How Much House Can You Afford on a $50K, $75K, or $100K Salary?

If you are thinking about buying a home, you have probably spent a few late nights scrolling through real estate listings. You look at a nice house, check the price tag, and then immediately ask yourself the most stressful question in personal finance: How much house can I afford on my salary?

When you see home prices sitting at $300,000, $400,000, or more, it is incredibly easy to feel priced out of the market. You start doing mental math, comparing your monthly take-home pay to estimated mortgage payments, and the numbers can quickly feel overwhelming.

But guessing is a dangerous game when it comes to a 30-year financial commitment. Lenders do not guess. They use specific mathematical formulas to decide exactly how much money they are willing to lend you. If you want to buy a house, you need to stop guessing and start running the exact same math the banks use.

This guide will break down exactly how much house you can realistically afford if you earn $50,000, $75,000, or $100,000 a year. We will walk through the real-world math, explain the hidden costs that shrink your buying power, show you how your existing debts impact your approval, and give you a concrete action plan to prepare for closing day.

The 28/36 Rule: How Banks View Your Salary

Before we look at specific salaries, you need to understand the golden rule of mortgage lending: the 28/36 rule.

When you apply for a mortgage, the underwriter (the person at the bank who approves or denies your loan) uses this rule to determine if you make enough money to safely cover the payments.

The Front-End Ratio: 28%

The front-end ratio focuses entirely on your housing costs. Lenders generally want your total monthly housing payment to be no more than 28% of your gross monthly income (your income before taxes are taken out).

If you’re unsure whether spending 28% of your income on housing is actually right for your situation, read How Much of Your Income Should Go Toward Housing Costs? for a deeper look at how this guideline applies to different budgets and financial goals.

Your total housing payment is not just the loan itself. It includes:

- Principal (paying down the loan balance)

- Interest (the cost of borrowing the money)

- Property Taxes

- Homeowners Insurance

- Private Mortgage Insurance (PMI) if you put down less than 20%

- HOA fees (if applicable)

The Back-End Ratio: 36%

The back-end ratio focuses on your overall debt. This is also known as your Debt-to-Income (DTI) ratio. Lenders generally want your new housing payment plus all of your minimum monthly debt payments (student loans, car loans, credit cards) to be no more than 36% of your gross monthly income.

Note: While 36% is the conservative standard for a highly affordable conventional loan, many lenders will push this limit to 43%, and government-backed programs like FHA loans might even allow a DTI up to 50% if you have a strong credit score. However, pushing your budget to the absolute maximum limit is a fast track to becoming “house poor”.

To test your own numbers safely, you can use our Debt-to-Income Analyzer & Loan Readiness Planner to see exactly where your ratios stand right now.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI RatioThe Reality of Buying on a $50,000 Salary

