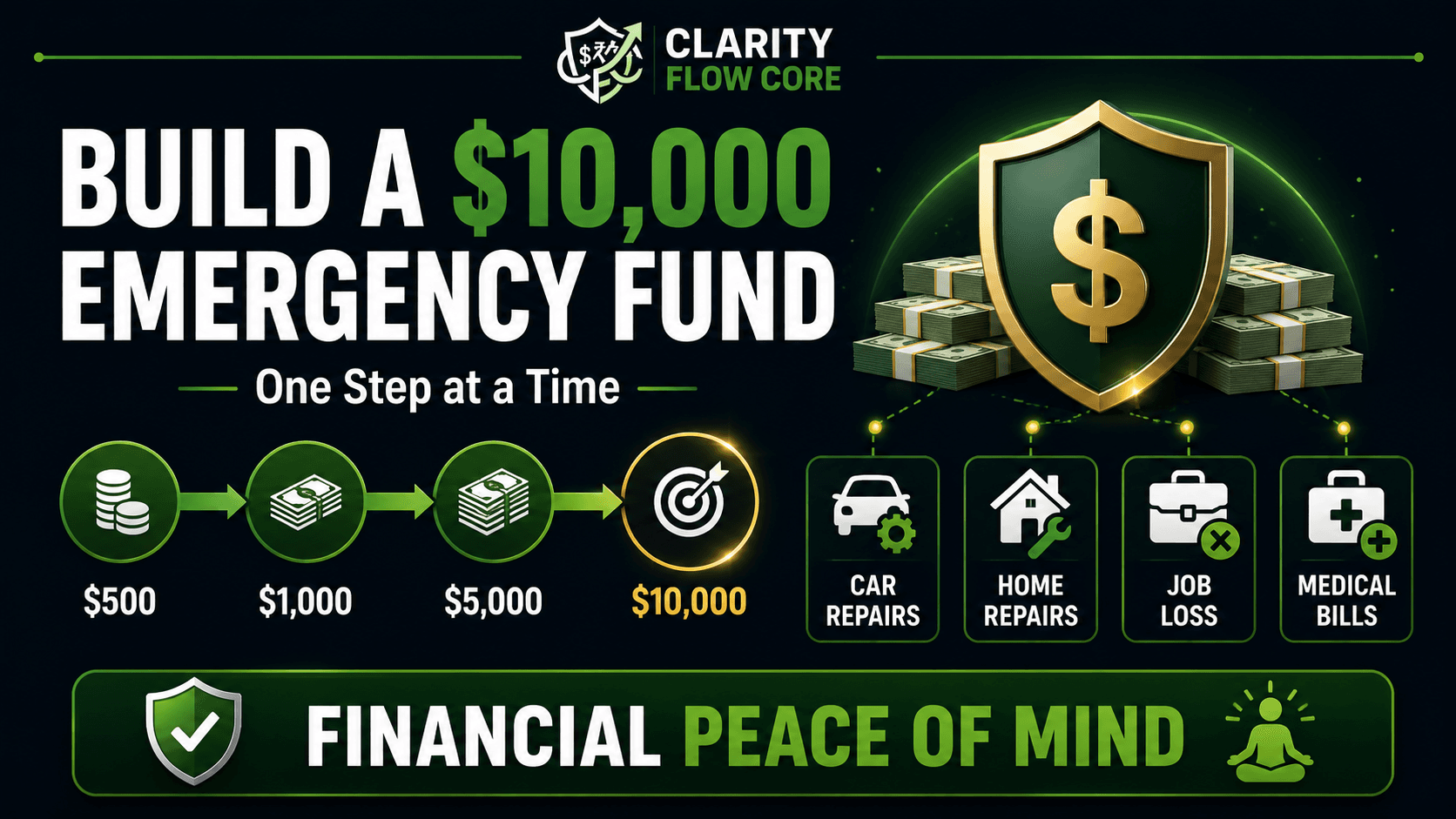

How to Build a $10,000 Emergency Fund: Step-by-Step

You are driving down the highway when you hear a terrifying metallic clunk from your engine. You pull over, call a tow truck, and spend the next two hours dreading the conversation with the mechanic. When they finally call, the news is exactly what you feared: you need a new transmission, and it is going to cost $3,500.

