How to Create a Sinking Fund for Irregular Expenses

You are checking your mail, and there it is: a bill for your annual car registration. It is $400, and it is due in three weeks. If you are like most people, your stomach drops. You did not budget for this. You look at your checking account, realize you do not have an extra $400 sitting around, and mentally prepare to put the expense on your credit card.

This cycle of financial panic is incredibly common, but it is completely avoidable. The solution is not making more money; the solution is changing how you plan for the expenses you know are coming.

That is where a sinking fund comes in. Instead of scrambling to pay for a large bill all at once, you set aside a small amount of money each month. By the time the bill is due, the money is already there, waiting to do its job.

In this guide, you will learn exactly how to create a sinking fund, why it is the secret to stopping credit card debt, and how to use this strategy to completely smooth out your budget.

⚡ Quick Answer

A sinking fund is money set aside for a specific future expense such as car repairs, holiday gifts, insurance premiums, or home maintenance. By saving a small amount each month, you can pay these bills in cash when they arrive without using credit cards or draining your emergency fund.

To visualize how this looks in practice, here is a quick breakdown of how standard irregular expenses translate into highly manageable monthly savings goals:

| Expense | Annual Cost | Monthly Savings Needed |

| Car Insurance | $1,200 | $100 |

| Holiday Spending | $900 | $75 |

| Car Repairs | $600 | $50 |

| Total | $2,700 | $225 |

What is a Sinking Fund?

At its core, a sinking fund is a dedicated savings bucket with a specific purpose and a specific timeline. You are sinking money into this fund over time so that when the expense arrives, it does not sink your budget.

Think of it as giving your money a highly specific job description. Instead of having a generic savings account where money gets easily blurred together, a sinking fund is earmarked for one clear purpose: “New Tires,” “Christmas 2026,” or “Home Owners Association Dues.”

The same strategy works exceptionally well if you’re preparing to move into your own place. Creating a dedicated moving fund for security deposits, moving costs, and basic furniture can make the transition much less stressful. See How Much Should You Save Before Moving Out on Your Own? to estimate your savings goal.

Sinking Fund vs. Emergency Fund

A common question from beginners is whether a sinking fund is just another name for an emergency fund. They are entirely different tools, and you need both to have a healthy financial foundation.

- Emergency Funds are for the unknown. You do not know when you might lose your job, or when a massive tree branch will fall on your roof. If you’ve already experienced a layoff and need to make those emergency savings last, I Lost My Job: A 30-Day Financial Survival Plan provides a step-by-step guide to prioritizing bills, preserving cash flow, and navigating the first month of unemployment. You use your emergency fund for unpredictable, catastrophic events. If you are unsure where your emergency savings stand, you can run your numbers through our Advanced Emergency Fund Analyzer to see if you have enough cash reserved for genuine surprises.

- Sinking Funds are for the known (or highly expected). You know Christmas happens on December 25th every year. You know your car will eventually need new brakes. You know your six-month car insurance premium is coming up. These are not emergencies; they are irregular expenses.

Using an emergency fund to pay for Christmas gifts is a fast track to financial vulnerability. Sinking funds protect your emergency fund from being drained by predictable life events.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetSinking Fund vs. Checking Account Buffer

Some people try to handle irregular expenses by simply keeping a “buffer” of extra cash in their primary checking account. While a buffer is great for avoiding overdraft fees, it is a terrible strategy for large, irregular expenses.

When money sits in a checking account without a specific label, human psychology takes over. You log into your banking app, see a high balance, and feel artificially wealthy. You might decide to treat yourself to a nice dinner out, forgetting that $600 of that balance is supposed to pay for your dog’s annual vet visit next month. Sinking funds separate the money so you cannot accidentally spend it on pizza.

How to Create a Sinking Fund in 5 Steps

Setting up your first sinking fund is simple. We will walk through the math and the logistics using a real-world scenario.

Step 1: Identify Your Categories

Do not try to set up twenty sinking funds on your first day. Start by looking at the next 12 months. What are the three largest irregular expenses you know are coming? List them out.

