How Much Does Credit Utilization Affect Credit Score?

If you are wondering exactly how much credit utilization affect credit score, you are not alone. You might feel like you are doing everything right—paying rent on time, never missing a car payment, and always paying your credit card bill before the due date.

Instead of seeing the steady progress you expect, your score has suddenly dropped 35 points. Your heart skips a beat. You immediately check your credit report, terrified that someone stole your identity or a medical bill went to collections.

But there is no identity theft. There is no missed payment. The only alert on your file says: “Your credit card balance increased.”

You stare at the screen in complete disbelief. You used your card to book a flight for your sister’s wedding, but you had the cash sitting in your checking account, fully prepared to pay the card off on payday. Why in the world is the credit bureau punishing you for spending money you actually have?

Welcome to the incredibly frustrating reality of credit utilization.

When you are working hard to build a solid financial foundation, watching your credit score tank because of a temporary balance feels incredibly unfair. It feels like you are playing a high-stakes game where the banks are hiding the rulebook.

Let’s pull the curtain back. We are going to look at exactly how much weight this one factor carries, why the credit bureaus care so much about your balance, and the practical steps you can take to control your score starting today.

⚡ Quick Answer

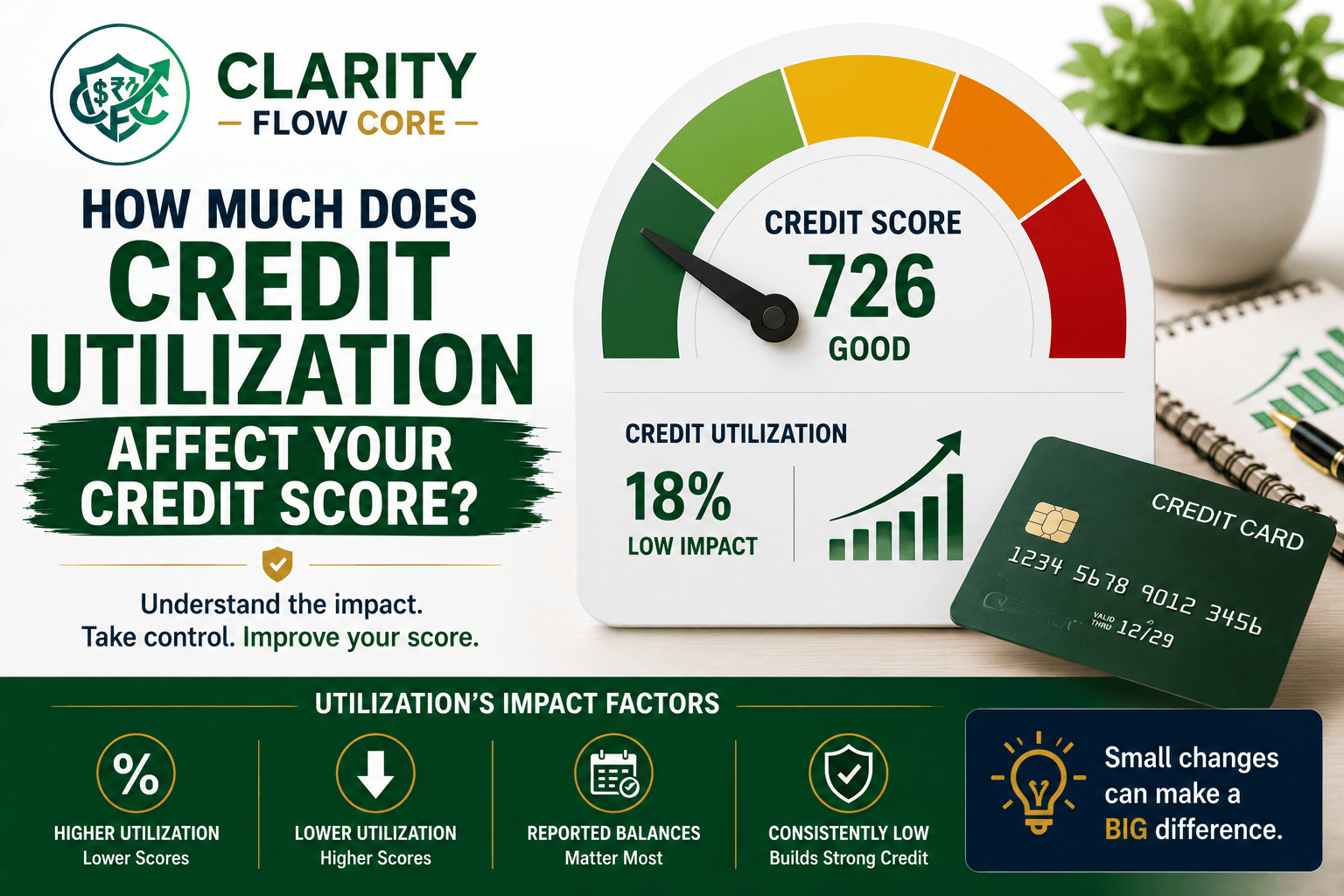

Credit utilization accounts for approximately 30% of your FICO score and is one of the fastest-changing factors in credit scoring. High utilization can significantly lower your score, while reducing balances can often lead to noticeable improvements within a short period of time.

| Credit Score Factor | Weight | How It Affects You |

| Payment History | 35% | Do you pay your bills on time? |

| Credit Utilization | 30% | How much of your available credit are you using? |

| Length of Credit History | 15% | How long have your accounts been open? |

| Credit Mix | 10% | Do you have different types of loans? |

| New Credit | 10% | How many new accounts have you opened recently? |

The Real Problem: The Hidden 30% Weight

To understand why your score fluctuates so wildly, you have to understand how the grading rubric works.

Most people assume that building a good credit score is simply about being a responsible person. You borrow money, you pay it back, and the banks reward you with a high score. But your credit score is not a loyalty program. It is a highly sensitive mathematical algorithm designed to predict risk.

