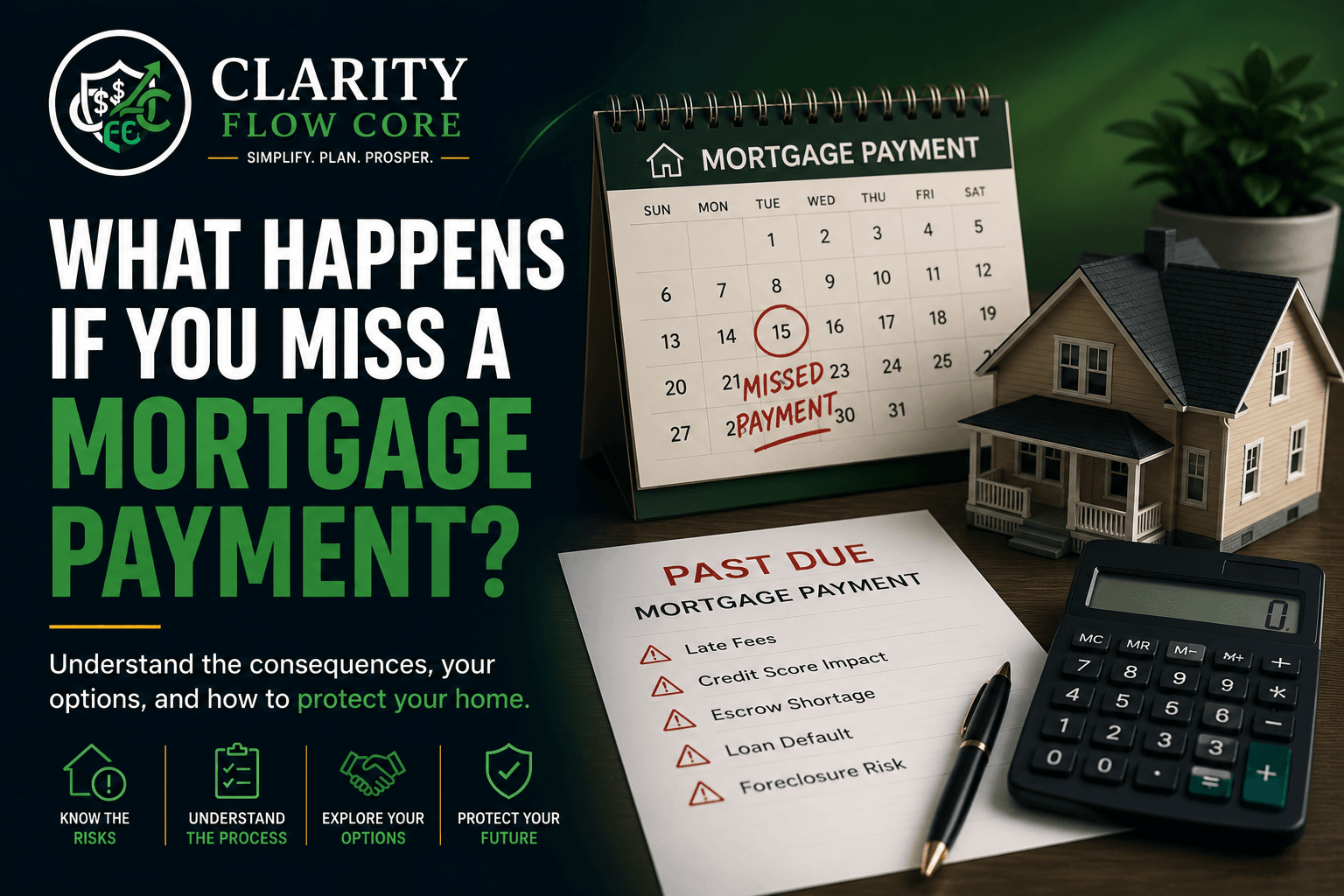

What Happens If You Miss a Mortgage Payment?

If you are suddenly wondering what happens if you miss a mortgage payment, you are not alone. You wake up, look at the calendar on your phone, and a cold wave of dread washes over you.

It didn’t. The math simply does not work this month.

Missing a mortgage payment is one of the most terrifying financial milestones a person can face. Your home is not just an asset; it is your safe harbor. It is where you sleep, where your family gathers, and where you are supposed to feel secure. The moment you realize you cannot pay for it, the anxiety is physical. You might start picturing moving boxes, eviction notices, and ruined credit.

If you are sitting there right now, silently panicking and wondering what to do next, take a deep breath.

We need to separate the emotional terror of losing your home from the actual, logistical reality of how the mortgage industry works. The bank is not going to show up tomorrow and change the locks. You have time, you have options, and you have federal rights.

