Best Secured Credit Cards for Beginners in 2026

You applied for a credit card and got denied. The letter from the bank says you lack a credit history. But how do you establish a credit history if no one will give you a credit card in the first place?

It is the ultimate financial catch-22, and it frustrates millions of beginners every single year. You know you are responsible with money, but the algorithms at the major credit bureaus do not know you yet.

Breaking out of this cycle is entirely possible. You do not need to rely on predatory lenders, sketchy payday loans, or expensive financial products to prove you are reliable. You just need the right tool for the job: a secured credit card.

⚡ Quick Answer

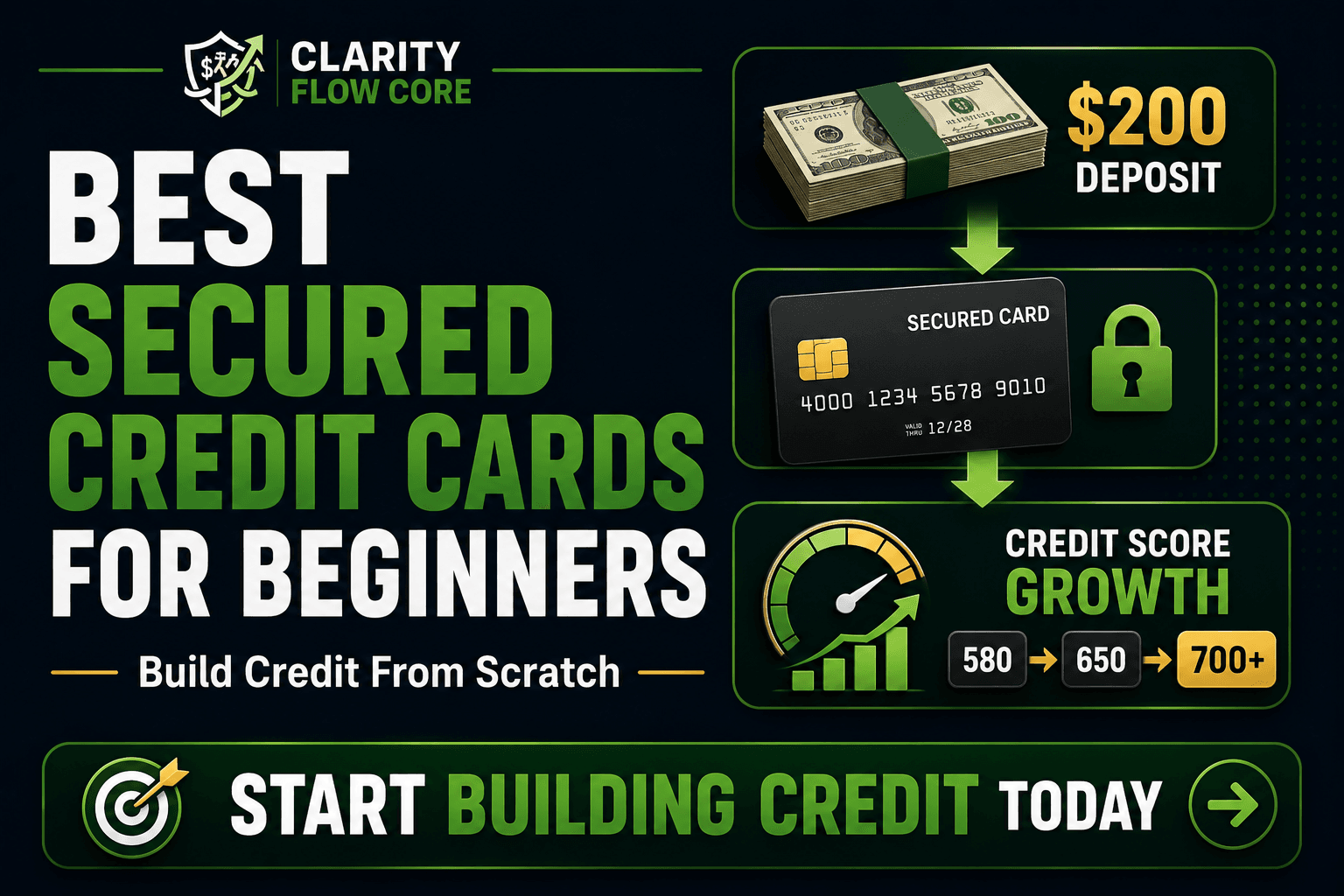

A secured credit card helps build or rebuild credit by requiring a refundable security deposit that becomes your credit limit. The best secured credit cards for beginners report to all three credit bureaus, have low fees, and offer a path to upgrade to an unsecured card after consistent on-time payments.

To help you skip the research phase, here is a quick comparison of the top secured cards available this year:

| Card | Minimum Deposit | Annual Fee | Reports to Bureaus | Graduation Available |

| Discover it® Secured | $200 | $0 | Yes | Yes |

| Capital One Platinum Secured | $49 – $200 | $0 | Yes | Yes |

| Chime Secured Visa® | Varies | $0 | Yes | N/A (No Credit Check) |

| OpenSky® Secured Visa® | $200 | $35 | Yes | Yes (No Credit Check) |

In this guide, we will explain exactly how secured credit cards work, review our top picks in detail, and show you exactly how to use them to build an excellent credit score from scratch.

What is a Secured Credit Card?

Before you apply for a card, you must understand the mechanics of how it actually works. A secured credit card looks, feels, and swipes exactly like a standard credit card. The cashier at the grocery store will not know the difference. The difference happens behind the scenes.

When you open a traditional (unsecured) credit card, the bank takes a massive risk. They hand you a $5,000 credit limit based purely on their trust that you will pay them back. If you have no credit score, they have no reason to trust you.

With a secured credit card, you provide the trust in the form of a cash security deposit.

If you give the bank a $200 deposit, they give you a credit card with a $200 limit. The bank holds your cash in a secure reserve account. If you ever stop paying your credit card bill, the bank simply takes your deposit to cover their losses. Because their risk is essentially zero, their approval rates are incredibly high.