The FICO scoring model—which is the model used by 90% of top lenders—breaks your financial behavior into five categories. As you can see in the table above, Payment History is the undisputed king at 35%. If you miss a payment, your score crashes. That makes logical sense to most of us.

But sitting right behind it, carrying a massive 30% of the weight, is your credit utilization ratio.

Together, your payment history and your utilization make up nearly two-thirds of your entire credit score. You could have a credit history spanning twenty years, a perfect mix of mortgages and auto loans, and zero new credit inquiries. But if your credit cards are maxed out, your score will still plummet.

This is the real problem that catches so many beginners and young adults off guard. You can have a flawless payment history, but if you don’t understand the math of utilization, your score will remain trapped in the “fair” or “average” zone.

Why It Happens: The Math Behind the Curtain

Let’s break down exactly what credit utilization is and why the algorithm obsesses over it.

Your credit utilization ratio is the amount of revolving credit you are currently using divided by the total amount of revolving credit you have available.

If you’re new to credit utilization and want a complete beginner-friendly explanation of how this ratio is calculated and why lenders pay so much attention to it, What Is Credit Utilization — And Why Does It Matter? covers the fundamentals in greater detail.

Let’s say you have one credit card. The bank gave you a $5,000 credit limit. This month, you used the card to pay for some car repairs and a few grocery trips, bringing your current balance to $2,500.

You divide $2,500 by $5,000, which equals 0.50. Your credit utilization is 50%.

Why does the algorithm care? To a computer, a high balance is a flashing warning sign of financial distress.

Statistically speaking, when people start using a large percentage of their available credit, they are more likely to default on their payments in the near future. The algorithm assumes that if you are using 80% of your credit limit, you might be out of cash and relying on credit cards to survive.

Even if you are completely financially stable and just wanted the airline miles for a big purchase, the computer doesn’t know that. It only sees the math. The higher the ratio, the riskier you look. The riskier you look, the lower your score drops. (Read more: The 30% Credit Utilization Myth: What Actually Matters?).

