HYSA vs. Money Market Account: What’s the Difference?

Before locking up your emergency fund, understanding the nuances of the HYSA vs Money Market dynamic will save you from missing out on higher yields. When deciding where to park your cash, the HYSA vs Money Market debate is the most critical choice you will make for your financial foundation.

The changes in the economy over the past few years have shown us that cash is not just “trash”—it is your best defense. The most important part of any good financial plan is to set up a shield that can cover three to six months’ worth of survival expenses. But where you keep that shield is more important than ever.

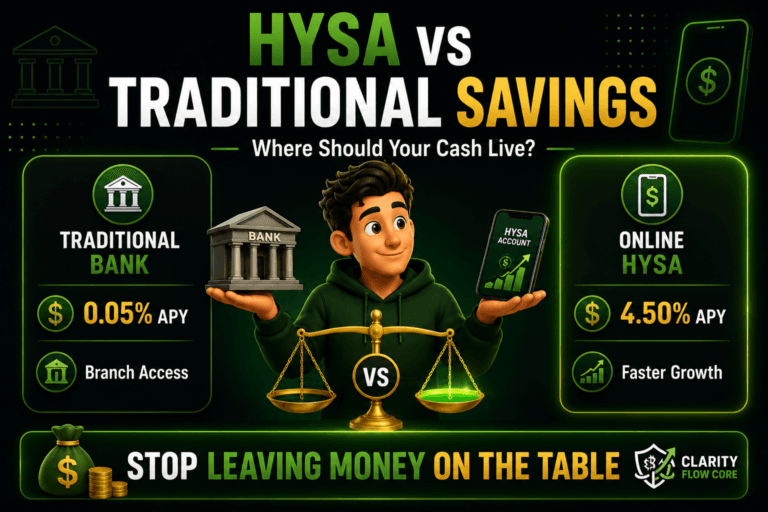

If you keep your emergency fund in a regular bank account that pays 0.01% APY (Annual Percentage Yield), you are actively losing buying power every single day. If you have $10,000 sitting in a big-brand bank, you are earning about $1.00 per year in interest. That isn’t a savings plan; it’s a donation to the bank. You need an account that delivers high rates without making it hard to get to your money in order to secure your core capital.

⚡ Quick Answer

- Choose an HYSA if you want the highest interest rates and do not need direct debit card or check-writing access to your cash.

- Choose a Money Market Account (MMA) if you want check-writing privileges, debit card access, and immediate liquidity for weekend emergencies.

- The Verdict: For most people building an emergency fund, an HYSA is the simpler and more cost-effective choice.