Who Should Get a Secured Card?

A secured card is a highly specific financial tool. It is not for earning luxury travel points; it is for foundational credit repair and building. A secured card may be right for you if:

- You have no credit history. (You are a student, a recent immigrant, or have simply avoided debt your whole life).

- You were denied a traditional card. (If you are wondering what standard cards require, read our guide on What Credit Score Is Needed for Each Type of Credit Card?).

- You are rebuilding after financial mistakes. (Such as a past bankruptcy, foreclosure, or multiple accounts in collections).

- You want to establish credit before applying for a mortgage. (Having an active, positive revolving credit line is essential for underwriting).

Building strong credit before applying for a home loan can significantly improve your borrowing options. What Credit Score Do You Need to Buy a House in 2026? explains the score ranges lenders typically expect and how they affect mortgage approval.

Secured Cards vs. Prepaid Debit Cards

A common point of confusion for beginners is the difference between a secured card and a prepaid debit card (like a Visa gift card you buy at the grocery store). They are completely different products.

When you use a prepaid debit card, you are spending the actual money you loaded onto the card. Once the balance hits zero, the card stops working. Most importantly, prepaid debit cards do not report to the credit bureaus. They do absolutely nothing to build your credit score.

When you use a secured credit card, your $200 deposit sits untouched in a vault. When you swipe the card, you are borrowing the bank’s money. At the end of the month, you receive a bill, and you must pay that bill from your regular checking account. Because you are actively borrowing and repaying debt, the bank reports this responsible behavior to the credit bureaus, which builds your score.

The Best Secured Credit Cards for Beginners in 2026

The secured credit card market has improved dramatically in recent years. In the past, secured cards were plagued by predatory annual fees and hidden charges. Today, major lenders offer excellent starter cards with real rewards.

Here are the four best options available for beginners in 2026.

1. Discover it® Secured Credit Card (Best Overall)

The Discover it® Secured card consistently ranks as the absolute best starter card on the market. It offers perks that rival traditional unsecured cards, making it an incredibly powerful tool for beginners.