Step 2: Estimate the Total Cost and Timeline

For each category, determine how much money you need and exactly when you need it. Do not guess; look at last year’s bank statements or call your service providers to get accurate numbers.

Example Scenario:

- Christmas: You want to spend $900. You need the money in 10 months.

- Vacation: You want to spend $1,500. You are leaving in 6 months.

- Auto Insurance: Your premium is $600. It is due in 3 months.

Step 3: Calculate Your Monthly Contribution

Take the total target amount and divide it by the number of months you have left to save.

Example Scenario:

- Christmas: $900 / 10 months = $90 per month.

- Vacation: $1,500 / 6 months = $250 per month.

- Auto Insurance: $600 / 3 months = $200 per month.

You need to add $540 per month to your budget to fully fund these three upcoming expenses. If you look at your budget and realize you do not have $540 of free cash flow, you have a choice to make now, rather than panicking later. You can either reduce your vacation budget, plan to spend less on Christmas, or look for ways to increase your income. If you are planning to finance a home or take out a large loan soon, ensuring your monthly obligations fit within your income is critical. Run a full assessment using our Debt-to-Income Analyzer & Loan Readiness Planner.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI RatioStep 4: Choose the Right Place to Keep Your Money

Where should you actually put this money? The goal is to keep the money separate from your daily checking account while keeping it easily accessible.

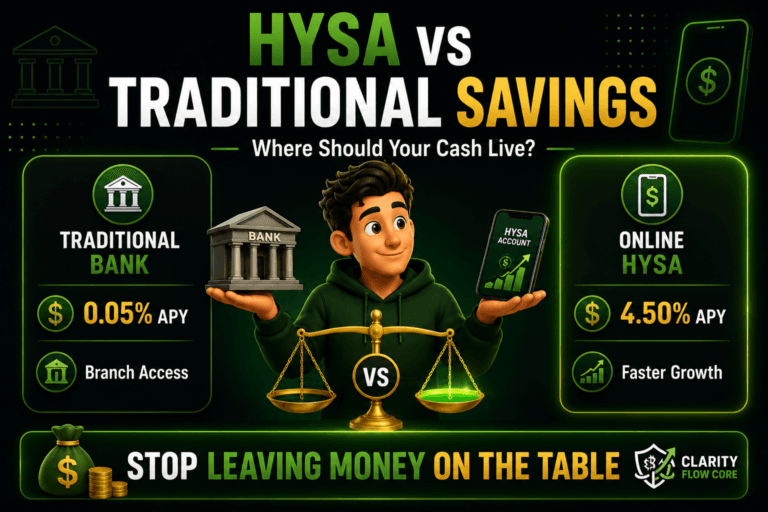

- High-Yield Savings Accounts (HYSA): This is the best option for most people. HYSAs pay significantly higher interest rates than traditional brick-and-mortar banks, meaning your money grows while it waits to be used. Many online banks allow you to open multiple sub-accounts or “buckets” under one main account.

- Cash Envelopes: If you struggle with overspending digital money, pulling out physical cash and putting it in an envelope marked “Groceries” or “Gifts” is a highly effective psychological tool.

- Money Market Accounts: Similar to an HYSA, but they often come with a debit card or check-writing privileges, which makes it easier to pay a mechanic directly from the fund.

Do not put sinking funds into the stock market. Because you need this money on a specific, short-term timeline, you cannot risk the market dropping 15% the week before your car insurance is due.

