How to Read and Fix Your Credit Report (Step-by-Step)

If you are attempting to purchase a house, finance a reliable used car, or even rent a new apartment in a competitive market, learning exactly how to read and fix your credit report is the single most crucial financial skill you can master this year.

Most individuals view their credit score as a magical, immovable three-digit number issued by a secret banking council. They only look at it when they are desperately seeking a loan. If the figure is low, they simply accept defeat, assume they are bad with money, and agree to pay exorbitant, predatory interest rates.

To put the cost of bad credit into operational perspective, look at the math on a standard home purchase.

If you have a pristine credit score of 760 and buy a $350,000 house, you will secure the lowest possible mortgage rate. If your score sits at 620, the bank will charge you a substantially higher interest rate due to perceived risk. Over the life of a typical 30-year mortgage, that 140-point difference in your credit score could potentially cost tens of thousands of dollars in additional interest. That is massive wealth taken directly out of your future retirement to pay for a 3-digit number.

The reality the banking sector doesn’t want you to realize is this: your credit score is simply a math grade. It is an algorithmic output based only on the raw data included within your credit report. If that underlying data is faulty—and for millions of consumers, it absolutely is—your score will mathematically plummet. You are literally paying thousands of dollars in a “bad credit tax” because of minor clerical mistakes by banks and credit bureaus.

If you are ready to take ultimate control of your financial reputation, stop paying excessive interest, and secure your financial foundation, here is the comprehensive, step-by-step guide on how to read and fix your credit report.

⚡ Quick Answer

To read and fix your credit report:

- Obtain your reports from all three major credit bureaus.

- Review personal information, accounts, inquiries, and public records.

- Identify errors or outdated information.

- Submit disputes directly to the bureaus with supporting documentation.

- Build positive credit habits to improve your score over time.

Because credit scores are based exclusively on report data, correcting inaccuracies can help improve borrowing opportunities and reduce your lifetime interest costs.

Step 1: Your Score vs. Your Report

Before you can begin auditing the data, you must grasp the fundamental difference between a credit score and a credit report.

- Your Credit Report is the permanent historical record of your financial life. It is an incredibly detailed log of every loan you have ever taken out, every credit card you have ever opened, your month-to-month payment history, and any public financial judgments against you over the past seven to ten years.

- Your Credit Score (such as a FICO Score or VantageScore) is just the GPA of that transcript. An algorithm takes the raw data inside your report, crunches the figures, and spits out a three-digit number between 300 and 850. (To fully understand how lenders view these numbers, read FICO vs. VantageScore: Why Credit Scores Differ Between Apps).

You cannot directly “fix” a credit score. All you can do is correct the underlying data on the report. Clean up the report, and the algorithmic score will increase automatically.

Step 2: Get Your Official Credit Reports (For Free)

The first step in understanding how to read and fix your credit report is to pull the exact documents the lenders are looking at.

In the United States, there are three major credit bureaus: Experian, Equifax, and TransUnion. Lenders are not legally required to report your activity to all three. Therefore, a massive error might appear on your Equifax report but not on your Experian report. You need all three documents to conduct a comprehensive audit.

(Warning: Do not purchase a credit report. There are hundreds of scam websites that claim to offer “free” credit scores, but they require a credit card and will covertly sign you up for a $29/month credit monitoring subscription).

Under federal law, you are entitled to free, complete copies of your credit report from all three bureaus.

- Go directly to AnnualCreditReport.com. This is the only website authorized by federal law to provide your official free reports.

- Fill in your identifying details. You will be asked high-level security questions like, “Which of these streets did you live on in 2018?” or “Who is your current auto loan provider?”

- Download all three reports as PDF files to your computer, or print them out so you can grab a red pen and physically circle the errors.

(Note: If you fail the online security questions, the system will lock you out to deter identity theft. Do not panic. You simply follow their instructions to mail in a physical copy of your driver’s license and a utility bill to verify your identity).