Common Mistakes People Make with Utilization

Because financial literacy isn’t taught in most schools, millions of people end up making totally avoidable mistakes that accidentally trash their utilization ratios. Here are the most common traps you need to watch out for.

Mistake 1: Closing old credit cards

Let’s say you finally pay off a credit card that has been hanging over your head for years. Out of sheer relief, you call the bank and cancel the card so you never use it again.

The next month, your credit score drops 40 points. Why? Because you just destroyed your available credit limit.

Imagine you had two cards, each with a $5,000 limit, giving you $10,000 in total available credit. You have a $2,000 balance on one card. Your utilization is a healthy 20%.

If you close the empty card, your total limit suddenly drops to $5,000. That exact same $2,000 balance is now taking up 40% of your available credit. You didn’t spend a single extra dime, but your utilization doubled, and your score tanked.

Mistake 2: Waiting for the due date to pay

This is the most frustrating trap for responsible spenders. You buy a $1,500 laptop on your card and pay it off completely on your due date. But your score still drops.

This happens because banks do not report your balance to the credit bureaus on your due date. They typically report it on your statement closing date, which happens about three weeks earlier. If the bank reports that $1,500 balance to the bureaus before you pay it off, your utilization spikes, even if you never pay a penny in interest.

Mistake 3: Ignoring per-card utilization

Many people think the algorithm only cares about the overall math. Let’s say you have five credit cards with a combined limit of $25,000. You owe $4,000 on one card, and the other four are empty. Your overall utilization is a fantastic 16%.

However, if that $4,000 balance is sitting on a card with a $4,500 limit, that specific card is nearly maxed out. FICO looks at both your overall utilization and your per-card utilization. A single maxed-out card will drag your score down, even if your other cards are collecting dust.

How Much Does Credit Utilization Affect Credit Score? The Real Consequences

So, what actually happens when your utilization spikes?

First, the emotional toll is heavy. When you are working multiple jobs, trying to freelance, or aggressively paying down debt, watching your credit score slide backward is incredibly discouraging. It makes you feel like the system is rigged against normal people.

Practically speaking, the consequences depend entirely on what you are trying to do in your life right now.

If you are just going to work and living your normal routine, a drop in your credit score doesn’t really impact your day-to-day life. But if you are planning to apply for a mortgage, lease a new apartment, finance a car, or even apply for certain jobs, a high utilization rate can be a financial disaster.

A drop from a 740 credit score to a 680 credit score might mean the difference between getting a 6% interest rate on a car loan and a 9% interest rate. On a $25,000 car, that extra interest will cost you thousands of dollars over the life of the loan. High utilization makes borrowing money significantly more expensive. (If you’re already feeling the pinch, read: I Can Only Afford the Minimum Payments — Now What?).

| Utilization Rate | Typical Impact |

| 0% | Good, but may not be optimal |

| 1–9% | Often considered ideal |

| 10–29% | Generally healthy |

| 30–49% | Score may be affected |

| 50–74% | Significant impact possible |

| 75%+ | High-risk zone |

While there is no fixed number of points associated with credit utilization, its 30% weighting means maxing out a credit card can drop an excellent score into the “fair” category almost overnight. Conversely, paying off a high balance is one of the fastest ways to improve a credit score because balances are reported regularly.