If you are like most Americans, a $3,500 unexpected bill is an absolute crisis. It means draining your checking account, maxing out a credit card, or taking out a high-interest personal loan. It means months—or years—of financial stress paying off that single stroke of bad luck.

But what if, instead of panic, your only reaction was minor annoyance? What if you simply transferred $3,500 from your savings, paid the mechanic in cash, and went on with your life?

That is the peace of mind a fully funded emergency reserve provides. Getting to that level of financial security does not require a six-figure salary or a lucky lottery ticket. It requires a specific, automated system.

In this guide, we will break down exactly how to build a $10000 emergency fund from scratch, where to keep the money so it grows safely, and the exact mathematical steps you need to reach this milestone faster than you think.

⚡ Quick Answer

To build a $10000 emergency fund, you must separate your savings from your checking account by opening a fee-free High-Yield Savings Account (HYSA). Start by auditing your budget to free up cash, automate a weekly or monthly transfer, and direct all financial windfalls (like tax refunds and bonuses) straight into the fund. Focus on consistent, automated deposits rather than waiting until you feel “ready” to save.

The $10k Timeline Matrix

If the idea of saving $10000 feels completely impossible right now, the math might surprise you. Here is exactly how long it takes to reach your goal based on your monthly contribution:

| Monthly Contribution | Time to Reach $10 000 | Strategy Required |

| $150 / month | ~5.5 Years | Basic expense cutting |

| $250 / month | ~3.3 Years | Trimming subscriptions & dining out |

| $500 / month | 20 Months | Side hustle + optimized budget |

| $800 / month | ~1 Year | Major structural budget changes |

Why $10,000 is the Magic Number

Personal finance experts argue constantly about exactly how much cash you need in reserve. Some say $1,000 is enough to start; others insist you need an entire year of living expenses.

If you are unsure exactly what your personalized target should be based on your unique living expenses, you can run a full diagnostic using our Advanced Emergency Fund Analyzer. However, for the vast majority of households, $10,000 is the ultimate financial sweet spot. Here is why:

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings Target1. It Covers 90% of “Life Happens” Events

A $1,000 starter fund is great for a blown tire or a minor medical bill. But a true emergency—a flooded basement, a major car transmission failure, or a sudden emergency room deductible—will easily blow past $1,000. Having $10,000 liquid means you can handle almost any standard household or automotive disaster in cash without blinking.

2. It Provides Job Loss Insulation

The most critical function of an emergency fund is protecting you if you lose your primary source of income. If your basic bare-bones living expenses (rent, groceries, utilities, insurance) are $3,000 a month, a $10,000 fund gives you a solid three-month runway to find a new job. That means you can interview for roles you actually want, rather than taking the first terrible job you find out of pure desperation.

If you’re planning to move into your own apartment or house, this emergency fund becomes even more valuable. Before signing a lease, read How Much Should You Save Before Moving Out on Your Own? to estimate your upfront moving costs and the emergency savings you’ll want before living independently.

3. The Psychological Shift

There is a massive psychological difference between having $800 in the bank and having five figures sitting safely in reserve. At $10,000, you stop operating out of fear. You stop worrying about which bills will clear on Friday. You sleep better. You have essentially purchased your own financial stress insurance.

The 80/20 Rule of Building Your Fund

Before we map out the step-by-step process, we need to address how you are going to find the money.

Many beginners try to save $10,000 by cutting out $3 lattes and buying single-ply toilet paper. This is a fast track to burnout. According to the 80/20 rule of personal finance, 80% of your results come from 20% of your efforts.

To find large amounts of cash quickly, you must look at the big rocks in your budget:

- Housing: Can you get a roommate? Can you appeal your property taxes? Can you move to a cheaper apartment across town?

- Transportation: Are you paying $600 a month for a car loan? Selling an expensive car and buying a reliable used vehicle in cash can instantly free up hundreds of dollars a month.

- Food Strategy: Stop worrying about occasional coffee and focus on massive grocery optimization. Meal planning and switching to store-brand staples can easily save a family $300 a month. (Read our guide on 50 Things to Stop Buying If You’re Trying to Save Money for more massive wins).