This guide will walk you through exactly what happens when you miss a payment, the timeline you are actually working with, and the steps you need to take right now to protect your home and your peace of mind.

The Real Problem: The Fear of the Unknown

The biggest problem people face when they cannot pay their mortgage is the stories they tell themselves.

We are culturally conditioned to believe that banks are ruthless machines waiting to snatch our houses away the second we stumble. Because we are so afraid of this worst-case scenario, we freeze. We avoid opening the mail. We send phone calls from the mortgage servicer straight to voicemail.

But here is the reality of the banking business: Banks do not want your house.

Banks are in the business of collecting interest, not managing real estate. Foreclosing on a home, evicting the owners, hiring property managers, and putting the house up for auction is an incredibly expensive, time-consuming nightmare for a lender. They lose money on foreclosures.

In many cases, lenders prefer solutions that keep borrowers making payments rather than moving directly to foreclosure. Understanding that the bank actually wants to work with you changes the entire dynamic. You are not fighting an enemy; you are negotiating with a business partner who wants the same outcome you do.

Why Missing a Payment Happens to Normal People

There is a heavy stigma attached to missing a mortgage payment. People often feel a deep sense of shame, as if they have failed at being a responsible adult.

If you feel embarrassed, you need to let that go immediately. Most people do not fall behind on their mortgage because they are financially reckless. They fall behind because life threw a massive, expensive wrench into their plans.

- The Escrow Shock: Often, you didn’t do anything wrong at all. You paid your fixed-rate mortgage perfectly for a year, but then your local property taxes or insurance spiked, creating a massive shortage. (If you are completely blindsided by a massive, unexpected hike to your monthly bill, read our guide on Why Your Escrow Payment Increased Suddenly (And How to Fix It) to understand the math and fight back).

- Sudden Job Loss: Maybe you were unexpectedly laid off, and unemployment checks haven’t kicked in yet. If you are struggling to balance a sudden loss of income, you are in a highly stressful—but incredibly common—situation. (See our guide: I Lost My Job: A 30-Day Financial Survival Plan).

- Medical Emergencies: You had a medical emergency, and the out-of-pocket costs completely drained your savings. When you don’t have a reliable financial cushion, one bad month can put your housing at risk. (Review Emergency Fund Basics: How Much Cash Should You Keep?).

- Irregular Income: You are dealing with the harsh reality of self-employment. You could have a $5,000 invoice sitting out there, but the client is dragging their feet. Your money is coming, but it just won’t be in your checking account by the time the mortgage company wants their cut.

Cash flow crunches happen to incredibly smart, hardworking people every single day. The “why” doesn’t matter nearly as much as how you handle the “what next.”

The Timeline: What Happens If You Miss A Mortgage Payment

When you imagine missing a payment, you probably picture immediate disaster. The reality is that the mortgage timeline moves surprisingly slowly. Here is the actual, day-by-day breakdown of what happens when the money doesn’t leave your account on the first of the month.

Days 1 to 15: The Grace Period

Many traditional mortgages include a grace period, often around 15 days, but the exact terms vary by lender and loan agreement.

If your payment is due on the 1st, but you pay it on the 10th, you are generally not considered “late” in the eyes of the bank. You will not be charged a late fee, your credit score will not drop a single point, and nobody is going to call you.

If you are just waiting on a delayed paycheck or a late client invoice to clear, and you know you can pay within that window, you can take a deep breath. You are entirely fine.

Days 16 to 30: The Late Fee Era

If the 16th of the month rolls around and you still haven’t paid, the grace period is over. Now, a late fee is applied to your account.

Mortgage late fees are typically between 3% and 6% of your monthly payment. If your mortgage is $1,500, expect a penalty of around $45 to $90 to be tacked onto your balance.

During this window, your mortgage servicer will likely start calling you and sending letters. It is annoying, and the late fee hurts, but your credit score is still completely safe. The credit bureaus only care about debts that are a full 30 days past due.

Day 30: The Credit Score Hit

Once you pass the 30-day mark without making a payment, the situation escalates.

Your mortgage servicer will officially report your account as “30 Days Past Due” to Equifax, Experian, and TransUnion. This can significantly lower your credit score, especially if you previously had a strong payment history.

This drop will stay on your credit report for seven years, though the impact of it fades significantly as time goes on. It is incredibly important to review your credit report regularly to ensure the lender is reporting your dates accurately. (Learn more in How to Read and Fix Errors on Your Credit Report).

Day 31 to 120: The Danger Zone and Default

If you miss a second payment (60 days late) and a third payment (90 days late), your credit score will continue to take heavy damage.

At this stage, your lender will send you a “Demand Letter” or “Notice of Intent to Foreclose.” This letter sounds terrifying because it is. It legally informs you that you are in default and gives you a deadline (usually 30 days) to pay everything you owe, including all accumulated late fees, to bring the account current.