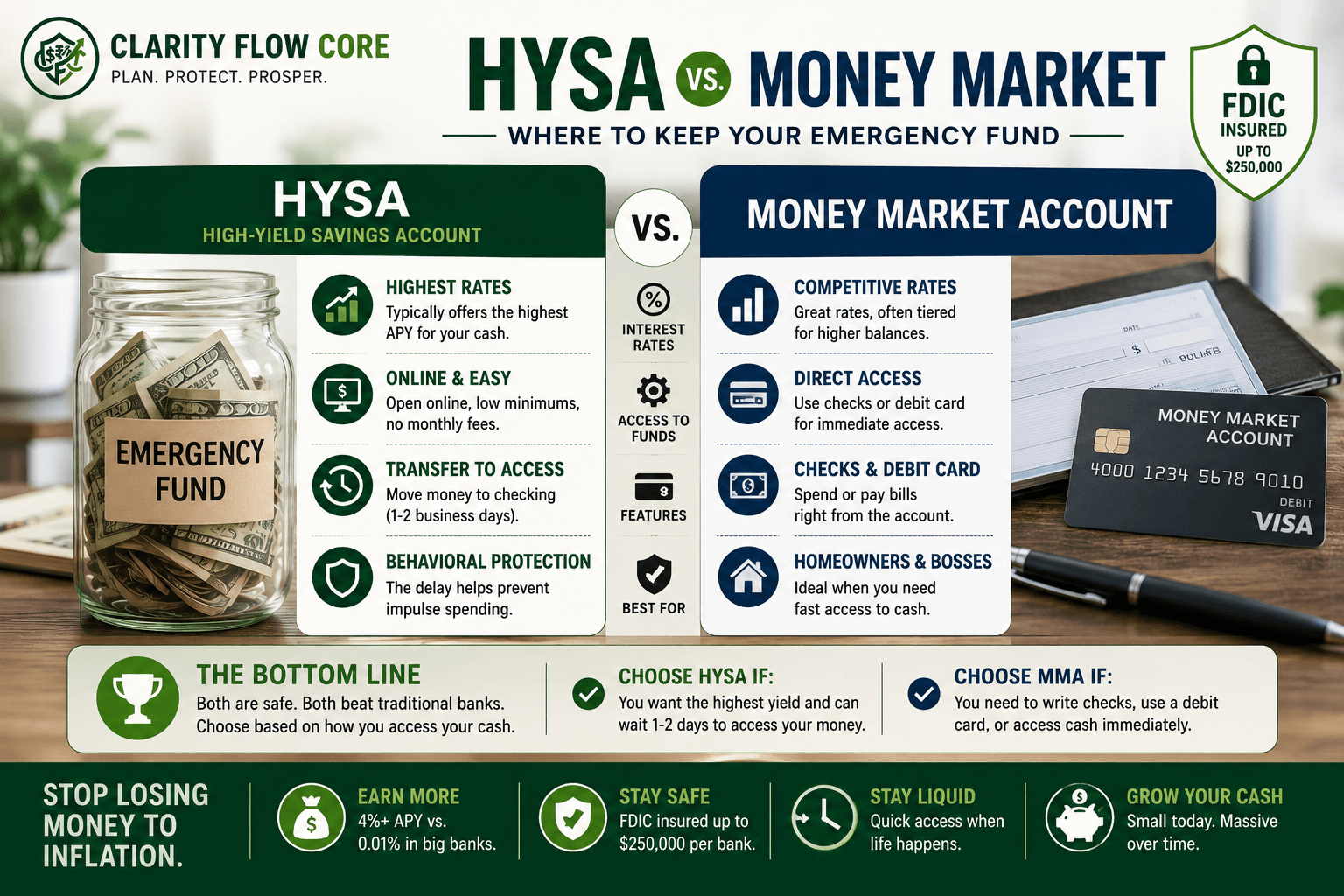

High-Yield Savings Accounts (HYSAs) and Money Market Accounts (MMAs) are the two biggest players in this field. They both offer competitive interest rates, safety, and liquidity, but they operate with different operational mechanics. Here is your complete guide to the HYSA vs Money Market landscape and how to choose the best place for your cash.

The Savings Landscape: Why Big Banks Fail Savers

The banking sector has become deeply divided. Traditional “brick-and-mortar” banks have incredibly high overhead. They have to pay for thousands of physical buildings, thousands of tellers, and massive marketing campaigns. To maintain their profit margins, they pay you near-zero interest.

Online-only banks and credit unions operate differently. Because they don’t have physical stores, they pass those savings directly to you. In the current HYSA vs Money Market market, online institutions often offer significantly higher rates than traditional banks.

If you have an emergency fund with $20,000, the difference is massive. In a 0.01% account, you earn $2. In a 4.50% high-yield account, you earn $900 per year. That is $75 a month in passive income just for moving your money to a better “bucket.”

High-Yield Savings Accounts (HYSA) Explained

An HYSA is exactly what it sounds like: a savings account that offers a much higher interest rate than a regular account.

How an HYSA Operates

When you put money into an HYSA, the bank lends that money to other customers at a higher rate. Because digital-first banks have reduced costs, they return a significant portion of that profit to you as yield. Interest is usually compounded daily and paid out monthly, creating a “snowball” effect on your balance.

The Benefits of the HYSA

- Top-Tier Yields: HYSAs often offer some of the highest rates available for liquid cash savings.

- Low Barriers: Most of the best HYSAs have a $0 minimum deposit requirement and $0 monthly maintenance fees.

- The Psychological Moat: These accounts are usually held at a different bank than your daily checking account. If it takes two business days to move the money, you are far less likely to spend your emergency fund on a non-emergency whim.

The Drawbacks of an HYSA

- Limited Access: Most HYSAs do not provide full checking-account style access such as debit cards or check writing. You must initiate an ACH transfer to your checking account to use the funds.

- Variable Rates: The APY is not locked in. If the Federal Reserve drops rates, your HYSA rate will drop shortly after.

Money Market Accounts (MMA) Explained

A Money Market Account is a hybrid financial product. It combines the interest-earning power of a savings account with the flexibility of a checking account.

How an MMA Operates

Banks often invest MMA funds into low-risk, short-term debt instruments like government bonds or certificates of deposit (CDs). This allows them to offer competitive rates while keeping the money liquid.

(Note: Do not confuse a Money Market Account—an FDIC-insured bank account—with a Money Market Fund, which is an investment product bought through a brokerage. In the HYSA vs Money Market comparison, the “Account” is the only one with government insurance).

The Benefits of an MMA

- Direct Access: Most MMAs come with a debit card and check-writing privileges.

- Tiered Rates: Many MMAs offer higher interest rates if you maintain a large balance (e.g., over $50,000).

- Immediate Liquidity: If your furnace dies on a Sunday night, you can write a check to the repairman immediately, skipping the two-day transfer window of an HYSA.