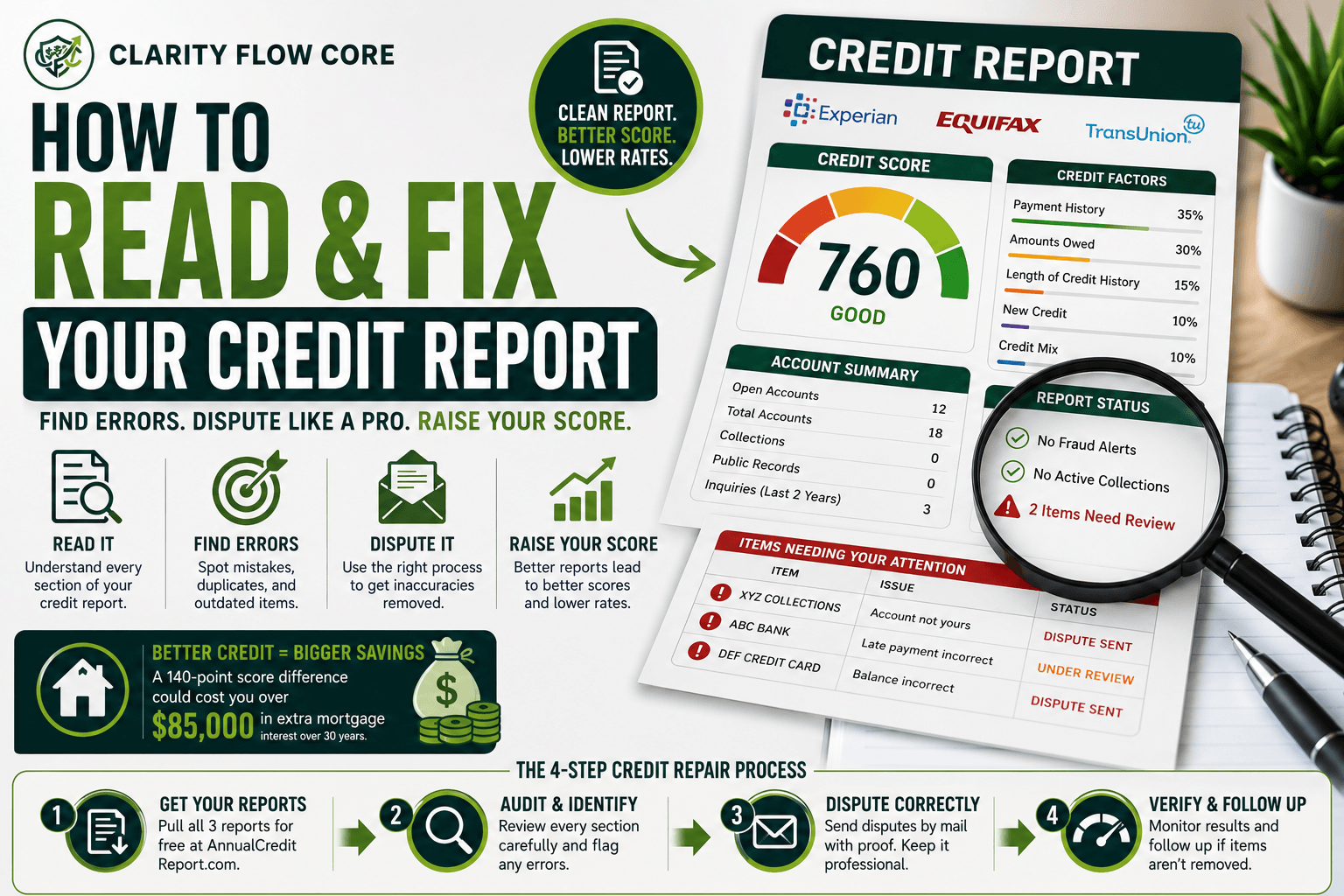

Step 3: Decode the 4 Main Parts of Your Report

When you open your report for the first time, it will look like a massive, terrifying wall of text, dates, and account numbers. A core part of learning how to read and fix your credit report is learning how to parse this data. A credit report is divided into four standard sections.

1. Personally Identifiable Information (PII)

This area includes your legal name, aliases, current and former addresses, your Social Security Number, and your employment history.

- What to Audit: Look for addresses you have never lived at, misspelled names, or employers you have never worked for. While an incorrect address will not immediately lower your credit score, it is the number one red indicator that someone has stolen your identity and is applying for loans in a different state.