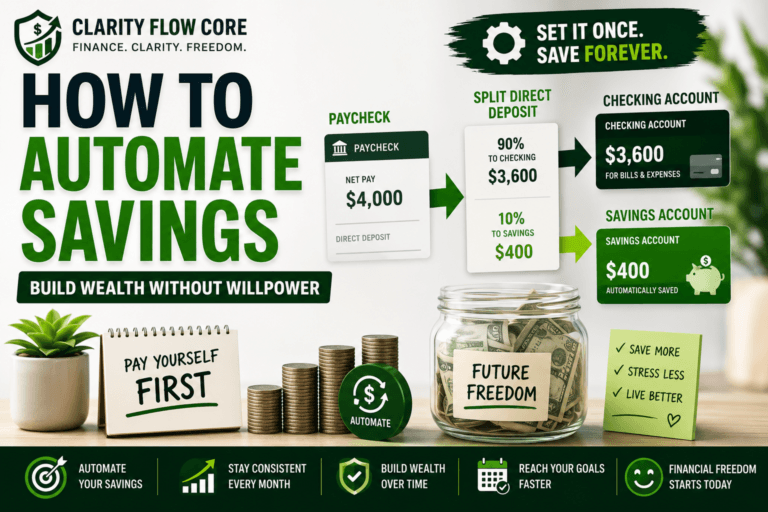

Step 5: Automate Your Savings

Do not rely on willpower to fund your irregular expenses. Willpower is finite; automation is foolproof.

Once you know your monthly target, set up an automatic transfer from your checking account to your sinking fund. Have the transfer pull the day after your paycheck clears. Treat your sinking fund contribution like a non-negotiable bill.

Best Sinking Funds to Start First

If you are wondering where to begin, focus on the categories that catch people off guard the most. Here are the best sinking funds for beginners:

- Car Repairs: Even reliable cars need new tires, brakes, and batteries. Aim to save at least $50 to $100 a month for inevitable maintenance.

- Annual Insurance Premiums: Paying your auto, home, or life insurance annually or semi-annually usually comes with a significant discount. Save monthly so you can pay in full.

- Holiday Spending: Christmas arrives on December 25th every year. Decide on your budget in January and divide it by 11 or 12 months.

- Home Maintenance: The rule of thumb is to save 1% to 4% of your home’s value each year for repairs. A broken HVAC or leaky roof shouldn’t be a financial disaster.

- Medical Expenses: Even with insurance, deductibles and copays add up. A medical fund covers prescription costs, dental work, and new glasses.

- Pet Care: Annual vet visits, flea and tick medication, and emergency health issues are a guaranteed part of pet ownership.

Why It Works

Implementing sinking funds is one of the fastest ways to take control of your financial life. Here is how they fundamentally change the way you manage money.

1. They Break the Credit Card Cycle

Most credit card debt does not come from luxury purchases. It comes from death by a thousand cuts—the $300 dental bill, the $500 back-to-school shopping trip, the $800 set of new tires. When you do not have sinking funds, these irregular expenses end up on high-interest credit cards. If you are currently trying to dig your way out of this cycle, our Credit Utilization Calculator & Recovery System can help you map out a strategy to pay down existing balances. Sinking funds ensure you never have to add to those balances again.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My Utilization2. They Eliminate Budget Guilt

Have you ever booked a vacation and spent the entire trip feeling guilty about the money you were spending? When you use a sinking fund, you have permission to spend. You spent twelve months systematically saving $2,000 for a trip. When it is time to go, you can enjoy every dollar completely guilt-free because the money was specifically saved for that exact purpose.

3. They Make Your Monthly Budget Predictable

If you only budget for your regular monthly bills, your budget is going to “fail” almost every month because life is full of irregular expenses. By incorporating sinking funds, you take an irregular $1,200 annual expense and turn it into a predictable $100 monthly line item. This makes tracking your cash flow using tools like our Financial Freedom Planner much more accurate.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanReal-World Examples of Irregular Expenses

Beyond the beginner funds, here are a few other irregular expenses that you might want to consider as you build out your financial system.

Family and Personal Life

- Gifts: Birthdays, weddings, baby showers, and anniversaries.

- Back-to-School: New clothes, supplies, technology, and activity fees.

Professional and Freelance Costs

- Taxes: Setting aside quarterly estimated taxes if you have a side hustle.

- Licenses and Subscriptions: Annual software renewals (like Adobe or Microsoft), professional licensing fees, union dues.

Common Mistakes When Building Sinking Funds

Watch out for these frequent mistakes when setting up your new system.

- Creating Too Many Categories: If you have 35 different sinking funds for every tiny possibility, you will make yourself crazy. Consolidate smaller, similar items. Instead of separate funds for tires, oil changes, and registration, just have one “Auto Maintenance” fund.