Fix the big structural expenses first. The savings will compound rapidly.

How to Build a $10000 Emergency Fund in 5 Steps

Ready to build the safety net? Follow this exact, proven sequence to fund your account and protect your family.

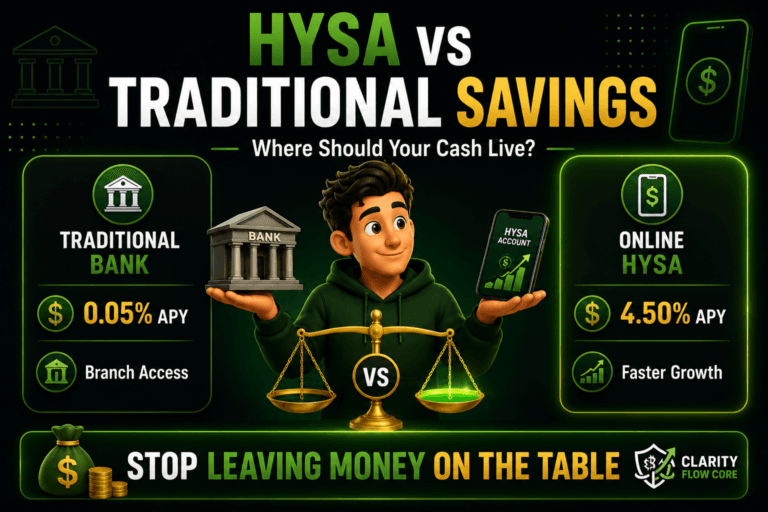

Step 1: Open the Right Account (The HYSA)

The single biggest mistake people make is keeping their emergency savings inside their daily checking account. If your savings are mixed with your grocery money, human psychology guarantees you will eventually spend it. You look at your balance, feel artificially rich, and decide to book a vacation.

You must separate the money. Open a High-Yield Savings Account (HYSA).

If you’re opening your first online savings account, How to Choose Your First High-Yield Savings Account explains how to compare APYs, fees, FDIC insurance, and account features before selecting a bank.

HYSAs are completely free, FDIC-insured online accounts that offer significantly higher interest rates than traditional brick-and-mortar banks. If you keep $10,000 in a traditional bank earning 0.01%, you earn $1 a year. If you keep it in an HYSA earning 4.5%, you earn $450 a year in free money just for letting it sit there.

Step 2: Establish Your Monthly Target

Look at your budget and decide on a painful but achievable monthly transfer amount. If your budget is tight, start with $150. If you have decent income but terrible spending habits, challenge yourself to $500 a month.

You need to know exactly how much free cash flow you have available. If you are drowning in minimum debt payments and cannot find a single spare dollar, you need to map out a debt reduction strategy first. Run your numbers through our Debt-to-Income Analyzer & Loan Readiness Planner to see exactly where your money is trapped.

Calculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI RatioStep 3: Automate the Transfer

Willpower is a finite resource. If you wait until the end of the month to see “what is left over” to transfer to savings, the answer will always be zero.

Log into your checking account today and set up a recurring, automatic transfer to your new HYSA. Schedule the transfer to execute the exact day after your paycheck clears. Treat your emergency fund deposit exactly like your rent payment—it is non-negotiable and it leaves the account automatically.

Step 4: The Kickstarter Phase (Sell the Clutter)

Saving $200 a month is great, but starting from $0 feels incredibly slow. You need a quick win to build momentum.

Dedicate one weekend to a massive house sweep. Go through your garage, your closets, and your basement. Find the golf clubs you have not used in three years, the designer clothes that no longer fit, and the old electronics collecting dust. Sell them on Facebook Marketplace, eBay, or Craigslist.

Most households have between $500 and $1,500 worth of unused items sitting in their house. Liquidate it, and immediately drop that cash into your new HYSA. You just skipped three months of standard saving.

Step 5: Direct All Windfalls Here

Throughout the year, you will likely receive unexpected “windfalls” of cash. This includes:

- Annual tax refunds

- Work bonuses

- Birthday or holiday cash

- Cash back from credit card rewards

- Three-paycheck months (if you are paid bi-weekly)

The average US tax refund is roughly $3,000. If you take that single check and drop it straight into your emergency fund instead of using it as a down payment on a new car, you instantly cover 30% of your total $10,000 goal.