2. Credit Accounts (Tradelines)

This is the absolute core of your report. It logs every credit card, auto loan, student loan, and mortgage you have taken out in the last seven to ten years. It displays your original loan amount, your credit limit, your current balance, and a grid showing your payment history.

- What to Audit: You must analyze this section ruthlessly.

- Look for 30-, 60-, or 90-day late payments that you know for a fact you paid on time.

- Look for “Open” accounts that you successfully closed years ago.

- Look closely at the “Date of First Delinquency.” By law, negative marks must fall off your report after exactly 7 years. An old, unpaid medical bill from 9 years ago should not be illegally dragging your score down today.

3. Public Records

Serious financial events filed in the federal court system are listed here. Today, this section is almost exclusively reserved for bankruptcies. (Tax liens and civil judgments were largely removed from credit reports a few years ago due to changing regulations).

- What to Audit: If you have a history of bankruptcy, verify that the filing date, the chapter type (Chapter 7 vs. Chapter 13), and the discharge status are 100% accurate. A Chapter 7 bankruptcy legally stays on your report for 10 years, while a Chapter 13 stays for 7 years.

4. Hard Inquiries

There are two types of inquiries. A “Soft Inquiry” happens when you check your own score on an app or an employer runs a background check; these do not damage your score. A “Hard Inquiry” happens when you deliberately apply for new credit, and the lender pulls your official file to make a decision. Hard inquiries drop your score by a few points and stay on your report for exactly two years.

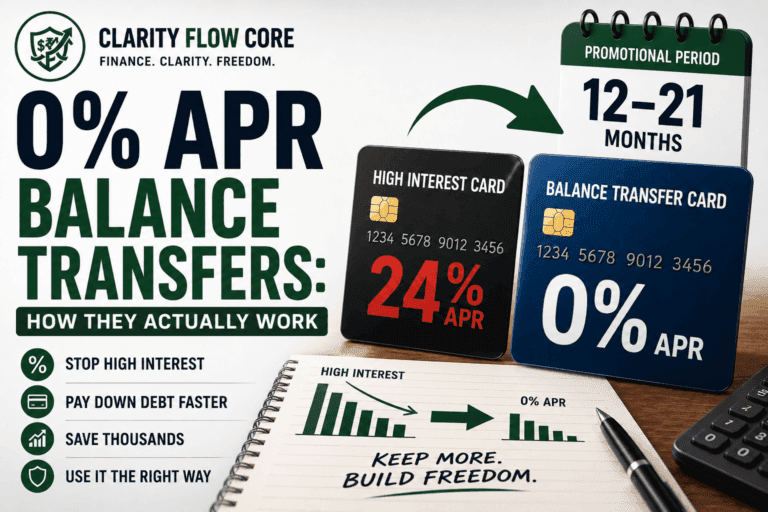

- What to Audit: If you see a hard inquiry from a bank or auto dealership that you never applied to, it means a fraudster is actively trying to open debt in your name. (If you are the one intentionally opening new lines of credit to lower your interest rates, ensure you fully grasp the process by reading 0% APR Balance Transfers: How They Actually Work).

Step 4: The Official Dispute Process

If you find a clerical error—a phony account, an incorrect balance, or a stale late payment that should have aged off—you have the legal right to challenge it under the Fair Credit Reporting Act (FCRA). This is the operational engine of how to read and fix your credit report.

Once you submit a formal dispute, the legal burden of proof shifts to the credit bureau and the lender. They generally have about 30 days to verify the negative mark with hard documentation. If they cannot prove it, they are legally compelled to delete it from your file.

The Bulletproof Dispute Strategy:

- Do Not Dispute Online: This is the single biggest mistake consumers make. Credit bureaus make it incredibly easy to hit a “Dispute” button on their website. However, some consumer advocates strongly prefer mailed disputes because they create a stronger paper trail and allow for much more detailed documentation. You avoid being forced into generic dropdown menus that don’t explain the nuance of your specific situation.

- Write a Custom Dispute Letter: Draft a formal, physical letter. Identify the precise item that is incorrect, the account number, and the specific reason it violates the FCRA. (e.g., “Account #1234 is reported as 30 days late in May 2024. I have attached a bank statement confirming the payment was successfully posted on time.”)