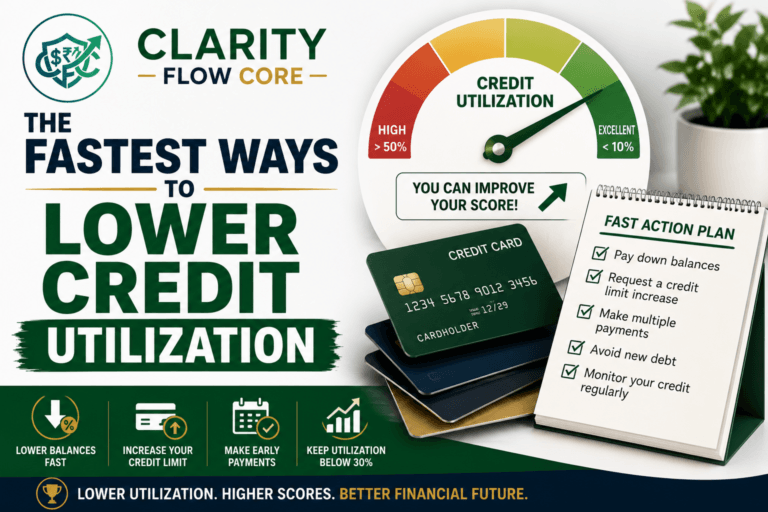

Practical Solutions: How to Take Control

The good news is that credit utilization is highly manageable once you understand how the game is played. You do not have to be rich to have an elite credit score; you just have to be strategic. Here are the most realistic ways to fix your utilization math. (For a deep dive, see: The Fastest Ways To Lower Credit Utilization).

1. The Statement Date Hack

If you pay off your card in full every month but your score keeps fluctuating, you need to change your payment timing.

Log into your credit card portal and find your “Statement Closing Date” (this is different from your payment due date). Set a calendar alert on your phone for three days before that closing date.

Go in and pay your balance down to nearly zero before the statement closes. When the bank reports to the credit bureaus a few days later, they will report a tiny balance, keeping your utilization near zero and your score as high as possible.

2. Request a Credit Limit Increase

If you are on a tight budget and your credit limit is only $1,000, buying a month’s worth of groceries will push your utilization dangerously high. It is exhausting trying to micromanage a tiny limit.

If your income has increased, or if you have a solid history of on-time payments, call your bank and ask for a credit limit increase. If they bump your limit from $1,000 to $3,000, your grocery runs suddenly take up a much smaller percentage of your available credit.

Warning: Only do this if you trust yourself. Increasing your limit to lower your utilization only works if you do not increase your spending to match the new limit.

If you’re new to credit and don’t yet qualify for higher credit limits, Best Secured Credit Cards for Beginners in 2026 compares secured cards that can help you establish positive payment history and eventually qualify for larger credit lines.

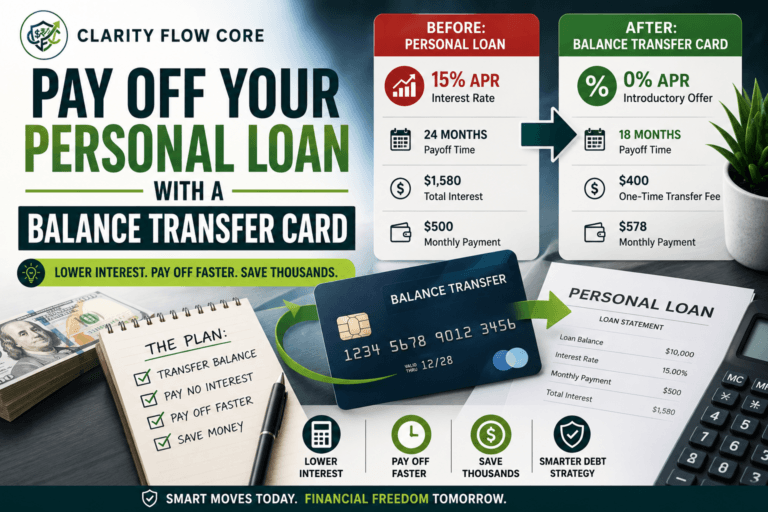

3. Shift the Debt (Balance Transfers)

If you are carrying a large balance and cannot pay it off before the statement date, the math is working against you. If you have decent credit, consider applying for a balance transfer card.

These cards usually offer a 0% introductory APR for 12 to 18 months. By moving your debt from a maxed-out card to a brand new card with a fresh limit, you instantly lower your per-card utilization, stop the bleeding on interest, and give yourself a timeline to pay off the principal balance.

A Beginner-Friendly Action Plan

Credit scores can feel intimidating, but fixing your utilization is one of the easiest financial wins you can get. If you want to optimize your score this week, follow this exact step-by-step plan:

- Step 1: Uncover the MathLog into every credit card account you own. Write down the current balance and the total credit limit for each card. Add all the balances together, and add all the limits together.

