Debt Consolidation vs Debt Settlement: Which Actually Saves More Money?

If you are reading this, there is a good chance you are familiar with the 2 AM ceiling stare, desperately trying to weigh the pros and cons of debt consolidation vs debt settlement. It is that quiet, heavy moment in the middle of the night when your brain decides to tally up your credit card balances, personal loans, and auto payments. You do the mental math, realize your paycheck barely covers the minimums, and feel a cold wave of panic wash over you.

When you are trapped in that cycle, you are incredibly vulnerable. You want a life raft. And suddenly, your social media feeds are flooded with advertisements promising a miracle: “Erase your credit card debt!” or “Cut your monthly payments in half without bankruptcy!”

These ads sound amazing. They promise to make the crushing weight go away. But the finance industry thrives on confusing terminology, and those ads usually disguise a dangerous financial tactic as a helpful lifeline. They throw around terms like “consolidation” and “settlement” as if they mean the same thing.

Let’s get one thing perfectly clear right from the start: when looking at debt consolidation vs debt settlement, they are exact opposites. One is a strategic financial move that protects your credit score. The other is the financial equivalent of dropping a nuclear bomb on your credit profile.

If you are trying to figure out how to dig yourself out of a financial hole, making the wrong choice between these two can cost you thousands of dollars in hidden fees, trigger surprise tax bills, and keep you from buying a house or a car for the next seven years. Let’s break down exactly how these two methods work, what the hidden catches are, and which one will actually save you money in the real world.

The Real Problem: Why the Debt Trap Feels Impossible to Escape

To understand why people get so desperate that they turn to debt settlement, we have to look at the math of minimum payments.

When you carry a balance on a credit card with a 24% interest rate, the credit card company is not your friend. They are a highly efficient profit machine. They set your minimum payment just high enough to cover the interest generated that month, plus a tiny fraction of the principal balance.

If you have $10,000 in credit card debt and only make the minimum payments, you aren’t just paying back $10,000. You might end up paying $18,000 over the course of ten years. That is why you feel like you are working incredibly hard, sending money to the bank every single month, but the balance never actually goes down.

When you reach the point where you can only afford the minimum payments on your credit cards, you realize you cannot out-earn the interest rate. You need a structural change. That is when people start Googling for solutions, and that is exactly where the confusion begins.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyIf your financial situation has become overwhelming because you’ve recently lost your income, I Lost My Job: A 30-Day Financial Survival Plan explains how to prioritize bills, preserve cash, and stabilize your finances before deciding on a long-term debt strategy.

Why the Confusion Happens: The Marketing Trap

The reason people confuse consolidation and settlement is simple: debt settlement companies intentionally market themselves as “debt consolidation” or “debt relief” programs.

They use soft, comforting language. They tell you that you will make “one easy monthly payment” to their company. They tell you that you will save 50% of what you owe. They make it sound like they have a secret VIP relationship with Visa and Mastercard that allows them to magically slash your balance.

They do not.

To make the right choice for your family, you need to strip away the marketing jargon and look at the raw mechanics of how these two distinct paths actually handle your money.