- Minimum Deposit: $200

- Annual Fee: $0

- Rewards: You earn 2% cash back at gas stations and restaurants (on up to $1,000 in combined purchases each quarter), and 1% cash back on everything else. Furthermore, Discover will automatically match all the cash back you earned at the end of your first year.

- The Graduation Path: Starting at month seven, Discover will automatically review your account every month to see if you have managed your credit responsibly. If you have, they will automatically “graduate” you to an unsecured card and mail you a check to refund your initial deposit.

2. Capital One Platinum Secured Credit Card (Best for Low Deposits)

If saving a $200 deposit feels like a massive financial hurdle right now, Capital One offers a unique solution designed for tight budgets.

- Minimum Deposit: $49, $99, or $200 (depending on your initial credit check).

- Annual Fee: $0

- Rewards: None. This is a bare-bones card built purely for credit building.

- The Benefit: Regardless of whether your required deposit is $49 or $99, Capital One will give you an initial credit line of $200. This is one of the only cards on the market that will give you a credit limit higher than your cash deposit. Furthermore, Capital One automatically reviews your account for a potential credit line increase after just six months of responsible use.

3. The Secured Chime Visa® Credit Card (Best for No Credit Check)

Chime is a financial technology company that has completely revolutionized how beginners build credit. If you have been denied by other banks, the Chime card is an excellent alternative.

- Minimum Deposit: Varies based on how much money you move to your Chime account.

- Annual Fee: $0

- Rewards: None.

- The Benefit: Chime does not run a hard credit check when you apply. There is no minimum security deposit requirement like the standard $200 at traditional banks. Instead, the card is linked to a Chime checking account. The money you transfer into your “Credit Builder” account becomes your credit limit. You can safely build your credit using the money you already have on hand to pay your daily bills.

4. OpenSky® Secured Visa® Credit Card (Best for Past Financial Hardship)

If you are actively trying to rebuild your financial life after a bankruptcy, foreclosure, or massive debt default, OpenSky offers a highly accessible path forward.

- Minimum Deposit: $200

- Annual Fee: $35

- Rewards: None.

- The Benefit: OpenSky does absolutely no credit check. None. They do not care about your past financial mistakes. As long as you can provide the $200 security deposit, you are almost guaranteed approval. While this card does carry a $35 annual fee, it is a necessary stepping stone for consumers who have been blacklisted by major banks.

How Secured Cards Actually Build Your Credit

Getting the card is only step one. How you use the card dictates whether your credit score goes up or plummets.

A Realistic Credit Building Timeline

Building credit is a marathon, not a sprint. If you open a card today and use it perfectly, here is a realistic timeline of what to expect:

| Time | Possible Result |

| Month 1 | Account opens, initial deposit locked. |

| Month 3 | First positive reporting hits the credit bureaus. |

| Month 6 | Official FICO score generated (often high 600s/low 700s). |

| Month 8 | Graduation review (deposit potentially refunded). |

| Month 12 | Eligible to apply for better, unsecured rewards cards. |

Once you’ve graduated to an unsecured card, Cash Back vs Travel Credit Cards: Which Should You Choose? can help you decide which type of rewards card best fits your spending habits.

If you notice different credit scores across various apps, FICO vs VantageScore: Why Credit Scores Differ Between Apps explains why those numbers rarely match and which score lenders actually use.

If you’re wondering how long the overall credit-building journey usually takes, How Long Does It Take to Build Credit From Scratch? walks through realistic milestones and expectations.

Mastering Payment History (35% of Your Score)

Your track record of paying bills on time is the single largest factor in your credit score. If you pay your secured credit card bill perfectly on time every single month, the issuer sends a positive report to Equifax, Experian, and TransUnion. A single late payment, however, will destroy your progress. You must set up automatic payments the day you activate the card.

If you ever miss a payment, How Long Do Late Payments Stay On Your Credit Report? explains how long the damage lasts and how to rebuild your credit afterward.

Managing Credit Utilization (30% of Your Score)

This is where beginners constantly stumble. Credit utilization is the ratio between how much debt you owe and your total available credit limit.