Day 120+: The Legal Foreclosure Process Begins

Under federal law, thanks to the Consumer Financial Protection Bureau (CFPB), a mortgage lender cannot legally start the official foreclosure process until you are more than 120 days delinquent on your loan.

That means you have four full months from your first missed payment to find a solution before the legal gears of foreclosure can even begin turning. You have time to fix this. If the situation goes entirely sideways and the bank later sells any remaining deficiency balance to collection agencies, you still have rights you can enforce. (See How To Handle Debt Collectors Without Making Things Worse).

3 Massive Mistakes You Cannot Afford to Make Right Now

When people are terrified of losing their homes, they often make impulsive decisions to find quick cash. These mistakes can permanently damage your financial future. Avoid these three traps at all costs.

1. Ghosting Your Lender

The worst possible thing you can do is ignore the phone calls and throw the letters from your mortgage company into the trash.

Lenders have dozens of hardship programs available, but they are completely optional. They do not have to offer them to you. If you go silent and refuse to answer the phone, the lender assumes you have abandoned the property or simply do not care. They will fast-track the foreclosure process.

If you pick up the phone and explain your hardship, they will assign you a mitigation specialist to figure out a plan. You must communicate.

2. Draining Your 401(k) or Retirement Accounts

When you are staring at a past-due mortgage, looking at the money sitting in your 401(k) is incredibly tempting. You think, I’ll just pull a few thousand out to save the house, and I’ll rebuild it later.

Do not do this.

If you withdraw money from a traditional retirement account before age 59½, the IRS will hit you with a massive 10% early withdrawal penalty. On top of that, the money you withdraw is taxed as regular income. If you pull $10,000 out to cover your mortgage, you might lose 30% of it instantly to taxes and penalties.

Furthermore, if the worst-case scenario happens and you do have to file for bankruptcy down the road, your retirement accounts are federally protected. Creditors cannot touch your 401(k). If you pull that money out and put it into your checking account, you just handed over your protected safety net.

3. Paying Unsecured Debt Over the Mortgage

If you only have $1,500 in your bank account, and your mortgage is $1,500, but you also have a $300 credit card bill and a $200 medical bill, where does the money go?

It goes to the mortgage. Always.

When you are in a financial crisis, you must protect your “Four Walls” first: Food, Housing, Utilities, and basic Transportation. Everything else is secondary.

A credit card company can yell at you. A medical billing office can send you to debt collectors. But they cannot evict you from your home. Never pay a credit card bill if it means you will bounce a mortgage check. (If you are drowning in minimum payments right now, use our tool below to build an aggressive plan to eliminate that consumer debt so you never have to choose between your credit cards and your house again).

Practical Solutions: How to Keep (or Transition Out of) Your House

So, you don’t have the money. You understand the timeline. Now, what are your actual options?

When you call your mortgage servicer, you are going to ask to speak to the “Loss Mitigation Department.” These are the employees who specialize in keeping people out of foreclosure. Here are the four most common solutions.

Option 1: Forbearance (The Temporary Pause)

If your financial hardship is temporary—like a short-term job loss, an unpaid medical leave, or a major freelance contract that was unexpectedly canceled—forbearance is your best friend.

A forbearance agreement temporarily pauses or reduces your mortgage payments for a set period, usually 3 to 6 months.

The Catch: Forbearance is not forgiveness. You still owe the money you paused. The exact repayment terms depend on the lender and the specific forbearance agreement. When the forbearance period ends, you have to pay the regular mortgage plus the amount you skipped. However, lenders rarely demand a lump sum. They will usually let you tack the missed payments onto the very end of your loan term, or spread them out over the next year.

Option 2: Repayment Plan

If you only missed one or two payments, but you are back on your feet and have steady income again, the lender will put you on a repayment plan.

Let’s say your mortgage is $1,000 a month, and you missed two payments (you are $2,000 in the hole). The lender might increase your monthly payment to $1,500 for the next four months. You pay your regular amount, plus a chunk of the past-due amount, until you are fully caught up.

Option 3: Loan Modification

If your financial situation has changed permanently—for example, you had to take a new job that pays $20,000 less than your old one, or your spouse passed away and you lost their income—a short-term pause won’t fix the problem. You need a permanent solution.

A loan modification actually changes the original terms of your mortgage to make the payment affordable again. The lender might lower your interest rate, extend the life of your loan from 30 years to 40 years, or roll your past-due balances into the principal. The goal is to drop your monthly payment to a number you can realistically afford on your new income.

Option 4: Sell the Property Before Foreclosure

Sometimes, the hardest but smartest financial decision you can make is walking away on your own terms.