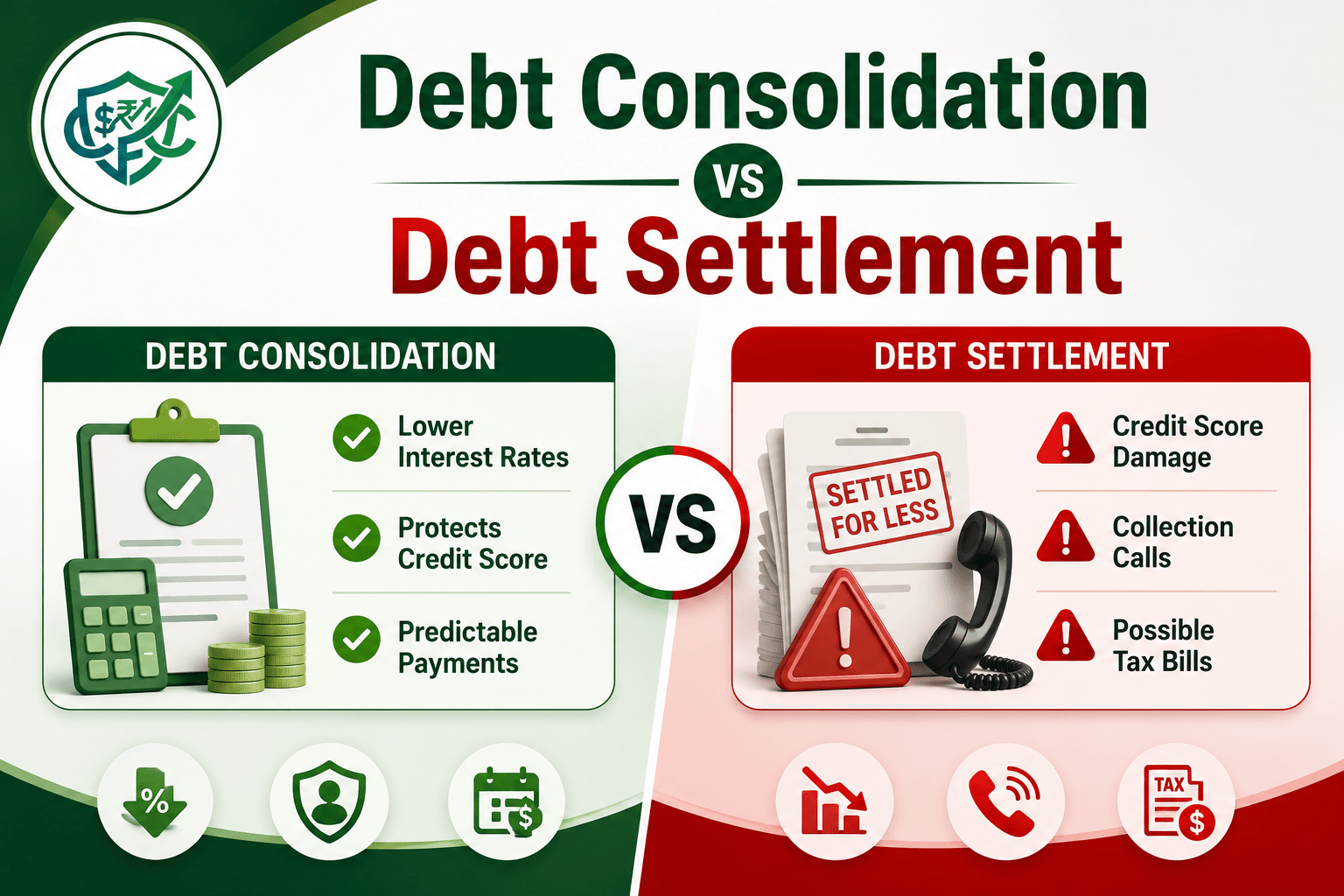

Deep Dive: Debt Consolidation (The Safe Route)

Debt consolidation is not a magic trick. It does not erase a single penny of the money you owe. If you owe $20,000 across five different credit cards, after you consolidate, you still owe exactly $20,000.

How it actually works: Consolidation simply means taking out one new, large loan at a lower interest rate, and using that cash to pay off all your smaller, high-interest debts. You are moving your debt from five expensive buckets into one cheaper bucket.

The Real-World Example: Let’s say you have three credit cards maxed out at a 25% interest rate. Your total balance is $15,000. You go to a local credit union or an online lender and apply for a $15,000 personal consolidation loan. Because you still have a decent credit score, the bank approves you at a 10% interest rate. The bank hands you $15,000. You immediately use it to pay the three credit cards down to zero. Now, your credit cards are clear, and you just owe the credit union $15,000 at a much lower, fixed monthly payment.

The Pros of Consolidation:

- It protects your credit score: In fact, it often improves it! Because you paid off your maxed-out credit cards, your credit utilization drops to 0%, which is a massive boost to your score.

- You save money on interest: You are no longer bleeding cash to 25% interest rates.

- It is predictable: You get a fixed payment every month and an exact “debt-free date” when the loan will be completely gone.

The Catch: To get a good consolidation loan, you have to have a good credit score before you apply. If you are already falling behind on payments, banks will view you as too risky and deny the loan.