- Use Certified Mail: Print your letter, attach copies of your ID and proof of address, and mail it using USPS Certified Mail with a Return Receipt requested. This creates a legally binding paper trail. It proves exactly when the agency received your complaint, which starts their legal ticking clock.

- Escalate to the CFPB: If time passes and the bureau refuses to delete an obvious, proven mistake, escalate immediately. File a complaint online with the Consumer Financial Protection Bureau (CFPB). The federal government will intervene, contact the bureau’s legal department on your behalf, and force them to remedy the problem.

Step 5: Advanced Tactics for Accurate Negative Marks

What happens if you are researching how to read and fix your credit report, but you realize the negative mark is actually accurate? If you legitimately missed a payment or had an account go to collections, you cannot legally contest it as an “error.” However, you still have powerful negotiation tactics.

- The “Goodwill” Letter: If you have been a loyal customer of a bank for five years, and you missed just one single payment because you were in the hospital or lost your job, write the bank a Goodwill Letter. Do not send this to the credit bureaus; send it directly to the lender. Explain the hardship, highlight your long history of on-time payments, and ask them to remove the late mark as an act of goodwill. Many banks will update your file to “Paid as Agreed” to retain your business.

- Pay-For-Delete Agreements: If you have a debt sitting in collections, the collections agency wants your cash far more than they want to damage your credit score. Before you pay them, offer a “Pay-For-Delete” agreement. You agree to pay the debt (or settle for a percentage of the total), but only if they agree in writing to contact the credit bureaus and delete the collection account entirely. (Note: Not all collection agencies will agree to pay-for-delete requests, but it is always worth negotiating. Never hand cash to a collection agency without getting the agreement in writing first).

When This Backfires: The Zombie Debt Trap

If you do not fully understand the legal rules of how to read and fix your credit report, your actions can backfire and ruin your finances. The biggest trap involves “Zombie Debt.”

Every state has a “Statute of Limitations” on debt (usually between 3 to 6 years). After this time passes, a debt collector can no longer legally sue you or garnish your wages to collect the old debt.

However, if you contact a debt collector and acknowledge the old debt, or if you make even a $5 “good faith” payment, you instantly reset the Statute of Limitations clock. A debt that you were legally protected from is suddenly reactivated, and the collector can now sue you for the full amount. If a debt is extremely old, consult with a consumer protection attorney before you attempt to pay it off or dispute it.

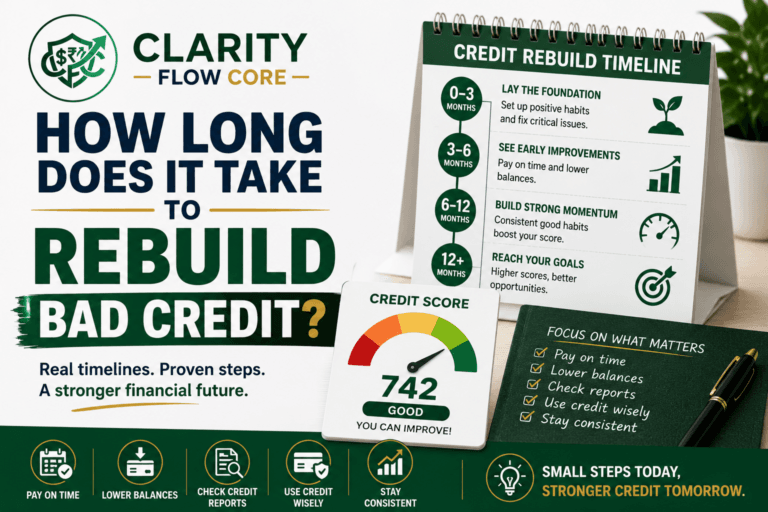

Step 6: Flood Your File With Positive Data

You stop the bleeding by eliminating errors, but to push your score into the elite 750+ range, you have to drown out previous mistakes with overwhelming positive data.

