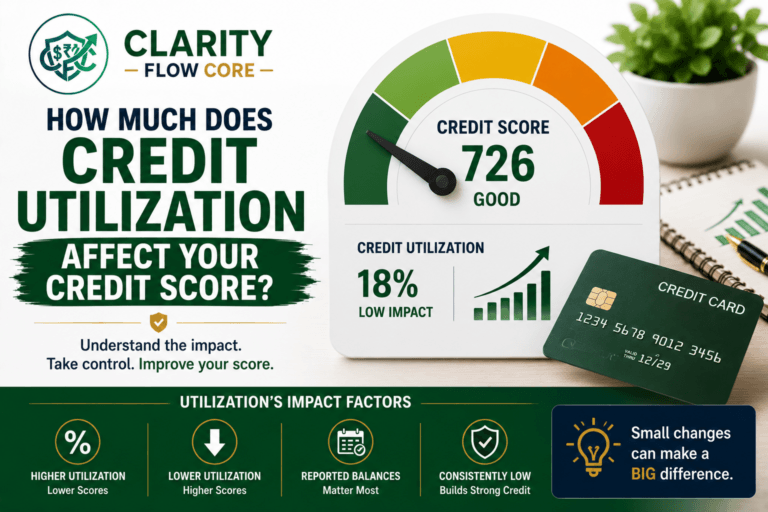

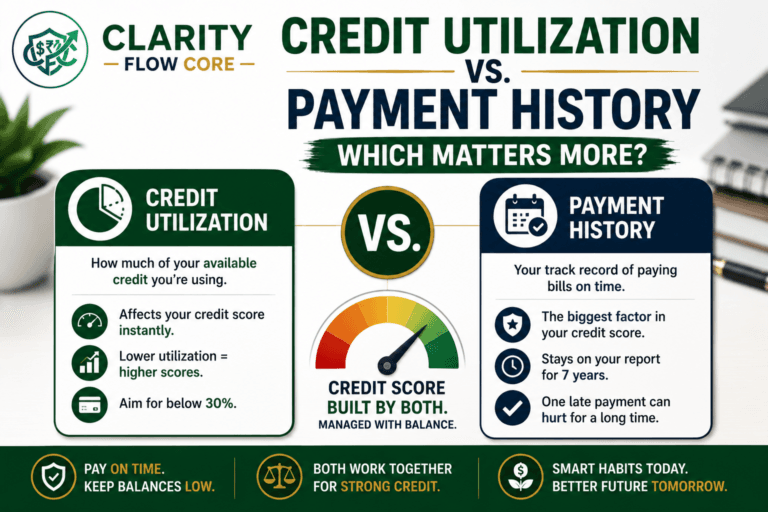

When you carry a high balance, your credit score can take a noticeable hit. According to Experian, one of the three major credit bureaus, your “Credit Utilization Ratio”—how much debt you owe compared to your total limits—makes up 30% of your FICO score. Experian and other financial authorities generally recommend keeping your credit utilization below 30% to maintain a healthy score.

If your cards are maxed out, your score will likely drop. This can make it harder to qualify for an apartment, secure a decent rate on an auto loan, or get approved for a mortgage down the road.

📈 Check Your Credit Utilization Risk

Credit utilization is one of the most influential credit score factors. Use our Credit Utilization Calculator & Recovery System to see where you stand and discover ways to improve your utilization ratio.

Beyond the score, debt carries a heavy emotional weight. It can create a persistent sense of stress that makes it difficult to enjoy your daily life or feel secure in your career.

Practical Solutions: How to Stop the Bleeding

If you have realized your balances are getting too high, the worst thing you can do is panic. You need to treat your finances methodically. Here is a practical, step-by-step protocol to start turning things around.

Step 1: The 30-Day Plastic Freeze

You cannot bail water out of a sinking boat if there is still a leak. Your first goal is to stop adding new charges to the pile.

Consider taking your physical credit cards out of your wallet for 30 days. Remove the card information from your digital wallets and food delivery apps. Operating strictly on a debit card or physical cash brings the “pain of paying” back into your daily routine, helping to naturally slow down impulsive spending.

Step 2: The Brutal Honesty Audit

You have to look at the exact numbers. Sit down, log into your accounts, and write down three specific things for every card you own:

- The Total Balance

- The Minimum Payment

- The Interest Rate (APR)

It might feel uncomfortable to see the total sum, but confronting the exact dollar amount is the necessary first step to building a realistic payoff plan.