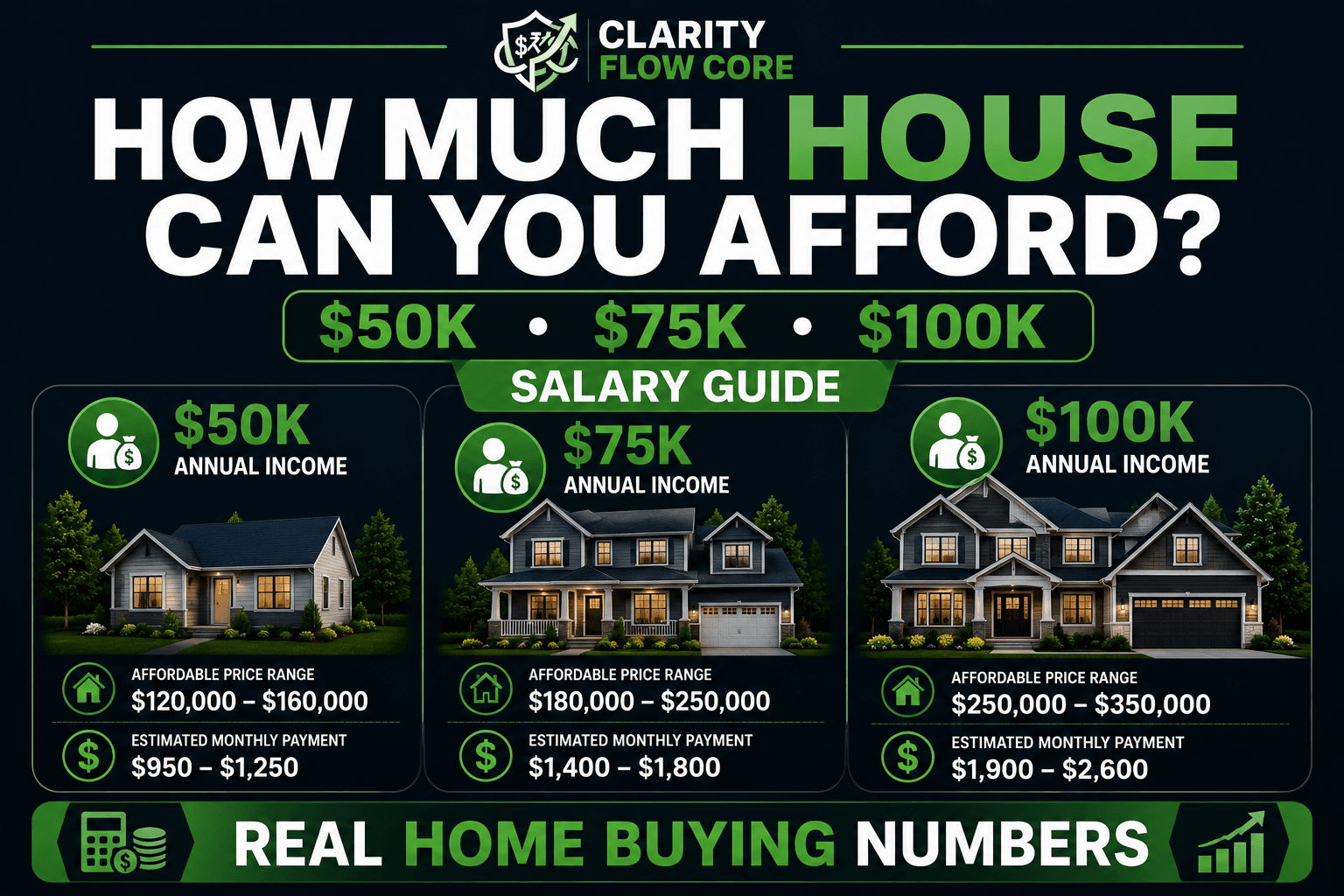

Earning $50,000 a year translates to a gross monthly income of roughly $4,166. Let’s run this through the 28/36 rule to see your true buying power.

- Maximum Housing Payment (28%): $1,166 per month.

- Maximum Total Debt (36%): $1,500 per month.

The Math in Action

If your total debt limit is $1,500 and your housing limit is $1,166, that leaves you with just $334 a month for other debt. If you have a $400 monthly car payment and $150 in student loans, you are already over your back-end limit. To get approved, the bank will force you to buy a cheaper house so your overall DTI drops back into the safe zone.

What Home Price Does This Equal?

Assuming you have zero outside debt, a 6.5% interest rate, a 5% down payment, and average property taxes and insurance, a maximum monthly payment of $1,166 translates to a home price of roughly $140,000 to $160,000.

Your Strategy

Buying a traditional single-family home on a $50,000 salary is challenging in many major US cities today. Your best strategy is to look into government-backed programs like FHA or USDA loans, which offer more forgiving debt-to-income limits and lower down payment requirements. You should also heavily consider buying a starter condo, a townhome, or exploring house-hacking (buying a duplex, living in one side, and renting out the other).

The Reality of Buying on a $75,000 Salary

Earning $75,000 a year translates to a gross monthly income of roughly $6,250. Let’s run the 28/36 rule for this income bracket:

- Maximum Housing Payment (28%): $1,750 per month.

- Maximum Total Debt (36%): $2,250 per month.

The Math in Action

At $75,000, you have significantly more breathing room. The bank allows you to spend up to $2,250 on total debt. If your housing payment maxes out at $1,750, you still have $500 a month allowable for a car payment or student loans without it damaging your mortgage approval.

What Home Price Does This Equal?

Assuming you have manageable debt (under $500/month), a 6.5% interest rate, a 5% down payment, and standard taxes and insurance, a $1,750 monthly payment allows you to shop for homes in the $230,000 to $260,000 range.

Your Strategy

At this salary, you are a strong candidate for first-time homebuyer Conventional loan programs (like Fannie Mae HomeReady), which allow for a 3% down payment and reduced mortgage insurance costs. However, you need to be incredibly careful with your credit. A lower credit score will result in a higher interest rate and expensive Private Mortgage Insurance (PMI), which will rapidly eat up that $1,750 monthly budget and force you to buy a cheaper house.

Before applying, take a minute to optimize your credit profile using our Credit Score Simulator & Improvement Planner.

Simulate Your Future Credit Score

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our free simulator.

Launch Credit SimulatorThe Reality of Buying on a $100,000 Salary

Earning $100,000 a year translates to a gross monthly income of roughly $8,333. Let’s run the 28/36 rule for a six-figure salary:

- Maximum Housing Payment (28%): $2,333 per month.