- Step 2: Find Your Optimal Target To get the maximum possible benefit to your credit score, you want your overall utilization to be under 10%. Multiply your total credit limit by 0.09. That number is your target balance. (Want the fast track? Stop doing manual math. Use our free Credit Utilization Calculator & Recovery System to plug in your numbers and see exactly how much you need to pay down to hit the perfect credit-boosting tier!).

- Step 3: Keep Old Cards AliveIf you have an old credit card you never use, do not close it. To keep the bank from closing it due to inactivity, put one small recurring subscription on it (like Netflix or Spotify) and set it to autopay in full every month. This keeps the account active, adds to your on-time payment history, and preserves that valuable credit limit.

- Step 4: Protect Your Cash BufferAggressively paying down credit cards to improve your score is great, but not if it leaves you with zero cash in your checking account. If an emergency happens, you will just have to run the cards back up again. Always keep a small starter emergency fund in a separate savings account before throwing every last dollar at your credit card balances.

Frequently Asked Questions

How quickly can lowering utilization improve my score? Credit card issuers usually report balances once per month. After a lower balance is reported, score improvements may appear within a few days to several weeks depending on the reporting cycle and scoring model. (Read more: How Long Does It Really Take To Rebuild Bad Credit?).

Does credit utilization have a memory?

No, and this is the best kept secret in the credit industry! Unlike a missed payment, which stays on your credit report for seven years, credit utilization has absolutely no memory. It is just a snapshot in time. If you max out a card this month, your score will tank. But if you pay it off entirely next month, your score will bounce right back up as if the high balance never happened.

Is a 0% utilization rate the best possible number?

Surprisingly, no. A completely 0% utilization rate can sometimes result in a slightly lower credit score than a 1% or 2% rate. The algorithm wants to see that you are actually using the credit extended to you and managing it well. Having a very small balance report on your statement date is often the optimal strategy for hitting an 800+ score.

Why did my score drop when I paid off a loan?

Credit utilization strictly applies to revolving credit, like credit cards and lines of credit. It does not apply to installment loans, like auto loans, student loans, or mortgages. When you pay off an installment loan, your score might temporarily drop because you closed an active account, changing your overall credit mix. It usually recovers in a few months.

Stop Stressing, Start Strategizing

If you have been agonizing over every slight dip in your credit score, it is time to give yourself a break.

The financial system is complex, and the rules are rarely explained to us in plain English. When your credit score drops because of a temporary balance, it is not a reflection of your character, your worth, or your ability to succeed. It is just a computer algorithm reacting to raw data.

Now that you understand that credit utilization controls 30% of your score, you hold the keys. You know that statement dates matter more than due dates. You know that keeping old accounts open protects your math. And most importantly, you know that a high balance today does not ruin your credit permanently, because utilization has no memory.

Don’t let the credit bureaus dictate your stress levels. Find your statement dates, optimize your payment timing, and watch your score start moving in the right direction. You are completely capable of mastering this.

Sources & References

- FICO® – What’s in Your FICO® Score? – Learn how payment history, credit utilization, and other factors influence your FICO® Score, and why credit utilization makes up approximately 30% of the scoring model.

- FICO® – Credit Utilization – Understand how revolving credit balances, credit limits, and utilization ratios can affect your credit score.

- Consumer Financial Protection Bureau (CFPB) – Credit Reports and Scores – Official guidance on how credit scores work, how credit card balances are reported, and how consumers can build healthy credit habits.

- Experian – Credit Utilization Ratio – Educational resources explaining how utilization is calculated, why statement balances matter, and practical ways to lower your ratio.

- Equifax – What Is Credit Utilization? – Learn how overall and per-card utilization can influence your credit profile and borrowing ability.

- AnnualCreditReport.com – Request your free credit reports from Equifax, Experian, and TransUnion to monitor account balances, payment history, and credit reporting accuracy.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.