Fund Your $10k Goal Faster

Waiting for a $3,000 tax refund to boost your emergency fund? That means you’re giving the IRS an interest-free loan. Use our optimizer to adjust your W-4, increase your take-home pay, and route that extra cash directly into your HYSA every month.

Optimize My W-4Where NOT to Keep Your Emergency Fund

Knowing where to put your money is just as important as saving it. When figuring out how to build a $10,000 emergency fund, beginners often try to get too clever and put the money in dangerous places.

- The Stock Market: Never invest your emergency fund. The stock market is for long-term wealth building (5+ years). If a recession hits, you could lose your job and watch your $10,000 fund instantly drop to $6,000 on the exact day you need the money most.

- Certificates of Deposit (CDs): While CDs offer great interest rates, your money is locked up for a specific term (like 12 or 24 months). If your car breaks down and you pull the money out of a CD early, you will be hit with steep financial penalties. Emergency funds must be 100% liquid.

- Physical Cash Under the Mattress: Keeping $10,000 in your house is a massive risk. It can be stolen, destroyed in a fire, and it constantly loses purchasing power to inflation because it earns zero interest.

Keep it in a High-Yield Savings Account. It is boring, and boring is exactly what you want for an emergency fund.

🚨 The Biggest Emergency Fund Mistake

The most common reason people fail to build a $10,000 reserve is confusing inconveniences with emergencies. > Buying last-minute Christmas gifts, upgrading your phone because the screen cracked, or paying for an annual vacation are not emergencies. They are predictable expenses you failed to budget for. If you drain your emergency fund for a vacation, you will have nothing left when your HVAC unit explodes.

When Building an Emergency Fund Backfires

Is it ever a bad idea to save $10,000? Surprisingly, yes. There are specific scenarios where hoarding cash will actually destroy your financial momentum.

1. Saving While Carrying High-Interest Credit Card Debt

If you have $8,000 in credit card debt at a 25% interest rate, and you are slowly trying to save $10,000 in a bank account earning 4%, you are losing math. The credit card interest is draining your wealth faster than the savings account can build it.

In this scenario, you should save a starter emergency fund (usually $1,000 to $2,000 to prevent overdrafts and minor emergencies), and then throw every single extra dollar at the credit card debt until it is gone. Use our Credit Utilization Calculator & Recovery System to map out your exact payoff date. Once the debt is cleared, resume building the $10,000 fund.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My Utilization2. Pausing Employer 401(k) Matches

Do not stop contributing to your 401(k) if your employer offers a match. An employer match is a 100% immediate return on your investment. If you pause your retirement contributions to aggressively fund your savings account, you are leaving thousands of dollars of free money on the table. Contribute just enough to get the full match, and direct the rest of your cash flow to the emergency fund.

Real-Life Scenario: The Power of the Buffer

Let’s look at a practical example of how this plays out in the real world.

Sarah is 28 years old, makes $60,000 a year, and has zero savings. She gets a flat tire on her way to work. She pays $150 to get it fixed, putting it on a credit card because she has no cash. The stress ruins her week.

She decides to get serious. She audits her budget, cancels $80 in unused subscriptions, stops eating out twice a week (saving $200), and sells an old camera for $400. She opens an HYSA and sets up an automatic transfer of $300 a month.

Six months later, her car’s alternator dies. The bill is $600.

But this time, Sarah has $2,200 in her HYSA (her initial $400 kickstarter + $1,800 from six months of automated savings). She pays the mechanic in cash. She does not pay a dime in credit card interest. She is annoyed, but she is completely financially secure. That is the power of the system in action.

Action Plan: Start Your Fund Today

Reading about savings strategies will not protect you from a job loss; taking action will. Do these three things before you go to sleep tonight:

- Open an HYSA: Research online banks (like Ally, Marcus, or Discover) and open a free High-Yield Savings Account. It takes less than 10 minutes.

- Run the Math: Open your checking account app. Find $100 you wasted last month on things you do not even remember buying.

- Set the Automation: Set up a recurring, automatic transfer of $100 from your checking to your new HYSA. Schedule it to happen the day after your next paycheck.