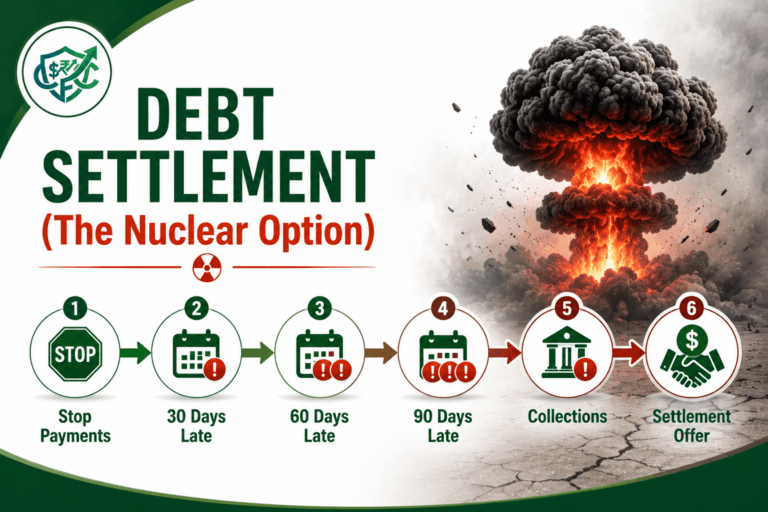

Deep Dive: Debt Settlement (The Nuclear Option)

Debt settlement is entirely different. This is when you (or a company you hire) negotiate with your credit card company to let you pay a smaller lump sum to resolve the debt. For example, offering the bank $4,000 to walk away from a $10,000 balance.

How it actually works (The Brutal Reality): Banks do not just say, “Oh, sure, you can pay us less.” If you are currently making your minimum payments, the bank has absolutely no incentive to negotiate with you. Why would they? They are making money.

To force the bank to the negotiating table, debt settlement companies will instruct you to stop paying your credit cards entirely.

Instead of paying the bank, you send a monthly payment to an escrow account managed by the settlement company. You sit back and wait while your credit card goes 30 days late, then 60 days late, then 90 days late. Your credit score free-falls into the 400s. Your phone rings off the hook with aggressive debt collectors. You receive threatening letters.

Once collection agencies become involved, every conversation matters. Before responding to collection calls or agreeing to a settlement, read How To Handle Debt Collectors Without Making Things Worse to understand your rights, verify the debt, and negotiate from a stronger position.

Finally, after six months of missed payments, the bank realizes, “Wow, this person is really not going to pay us.” They write your account off as a loss. At this exact moment, the settlement company steps in and says to the bank: “Our client has $4,000 in this escrow account. Will you take this lump sum right now and forgive the other $6,000?” Sometimes, the bank says yes. Sometimes, they sue you instead.

The Pros of Settlement:

- You pay less principal: You can technically get out of debt for less than you originally spent.

- It avoids bankruptcy: It is often viewed as the final stop before filing for Chapter 7 bankruptcy.

The Catch: It absolutely annihilates your financial reputation. Missing a credit card payment stays on your credit report for seven years. Having an account marked as “Settled for less than full balance” is a massive red flag to future lenders, landlords, and even employers.

4 Brutal Beginner Mistakes People Make with Debt Relief

When you are stressed about money, you want a quick fix. That urgency makes beginners incredibly susceptible to traps. Here are the four biggest mistakes we see people make when trying to choose between consolidation and settlement.

1. Believing Settlement is a “Secret Government Program”

Many predatory settlement companies use fake seals or misleading names like “Federal Debt Relief Initiative” to make you think there is a government bailout for your credit card debt. There isn’t. You are simply paying a for-profit company a massive fee (often 15% to 25% of your total debt) to do something you could technically negotiate yourself.

2. Consolidating Debt, Then Running Up the Cards Again

This is the single most common tragedy in personal finance. Someone gets a $15,000 personal loan, pays off their credit cards, and feels a massive wave of relief. They celebrate. But because they didn’t fix the underlying spending problem or build an emergency fund, a car breaks down three months later. They swipe the now-empty credit card. Fast forward two years, and they now have a $15,000 personal loan plus $15,000 in new credit card debt. They effectively doubled their debt.

3. Forgetting the “Tax Bomb” of Debt Settlement

This is the dirty secret of the debt settlement industry. If a bank forgives $6,000 of your debt in a settlement, the IRS does not consider that a lucky break. The IRS considers that $6,000 to be taxable income. At the end of the year, the bank will send you a 1099-C tax form, and you will have to pay federal income taxes on the money you didn’t pay back to the bank.

4. Letting the Settlement Company Handle Everything Blindly

If you hire a settlement company, they tell you to stop paying your bills. But while you are ignoring your mail, the credit card company might decide to sue you for the balance. The settlement company does not magically protect you from a lawsuit or wage garnishment. If you get sued, you are still the one who has to show up in court.

Debt Consolidation vs Debt Settlement: Which Actually Saves More Money?