- Maximum Total Debt (36%): $3,000 per month.

The Math in Action

With $3,000 in allowable total monthly debt, you can carry a couple of car payments and standard student loans and still easily qualify for a substantial mortgage.

What Home Price Does This Equal?

Assuming a 6.5% interest rate, a 10% down payment, and average taxes and insurance, a $2,333 monthly payment puts your home shopping budget squarely in the $330,000 to $370,000 range.

Your Strategy (And The “House Poor” Trap)

When you make $100,000, banks are very eager to lend you money. Because you have a high income, many lenders will ignore the conservative 36% back-end limit and approve you up to a 45% or even 50% DTI. They might hand you a pre-approval letter for $450,000.

Do not max out your pre-approval. Just because the bank says you can spend $4,000 a month on a mortgage does not mean you should. The bank calculates your limits based on your gross income before taxes. They do not care about your 401(k) contributions, your daycare bills, your grocery budget, or your desire to take a vacation once a year. If you max out your pre-approval, you will become classic “house poor”—living in a beautiful home but completely stressed out every time a utility bill arrives.

Use our Financial Freedom Planner to map out your long-term wealth goals before committing to a massive mortgage payment.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanWhy Your Salary Isn’t the Only Number That Matters

Your salary sets the ceiling for what you can afford, but three other massive factors can bring that ceiling crashing down.

1. Existing Debt Obligation

As we saw in the math above, your car loans, student loans, and credit card minimums directly cannibalize your borrowing power. Every $100 you owe in monthly debt payments is roughly $100 less you can spend on a mortgage. If you want to afford a more expensive house on your current salary, the fastest way to do it is to aggressively pay down your consumer debt before applying for the loan.

2. Your Credit Score

Your credit score dictates your interest rate. If you have a 760 credit score, you get the bank’s best rate. If you have a 630 credit score, the bank views you as a higher risk and charges you a higher interest rate and more expensive mortgage insurance.

That higher interest rate increases your monthly payment. If your monthly payment goes up, it hits that 28% salary cap much faster, forcing you to look at cheaper homes. Simply improving your credit score from “Fair” to “Excellent” can increase your buying power by tens of thousands of dollars without you having to earn a single extra dollar at your job.

3. Your Cash Reserves

Affording a house is not just about the monthly payment; it is about having the cash to close the deal and survive homeownership. You need cash for:

- The Down Payment: Typically 3% to 5% for first-time buyers.

- Closing Costs: An additional 2% to 5% of the loan amount just to process the paperwork. For a full breakdown, read our guide on Closing Costs Explained: What Home Buyers Actually Pay.

- The Emergency Fund: When the HVAC breaks a month after you move in, the landlord isn’t going to fix it. You are.

Never drain your bank account to zero to buy a house. Ensure you have a post-purchase safety net mapped out using the Advanced Emergency Fund Analyzer.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings Target5 Common Mistakes Buyers Make When Budgeting

1. Forgetting About Property Taxes and Insurance

A $300,000 mortgage does not cost the same in New Jersey as it does in Alabama. High property taxes and expensive homeowners insurance (especially in coastal or flood-prone areas) can add hundreds of dollars to your monthly payment, completely blowing up your 28% housing ratio.

2. Financing Furniture Before Closing

You get approved for the house, you get excited, and you run to a store to finance a new living room set on a “0% for 12 months” credit card. This adds a new debt payment to your profile. The lender checks your credit one last time before closing day, sees your DTI has spiked past the limit, and denies your mortgage. Do not take on new debt until the keys are in your hand.

3. Relying Solely on “Rule of Thumb” Calculators

Generic calculators tell you that you can afford “3x your income”. This is terrible, outdated advice. It ignores current interest rates, ignores your personal debt, and ignores local taxes. You must run your specific scenario using a detailed tool like the Mortgage Affordability Calculator & Home Buying Planner.

How Much House Can You Actually Afford?

Stop guessing your home buying budget. Instantly calculate your realistic price range, estimated monthly payments, and overall loan readiness based on your exact income and debts.

Calculate My Buying Power4. Ignoring the Cost of PMI

If you put down less than 20%, you will pay Private Mortgage Insurance (PMI) or FHA Mortgage Insurance Premiums (MIP). This is an insurance policy that protects the lender, but you pay for it. It can easily add $100 to $300 to your monthly payment.

5. Using Expected Bonuses as Income

If your base salary is $75,000, but you usually get a $10,000 end-of-year bonus, do not assume the bank will calculate your income at $85,000. Unless you have a two-year history of consistently receiving that exact bonus, underwriters will likely exclude it from your qualifying income.