If you’re unfamiliar with how credit utilization is calculated or why lenders pay so much attention to it, What Is Credit Utilization — And Why Does It Matter? explains the concept in detail with beginner-friendly examples.

Because secured credit cards have tiny limits (often just $200), it is incredibly easy to accidentally ruin your utilization. If you have a $200 limit and you buy $180 worth of groceries, your utilization is 90%. The credit bureaus view anyone utilizing more than 30% of their limit as a massive financial risk, and your score will drop accordingly.

To build your score quickly, keep your utilization exceptionally low. If your limit is $200, never let your statement balance exceed $20. If you need help managing this metric across multiple cards, map out a strategy using our Credit Utilization Calculator & Recovery System.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationWhile many people focus on staying below 30%, the reality is more nuanced. The 30% Credit Utilization Myth: What Actually Matters? explains how utilization is actually evaluated by modern scoring models.

How to Graduate to an Unsecured Card

Your ultimate goal is not to use a secured credit card forever. Your goal is to graduate.

Graduation occurs when your bank reviews your account, decides you are no longer a risk, upgrades your account to a standard unsecured credit card, and refunds your security deposit.

Here is the exact playbook to force your bank to upgrade you as fast as possible:

- Never Miss a Payment: One late payment resets the graduation clock. Even a single missed payment can damage months of progress. What Happens If You Miss a Credit Card Payment? explains the fees, credit score impact, and recovery timeline.

- Keep Balances Tiny: Spend no more than 10% of your limit each month.

- Do Not Overdraw: Never attempt a purchase that is larger than your credit limit.

- Wait Six to Eight Months: Most major banks begin their automatic account reviews at the six-month mark.

Once you graduate, your credit limit will typically increase significantly (e.g., jumping from $200 to $1,500), which further improves your credit utilization and boosts your score. If you want to learn how to keep pushing that limit higher, read our guide on How to Increase Your Credit Limit Without Hurting Your Credit Score. You can also model how a larger credit limit will positively impact your long-term numbers using our Credit Score Simulator & Improvement Planner.

Test Your Credit Score Before Making Big Moves

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our simulator.

Launch Credit SimulatorCommon Mistakes with Secured Cards

Using a secured credit card requires discipline. Avoid these frequent beginner traps to ensure your credit score grows smoothly.

Many of these beginner mistakes appear in other areas of credit management as well. 10 Credit Score Mistakes That Can Cost You 100+ Points covers additional habits that can quietly lower your score.

Mistake 1: Treating It Like a Debit Card

Your deposit is collateral, not cash to be spent. When your bill arrives, you must have actual cash in your checking account to pay the balance. If you assume the bank will just “take it out of the deposit,” your account will be reported as delinquent.

Mistake 2: Carrying a Balance to “Build Credit”

There is a massive myth in personal finance that you must carry a balance and pay interest to build your credit score. This is entirely false. Paying interest does nothing to boost your score; it only enriches the bank. Pay your entire statement balance in full every single month.

Mistake 3: Closing the Card Immediately After Getting a Better One

Once your score hits 700, you will suddenly start receiving mail offers for premium rewards cards. When you open your first “real” credit card, do not immediately close your old secured card. The length of your credit history accounts for 15% of your FICO score. If the secured card has graduated and has no annual fee, throw it in a drawer, put a small recurring $5 subscription on it, and set it to auto-pay. Keep that foundational account alive.

After graduating from a secured card, your next step is choosing your first traditional card wisely. Best Credit Cards for Beginners: What Actually Matters explains which features deserve your attention beyond flashy rewards.

As your credit profile grows, you may wonder how many cards you should ultimately keep. How Many Credit Cards Should You Have for the Best Credit Score? explains how multiple accounts affect your long-term credit health.