You have officially started the journey.

Next Steps

Once your emergency fund hits that $10,000 milestone, your financial life completely transforms. You are no longer living paycheck to paycheck. Your next priorities should be optimizing how your money works for you.

If you are wondering how this $10,000 fits into your broader life goals, check out our guide on How Much Should You Have Saved by Age 30, 40, and 50? to see if you are on track.

What Comes After the Emergency Fund?

Securing your $10,000 cash safety net is the absolute foundation of your finances. Once your fortress is built, use our interactive analyzer to project your future wealth, calculate your exact targets, and chart your path to retirement freedom.

Plan My RetirementRelated Guides to Read Next:

- Emergency Fund Basics: Where to Start

- How to Automate Savings Using Split Direct Deposit

- Debt Avalanche vs Debt Snowball

- HYSA vs Money Market Account

Frequently Asked Questions

Is $10,000 enough for a family of four?

It depends entirely on your monthly expenses. For a single W-2 employee, $10,000 might cover four months of living expenses. For a family of four with a large mortgage in a high-cost-of-living area, $10,000 might only last six weeks. Start with $10,000 as your first massive milestone, but calculate your true target based on 3 to 6 months of actual bare-bones expenses.

Should I keep my emergency fund at the same bank as my checking account?

It is highly recommended to keep your emergency fund at a completely separate institution. If you keep it at your primary bank, it is too easy to transfer money into your checking account instantly to cover a non-emergency impulse purchase. Opening an account at a different bank creates a 2-to-3 day transfer delay, which acts as a psychological cooling-off period to prevent impulse spending.

What if I have to drain the fund for an emergency?

That is exactly what the money is there for! Do not feel guilty about using it. Pay the emergency bill in cash, celebrate the fact that you avoided credit card debt, and immediately restart your automatic monthly transfers to rebuild the balance.

Does a Roth IRA count as an emergency fund?

While you can withdraw your contributions (but not the earnings) from a Roth IRA without penalty, you should absolutely not treat it as your primary emergency fund. A Roth IRA is a wealth-building vehicle. If you withdraw money for a car repair, you lose years of tax-free compound growth.

How do taxes work on a High-Yield Savings Account?

The interest you earn in your HYSA is considered taxable income by the IRS. Your bank will send you a 1099-INT form at the end of the year if you earned more than $10 in interest. You simply report this amount when you file your annual tax return.

Can I use my emergency fund to pay off my mortgage faster?

No. Your emergency fund must remain highly liquid (easily converted to cash). If you tie that $10,000 up in your home equity, you cannot use it to buy groceries if you lose your job. Keep the cash liquid and accessible.

References and Resources

To ensure you are making the best decisions regarding where to hold your money safely, we recommend utilizing these official government resources:

- Consumer Financial Protection Bureau (CFPB): The CFPB provides unbiased, straightforward worksheets on how to set savings goals and build your safety net. Visit the CFPB Savings Guide.

- Federal Deposit Insurance Corporation (FDIC): When choosing an online High-Yield Savings Account, always ensure the bank is FDIC-insured. This guarantees your cash up to $250,000 per depositor. You can verify a bank’s status directly via their official tool. Visit the FDIC BankFind Suite.

- Internal Revenue Service (IRS): To understand exactly how the interest on your new savings account will be taxed at the end of the year, review the official IRS guidelines. Read IRS rules on Interest Income.

- Federal Reserve: If you want to understand why High-Yield Savings Account interest rates move up and down based on broader economic policies, the Federal Reserve provides excellent educational breakdowns. Explore Federal Reserve Education.

Conclusion

Learning how to build a $10,000 emergency fund is not about depriving yourself of joy; it is about buying yourself the ultimate luxury: peace of mind.

Unexpected disasters are going to happen. Your car will break down, a pipe will burst, or the economy will shift. You cannot control these events, but you have absolute control over how you respond to them. By opening a dedicated High-Yield Savings Account, cutting the structural fat from your budget, and setting up automated transfers, you are building an impenetrable financial fortress.

Stop waiting for a massive raise or the “perfect time” to start saving. The perfect time is today. Audit your budget, set up your first $100 automatic transfer, and take the first step toward true financial freedom.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.