If keeping the home is no longer realistic, selling before foreclosure may allow you to protect some equity, avoid severe credit damage, and move on with more financial control. In a strong housing market, you might be able to list the home, pay off the entire mortgage balance with the proceeds, and even walk away with cash in your pocket to start fresh. If you owe more than the home is worth, you can negotiate a “short sale” with the bank.

Your Beginner-Friendly Action Plan

If your head is spinning, stop looking at the massive mountain of debt and just look at the next step in front of you. If you know you are going to miss a payment, do these four things in the next 48 hours.

- Check your exact due date and grace period. Pull out your last mortgage statement or log into your portal. Confirm what day the late fee hits. If you just need a few extra days, use the grace period.

- Strip your budget down to the bare bones. Cancel every single subscription, pause all unnecessary spending, and stockpile cash. Pay only for groceries, basic utilities, and keeping your car running.

- Call your mortgage servicer immediately. Do not wait until the 30-day mark. Call them on day 5. Use this exact script: “Hi, my name is [Name] and my account number is [Number]. I have experienced a sudden drop in my income and I will not be able to make my full payment this month. I want to keep my home and keep my account in good standing. Can you connect me with your Loss Mitigation department to discuss hardship options like forbearance?”

- Document absolutely everything. Every time you talk to the bank, write down the date, the time, the name of the representative, and exactly what they told you. Keep a physical folder. If they promise to pause your late fees, tell them you need that agreement emailed or mailed to you in writing.

Frequently Asked Questions (FAQs)

Does a 3-day late payment hurt my credit score? No. Credit bureaus only record late payments in 30-day increments. If you pay on the 3rd, the 10th, or the 25th of the month, your credit score will not be impacted at all. You will likely just owe a late fee to the lender.

Can I ask the bank to waive my late fee? Yes! If you have a history of paying on time and this is your first offense, simply call customer service once you make the payment and politely ask for a “one-time courtesy waiver” of the late fee. Lenders will frequently say yes to keep a good customer happy.

Will a forbearance ruin my credit? Under normal circumstances, entering a forbearance program will show up on your credit report with a note that says “Account in forbearance.” While it is not a direct negative mark like a missed payment, future lenders may see it and hesitate to give you new credit until the forbearance is over. However, it is vastly better for your credit profile than letting your house go into foreclosure.

What happens if I just hand the keys back to the bank? This is called a “Deed in Lieu of Foreclosure.” You voluntarily sign the house back over to the lender to avoid the legal foreclosure process. While it is slightly faster and less stressful than a forced eviction, it will still devastate your credit score almost as heavily as a traditional foreclosure.

A Final Word of Encouragement

Sitting at your kitchen table, looking at a bank account balance that cannot cover the roof over your head, is a profoundly dark feeling. It makes you feel incredibly small and entirely alone.

But you are not alone, and this is not the end of your story.

Millions of Americans have missed mortgage payments, navigated the terrifying maze of loss mitigation, and come out the other side with their homes and their dignity intact. Your financial net worth has absolutely nothing to do with your value as a human being. A mortgage is just a contract written on paper. Your home is just wood, drywall, and nails.

Do not let the shame of a tight bank account prevent you from picking up the phone and asking the bank for the help you are legally entitled to. Take a deep breath, use the grace period if you need it, call the mitigation department, and tackle this one logical step at a time. You have more power than you think.

Sources & References

- Consumer Financial Protection Bureau (CFPB) – Trouble Paying Your Mortgage? – Learn about mortgage forbearance, foreclosure prevention, and the options available if you’re struggling to make your mortgage payments.

- U.S. Department of Housing and Urban Development (HUD) – Avoiding Foreclosure – Official guidance on foreclosure prevention, housing counseling, and homeowner assistance programs.

- Consumer Financial Protection Bureau (CFPB) – Find a HUD-Approved Housing Counselor – Connect with certified housing counselors who can help you understand your mortgage relief options and communicate with your lender.

- Fannie Mae – Homeowners in Financial Hardship – Educational resources explaining mortgage assistance, forbearance, repayment plans, and loan modifications.

- Freddie Mac – My Home by Freddie Mac – Learn about missed mortgage payments, foreclosure alternatives, and working with your loan servicer.

- Consumer Financial Protection Bureau (CFPB) – Mortgage Servicing Rules – Understand your rights when working with mortgage servicers, including federal foreclosure protections and servicing requirements.

Disclaimer: The information provided in this article is for educational and informational purposes only and should not be construed as professional financial, legal, or tax advice. Every individual’s financial situation is unique. Before making any major financial decisions, such as applying for new credit lines or taking on debt, consider consulting with a certified financial planner or qualified professional. Additionally, we want to be fully transparent: we may earn a commission if you click on or apply for products through some of the links on our site. You can read exactly How We Make Money and review our full site Disclaimer for more details.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.