The Drawbacks of an MMA

- Minimum Balance Rules: MMAs often require a $2,500 to $5,000 initial deposit. If your balance drops below a certain threshold, you might be hit with a $15 to $25 monthly fee.

- Slightly Lower Base Rates: Because it costs the bank more to process checks and issue debit cards, the base APY on an MMA is often slightly lower than a pure HYSA.

Direct Comparison: HYSA vs Money Market

When evaluating the HYSA vs Money Market landscape, liquidity is just as important as the interest rate. To be certain which account fits your specific cash flow, let’s look at the operational data side-by-side:

| Feature | HYSA | Money Market Account |

| Primary Goal | Maximum yield; “Set it and forget it.” | Tactical flexibility with high yield. |

| Interest Rates | Highest available; flat across balances. | Competitive; often tiered by balance. |

| Check Writing | No. | Yes (often limited to 6/month). |

| Debit Card | No. | Yes. |

| Min. Balance | Usually $0. | Often $1,000 – $5,000. |

| Monthly Fees | Extremely Rare. | Common if balance is low. |

| Insurance | FDIC/NCUA up to $250,000. | FDIC/NCUA up to $250,000. |

Can You Use Both?

Many savers do not need to choose one account exclusively. A highly effective and common strategy is:

- Keep immediate, highly liquid emergency cash in a Money Market Account.

- Keep longer-term emergency reserves in a High-Yield Savings Account.

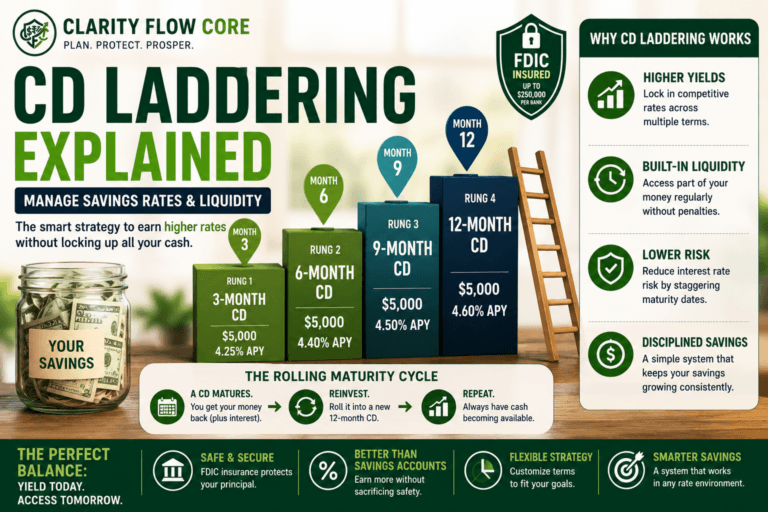

- Use CD ladders for money that will not be needed for several months.

This creates multiple layers of liquidity while maximizing your total interest income.

Which Account Wins the HYSA vs Money Market Debate?

The winner of the HYSA vs Money Market debate comes down to how you behave with money and what your specific risks are. One question will help you choose: Do you value a psychological barrier or immediate access?

Choose an HYSA if:

- You struggle with impulsive spending: If seeing a large balance in your banking app makes you want to spend it, the HYSA is for you. The 48-hour “lag time” required to move money to your checking account acts as a cooling-off period.

- You are just starting out: If you are building your first $1,000 starter fund (as recommended in our Emergency Fund Basics: How Much Cash Should You Keep?), an HYSA is the better choice because you won’t get hit with low-balance fees.

- You want simplicity: You don’t need a third debit card in your wallet. You just want the highest interest rate possible.

Choose an MMA if:

- You own a home or a business: In the HYSA vs Money Market world, homeowners often prefer the MMA. If a pipe bursts at 3:00 AM, you need to pay a plumber immediately. You cannot wait for an ACH transfer to clear on Tuesday morning.

- You have a massive cash pile: If you have $25,000 or more saved, you can easily meet the minimum balance requirements and may even unlock a “Premier” tier.

- You have high discipline: You can trust yourself to keep the MMA debit card in a safe place and only use it for true emergencies.

When the HYSA vs Money Market Strategy Backfires

The HYSA vs Money Market decision isn’t just about yield; it’s about avoiding operational traps. Here is exactly when these accounts can fail you:

1. The Transfer Lag Trap (HYSA)

If your entire life’s savings are in an HYSA and you have $0 in your checking account, you are in a dangerous position. If you have a true emergency on a Friday evening, the banks are closed. Your ACH transfer might not hit your spending account until the following Tuesday. If you choose an HYSA, you must understand How Much Should You Keep in Checking vs Savings? and keep at least $500 to $1,000 in your primary checking account as a “buffer.”