So, if we put the two options in a boxing ring, which one actually leaves more money in your bank account?

The Short Answer: Debt Settlement might save you money on the actual balance of the debt, but Debt Consolidation saves you drastically more money across your entire financial life.

The Long Answer: Let’s pretend you settle a $20,000 debt for $10,000. You feel like you “saved” $10,000. But wait. You have to pay the settlement company their 20% fee ($4,000). Now you’ve only saved $6,000. Then the IRS hits you with a tax bill on the forgiven amount, costing you another $1,500. You actually only “saved” $4,500.

Now, look at the collateral damage. Because your credit is ruined, your car insurance premiums go up. You have to put down massive cash deposits to get a new cell phone plan or turn on the electricity in a new apartment. Two years later, when you try to buy a reliable used car, you are hit with a 22% auto loan interest rate because of the settlement on your record. You will end up paying $8,000 extra in interest on that car alone.

The $4,500 you saved upfront just cost you tens of thousands of dollars over the next seven years.

Consolidation, on the other hand, saves you money by stopping the bleeding. You pay back everything you borrowed, which is the honorable thing to do, but you do it at a fair interest rate. You keep your credit pristine, meaning when you go to buy a house or a car later, you get the absolute best rates, saving you a fortune in the long run.

The Beginner-Friendly Action Plan

If you are overwhelmed by your debt today, you need a safe, actionable roadmap. Do not call an 800-number from a late-night TV commercial. Follow these steps instead:

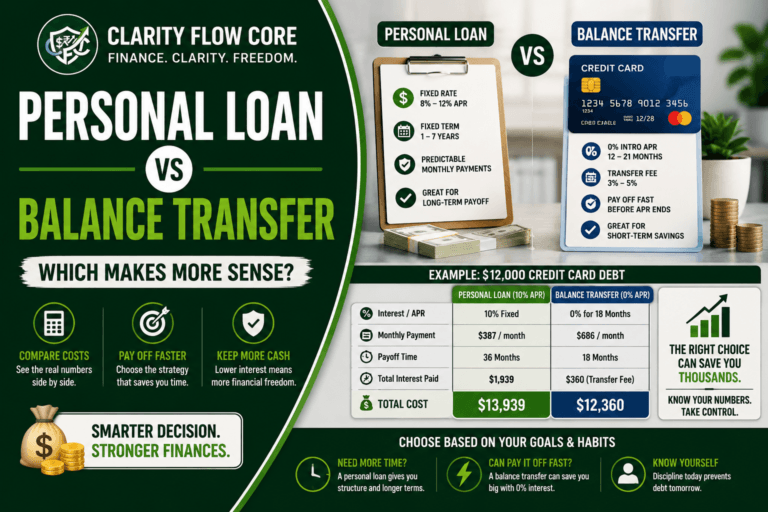

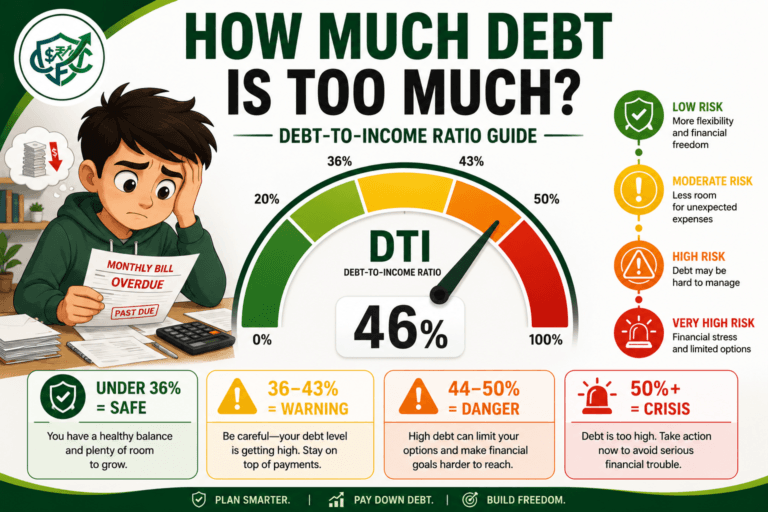

Step 1: Check your actual credit score and DTI. Before you can make a plan, you need to know if banks will even talk to you. Check your actual credit score and DTI. If your score is over 660 and your DTI is manageable, you are a prime candidate for a safe consolidation loan.