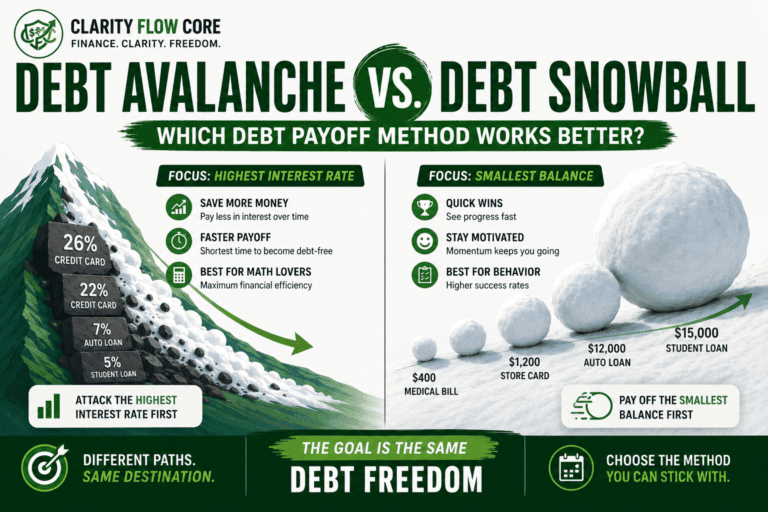

Step 3: Implement the Debt Avalanche

If you have multiple credit cards, throwing random amounts of cash at different accounts usually won’t make a dent. You need a structured approach.

The Debt Avalanche method is highly recommended by financial professionals because it saves you the most money. Here is how it works:

- Line up your debts starting with the card that has the highest interest rate (APR) at the top.

- Set all your other cards to Autopay for the exact minimum balance (to protect your credit score).

- Take any extra cash you have left in your budget and throw it entirely at that highest-interest card.

- Once that card is at $0, take that entire monthly payment and “avalanche” it down to the next highest card.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyStep 4: Consider a Balance Transfer

If your credit score is still in good shape (typically 680 or higher), you may qualify for a 0% APR Balance Transfer Credit Card.

This allows you to move your debt from your high-interest card to a new bank. The new bank will often charge a small transfer fee (usually 3% to 5%), but in exchange, they will pause your interest charges for 12 to 21 months. Without that 24% interest eating away at your payments, 100% of your money goes directly toward killing the principal balance.

Frequently Asked Questions (FAQs)

1. Should I close my credit card accounts after I pay them off? In many cases, no. Because part of your credit score is determined by the length of your credit history and your total available credit, closing an old account can sometimes temporarily hurt your score. A common strategy is to pay it off, put the physical card in a drawer, and let the open account quietly anchor your credit profile.

2. Can I negotiate my credit card interest rate? Yes, and it is usually free to try. You can call the customer service number on the back of your card and politely explain that you are experiencing hardship. Ask if they have any internal programs to lower your APR. They will sometimes offer a temporary rate reduction to keep your account in good standing.

3. Does checking my credit score lower it? No. Checking your own credit score through your bank or a monitoring app is classified as a “soft inquiry.” Soft pulls have absolutely no impact on your credit score.

4. Should I build an emergency fund while paying off debt? Yes. While it makes mathematical sense to pay off 24% interest debt as fast as possible, it is highly recommended to build a small cash safety net first (even just $500 to $1,000). If you don’t have any liquid cash, the next time you get a flat tire, you will be forced to swipe the credit card and start the cycle all over again. (If you are a freelancer or have variable income, you can read our guide on the best beginner budgeting method for irregular income to help stabilize this cash flow).

The Bottom Line

Getting caught in the credit card trap is a very common hurdle for young adults. The financial system can be confusing, and life is expensive.

If you are staring down a mountain of high-interest debt right now, try to let go of the guilt. Beating yourself up won’t pay the bills. Instead, grab a piece of paper, write down your realistic numbers, and start forming a plan.

Freeze your card usage temporarily, review your budget, and start executing the debt avalanche. It will require patience and likely a few temporary lifestyle adjustments. But the physical sense of relief you will feel the day your statement finally reads $0.00 is worth the effort. You have the ability to turn this around.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

Sources & References

Articles published on Clarity Flow Core are researched and reviewed using publicly available information from official government agencies, financial institutions, consumer protection organizations, credit bureaus, and trusted educational resources.

Reference sources may include:

- Internal Revenue Service (IRS)

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve

- U.S. Department of the Treasury

- Federal Trade Commission (FTC)

- Bureau of Labor Statistics (BLS)

- Federal Deposit Insurance Corporation (FDIC)

- Securities and Exchange Commission (SEC Investor.gov)

- Experian

- Equifax

- TransUnion

- myFICO

- AnnualCreditReport.com

- Official banking, lending, insurance, and financial institution websites

- Public consumer finance studies and educational resources

Additional editorial references may include reputable financial publications, academic research, behavioral finance studies, housing and credit market data, and publicly available consumer finance resources where relevant.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.