Your Home Buying Action Plan

Ready to stop guessing and start preparing? Follow these exact steps to lock in your true home buying budget.

- Step 1: Calculate Your True DTI: Sit down and list out your gross monthly income and your minimum monthly debt obligations. Find out exactly how much “room” you have left before hitting that 36% to 43% ceiling.

- Step 2: Check Your FICO Scores: Pull your official mortgage FICO scores. Do not rely on the free educational apps on your phone; mortgage lenders use older, stricter FICO models. If your score is below 620, pause your home search and focus on paying down credit card balances first.

- Step 3: Save for Closing Costs, Not Just the Down Payment: If your goal is to save $15,000 for a down payment, increase your savings goal to $25,000. You will absolutely need that extra buffer for lender fees, title insurance, property tax prepayments, and moving costs.

- Step 4: Get a Hard Pre-Approval: A pre-qualification from a website is just a guess. To find out exactly how much house you can afford, submit your W-2s, pay stubs, and bank statements to a licensed mortgage broker and get an official pre-approval letter.

Frequently Asked Questions (FAQs)

What is a good Debt-to-Income (DTI) ratio for buying a house? A highly safe, conservative DTI is 36% or lower. Most conventional lenders prefer to see your DTI below 43%. While some government-backed loans (like FHA) will allow you to push your DTI up to 50% with strong credit, doing so leaves you with very little disposable income for emergencies or retirement investing.

Do I really need a 20% down payment? No. This is one of the most common myths in real estate. First-time buyers can frequently qualify for Conventional loans with just 3% down, and FHA loans require just 3.5% down. If you qualify for a VA loan or a USDA loan, you can actually buy a home with 0% down.

Does my credit card limit affect how much house I can afford? Your credit limits themselves do not hurt your application, but your Credit Utilization (how much of that limit you are using) does. If your credit cards are maxed out, your credit score will drop, resulting in higher interest rates. Additionally, the minimum monthly payment on those maxed-out cards will count against your DTI, reducing your borrowing power.

Can I afford a $400k house on a $100k salary? It is possible, but tight. If you have absolutely zero other debt, excellent credit, and low property taxes, your monthly payment on a $400,000 house (with 10% down) will likely land around $2,600 to $2,800. This pushes you past the conservative 28% front-end ratio, but many lenders will still approve it. However, it will consume a large portion of your take-home pay.

How do student loans affect my mortgage approval? Student loans count directly against your back-end DTI ratio. Even if your loans are in deferment or on an Income-Driven Repayment (IDR) plan, the mortgage underwriter is required to use a specific formula (often 0.5% to 1% of the total loan balance) as your assumed monthly payment to ensure you can still afford the house when the student loans resume.

Should I pay off my car before buying a house? Mathematically, yes. Paying off a $400/month car loan frees up $400 a month in your DTI ratio. That $400 increase in your monthly budget can instantly give you the borrowing power to afford an extra $50,000 to $60,000 in home price.

What happens if I change jobs right before buying a house? Lenders want to see a stable, two-year work history. If you change jobs within the same industry for equal or higher pay, it is usually fine, though the underwriter will demand an offer letter and your first pay stub. If you switch from a salaried W-2 job to starting your own freelance business, your mortgage will likely be denied until you have two years of self-employed tax returns to prove your income is stable.

Conclusion: How much house can I afford on my salary

Figuring out how much house you can afford is often a reality check. Seeing how your salary translates into a maximum purchase price can sometimes feel discouraging, especially in a competitive housing market.

But understanding the math is empowering. When you know exactly how the 28/36 rule works, you stop relying on hopeful guesses and start making strategic financial decisions. You realize that paying off a car loan, negotiating a lower interest rate, or saving up a slightly larger down payment puts you entirely in the driver’s seat.

Do not let the banking process intimidate you. Control what you can control. Use the tools available to you, aggressively pay down your consumer debt, and protect your credit score. You are entirely capable of navigating this math, and with a little bit of preparation, you will be ready for closing day.

References & Trusted Resources

When you are making a massive financial decision, you should rely on facts from trusted authorities. The math and guidelines in this article are based on standards set by the following entities:

- Consumer Financial Protection Bureau (CFPB): The federal agency that provides unbiased guidelines on safe Debt-to-Income limits and mortgage estimates.

- Federal Housing Administration (HUD/FHA): The government body that sets the standard 3.5% down payment rules and DTI limitations for FHA borrowers.

- Fannie Mae / Freddie Mac: The government-sponsored enterprises that set the baseline underwriting guidelines (like the 28/36 rule) for conventional mortgages in the United States.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.