- Raiding Funds for the Wrong Reason: If you see $1,000 sitting in your “Home Repair” fund, it is tempting to use it to buy concert tickets. Be disciplined. If you borrow from a sinking fund, you are stealing from your future self.

- Forgetting to Replenish: Sinking funds are cyclical. You save up, you spend the money, and then the balance goes to zero. Do not stop the automatic transfers.

- Confusing Sinking Funds with Wealth Building: Sinking funds are a defensive strategy to protect your cash flow and keep you out of debt. They are not investments. Once your sinking funds are adequately funded, direct your extra cash flow toward true wealth-building activities. If you want to see how managing your debt and credit impacts your long-term wealth, check out our Credit Score Simulator & Improvement Planner.

Simulate Your Future Credit Score

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our free simulator.

Launch Credit SimulatorFrequently Asked Questions

How much money should be in a sinking fund?

There is no universal dollar amount. The total depends entirely on your specific upcoming expenses. If you are saving for a $600 car repair and a $1,000 vacation, your total sinking fund goal for those categories is $1,600. The math is highly individual.

Can I keep my sinking fund and emergency fund in the same account?

Technically yes, but it is risky. If you keep them in the same account, you must be incredibly disciplined to track exactly which dollars belong to emergencies and which belong to upcoming bills. It is highly recommended to keep them in separate accounts or distinct “buckets” to avoid accidental spending.

What is the difference between a sinking fund and a savings account?

A savings account is the actual financial product provided by a bank. A sinking fund is the strategy or the job you give to the money inside that account. You use a savings account to house your sinking fund.

Should I pay off debt or fund sinking funds first?

You should do both simultaneously. If you aggressively pay off debt but ignore upcoming irregular expenses, you will be forced to use credit cards when a $500 car repair hits, putting you right back into debt. Fund your absolute necessary sinking funds while making extra payments on your debt.

Is a sinking fund taxable?

The money you put into the fund is already yours, so transferring it does not trigger taxes. However, if you keep your sinking fund in an interest-bearing account like a High-Yield Savings Account, the interest you earn is considered taxable income by the IRS.

What if I do not know exactly how much an expense will cost?

Make your best educated guess. Look at historical data (what did you spend on Christmas last year?) or get a quote. It is always better to over-save and have extra money left over than to under-save and scramble.

Conclusion

Irregular expenses are a fact of life. Cars break down, property taxes are due, and the holidays arrive on the exact same date every single year. The anxiety associated with these events does not come from the expenses themselves; it comes from a lack of preparation.

By taking the time to set up sinking funds, you are taking proactive control of your financial narrative. You transition from reacting to your bills to anticipating them. Start small. Pick just two or three categories, run the math, and automate your first transfer today. Keep planning, stay disciplined, and watch your financial stress disappear.

Next Steps

If you have built your sinking funds, your next priorities should be:

- Building a full emergency fund

- Automating your savings

- Eliminating high-interest debt

- Increasing your savings rate

Related Guides:

- Emergency Fund Basics

- How to Automate Savings Using Split Direct Deposit

- Debt Avalanche vs Debt Snowball

- HYSA vs Money Market Account

References and Resources

To ensure you have the most accurate and up-to-date information, we recommend exploring these official financial resources:

- Consumer Financial Protection Bureau (CFPB): The CFPB offers excellent, unbiased guidance on setting up savings goals and protecting your money. Visit the CFPB guide on building savings.

- Federal Deposit Insurance Corporation (FDIC): When choosing a bank for your sinking funds, always ensure it is FDIC-insured. This guarantees your deposits up to $250,000 per depositor. You can learn more about how deposit insurance works directly from the source. Visit the FDIC website.

- Internal Revenue Service (IRS): If you are setting up sinking funds for freelance taxes or want to understand how the interest earned on your savings account is taxed, review official IRS guidelines on interest income. Review IRS Publication 550.

- Federal Reserve: To understand the broader economic environment and why High-Yield Savings Account interest rates fluctuate based on federal policy, the Federal Reserve provides extensive educational materials. Explore Federal Reserve Education.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.