- Crush Your Credit Utilization: If you have a credit card with a $10,000 limit and an $8,000 balance, your utilization is a highly risky 80%. Aggressively attack those balances using the Debt Avalanche vs. Debt Snowball method. This is the fastest way to manually raise your score. To master this specific metric, read our complete breakdown on What Is Credit Utilization and Why Does It Matter?.

- Become an Authorized User: If a parent or spouse has a pristine credit history and an old credit card with a massive limit, ask them to add you as an Authorized User. They do not even need to hand you a physical card. Once added, their years of excellent payment history are instantly copied and pasted onto your credit report. If becoming an authorized user isn’t an option, opening a secured credit card is another effective way to build fresh positive payment history. Best Secured Credit Cards for Beginners in 2026 compares the top secured cards based on deposits, fees, graduation policies, and credit-building features.

- Keep Old Accounts Open: 15% of your FICO score is based on the average age of your credit history. Never close your oldest credit card, even if you do not use it anymore. Lock it in a drawer, put a small recurring subscription (like Netflix) on it, and set it to autopay.

Frequently Asked Questions (FAQs)

How often should I check my credit report? Many consumers review their reports at least once per year using AnnualCreditReport.com, while others monitor them more frequently when preparing for major loans like a mortgage or auto loan.

Does checking my own credit report hurt my score? No. Reviewing your own report is considered a “soft inquiry” and does absolutely no damage to your credit score.

How long does a dispute take? Credit bureaus generally have about 30 days to investigate your formal disputes, though specific timelines can vary depending on the complexity of the issue.

Can accurate negative information be removed? Generally, accurate information remains on your file until it legally ages off under applicable reporting rules (usually 7 years for late payments), although goodwill letters may occasionally help for single missed payments.

What credit score is considered good? Credit score ranges vary by model, but scores in the upper 600s to low 700s are generally considered good by most lenders, while scores 750 and above are considered excellent and secure the best interest rates.

References & Trusted Sources

To secure your official credit reports and verify your legal rights under the Fair Credit Reporting Act, rely on these authorized consumer resources:

- AnnualCreditReport.com (The Authorized Federal Portal)

- Consumer Financial Protection Bureau (CFPB) – Credit Reporting

- Federal Trade Commission (FTC) – Free Credit Reports

- Experian Consumer Education

- Equifax Credit Education Center

- TransUnion Credit Learning Center

The Bottom Line

You do not have to pay a dodgy “credit repair agency” $150 a month to fix your score. They are simply charging you a massive premium to execute the exact operational steps outlined in this article.

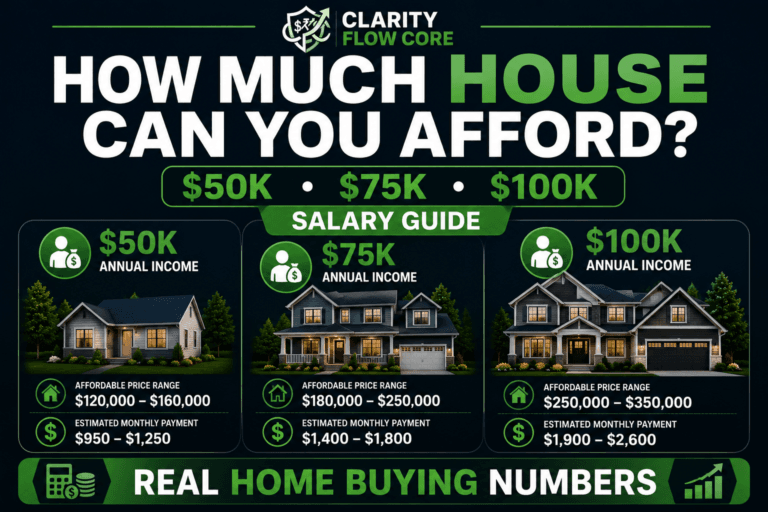

Auditing your financial reputation is something you can do yourself. If you are preparing to finance a car or use the First-Time Homebuyer Guide: How Much House Can You Really Afford? to prep for a mortgage, you must ensure your data is flawless.

Understanding how to read and fix your credit report requires a few hours of focused work, a highlighter, and some postage stamps. Download your free reports tonight, hunt down the clerical errors, mail your dispute letters, and lock in the very best interest rates for your financial future.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

3 Comments

Comments are closed.