Mistake 4: Using Your Emergency Savings for the Deposit

Do not pull money out of your emergency reserves to fund your security deposit. That deposit will be locked away in a vault for six to twelve months. Only use disposable cash for your deposit. Your actual emergency reserves must remain fully liquid and accessible. Unsure what your true emergency target should be? Run a diagnostic with our Advanced Emergency Fund Analyzer.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetAction Plan: Get Your First Card Today

Reading about credit scores will not change your financial profile. Taking action will. Follow these exact steps today to get your system up and running.

- Check Your Cash Flow: Before taking on new financial responsibilities, ensure your monthly budget is balanced. Use the Financial Freedom Planner to verify you have the free cash flow to pay a credit card bill every month.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom Plan- Save the Deposit: Set aside $200 in a separate checking account. Do not use your rent money.

- Apply for the Right Card: Go online and apply for the Discover it® Secured card or the Capital One Platinum Secured card.

- Set the Subscription Strategy: When the physical card arrives in the mail, log into your Netflix or Spotify account and change the billing method to your new secured card.

- Automate the Payment: Log into your new credit card portal and set up Auto-Pay for the “Full Statement Balance.”

- Cut the Card Up (Optional): If you do not trust yourself, take scissors and cut the physical plastic card in half. Your Netflix bill will still process digitally every month, your auto-pay will clear it, and your credit score will grow on pure autopilot without the temptation to impulse shop.

Frequently Asked Questions

Do secured cards build credit as fast as regular cards?

Yes. Credit bureaus do not care whether a card is secured or unsecured. A $200 secured card builds payment history exactly the same way a $10,000 premium travel card does. The algorithm only cares that you are paying your bill on time.

When will I get my security deposit back?

You get your deposit back when you either close the account in good standing or when the bank decides to graduate your card to an unsecured product.

Can I be denied for a secured credit card?

Yes. While approval odds are exceptionally high, banks can still deny you if you do not have a verifiable source of income, if you have a recent active bankruptcy, or if you apply for too many credit cards in a single month.

Do secured credit cards check your credit?

Most major banks (like Discover and Capital One) will perform a “hard pull” on your credit report when you apply, which will temporarily drop your score by a few points. However, cards like the Chime Credit Builder or OpenSky Visa do not require a credit check.

Will my credit limit ever increase?

Yes. With cards like the Capital One Platinum Secured, the bank will automatically review your account after six months and may grant you a higher credit limit without asking for more deposit money.

Can I use a secured credit card to rent a car or book a hotel?

Technically yes, but it is highly discouraged. Rental car agencies and hotels place “holds” on your card for incidentals (often $100 to $250). If your card only has a $200 limit, that hold will instantly max out your card, temporarily ruining your credit utilization.

References and Resources

To ensure you have the most accurate and up-to-date consumer protection information, we highly recommend exploring these official financial resources:

- Consumer Financial Protection Bureau (CFPB): The CFPB offers exceptional, unbiased guidance on how secured cards work and what your rights are regarding security deposits. Visit the CFPB guide on building credit.

- FICO: Since FICO is the exact mathematical model used to determine your creditworthiness, reviewing their official breakdowns of score components is mandatory for serious planners. Review FICO score factors.

- Consumer.gov: Managed by the FTC, this site provides straightforward, plain-language advice on recovering from bad credit safely. Explore Consumer.gov credit building basics.

- Federal Deposit Insurance Corporation (FDIC): When choosing a bank for your secured card, the FDIC provides excellent educational materials on avoiding predatory lending practices. Explore FDIC Consumer Assistance.

Conclusion

Building a credit score from scratch can feel like an impossible puzzle. When every lender demands a history of good credit before offering you a loan, getting your foot in the door is the hardest part.

A secured credit card completely bypasses that barrier. By offering a cash deposit, you take the risk away from the bank, forcing them to give you the opportunity you deserve. Yes, putting down a $200 deposit for a $200 credit limit might not feel glamorous. It does not come with airport lounge access or massive sign-up bonuses. But it is the ultimate foundational tool.

Treat your new secured credit card with absolute respect. Keep your utilization tiny, automate your payments, and be patient. Within six to twelve months, you will watch your credit score climb from zero into the 700s. From there, the entire financial world opens up to you. Start small, stay disciplined, and take control of your financial reputation today.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.