2. The Low-Balance Fee Trap (MMA)

Let’s say you have a $5,000 emergency fund in an MMA with a $2,500 minimum balance requirement. You have a $3,000 emergency and spend the money. Your balance is now $2,000. Because you are below the minimum, the bank starts charging you a $20 monthly fee. You are now being penalized for using your emergency fund. If you use an MMA, you must be prepared to replenish it or move the money to an HYSA if the balance stays low.

3. The “Regulation D” Confusion

In the HYSA vs Money Market world, people often worry about withdrawal limits. Federal “Regulation D” used to limit you to six withdrawals per month from savings and money market accounts. While the government suspended this rule during the pandemic, many banks still enforce their own version of it. If you treat these accounts like a checking account and make 15 transfers a month, the bank might close your account or convert it to a low-interest checking account without warning.

Your Action Plan: Executing the Strategy

Execution is everything once you have made your choice. In the HYSA vs Money Market world, inertia is your greatest enemy.

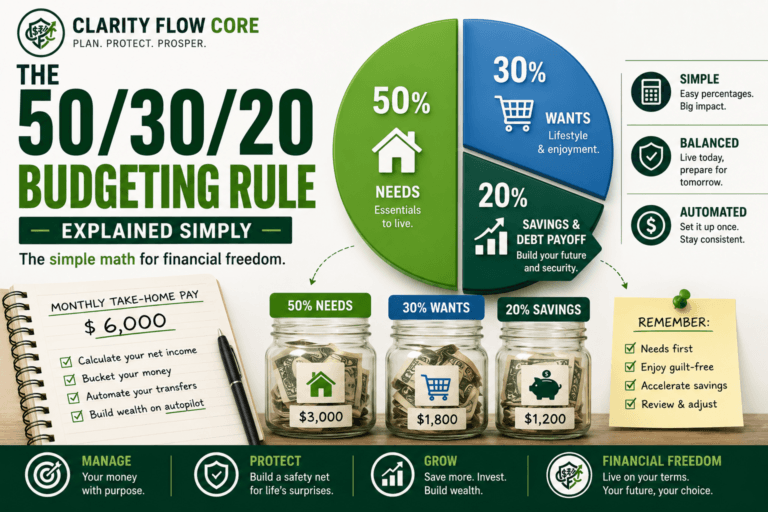

- Calculate Your Survival Number: Determine exactly how much cash you need to cover 6 months of expenses. (Use the 50/30/20 Budgeting Rule to find your exact needs).

- Audit Your Current Interest: Look at your last bank statement. If your interest earned is less than $10 for every $5,000 you have, you are losing the war against inflation.

- Check for FDIC/NCUA Insurance: Never put your emergency fund in a “fintech” app that isn’t a licensed bank or doesn’t have a partner bank for insurance. You need to know that if the company goes out of business, the government will return your money.

- Automate the Moat: Set up a Split Direct Deposit through your employer. Have $100 or $200 from every paycheck sent directly to your HYSA or MMA.

Frequently Asked Questions (FAQs)

Is a Money Market Account safer than an HYSA?

No. Both are generally equally safe when held at FDIC- or NCUA-insured institutions.

Can I lose money in a Money Market Account?

Not in a traditional FDIC-insured Money Market Account, though money market funds (investment products) are different and carry slight risk.

Which pays more: HYSA or MMA?

It depends on the institution and current market rates, though HYSAs generally offer slightly higher base APYs without strict minimum balance requirements.

Should my emergency fund be in an HYSA or MMA?

For most people, an HYSA is the simplest option. Those needing immediate, check-writing access for larger, sudden expenses may prefer an MMA.

Can I have both?

Yes. Many savers use both accounts for different purposes to maximize yield and liquidity simultaneously.

References & Trusted Sources

For official guidelines on deposit insurance and interest rate mechanics, consult these verified federal resources:

- FDIC – Deposit Insurance Coverage

- CFPB – Bank Accounts and Savings Accounts

- NCUA – Share Insurance Coverage

- Federal Reserve – Interest Rates and Savings

The Bottom Line

Regardless of which side of the HYSA vs Money Market decision you land on, moving your money out of a traditional 0.01% bank account is a massive victory.

Your emergency fund is not a collection of investments; it is insurance. Its main function is to be there when things go wrong, keeping you fully protected from high-interest credit card debt. Choosing the right side of the HYSA vs Money Market debate ensures that your money is working just as hard for you as you did to earn it.

The most important first step is to move the money. Whether you pick the high-yield simplicity of an HYSA, the tactical flexibility of an MMA, or lock in long-term rates by understanding CD Laddering, get your basic emergency fund out of the big banks and into an account that actually pays you to save.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

7 Comments

Comments are closed.