Step 2: Look for a Balance Transfer Card (The Free Consolidation). If your debt is relatively small (under $5,000) and your credit is great, look for a credit card offering a 0% introductory APR for 12 to 18 months. You transfer the balances to this new card, pay a small 3% transfer fee, and then aggressively pay off the debt while zero interest is accumulating.

Step 3: Shop for a Personal Consolidation Loan. If a balance transfer isn’t enough, shop around at local credit unions for a personal loan. Credit unions almost always offer better rates and more human underwriting than massive national banks.

Step 4: Cut up the cards. If you use a loan to clear your credit cards, you must physically remove the temptation to use them again. Cut them up. Delete them from Apple Pay. Remove them from your Amazon account. Treat the consolidation loan as your one and only priority.

Step 5: If you are already drowning, skip settlement and use Credit Counseling. If your credit is already wrecked and you cannot get a consolidation loan, do NOT hire a for-profit debt settlement company. Instead, look for a Non-Profit Credit Counseling Agency (search for an agency affiliated with the NFCC). They offer “debt management plans” (DMPs). They will negotiate with your creditors to lower your interest rates to almost zero, and you pay the non-profit one monthly payment. It is vastly safer, dramatically cheaper, and less damaging to your credit than debt settlement.

Once your finances are back under control, rebuilding your credit should become your next priority. Best Secured Credit Cards for Beginners in 2026 compares secured cards that can help you establish fresh positive payment history and strengthen your credit profile over time.

Frequently Asked Questions (FAQs)

Does debt consolidation hurt my credit score? Initially, you might see a small dip of 5 to 10 points because the lender performs a “hard inquiry” to check your credit, and you are opening a brand-new loan account. However, within a month or two, your score will usually jump up significantly because your credit card utilization drops to zero.

Can I settle my debts myself without hiring a company? Yes, absolutely. If your accounts are already heavily past due or in collections, you can call the collection agency yourself and offer a lump sum to settle the debt. Doing it yourself saves you the massive 20% fee that settlement companies charge, but it requires thick skin and strong negotiation skills.

Will a debt consolidation loan cover my auto loan? Usually, no. Personal consolidation loans are unsecured, meaning they are designed to pay off other unsecured debts like credit cards, medical bills, or personal loans. Auto loans are secured by the car itself, so it rarely makes mathematical sense to roll an auto loan into an unsecured personal loan.

What happens if I stop paying my settlement company? If you sign a contract with a debt settlement company, stop paying your creditors, and then stop paying the escrow account for the settlement company, you are in the worst possible position. Your credit will be ruined, the settlement company will drop you as a client, and the credit card companies will likely move forward with lawsuits against you.

Final Thoughts: You Are More Than Your Debt

Being heavily in debt carries an enormous amount of shame in our society. It makes you feel like you failed some invisible test of adulthood. But the truth is, the system is designed to trap you. Credit card companies spend billions of dollars employing psychologists and data scientists to figure out exactly how to keep you swiping.

If you are staring at a massive balance today, take a deep breath. Forgive yourself for whatever sequence of events or mistakes led you here. You cannot change the past, but you have absolute control over what you do tomorrow morning.

Do not let desperation push you into a reckless debt settlement program that will haunt you for a decade. Look at your numbers logically. Explore a consolidation loan to stop the bleeding of interest. If you cannot get a loan, seek out a non-profit credit counselor to help you negotiate safely.

It will take time. It will require discipline and saying “no” to things you want. But there is a day in the future where you will log into your banking app, look at your dashboard, and see a balance of $0.00. That day is entirely possible, and it starts with making the right choice today. You’ve got this.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

Sources & References

Articles published on Clarity Flow Core are researched and reviewed using publicly available information from official government agencies, financial institutions, consumer protection organizations, credit bureaus, and trusted educational resources.

Reference sources may include:

- Internal Revenue Service (IRS)

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve

- U.S. Department of the Treasury

- Federal Trade Commission (FTC)

- Bureau of Labor Statistics (BLS)

- Federal Deposit Insurance Corporation (FDIC)

- Securities and Exchange Commission (SEC Investor.gov)

- Experian

- Equifax

- TransUnion

- myFICO

- AnnualCreditReport.com

- Official banking, lending, insurance, and financial institution websites

- Public consumer finance studies and educational resources

Additional editorial references may include reputable financial publications, academic research, behavioral finance studies, housing and credit market data, and publicly available consumer finance resources where relevant.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.